AiPrise

5 min read

What FinCEN’s Proposed Rule Really Means for AI in KYB and AML

Key Takeaways

On April 7, 2026, FinCEN issued a Notice of Proposed Rulemaking that would significantly reform AML and CFT program requirements under the Bank Secrecy Act. Comments are due by June 9, 2026, and FinCEN says the proposal is intended to fundamentally reform how financial institutions design and run these programs.

That alone makes it worth paying attention to. But the more interesting question is what this proposal signals in practice.

For years, a lot of AML and KYB work has been built around process discipline: collect the right files, run the right checks, document the steps, and make sure nothing obvious is missing. That approach is understandable. It feels safe. But it has also produced a lot of manual work, a lot of noise, and not always the best outcomes. FinCEN’s proposal pushes the conversation toward something different: whether a program is actually effective, whether resources are focused on real risk, and whether institutions are using better tools to get there. FinCEN’s own fact sheet also says the Director would consider whether a bank is using innovative tools such as artificial intelligence that demonstrate AML and CFT program effectiveness.

That is why this proposal matters beyond the legal update itself.

It is one of the clearest signals yet that manual, checkbox driven compliance is getting harder to defend as the default.

The old compliance bargain is breaking

For a long time, the bargain was simple. If your team followed the process, documented the work, and kept the machinery moving, you could at least argue that you were being prudent.

But anyone who has sat inside a real compliance function knows how flimsy that bargain has become. You can have a process heavy program and still drown in false positives. You can have analysts manually stitching together registries, PDFs, sanctions hits, and notes, and still miss the cases that matter. You can have more controls on paper and worse outcomes in practice. FinCEN is now pushing that contradiction into the open by centering effectiveness, risk based design, and useful outcomes for law enforcement and national security.

The proposal says AML and CFT programs should be effective, risk based, and reasonably designed. It also makes clear that institutions should direct more attention and resources toward higher risk customers and activities, not spread the same level of manual effort across everything.

That is not a small philosophical tweak. It changes the economics of compliance. If the standard is effectiveness, then preserving manual process just because it feels familiar is no longer the conservative option. In many cases, it is the weaker one.

FinCEN did not “approve AI.” It did something more important.

This is the line that matters most for the market. FinCEN’s fact sheet says that, when deciding whether to pursue an enforcement action or significant supervisory action, or when reviewing a proposed supervisory action by a federal banking supervisor, the Director would consider whether the bank is employing innovative tools such as artificial intelligence that demonstrate the effectiveness of its AML and CFT program.

That is a huge signal.

FinCEN is not saying every AI product is a good idea. It is not saying innovation gets a free pass. It is saying something more important: if innovative tools improve program effectiveness, that counts in your favor.

For years, many compliance teams have treated AI as something they might experiment with only after they were sure regulators would not look at it suspiciously. This proposal flips that posture. The question is no longer just “is AI risky?” The more relevant question is “if AI can make your program more effective, more consistent, and more risk focused, why are you still relying on slower manual workflows by default?”

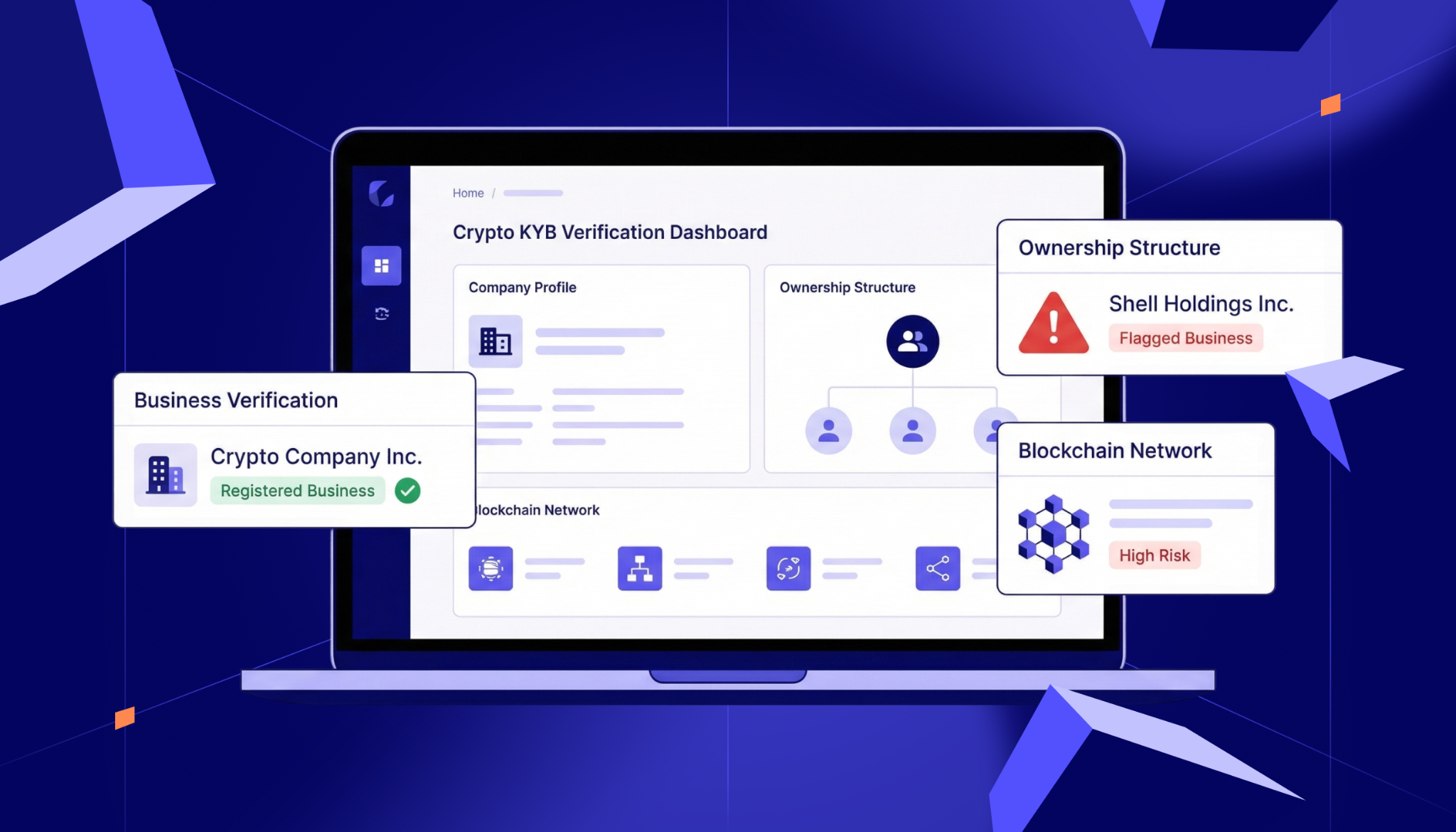

This is especially important for KYB

Most commentary on this proposal will stay at the AML program level. That makes sense. But there is a practical angle that deserves more attention: this is also a KYB story.

Business verification is still where an enormous amount of compliance time gets burned. Registry data is fragmented. Ownership information varies across jurisdictions. Website reviews are manual. Documents move back and forth. Analysts spend too much time gathering facts before they can even start judging risk.

That is exactly the kind of workflow an effectiveness based regime should force teams to rethink.

If your KYB process still depends on people jumping between vendors, pulling corporate records one by one, reading documents manually, checking websites by hand, and stitching everything together in case notes, that is not conservative. It is inefficient, inconsistent, and harder to defend.

Better KYB is not just onboarding hygiene. It is part of building a more effective compliance program overall. Weak business verification means risk enters the system earlier, and downstream AML controls are left to clean up the mess at higher cost. FinCEN’s shift toward risk based allocation and effective outcomes makes that harder to ignore.

The real winner here is not “AI.” It is context.

A lot of vendors will read this proposal and start shouting that FinCEN “blessed AI.” That is lazy.

What FinCEN is really rewarding is effective innovation. And effective innovation in compliance does not come from bolting a chatbot onto a brittle workflow.

It comes from systems that actually improve decision quality. Systems that can reason across registries, documents, websites, ownership structures, sanctions hits, and policy thresholds. Systems that can distinguish between noise and risk. Systems that leave behind a record a human can review, understand, and defend.

That is why simple point solutions are going to look weaker in this environment. If one tool screens names, another reads documents, another checks registries, and your analyst is still the one stitching the whole thing together in their head, then the intelligence is still manual. You have not built an effective program. You have built expensive workflow fragmentation.

The firms that benefit most from this shift will be the ones that stop thinking in features and start thinking in systems.

The proposal also lowers the political cost of modernizing

There is another important point buried in the proposal. FinCEN’s fact sheet says that, if a bank has established its AML and CFT program under the proposed rule, FinCEN generally would not take an enforcement action, and generally would not take a significant supervisory action, unless the bank has a significant or systemic failure to maintain that program. The proposal is explicitly trying to focus attention on significant or systemic failures, rather than isolated or technical deficiencies.

That is not immunity. And it is not a free pass for sloppy implementation.

But it is a meaningful signal that FinCEN is trying to distinguish between a genuinely broken program and a program that is well designed but not flawless in every tiny respect. For compliance leaders, that should reduce some of the fear that any use of new technology automatically creates enforcement risk. The standard being proposed is not perfection. It is effectiveness, sound design, and responsible implementation.

What smart compliance teams should do now

First, audit where your current workflow is still manual for the wrong reasons. Not where human judgment is genuinely needed, but where people are simply acting as glue between systems.

Second, pressure test your current vendors against an outcomes standard. Do they help your team make better, more consistent, more explainable decisions, or do they just create one more review step.

Third, evaluate AI systems the way FinCEN is implicitly telling you to evaluate them: by effectiveness. Can they reduce false positives. Can they direct effort toward higher risk activity. Can they improve consistency. Can they leave behind a clear trail of how the decision was made. FinCEN’s proposal is explicit that programs should be effective, risk based, and updated as risks evolve.

If the answer is no, then the problem is not that regulators are not ready for AI. The problem is that the tool is not very good.

The direction of travel is now obvious

The safest possible reading of FinCEN’s proposal is still a big deal. FinCEN is telling the market that effective, risk based programs matter more than box checking. It is saying that institutions should put more resources on higher risk customers and activities. It is saying that innovative tools such as AI can strengthen a program’s position when they demonstrably improve effectiveness. And it is trying to focus enforcement on significant or systemic failure, not isolated technical issues.

That is not a message to slow down.

It is a message to modernize properly.

So here is the uncomfortable conclusion:

If your compliance program still depends on analysts stitching together registries, PDFs, and screening results by hand, you are not being cautious. You are building a weaker program at a higher cost.

The future of compliance is not more paperwork. It is better outcomes.

And increasingly, that means AI.

You might want to read these...

AiPrise

KYB Compliance: 2026 Regulations You Should Know About

As organizations expand globally and face tighter regulations, adherence to Know Your Business (KYB) standards has become one of the most critical compliance layers for fintech, online marketplaces, and other companies that need to verify business customers before letting them perform financial transactions.

.jpeg)

.jpg)

.jpg)

.jpeg)

%20Can%20Improve%20Your%20Compliance%20Strategy.png)

.png)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately