AiPrise

13 min read

October 9, 2025

Anti Money Laundering and Procurement Risk in Insurance Sector

Key Takeaways

The global insurance industry collected EUR 6.2 trillion in premiums across life, property & casualty, and health insurance in 2024. This massive financial flow, combined with complex product structures and cross-border transactions, creates significant vulnerabilities that criminals exploit for money laundering purposes.

As regulatory scrutiny intensifies, insurance companies must strengthen their anti-money laundering (AML) frameworks to protect against sophisticated financial crimes while maintaining operational efficiency.

We'll explore common money laundering tactics used in insurance, procurement risks, and how insurers can strengthen their anti-money laundering frameworks to stay compliant and secure.

Key Takeaways

- Anti-money laundering (AML) is crucial in the insurance sector to prevent money laundering through products like life insurance and annuities.

- Money laundering tactics in insurance include early policy surrender, overpayment and refund schemes, ownership transfers, and using shell companies to launder illicit funds.

- Procurement processes in insurance can be exposed to AML risks through insufficient vendor due diligence, complex ownership structures, and third-party intermediary risks.

- Global AML regulations like FATF recommendations, EU Anti-Money Laundering Directives, and the U.S. Bank Secrecy Act require insurers to conduct thorough KYC/KYB checks and ongoing monitoring to mitigate risks.

- Insurers need global compliance solutions, regular audits, and ongoing training to stay compliant with AML regulations across different regions.

Understanding Money Laundering Risks in Insurance

The insurance industry may not seem like an obvious target for financial crime. But in reality, it offers a discreet and complex structure that money launderers exploit.

Why Insurance Is a Target?

Insurance products, particularly life insurance and annuities, are attractive to money launderers because they offer large transaction capabilities, flexibility, and long-term financial structures that allow criminals to move illicit funds under the radar. These features provide a discreet way to store and move money over extended periods, making detection more difficult.

For example, with life insurance policies, criminals can buy policies using large sums of illicit money and then either cash out early or take loans against the policy later on, giving the appearance of legitimate financial transactions.

Annuities offer another avenue, as they are long-term contracts that promise regular, often sizable, payouts. By purchasing an annuity with illicit funds, criminals can disguise the origin of the money and receive clean, regular income over time, which is harder to trace.

The complexity and longevity of these products make it easier to avoid detection, and the ability to transfer ownership or sell policies on secondary markets further complicates monitoring.

Common Money Laundering Tactics in Insurance

Criminals use several methods to clean illegal money through insurance products:

These tactics are often layered together to avoid raising suspicion. Without strong monitoring systems, many insurers fail to detect the abuse until it's too late.

Do you know that procurement within the company creates further vulnerabilities? Let’s understand.

Suggested Read: Methods for Effective Money Laundering Detection

How Procurement Exposes Insurers to AML Breaches

Procurement in insurance isn’t just about purchasing office supplies or IT systems. It includes outsourcing claims management, compliance services, data storage, and onboarding third-party agents and brokers. Each of these activities introduces new risks.

Key risks include:

- Insufficient vendor due diligence before onboarding.

- Lack of transparency in vendor ownership structures (often hiding shell companies).

- Poor monitoring of third-party transactions and claims processing.

Example: Shell Vendor Risk

An insurer may contract a vendor to verify user documents or process international claims. If the vendor is a shell company used to clean illicit funds, the insurer unknowingly becomes part of the laundering process.

These procurement risks go beyond financial loss; they directly impact regulatory compliance and brand trust. Therefore, it’s essential to understand the major procurement risks thoroughly.

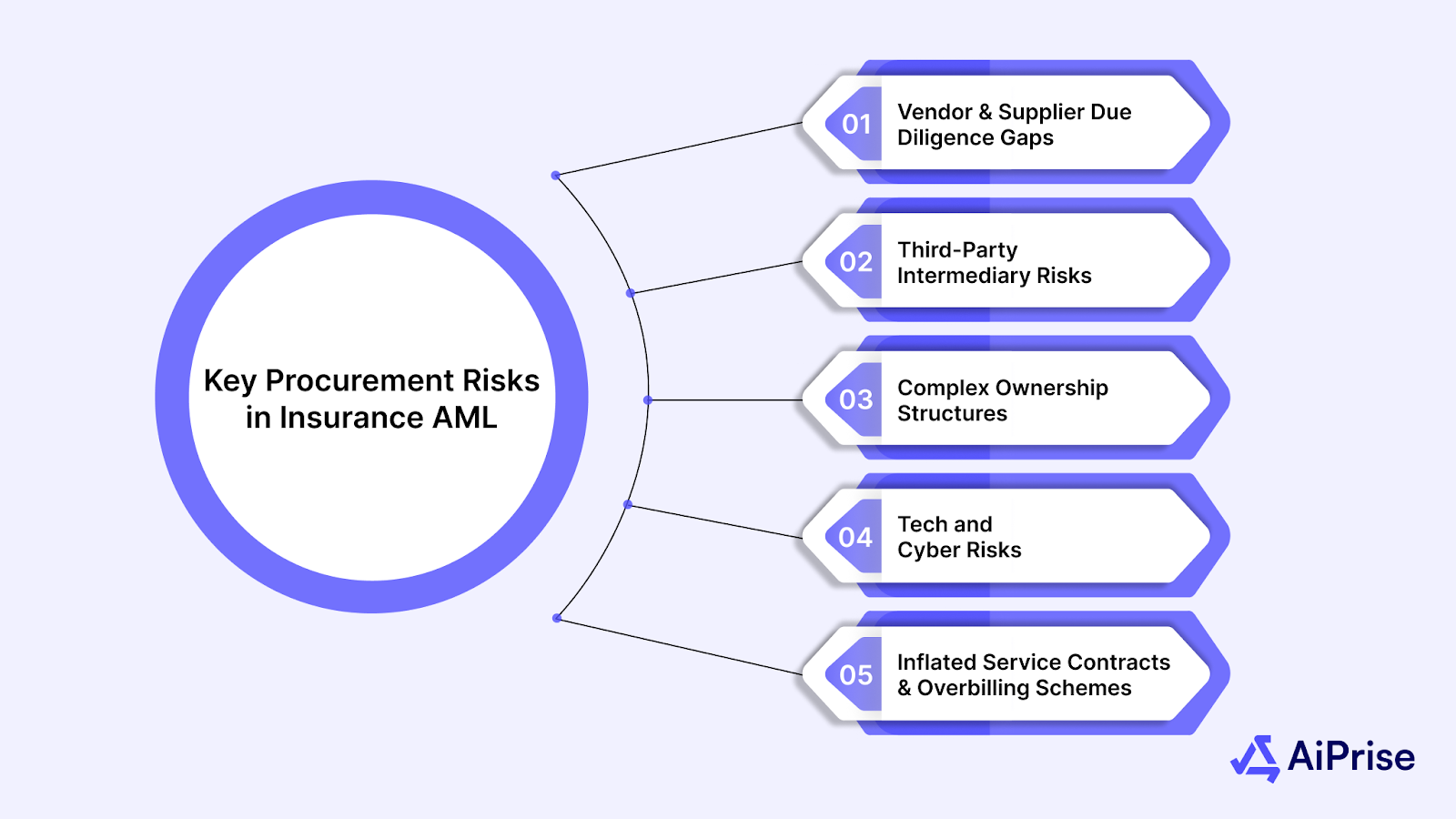

Key Procurement Risks in Insurance AML

Procurement in insurance presents unique money laundering vulnerabilities that extend far beyond traditional customer-facing risks. Insurance companies must manage complex vendor relationships, third-party partnerships, and supply chain dependencies that can serve as entry points for illicit financial activities.

Understanding these procurement-specific risks is essential for building comprehensive AML defense strategies.

Vendor and Supplier Due Diligence Gaps

Insurance companies work with thousands of vendors, from technology providers to claims adjusters. Each relationship presents potential AML risks if proper due diligence isn't conducted.

Criminal organizations often establish shell companies to bid on insurance contracts, using these legitimate business relationships to launder money through inflated invoices or fraudulent services.

Common Vendor-Related Red Flags:

- Companies with unclear ownership structures or frequent leadership changes.

- Vendors operating from high-risk jurisdictions without a clear business justification.

- Unusual payment methods or requests for advance payments to offshore accounts.

- Lack of physical business presence or legitimate business operations.

- Inconsistent business registration information across different databases.

The procurement process becomes particularly vulnerable when companies prioritize cost savings over comprehensive background checks. This approach can lead to partnerships with entities that have hidden beneficial ownership structures or connections to individuals who are sanctioned.

Third-Party Intermediary Risks

Insurance brokers, agents, and other intermediaries handle significant transaction volumes and maintain direct customer relationships. These intermediaries can become unwitting facilitators of money laundering if they lack proper AML training or oversight mechanisms.

High-Risk Intermediary Scenarios:

- Brokers handling unusually large or complex transactions without a clear business rationale.

- Agents operating in multiple jurisdictions with varying regulatory oversight.

- Distribution partners with inadequate AML controls or training programs.

- Technology service providers with access to sensitive customer and transaction data.

The challenge intensifies in global operations where local intermediaries may operate under different regulatory frameworks. Without standardized AML procedures across all jurisdictions, insurance companies create compliance gaps that sophisticated criminals can exploit.

Complex Ownership Structures and Shell Companies

One of the most significant procurement risks involves vendors with opaque ownership structures designed to hide beneficial owners. Criminal organizations frequently use layered corporate structures spanning multiple jurisdictions to obscure their involvement in legitimate business relationships.

Warning Signs of Complex Ownership Structures:

Technology and Cybersecurity Vulnerabilities

Modern insurance operations rely heavily on third-party technology providers, creating additional AML risks through potential system compromises or data manipulation. Criminal organizations may target technology vendors to gain access to insurance systems for money laundering purposes.

Technology-Related Procurement Risks:

- Cloud service providers with inadequate security controls.

- Software vendors from high-risk jurisdictions with potential backdoor access.

- Payment processing partners with weak transaction monitoring.

- Data analytics providers with access to sensitive customer information.

Inflated Service Contracts and Overbilling Schemes

Procurement relationships provide opportunities for money laundering through systematic overbilling, inflated service contracts, or payments for services never rendered. These schemes often involve legitimate vendors that criminal organizations may compromise.

Common Overbilling Indicators:

- Service rates are significantly above market averages.

- Vague or poorly defined service descriptions.

- Frequent contract modifications increaseincreasing the scope and cost.

- Lack of competitive bidding processes.

- Payment terms favoring the vendor.

Effective procurement risk management requires a balance between operational efficiency and comprehensive compliance measures.

Key Global Regulations for Anti-Money Laundering in Insurance

Insurance companies must comply with key global AML regulations, such as the FATF Recommendations, EU Anti-Money Laundering Directives, and the U.S. Bank Secrecy Act. These regulations require thorough KYC and KYB processes, as well as continuous monitoring to detect suspicious activities.

Adhering to these regulations helps insurers avoid legal penalties, reputational damage, and ensures operational integrity, building trust with both regulators and customers.

1. FATF (Financial Action Task Force) Recommendations

The FATF is an intergovernmental body that sets global standards for combating money laundering. Its 40 recommendations form the foundation for AML laws in many countries, including those that govern the insurance sector. For insurers, these recommendations stress the importance of:

- Conducting thorough due diligence on customers, vendors, and partners.

- Ongoing monitoring of transactions and relationships to detect suspicious activities.

- Establishing internal controls and compliance measures to safeguard against money laundering.

2. European Union’s Anti-Money Laundering Directives

The 5th Anti-Money Laundering Directive (5AMLD) in the European Union places greater emphasis on customer due diligence and transparency, including enhanced checks on high-risk vendors and transactions.

Insurers must comply with these directives to avoid penalties and reputational harm, particularly when sourcing services from vendors in EU member states.

3. US Bank Secrecy Act (BSA) and Patriot Act

In the United States, the Bank Secrecy Act (BSA) and the Patriot Act impose stringent AML requirements on financial institutions, including insurance companies. These regulations require insurers to:

- Establish AML compliance programs.

- Report suspicious activities.

- Implement KYC and KYB measures.

Remember, failure to adhere to these regulations can lead to hefty fines and a loss of business licenses.

In addition to global frameworks, insurers must also consider local regulatory requirements that apply to their specific jurisdictions.

For example, Asia-Pacific and Middle Eastern countries have developed their own AML rules, which vary in scope and enforcement. This often means that insurers operating in multiple countries must adapt their compliance practices to meet a range of regulatory standards.

Also read: Anti Money Laundering (AML) Law: A Complete Guide

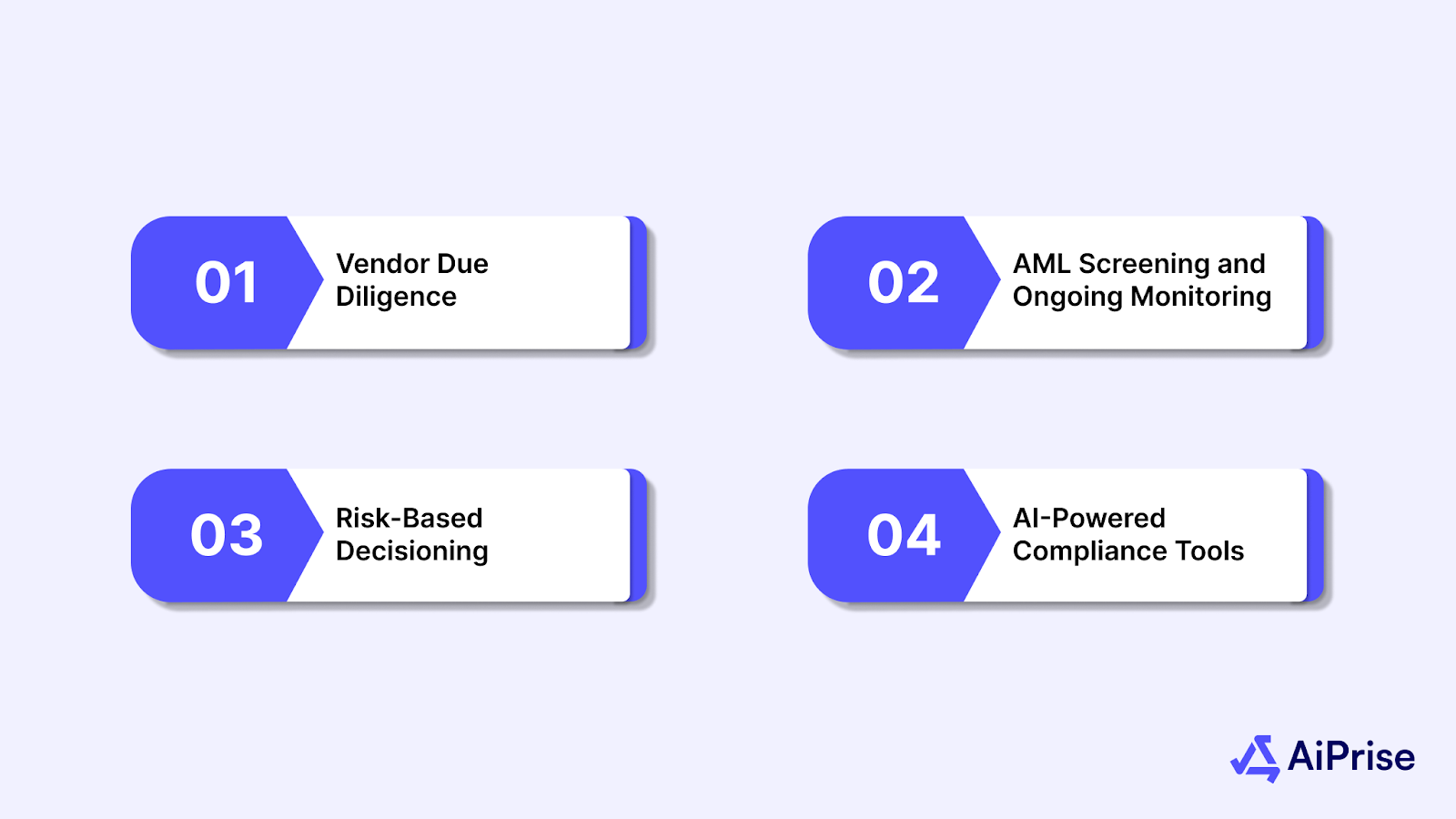

Key Strategies for Mitigating Anti-Money Laundering Procurement Risks

By implementing strong AML practices across the procurement process, insurers can better protect themselves from potential threats.

Below are some essential strategies to consider.

Vendor Due Diligence

The first and most critical step in mitigating AML procurement risk is conducting thorough vendor due diligence. This means assessing the background, financial health, and compliance status of potential vendors before entering into any contractual relationship. Proper vendor verification helps ensure that the parties involved are legitimate and have a clean regulatory history.

Key aspects of vendor due diligence include:

- Financial and Compliance History: Conduct background checks to ensure the vendor has no ties to financial crimes or money laundering activities.

- AML Policy and Practices: Confirm that vendors have their own robust AML policies in place and are compliant with international regulations. Vendors should be able to demonstrate their adherence to KYC and KYB standards.

- Risk Assessments: Assess whether the vendor’s operations or market position pose any heightened risks (e.g., if they are based in a high-risk jurisdiction).

AML Screening and Ongoing Monitoring

Once a vendor is onboarded, the work doesn’t stop there. Ongoing monitoring is essential to ensure that a vendor remains compliant with AML regulations over time. This can be done by screening vendors and suppliers against global watchlists, politically exposed persons (PEPs), and adverse media.

Insurance companies should consider using advanced tools that can:

- Regularly Screen Vendors: Continuous screening ensures that any changes in the vendor’s status—such as involvement in illegal activities—are immediately detected.

- Automated Alerts: Set up automated alerts to notify compliance teams if a vendor appears on a watchlist or is linked to suspicious activities.

By keeping a close eye on vendor activity and conducting ongoing screenings, insurers can detect issues before they escalate into more significant problems.

Risk-Based Decisioning

Risk-based decisioning allows insurance companies to apply varying levels of scrutiny to vendors based on their risk profile. Not all vendors represent the same level of risk, and this approach ensures that resources are allocated efficiently to where they are needed most.

For instance, high-risk vendors, such as those located in jurisdictions known for money laundering activities, should undergo more rigorous screening, while lower-risk vendors may be subject to lighter checks.

The customizable rule engine in AiPrise’s platform, for example, allows businesses to tailor their decision-making process based on specific criteria and weightage according to their unique risk tolerance.

This strategy helps insurers:

- Focus resources on high-risk vendors.

- Automate risk assessments for improved efficiency.

- Reduce operational costs associated with unnecessary checks.

AI-Powered Compliance Tools

In an increasingly digital world, leveraging AI-powered compliance tools can significantly improve the efficiency and accuracy of the procurement process. AiPrise’s Compliance Co-Pilot, for instance, is an AI-driven tool that helps insurers quickly identify potential risks and flag non-compliant vendors.

AI tools can also assist with:

- Automated Document Analysis: AI can quickly analyze complex documents (such as incorporation certificates, financial statements, and legal contracts) to detect discrepancies or red flags.

- Enhanced Due Diligence (EDD): AI can automate the Enhanced Due Diligence process, generating comprehensive EDD reports that provide insurers with deeper insights into vendor risk.

By automating repetitive tasks and improving decision-making accuracy, AI-powered tools help insurance companies stay compliant without overwhelming compliance teams.

By integrating these strategies into the procurement process, insurers can dramatically reduce the risk of engaging with non-compliant vendors and avoid exposure to money laundering activities.

Excellence in AML compliance requires commitment from leadership, investment in appropriate technology, and ongoing dedication to program improvement.

Challenges and Future Outlook

The segment of AML compliance in insurance continues to evolve rapidly, driven by technological advancement, regulatory changes, and complicated criminal tactics. Insurance companies need to advance in this dynamic environment while maintaining robust defenses against money laundering risks in their procurement and operational activities.

Balancing Compliance and Customer Experience

One of the primary challenges facing insurance companies is maintaining rigorous AML standards without creating friction for legitimate customers and business partners. Excessive verification requirements can delay policy issuance, complicate claims processing, and frustrate procurement activities.

The solution lies in implementing intelligent systems that can differentiate between high-risk and low-risk relationships, applying appropriate levels of scrutiny without imposing unnecessary burdens on routine transactions. This risk-calibrated approach maintains security while preserving operational efficiency.

Emerging Technologies and New Risks

The insurance industry continues to evolve with the adoption of new technologies such as blockchain, Internet of Things (IoT), and digital currencies. Each innovation brings potential benefits but also introduces new vulnerabilities that criminals may exploit for money laundering purposes.

Insurance companies must stay ahead of these developments by updating their AML frameworks to address emerging risks. This proactive stance requires collaboration with technology providers, regulatory bodies, and industry peers to share threat intelligence and best practices.

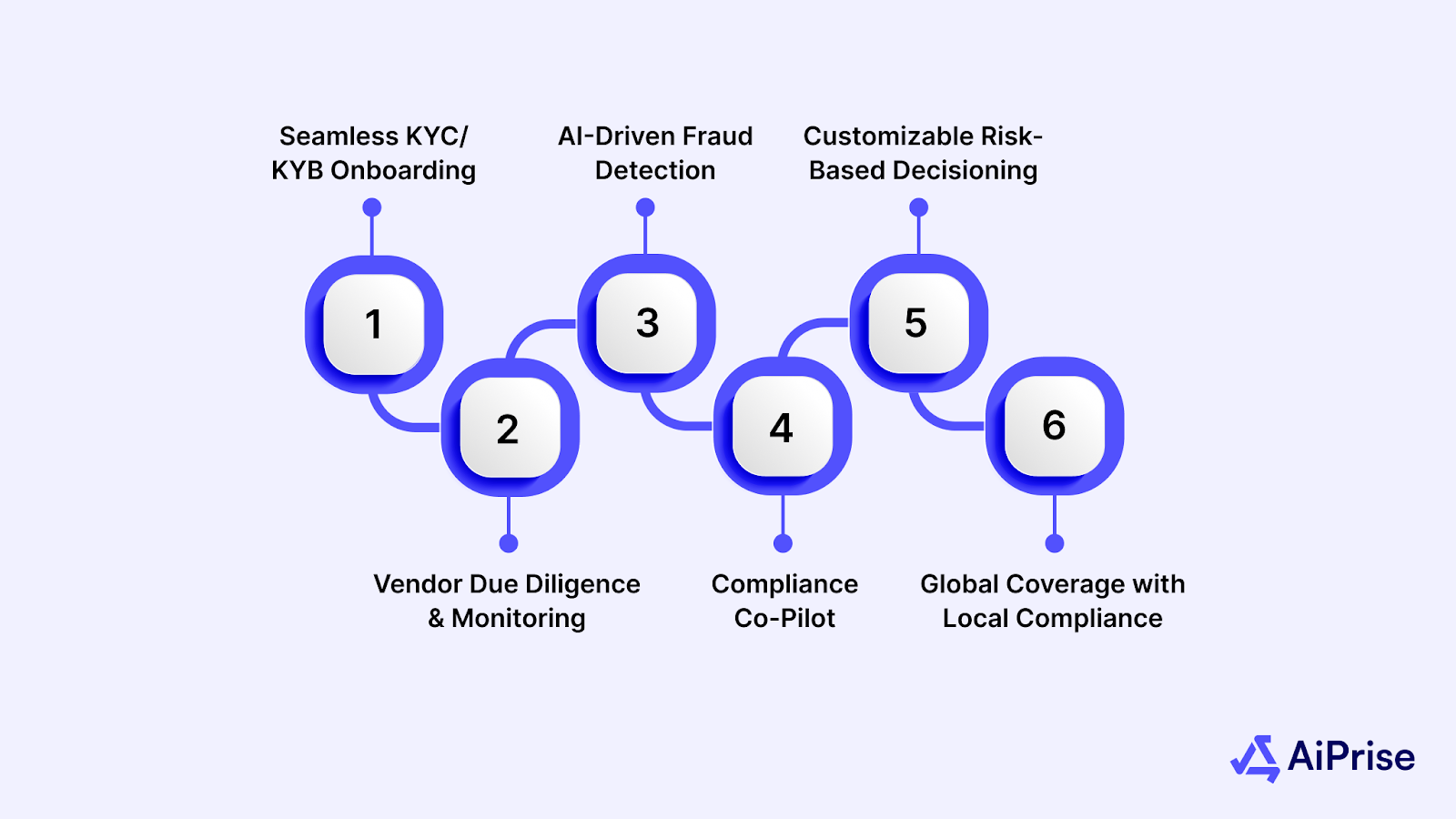

How AiPrise Helps with Anti-Money Laundering Compliance in Insurance

AiPrise provides insurance companies with advanced tools to streamline AML compliance while ensuring operational efficiency and reducing procurement risks.

- Seamless KYC/KYB Onboarding: AiPrise offers AI-powered identity verification for quick and reliable KYC and KYB checks, ensuring compliance during onboarding.

- Vendor Due Diligence & Monitoring: Continuous screening of vendors and suppliers helps identify AML risks in real-time, enabling insurance companies to manage procurement with confidence.

- AI-Driven Fraud Detection: AiPrise uses AI to detect suspicious transactions, flagging potential AML risks and enabling quick response to fraudulent activities.

- Compliance Co-Pilot: AiPrise’s AI-powered assistant automates document verification and reporting, improving efficiency and reducing errors in compliance processes.

- Customizable Risk-Based Decisioning: The flexible rule engine allows insurers to tailor AML checks based on their unique risk profiles, ensuring targeted and effective compliance management.

- Global Coverage with Local Compliance: AiPrise ensures compliance across 200+ countries, adapting to local AML regulations like 5AMLD and the U.S. Bank Secrecy Act.

AiPrise helps streamline compliance processes, providing a practical and adaptable solution that ensures both regulatory adherence and operational efficiency.

Conclusion

Anti-money laundering compliance in the insurance sector demands a comprehensive approach that addresses procurement risks while maintaining operational excellence. As regulations change and criminal methods become more complex, insurance companies must strengthen their compliance frameworks with the right technology and expertise.

The key to success lies in implementing risk-based approaches that use automation for efficiency while maintaining human oversight for complex decisions. Companies that embrace this balanced strategy will build competitive advantages through enhanced risk management capabilities.

Are you ready to build the competitive edge of security?

Book a Demo today to discover how advanced anti-money laundering solutions can streamline your processes while maintaining the highest security standards.

Frequently Asked Questions (FAQs)

1. What is anti-money laundering (AML) in the insurance sector?

AML in the insurance sector involves regulations and practices designed to prevent criminals from using insurance products to launder illicit funds. It includes measures like KYC and KYB to verify the identity of customers and vendors.

2. How does procurement risk contribute to money laundering in insurance?

Procurement risk arises when insurance companies work with vendors who fail to meet AML standards, potentially allowing criminals to launder money through fraudulent business relationships.

3. Why is the insurance industry vulnerable to money laundering?

The insurance industry is vulnerable due to large financial transactions, cross-border operations, and complex products that criminals can exploit to conceal illicit funds, especially through life insurance and annuities.

4. What are Ponzi schemes and how do they relate to money laundering in insurance?

Ponzi schemes are fraudulent investment schemes that pay returns to earlier investors using money from new investors. In insurance, criminals may use policies to disguise the flow of illicit money within these schemes.

5. How can AI and automation help with AML compliance in the insurance sector?

AI and automation streamline the verification and monitoring process, quickly identifying suspicious activities and ensuring compliance with AML regulations across large datasets, improving efficiency and accuracy.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately