AiPrise

12 min read

September 26, 2025

Fraud and Money Laundering: Key Differences and Connections

Key Takeaways

In 2023, global financial crime reached unprecedented levels, with a verified $3.1 trillion in illicit funds flowing through the financial system. Within this staggering total, fraud scams and bank fraud schemes alone accounted for $485.6 billion in losses globally.

As the financial world continues to digitize, fraud and money laundering schemes are becoming more sophisticated, leveraging technology like AI and deepfakes to bypass traditional security measures. This shift makes it harder for businesses to detect and prevent financial crimes.

In this blog, we'll explore the key differences between fraud and money laundering, their connection, and how businesses can adapt their strategies to combat these threats effectively.

Key Takeaways:

- Fraud is a criminal act where individuals intentionally deceive others for personal gain, using false information or misrepresentation to obtain money or assets.

- Money laundering involves disguising the illicit origin of funds, often obtained through criminal activities, to make them appear legitimate and reintroduce them into the financial system.

- Fraud and money laundering are closely connected; fraud often generates illicit funds that are then laundered to conceal their criminal origins.

- The key differences between fraud and money laundering lie in their intent, process, and legal implications, although they often overlap in real-world scenarios.

- Effective prevention strategies require proactive measures such as real-time monitoring, predictive analytics, AI-based fraud detection, and blockchain technology.

What is Fraud?

Fraud is the intentional deception of someone for personal or financial gain. It involves the use of false information or misrepresentation to achieve a desired outcome, typically at the expense of another party. Fraud can occur in various forms, from identity theft to insurance fraud, and it can target individuals, businesses, or even entire organizations.

Fraud is a criminal offense because it involves deliberate dishonesty or deceit to obtain something of value, such as money, goods, or services. Fraud patterns include those of physical settings, like a store or a bank, or they can occur in digital environments, such as online scams or phishing attacks.

Types of Fraud:

- Financial Fraud: This involves the illegal acquisition of money through deceptive means, such as embezzlement or fraudulent transactions.

- Identity Theft: Fraudsters steal personal information (e.g., social security numbers, credit card details) to impersonate someone and gain access to their assets.

- Insurance Fraud: This occurs when individuals submit false claims to insurance companies to receive financial compensation.

- Tax Fraud: Falsifying information to reduce tax liability or evade tax payments.

- Credit Card Fraud: Unauthorized use of another person’s credit card details to make purchases.

How Fraud Occurs:

- Misrepresentation: Fraudsters provide false information to deceive others.

- Deception for Financial Gain: The primary goal is to gain money, goods, or services without the rightful owner’s consent.

- Targeting Vulnerabilities: Fraudsters often exploit weaknesses in systems, like poor security measures or insufficient verification processes, to carry out their schemes.

Fraud impacts both individuals and businesses, leading to financial losses, reputational damage, and legal consequences. Understanding the nature of fraud is critical to preventing it, particularly in industries where financial transactions are prevalent.

Now that we understand fraud, let’s explore money laundering and how it differs from fraud in its goals and processes.

What is Money Laundering?

Money laundering is the act of concealing the origins of illegally obtained money, typically through criminal activities, to make it appear as if it comes from legitimate sources. The goal of money laundering is to transform "dirty" money—gained through activities like drug trafficking, embezzlement, or fraud—into "clean" money that can be freely used in the financial system without raising suspicion.

Money laundering is a multi-step process that allows criminals to integrate illicit funds into the legal economy. It usually involves a combination of various financial transactions and manipulations designed to obscure the true origins of the money.

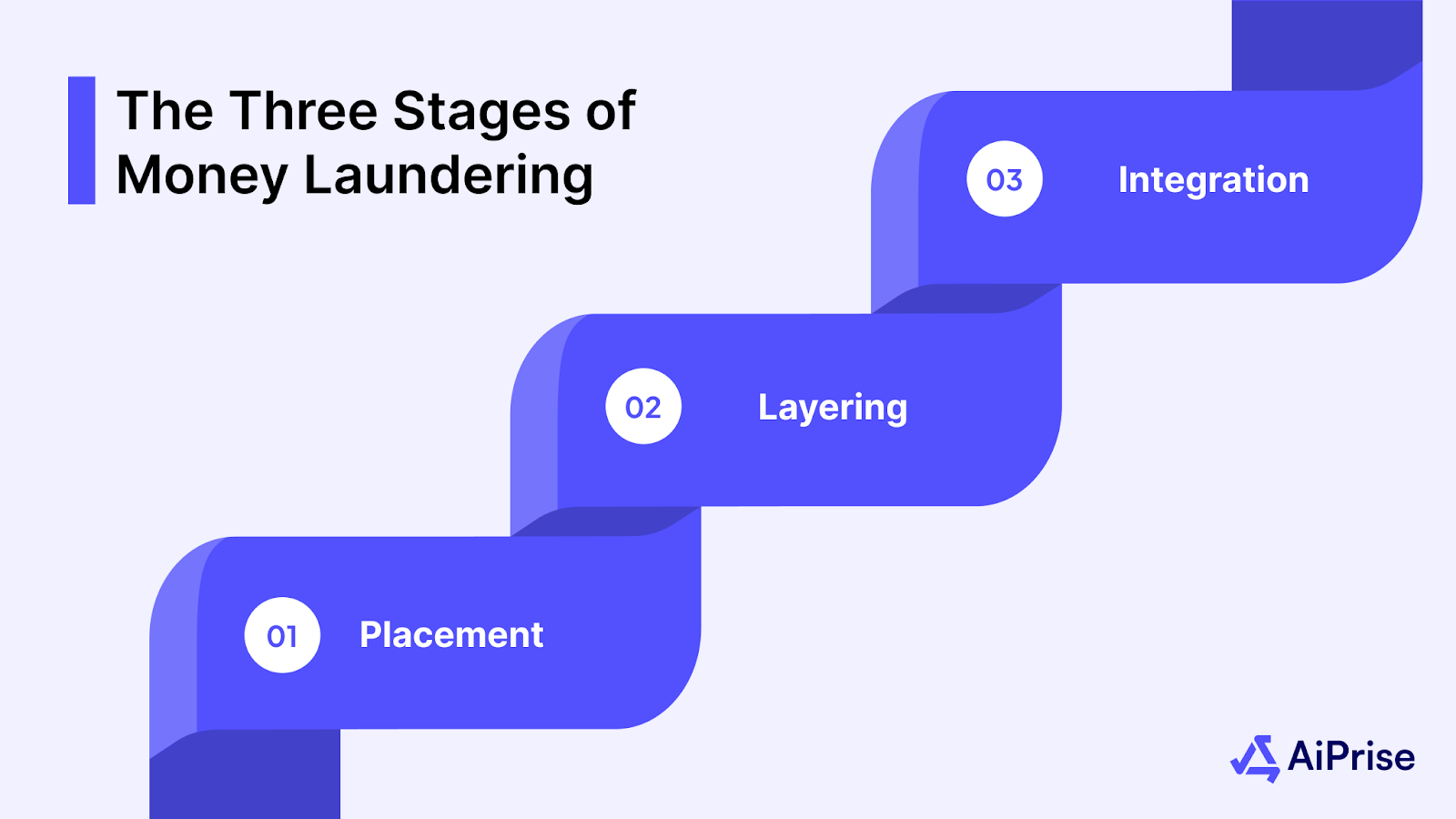

The Three Stages of Money Laundering:

- Placement: This is the first stage where illicit funds enter the financial system. It often involves depositing large amounts of cash into banks, purchasing assets, or exchanging currencies. This stage is intended to distance the money from its criminal origins.

- Layering: In this stage, the funds are moved through complex layers of transactions to obscure their source. This can involve transferring money across multiple accounts, converting the funds into different assets (like stocks or bonds), or purchasing goods and services. The aim is to make tracing the origin of the money more difficult.

- Integration: At this final stage, the laundered money is integrated into the legitimate economy. It is often used for investments, buying properties, or purchasing luxury goods. The funds appear legitimate and can be freely spent or reinvested without attracting attention.

Money laundering sabotages and facilitates further criminal activity, and can have devastating economic consequences for governments and businesses. Therefore, regulatory bodies around the world have strict laws and measures in place to prevent, detect, and punish money laundering activities.

Now that we’ve defined fraud and money laundering, let's take a look at their key differences, how they function separately, and the ways they overlap in the criminal world.

Key Differences Between Fraud and Money Laundering

While fraud and money laundering are often associated with financial crimes, they are distinct in their purpose, process, and legal implications. Understanding the key differences between the two is essential for businesses, regulators, and law enforcement agencies to effectively combat these crimes.

Understanding the differences between fraud and money laundering is key, but knowing how they connect can help businesses and regulators take more effective action. Let’s now explore how these two crimes often overlap in real-world scenarios.

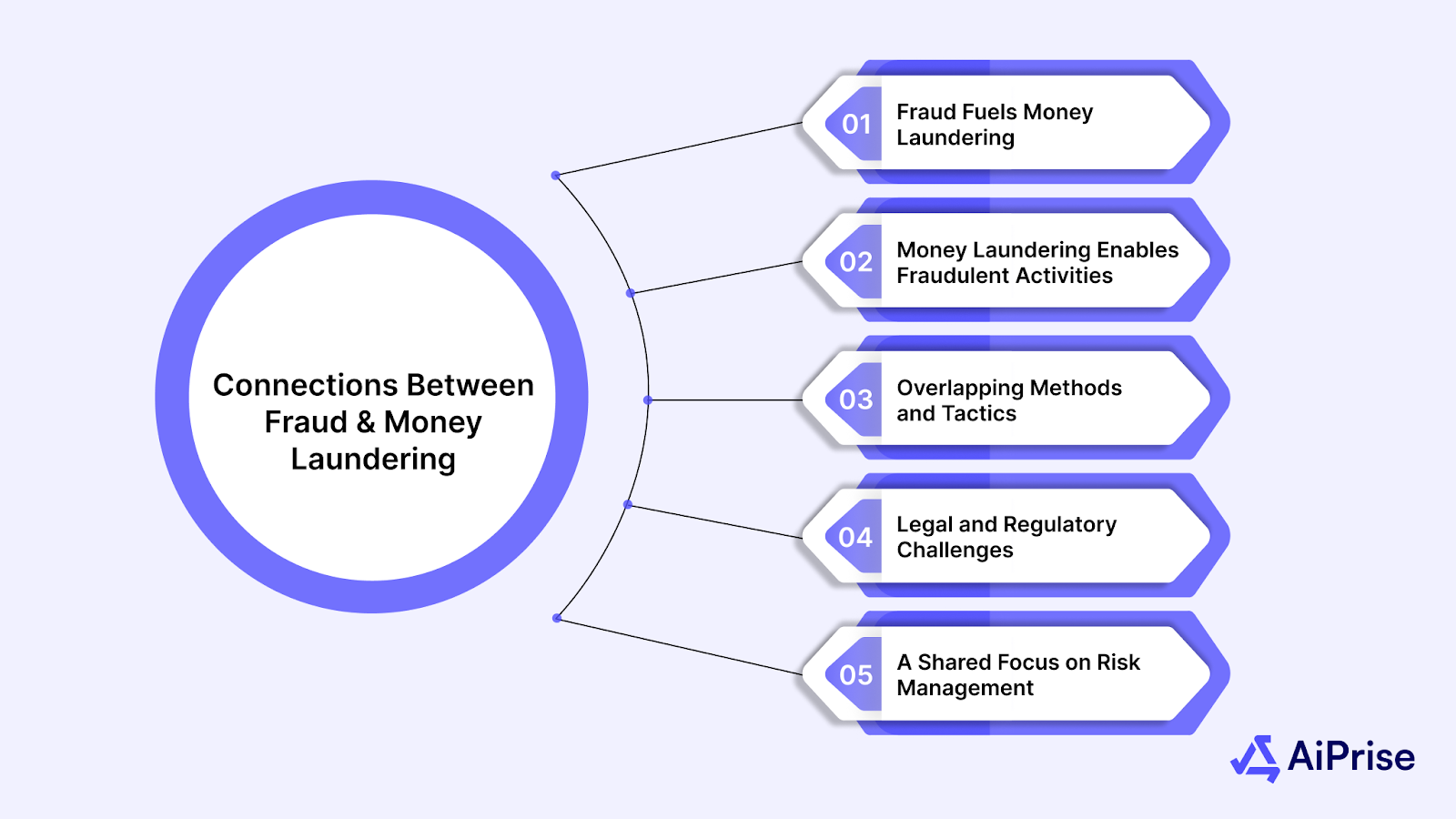

Connections Between Fraud and Money Laundering

Fraud and money laundering, though distinct in nature, are often closely linked. In many cases, fraud can act as the initial crime that leads to money laundering, and vice versa. Understanding how these two crimes intersect is crucial for businesses, regulators, and financial institutions to prevent and detect these activities.

1. Fraud Generates the Funds for Money Laundering

Fraudulent activities, such as identity theft, embezzlement, or insurance fraud, often generate illicit money. Once the fraudulent funds are obtained, they need to be "cleaned" or laundered to make them appear legitimate. Money laundering serves as a means to disguise the origin of these funds, allowing criminals to integrate the money into the legal economy.

- Example: A fraudster embezzles funds from a company and then uses those funds to buy high-value items or invest in a business, effectively laundering the stolen money.

2. Money Laundering Facilitates Fraudulent Activities

On the other hand, money laundering can provide the financial resources needed for committing fraud. By "cleaning" illicit funds, criminals can finance their fraudulent schemes or use the laundered money to support further illegal activities. The integration of dirty money into the legitimate economy allows criminals to have access to resources without suspicion.

- Example: After laundering stolen money, criminals might use it to fund fraudulent business ventures or scams, such as fake investment schemes.

3. Overlapping Methods and Tactics

Both fraud and money laundering involve deceitful practices, but they are carried out at different stages of the criminal activity:

- Fraud: Deception occurs at the initial stage to gain illicit funds.

- Money Laundering: Deception occurs at later stages, aiming to cover up the illegal origins of the funds.

While fraud may rely on falsifying documents or misrepresenting facts, money laundering often uses complex financial transactions, shell companies, or offshore accounts to hide the illicit nature of the funds.

4. Legal and Regulatory Challenges

Fraud and money laundering are governed by different legal frameworks, but they are often prosecuted together. For example, financial institutions are required to have robust anti-money laundering (AML) measures in place to detect suspicious transactions, including fraudulent activities that may lead to money laundering. Both crimes have severe penalties, including fines, asset forfeiture, and imprisonment, and regulators expect businesses to detect and report suspicious behavior associated with both.

Example: A person involved in a large-scale fraud scheme may also be investigated for money laundering as they attempt to hide the illicit gains.

5. A Shared Focus on Risk Management

Both fraud and money laundering require businesses to have strong Know Your Customer (KYC) protocols in place. By verifying the identities of clients and customers, businesses can reduce the risk of engaging with fraudulent entities and ensure that money laundering doesn’t occur through their systems. Ongoing monitoring of customer behavior and transaction histories is essential in identifying both fraudulent activities and laundering attempts.

As fraud and money laundering are often connected, businesses must be vigilant in identifying and addressing both issues. Let's now explore the best practices for businesses to mitigate the risks associated with these crimes.

Steps Businesses Can Take to Prevent Fraud and Money Laundering

In the United States, the situation is equally alarming. The Federal Trade Commission (FTC) declared that consumers lost $12.5 billion to fraud in 2024, a 25% increase over the previous year.

Businesses need to implement comprehensive strategies to mitigate the risks associated with these crimes, ensuring AML compliance with regulatory frameworks and safeguarding their operations. Below are essential steps businesses can take to protect themselves from fraud and money laundering:

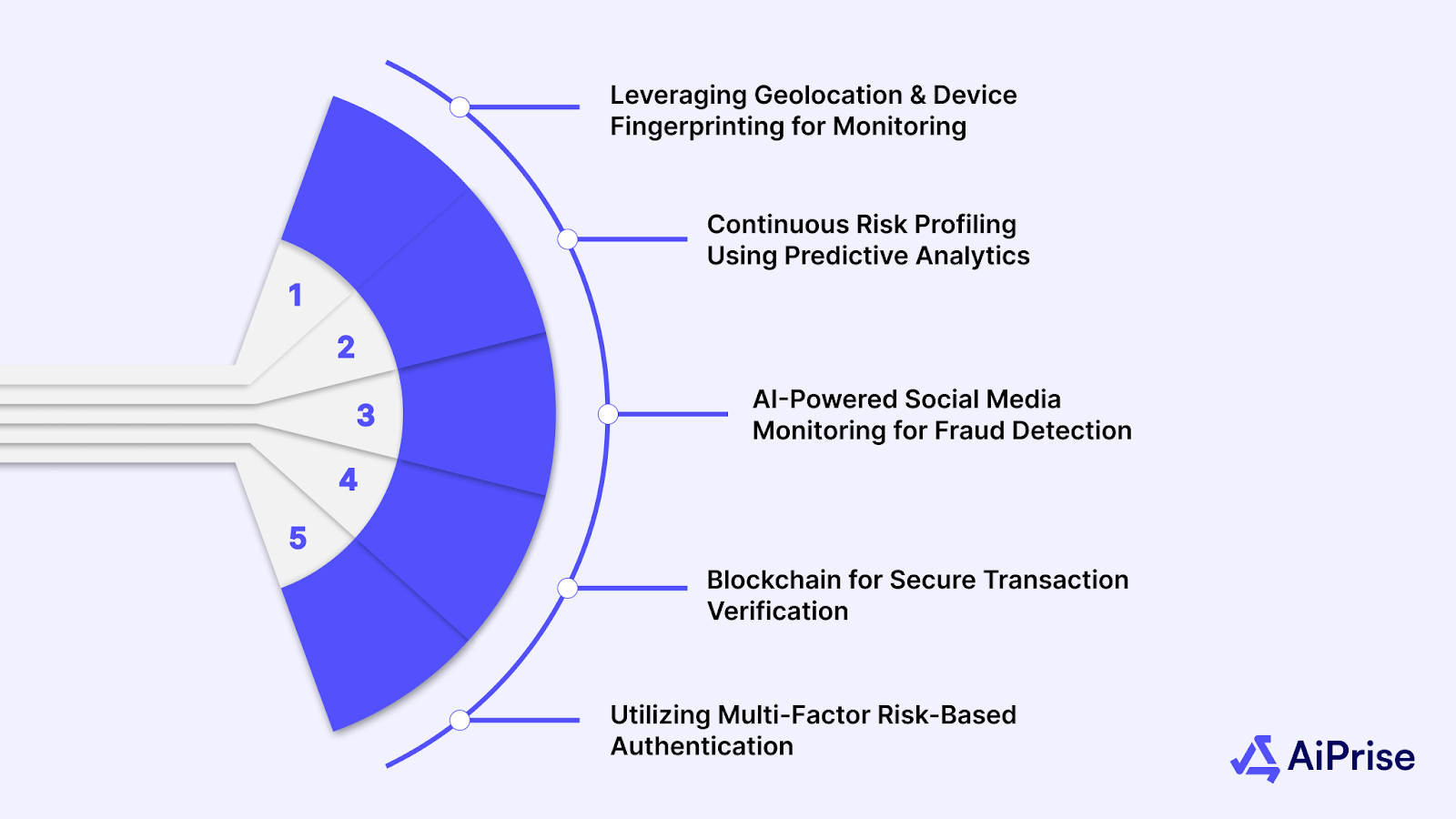

1. Leveraging Geolocation and Device Fingerprinting for Real-Time Monitoring

Fraudsters often try to bypass traditional verification systems by using fake IP addresses, VPNs, or proxy servers.

How to Implement This:

- Geolocation Tracking: Use APIs that provide real-time geolocation information, flagging any transactions from high-risk regions or unrecognized locations.

- Device Fingerprinting: Implement device fingerprinting solutions that track the specific device characteristics—such as browser, operating system, and screen resolution—used during every login.

- Cross-Check Locations with Known Data: Ensure that the IP address and device’s geolocation match the previously logged-in regions and user’s known activity.

2. Continuous Risk Profiling Using Predictive Analytics

Predictive analytics allow businesses to assess risk in real-time, rather than relying solely on historical data. This proactive approach helps identify potential fraud before it escalates.

How to Implement This:

- Data Modeling: Build machine learning models that analyze transaction data in real-time to assess risk levels based on customer behavior and historical transactions.

- Dynamic Risk Scores: Assign dynamic risk scores to customers based on predictive models that take into account unusual patterns in spending, transactions, and online activity.

- Automated Alerts: Set up automated alerts for high-risk transactions, such as unusual transaction sizes or sudden geographical changes in user behavior, allowing for immediate intervention.

3. Incorporating AI-Based Social Media Monitoring for Fraud Detection

Many fraudsters and money launderers use social media and online forums to conduct their illegal activities.

How to Implement This:

- Social Listening Tools: Implement AI tools that monitor social media platforms for keywords, phrases, or associations linked to criminal activity.

- Pattern Recognition: Use AI to detect inconsistencies between public social media profiles and customer data. Look for signs of social media activity that doesn’t match a person’s known behavior or identity.

- Cross-Reference with Other Data: Correlate social media activity with financial transactions and KYC data to identify potential fraud risks.

4. Blockchain for Secure Transaction Verification and Record-Keeping

Blockchain technology ensures the traceability of every transaction, making it virtually impossible for criminals to alter the records.

How to Implement This:

- Blockchain-Based Ledger: Store and track transaction records on a blockchain ledger that is immutable and transparent, preventing any tampering with transaction data.

- Smart Contracts for Automated Checks: Use smart contracts to automatically check transactions when certain conditions are met, ensuring that the transaction is legitimate before it is processed.

- Track Source of Funds: Use blockchain to trace the source of funds for high-value transactions, making it easier to detect suspicious activity or money laundering.

5. Utilizing Multi-Factor Risk-Based Authentication

Fraud prevention often relies on static checks like passwords or OTPs, but risk-based authentication (RBA) dynamically adjusts the authentication process depending on the perceived risk of a transaction.

How to Implement This:

- User Behavior Analytics: Incorporate behavioral biometrics and device recognition to track users' typical behavior, such as login times and device usage.

- Dynamic Authentication: Adjust the authentication process based on the risk score—requiring additional verification steps like facial recognition or phone call verification when a higher risk is detected.

- Incorporate Real-Time Monitoring: Use machine learning to assess transaction patterns and trigger more stringent authentication requirements if abnormal behaviors or risk patterns emerge.

The Future of Fraud and Money Laundering Prevention

It's crucial to stay ahead with a comprehensive solution that integrates fraud detection and anti-money laundering (AML) efforts. AiPrise offers an advanced platform designed to protect your business from evolving threats.

Key Features of AiPrise:

- Unified FRAML Framework: AiPrise integrates Fraud and Anti-Money Laundering (FRAML) operations into a single, unified system, streamlining processes and enhancing detection capabilities.

- Real-Time Behavioral Analytics: Utilizes machine learning to analyze user behavior patterns, identifying anomalies indicative of fraud or money laundering activities.

- Advanced Identity Verification: Employs AI-driven tools for liveness detection and document verification, ensuring secure and compliant onboarding processes.

- Comprehensive Transaction Monitoring: Monitors transactions in real-time, applying risk-based scoring to detect and prevent suspicious activities effectively.

- Automated Compliance Reporting: Generates and manages Suspicious Activity Reports (SARs) with enhanced accuracy and efficiency, reducing manual workload and ensuring regulatory compliance.

Don't let financial crimes jeopardize your business. Embrace the future of fraud and AML prevention with AiPrise.

Conclusion

Fraud and money laundering are not only widespread but are intricately connected, often feeding off each other in a cycle of deceit and financial crime. While the two crimes may differ in their intent and process, both have one common goal: to exploit and harm individuals, businesses, and economies.

AiPrise offers innovative solutions designed to streamline merchant verification, reduce fraudulent activities, and enhance compliance with global regulations. Protect your business today—partner with AiPrise for fraud prevention and identity verification solutions. Book A Demo with AiPrise to learn how we can help you combat fraud, money laundering, and other financial crimes with confidence.

FAQs

1. What are the main legal consequences of being involved in fraud or money laundering?

Both fraud and money laundering can result in severe legal consequences, including fines, asset forfeiture, and imprisonment. Depending on the scale of the crime, offenders may face decades of imprisonment and extensive financial penalties, as well as international sanctions.

2. How do financial institutions conduct risk-based assessments during merchant verification?

Financial institutions assess the risk of a merchant by examining factors such as business history, transaction volume, geographical location, and the type of goods or services offered. High-risk merchants may be subject to more detailed due diligence to ensure they don't engage in illegal activities.

3. What role do internal controls play in preventing fraud and money laundering?

Internal controls like division of duties, regular audits, and employee training are essential in identifying and preventing fraudulent activities. Proper internal controls can help businesses detect suspicious patterns early and stop fraud before it escalates.

4. How can businesses identify suspicious customer behaviors that may indicate money laundering?

Businesses should look for inconsistencies in customer behavior, such as frequent large transactions without clear business justification, use of multiple accounts under different names, or sudden changes in spending patterns. These could signal money laundering attempts.

5. Can smaller businesses effectively prevent fraud and money laundering with limited resources?

Yes, smaller businesses can take steps to mitigate risks by implementing affordable fraud detection tools, automating basic verification processes, and partnering with specialized service providers.

You might want to read these...

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately