AiPrise

19 mins read

August 13, 2025

How to Detect Financial Services Fraud: A Practical Guide for Businesses

Key Takeaways

Fraud in financial services is when someone uses lies or tricks to steal money, information, or access, think stolen identities, fake loan applications, or phishing scams. It sounds distant until you realize a fake email could wipe out a client’s account.

In 2024, 79% of US organizations faced payment fraud attempts, with business email compromise topping the threat list for 63% of them.

The real problem? Fraud keeps getting smarter while your tools often stay the same.

This guide to financial services fraud detection walks you through the most common types of fraud, why they're so hard to catch, and the tools that actually work.

In a Nutshell:

- Financial services fraud includes tactics like identity theft, account takeovers, fake loan applications, and insider threats.

- Detection tools like real-time monitoring, behavioral biometrics, device fingerprinting, and link analysis help flag threats early.

- Prevention starts with stronger KYC, session tracking, access controls, and vendor validation, before transactions ever happen.

- AiPrise supports fraud teams with AI-powered tools that catch synthetic identities and risky behavior before it leads to loss.

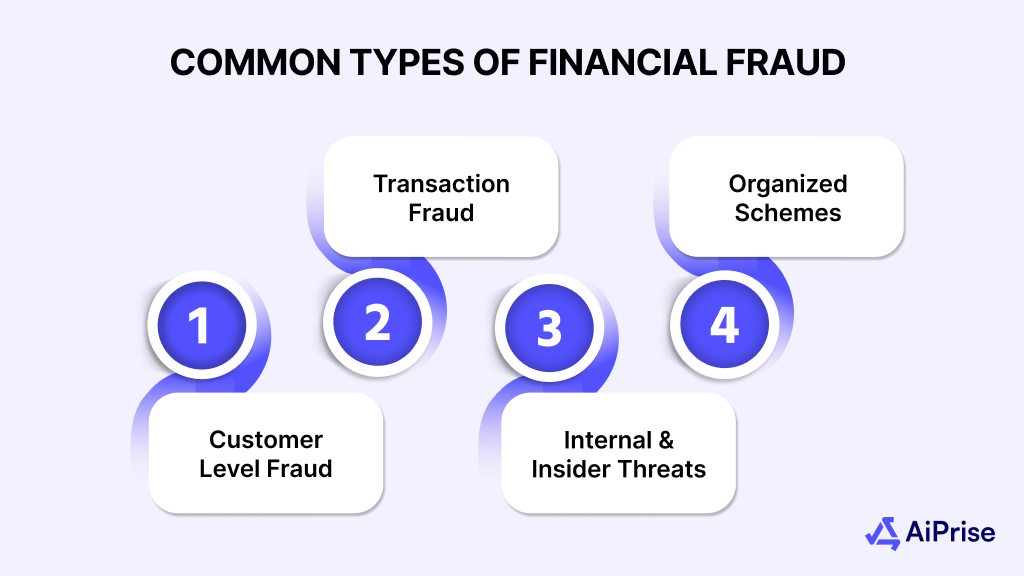

Common Types of Financial Fraud You Should Know

You approve a new customer account that looks clean on paper. A few days later, a large transfer goes through, followed by another, and then the contact details change. Suddenly, the account goes dark. By the time your team catches on, the damage is done, and the audit trail is a mess.

This kind of scenario isn’t rare. The trouble is, no two fraud cases look the same. Some are fast and obvious, others slow and calculated.

If you're serious about financial services fraud detection, you need to know what you're dealing with. Below are different categories of financial fraud your business might run into:

Customer-Level Fraud

Customer-level fraud usually hits your relationship with the user. It slips past basic checks, creates chargebacks, and chips away at customer trust.

1. Identity Theft

A fraudster uses stolen personal information, government IDs, tax numbers, and utility bills to pass off as a legitimate customer. Often, this data is purchased from data breaches or phished directly.

How does it show up?

You’ll see new accounts with clean but shallow histories, verified KYC but questionable behavior, or document mismatches during onboarding.

Why does this hurt your business beyond just one account?

- Regulatory exposure if fake identities pass through KYC/AML controls unchecked. This can trigger audits or fines.

- Credit losses if loans are issued to synthetic or non-existent customers who never intend to repay.

- Damage to internal metrics, your user acquisition or approval rate might look strong, but the underlying risk isn’t visible.

Watch for these early indicators before fraud reaches your balance sheet:

- Same IP, phone number, or address being used to open multiple “unique” accounts.

- Slight variations in names or DOBs, often just a character or digit off from real records.

- Rush behavior: full application completed within minutes, often during non-business hours.

2. Account Takeover (ATO)

A legitimate customer’s account is hijacked, usually via stolen credentials from phishing, malware, or credential stuffing attacks. From the outside, it looks like normal activity.

How does it show up?

Account activity continues as usual until the fraudster gains access. Then you'll notice password resets, changed contact info, or abnormal transactions from the same login.

How does ATO strain your support, systems, and customer trust?

- Customers blame your security controls when funds disappear, even if the breach was external.

- Increased call center and support load as panicked users try to reclaim access.

- Temporary or permanent churn, especially from high-value users, if the issue isn't caught early.

Here’s how you can spot ATO patterns before they escalate into losses:

- Logins from new devices paired with profile changes like email or mobile number updates.

- High-risk device/browser combos like Tor, emulators, or outdated OS versions.

- Unusual behavior like changing the password and initiating a high-value transfer immediately after.

3. Loan Application Fraud

The fraudster submits a loan or credit request using false employment details, inflated income, or stolen documents. Sometimes it’s a synthetic identity fraud built entirely from scratch.

How does it show up?

Loan applications pass initial checks but break down during income verification or repayment. Defaults happen early, often before the first installment.

How does this erode risk accuracy and eat into credit margins?

- Skews your underwriting models, your risk scoring assumes a legitimate applicant.

- Increases early-stage delinquencies, which can affect your lender rating or investor confidence.

- Wastes time and cost on due diligence, underwriting, and collections for fake accounts to begin with.

Red flags to catch before approvals go out:

- Employment details can’t be verified through known databases or the listed company doesn’t exist.

- IP address or device has applied for multiple loans in a short time span.

- Income documents look polished but lack third-party validation, like form-16s, tax filings, or salary slip metadata.

4. SIM Swap Fraud

A scammer tricks a telecom operator into assigning your customer’s mobile number to a new SIM. Once done, they intercept OTPs and 2FA codes to break into accounts.

How does it show up?

Legitimate users get locked out of their banking or wallet apps, often just after receiving phishing calls or strange SIM/network errors.

Why does SIM swap bypass your usual fraud defenses and become expensive fast?

- Your SMS-based 2FA becomes useless; fraudsters can drain accounts without ever knowing passwords.

- Escalates to account takeovers if the same number is linked across apps and services.

- Even when stopped in time, you still absorb the cost of incident handling, investigation, and user recovery.

Stay alert to these signals that your 2FA channel might be compromised:

- Multiple failed OTP verifications followed by a sudden successful login.

- Users reporting “no service” while your systems show successful OTP delivery.

- Same mobile number showing up in multiple user profiles, sometimes with altered last digits or spoofed caller IDs.

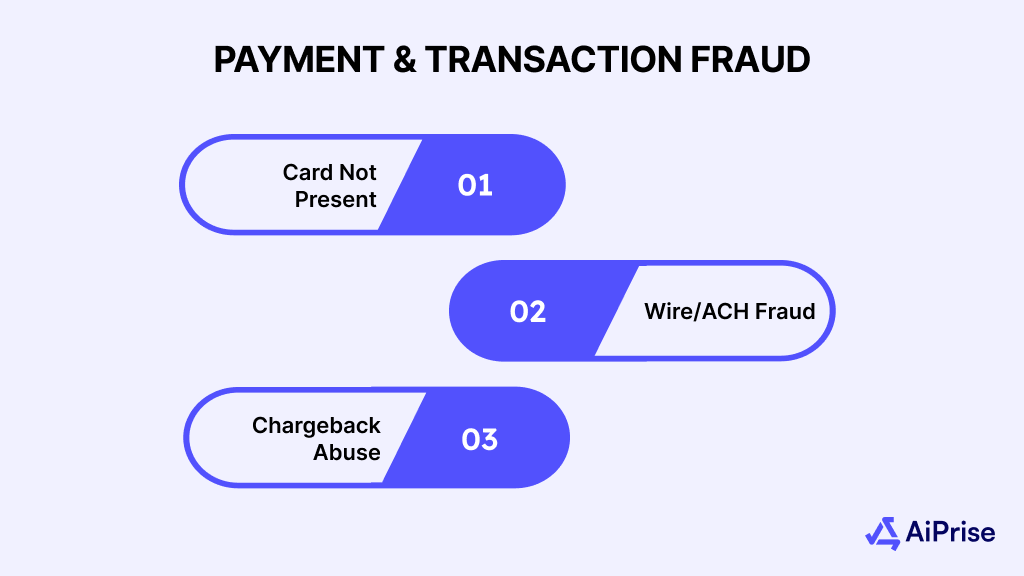

Payment & Transaction Fraud

You might see a flood of small transactions on a stolen card, a fake refund request, or a money transfer routed through six different accounts before vanishing. By the time your team catches the inconsistency, the money’s gone and the audit trail is messy.

For any business serious about financial services fraud detection, spotting these patterns early is non-negotiable. Here's what you're most likely to face:

1. Card-Not-Present (CNP) Fraud

A fraudster uses stolen card details to make purchases online or over the phone, anywhere the physical card isn’t required. Often, this data is pulled from breached sites or bought on the dark web.

How does it show up?

You approve what looks like a normal transaction, but it later gets disputed by the actual cardholder. This happens after the product or service is already delivered.

Why does CNP fraud quietly drain revenue and trust?

- Chargebacks stack up fast; you're not only refunding money but also losing goods or service hours.

- Repeated CNP disputes flag your business to card networks, which can increase processing fees or lead to penalties.

- High chargeback ratios can get your merchant account frozen or downgraded.

Track these behaviors before the dispute hits your inbox:

- Large orders from new customers using email IDs with random characters or free domains.

- Multiple attempts with different card numbers from the same IP/device in a short span.

- Mismatched billing and shipping addresses, or high-value international orders with no prior history.

2. Wire/ACH Fraud

This involves unauthorized or deceptive bank transfers, either by hacking into payment systems or by tricking someone into sending funds to a fraudulent account.

How does it show up?

Money is transferred to a vendor or customer, but later you find out the recipient details were altered, often due to business email compromise (BEC) or insider access.

How does wire fraud put operational processes under pressure?

- Funds are usually unrecoverable after they leave your account, especially across borders.

- It exposes poor verification workflows, like relying on unconfirmed email approvals for large payments.

- Creates audit headaches if your internal logs show “successful” but unauthorized transactions.

Be alert to these issues that usually precede wire/ACH fraud:

- Sudden vendor banking detail changes with no phone confirmation.

- Urgent payment requests from senior executives via email, often with odd phrasing or timing.

- Transfers requested outside usual payment cycles or flagged for manual review but pushed through.

3. Refund and Chargeback Abuse

A fraudster, or sometimes a legitimate customer, exploits your refund or return policy to get money back while keeping the product or falsely claiming unauthorized transactions.

How does it show up?

You process a refund assuming the item is returned or the claim is valid, only later to find patterns of abuse or no supporting evidence.

Why is refund fraud costly beyond just the transaction?

- It trains fraud rings to target your brand again, especially if policies are lenient or enforcement is slow.

- Legitimate users see these abuses and lose confidence in your fairness or security.

- It wastes support bandwidth with repeated, staged complaints or chargeback disputes.

Spot abuse trends before they become recurring loss patterns:

- Customers who frequently claim “item not received” right after delivery confirmation.

- Accounts tied to multiple refund requests across different payment methods.

- Refunds requested through support channels before the original transaction clears.

Internal & Insider Threats

Internal fraud doesn’t always come from hackers or outsiders; it can start right at someone’s desk. An employee with backend access tweaks account settings. A contractor quietly extracts customer data. A junior staffer approves a loan without proper checks in exchange for a kickback.

These cases are harder to catch because the access is legitimate on paper. That’s what makes insider threats so risky. For businesses serious about financial services fraud detection, this category requires a different kind of scrutiny.

Here's what you should be watching for:

1. Employee Manipulation of Accounts

An employee uses their access to alter customer or business accounts, adjusting limits, waiving fees, or approving loans or transactions that wouldn’t normally pass review. It can be done for personal gain or to benefit someone outside the company.

How does it show up?

Adjustments are made under valid credentials, but they don’t follow policy. You might notice exceptions being approved without documentation or irregular patterns tied to a single employee’s actions.

Why does this create long-term risk even after the fraud is caught?

- It weakens internal controls, if one person can bypass checks, others might too.

- Discovery often comes late, through audits or complaints, by which time multiple incidents may have occurred.

- Once exposed, it can lead to internal distrust, regulatory reporting, and a painful reputational hit.

Watch for behavioral patterns that often precede manipulation:

- Repeat actions just below approval thresholds to avoid dual-review triggers.

- Frequent use of override functions or manual account adjustments.

- High volume of transactions tied to the same customers, vendors, or regions.

2. Unauthorized Access or Privilege Abuse

An employee or contractor uses access permissions they shouldn’t have, or accesses systems beyond their role. This can range from peeking at customer data to downloading transaction logs or altering backend configurations.

How does it show up?

You won’t see it in the numbers at first. Instead, it surfaces through access logs, failed login attempts, or data anomalies. Often, it’s caught when something breaks, or a whistleblower comes forward.

Why do excessive access rights quietly leave your systems exposed?

- It breaks your audit trail, if access is shared or unmonitored, it’s hard to trace who did what.

- Sensitive customer data can be scraped and sold without triggering typical fraud alerts.

- If a disgruntled employee walks out with credentials, it leaves you open to larger breaches.

Keep an eye on these signals before privilege abuse turns into a security incident:

- Role changes that weren’t followed by a permissions update, people holding on to legacy access.

- Access to high-risk functions (refunds, account resets, config changes) being used after hours or unusually frequently.

- Employees downloading large volumes of data or exporting reports not tied to their daily role.

Large-Scale/Organized Schemes

Large-scale or organized fraud is harder to trace because it’s patient. Fraud rings might use synthetic identities to build credit over months or layer transactions to wash dirty money through clean systems. These schemes don’t trigger alarms right away because they’re meant to look like normal business.

Here's what you should be watching for:

1. Money Laundering

Criminals move illegally obtained money through legitimate financial channels to hide its origin. This often involves multiple steps, layering funds through accounts, businesses, and jurisdictions to make them appear clean.

How does it show up?

You might see structured deposits just under reporting thresholds, sudden large transfers from dormant accounts, or unusual customer behavior that doesn’t match their profile.

Why does money laundering quietly eat into compliance and expose the business to legal risk?

- Regulators expect robust AML checks; failure to report suspicious activity can trigger investigations, fines, or license reviews.

- It attracts high-risk clients that damage your portfolio's credibility and increase your audit load.

- These transactions can overlap with terrorist financing or tax evasion, dragging your institution into wider criminal probes.

Look for these signs before laundered money flows through your system:

- Clients frequently moving funds between unrelated accounts or jurisdictions without clear business rationale.

- Business accounts with high turnover but minimal payroll, operational spend, or supplier history.

- Repeated transactions involving countries or entities listed in OFAC or FATF watchlists.

2. Synthetic Identities

A synthetic identity combines real data (like a valid SSN or Aadhaar number) with fake or manipulated details to create a new, seemingly legitimate profile. These identities are then used to open accounts, build credit, and commit long-term fraud.

How does it show up?

The customer looks real, passes KYC, makes small deposits, and slowly builds activity. Then, over time, the account is used to secure credit or execute larger transfers, and eventually disappears.

Why do synthetic identities make fraud detection harder and more expensive?

- They corrupt your data, risk models assume synthetic users are real, skewing customer behavior baselines.

- Synthetic fraud often spans months or years, making it harder to trace and more damaging when it hits.

- Manual review doesn’t always catch them, because there’s just enough real data to pass most checks.

Spot synthetic identity behavior before it builds momentum:

- Profiles with thin credit files that suddenly show high usage or credit demand.

- Accounts with minimal human digital footprint, no social media presence, unusual browsing patterns, or duplicate IP/device use across users.

- Reuse of contact details (email, phone) across multiple identities with different names or DOBs.

3. Shell Company Scams

Fraudsters set up fake or inactive companies, often with minimal staff, vague business activity, or fake invoices, to route transactions and hide the true source or destination of funds.

How does it show up?

The company has a website, a registered address, maybe even a GST or EIN, but no real operations. Transactions go in and out, but there's no trace of goods or services changing hands.

Why do shell companies put pressure on your vendor verification and AML systems?

- They mask ownership structures, allowing fraud rings to move money without scrutiny.

- They often partner with complicit insiders, making detection harder through normal workflows.

- Once detected, they can trigger retrospective reviews of every connected transaction, creating a compliance backlog.

Red flags that often point to shell company abuse:

- Vendors with no digital footprint beyond a basic site or registry listing.

- Repeated high-value transactions with no purchase orders, invoices, or delivery records.

- Rapid onboarding of vendors with minimal due diligence or through non-standard channels.

You’ve seen how fraud plays out. Now, here’s how to spot it in real time.

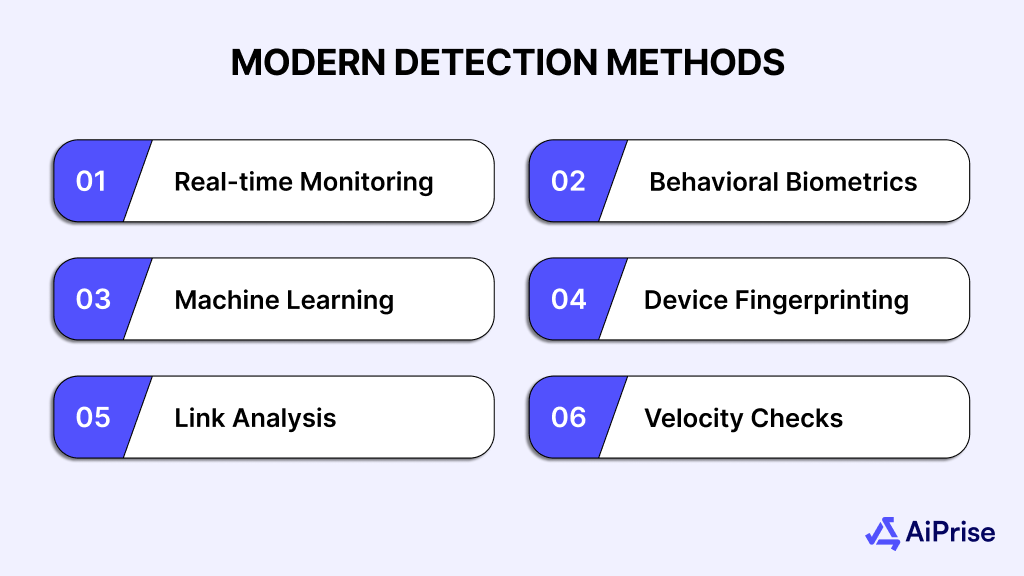

Modern Detection Methods and Tools

Let's say a flagged transaction hits your dashboard at 2:13 a.m. The customer’s IP is from overseas, the device is new, and the order value is five times higher than usual. By the time someone on your team notices, the payment clears and the product ships. Fraud score? Just low enough to pass.

To stay ahead, your financial services fraud detection approach needs to be faster, smarter, and built to spot the things you’d miss on your own.

Below are the modern detection methods and tools:

1. Real-time Monitoring

This flags fraud as it happens. Transactions are scored the moment they’re initiated, based on past behavior, risk signals, and contextual data. It’s key for stopping card-not-present fraud or rapid-fire transfers from newly opened accounts.

Use it for: Payment fraud, account takeovers, refund abuse.

Example: AiPrise uses real-time signals to stop suspicious fund flows before they settle.

2. Behavioral Biometrics

This method tracks how a user types, moves their mouse, or taps on a phone. Every customer has a digital rhythm, and when it changes, it’s often not them.

Use it for: Detecting stolen credentials, session hijacking, scripted logins.

Key point: Even if the device and password match, the behavior might not.

3. Machine Learning

ML models learn from past fraud cases and evolve as tactics change. They identify patterns too complex or rare for rule-based systems.

Use it for: Synthetic identity fraud, multi-step laundering, insider threats.

Example: AiPrise uses ML-based clustering to link accounts that appear unrelated but show shared fraud signals over time.

4. Device Fingerprinting

This builds a unique ID for every device that interacts with your platform, based on hardware, browser, IP history, and more. If one “customer” uses five different identities from the same phone, this method catches it.

Use it for: Catching account farming, repeat fraud attempts, SIM swap behavior.

5. Link Analysis

Link analysis maps out relationships between accounts, devices, transactions, and users. It’s used to expose fraud rings, mule networks, and shell company setups that rely on distributed activity.

Use it for: Organized fraud schemes, collusion between insiders and third parties.

6. Geolocation and Velocity Checks

These flag anomalies in time, distance, or access speed. If a user logs in from Delhi and five minutes later from Frankfurt, something’s off.

Use it for: Stopping impossible travel logins, bot-driven fraud, and proxy misuse.

Pro tip: Combine this with behavioral signals for stronger accuracy.

Once detection is in place, the next step is prevention, putting the right safeguards in place before fraud ever has a chance to occur.

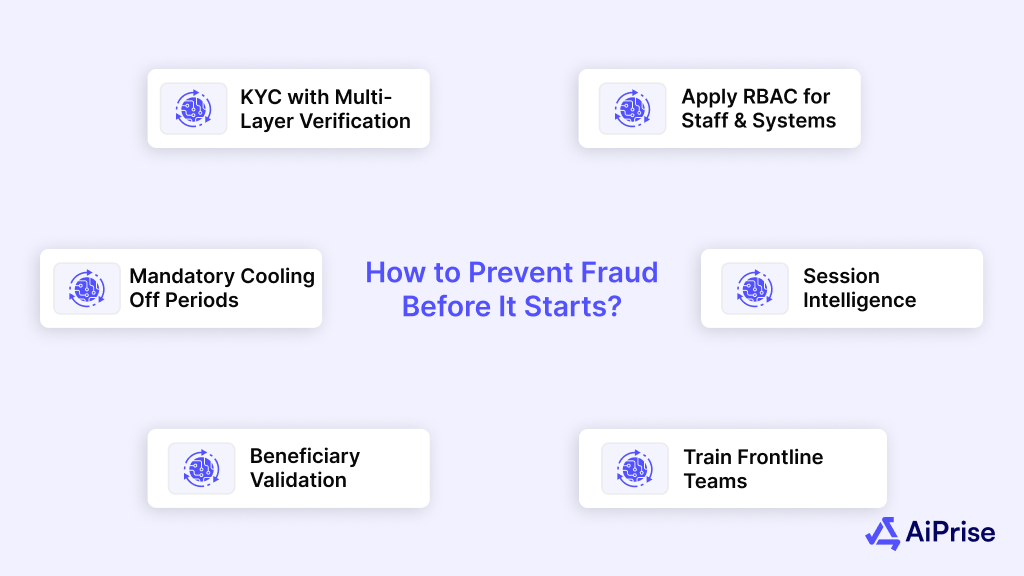

How to Prevent Fraud Before It Starts?

Fraud prevention starts long before a transaction is flagged. It’s built into how you verify users, protect access, and control sensitive actions. For financial services fraud detection to work at scale, your first line of defense needs to be strong, consistent, and hard to bypass.

Here’s what that looks like:

1. Tighten KYC with Multi-Layer Verification

Don’t rely on just one document or database. Cross-check government-issued IDs with telecom data, utility bills, and known fraud databases.

Example: A fake Aadhaar paired with a real phone number might pass basic KYC. But if the phone is registered in a different state than the address, that’s a red flag.

2. Apply Role-Based Access for Staff and Systems

Everyone in your organization shouldn’t have access to customer data or transaction controls. Limit it to what each role needs.

Example: A junior support agent shouldn’t be able to initiate refunds or reset login credentials without a second layer of approval.

3. Enforce Mandatory Cooling-Off Periods

Set delays between high-risk actions, like changing a phone number and making a large transfer.

Example: A 24-hour lockout after contact detail changes gives time to flag suspicious behavior before money moves.

4. Use Session Intelligence, Not Just Login Checks

Go beyond “successful login.” Track how users move inside your platform.

Example: Fraudsters often skip browsing and go straight to high-risk features, like payout settings or account closure.

5. Automate Vendor and Beneficiary Validation

Before payouts or fund transfers, verify beneficiary details through independent data sources.

Example: Validate bank account names against GST records or UPI handles to detect shell vendors.

6. Train Frontline Teams on Social Engineering Tactics

Your staff can be an entry point if they aren’t prepared.

Example: A fraudster pretending to be a senior manager requests an urgent manual override. Staff should be trained to verify through internal escalation paths, not email alone.

Review your controls regularly, test for gaps, and don’t rely on one system to catch everything. The stronger your financial services fraud detection framework, the fewer surprises you’ll face.

How AiPrise Helps Businesses Prevent Financial Services Fraud

AiPrise provides a reliable identity verification platform designed to handle large volumes, meet regulatory standards, and protect against sophisticated fraud.

Here’s how it stands out in enabling secure and efficient digital onboarding:

- Verifies IDs from 200+ countries in under 30 seconds with AI-driven OCR, barcode/MRZ scanning, and enhanced security feature checks for over 12,000 document types.

- Performs biometric checks (facial recognition, liveness detection) to prevent spoofing, deepfakes, and synthetic identity fraud.

- Integrates with 800+ data sources for instant cross-referencing against government, credit, and sanctions lists, ensuring global KYC and KYB compliance.

- Customizable rule engine and risk scoring: Tailor onboarding flows and risk thresholds, automating low-risk approvals and escalating high-risk cases for review, reducing manual review time by up to 95%.

- Continuous fraud monitoring: Real-time alerts, adverse media scans, and ownership checks mean your systems don’t stop at onboarding. AiPrise helps you track identity risk as it changes.

- Fast, flexible setup: With white-label UI, API and SDK support, and multi-language capability, AiPrise can go live in days, without disrupting your current flow.

AiPrise helps you verify identities, spot fraud, and stay compliant all in one place, without slowing things down.

Conclusion

Strong fraud prevention starts with knowing what to look for and acting before it hits your system. With the right mix of tools, policies, and checks, you can spot bad behavior early, protect customer trust, and keep losses in check.

It’s not just about ticking off a compliance box; it’s about staying one step ahead of the fraud tactics targeting your business every day.

Want to strengthen your identity checks and cut fraud risks? Book A Demo with AiPrise to see how the platform fits into your workflow and helps you stay secure and compliant.

FAQs

1. What is financial services fraud?

Financial services fraud involves illegal activities like identity theft, account takeovers, fake loan applications, and unauthorized transactions carried out to steal money or data from banks, fintechs, or lenders.

2. How do fraudsters typically commit financial fraud?

They use phishing, malware, social engineering, or stolen credentials to access accounts or systems. Some create fake identities or shell companies to appear legitimate.

3. What are the biggest red flags businesses should watch for?

Unusual transaction patterns, mismatched personal details, login attempts from unknown devices or locations, and rushed onboarding with incomplete documentation.

4. How does fraud impact financial businesses beyond monetary loss?

It damages customer trust, increases regulatory scrutiny, skews risk models, and often results in higher operational costs from chargebacks, reviews, and recovery processes.

5. What are the most common types of financial fraud businesses face today?

Identity theft, account takeover, synthetic identities, money laundering, refund abuse, and wire transfer fraud are among the most common.

6. How can businesses prevent fraud before it happens?

Use multi-layered KYC, enforce access controls, monitor session behavior, validate vendors and beneficiaries, and train staff to spot social engineering attempts.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately