AiPrise

6 mins read

September 11, 2025

Understanding Fraud: Patterns and Prevention Strategies

Key Takeaways

Fraud is a major issue for businesses, especially in the financial, payment, and cryptocurrency sectors. Companies are constantly under pressure to protect their customers while maintaining compliance with complex regulations. Balancing fraud prevention with customer experience can be challenging.

In 2024, 79% of organizations reported being victims of payment fraud attempts or attacks. This statistic highlights how serious the problem has become and the urgent need for businesses to act. As fraud schemes become more sophisticated, preventing fraud requires more than basic security measures.

In this blog, we’ll explore common fraud patterns and behaviors, effective fraud prevention strategies, and how technology can support these efforts. By the end, you’ll have a better understanding of how to build a plan that protects both your company and your customers.

Key Takeaways:

- Fraud detection requires spotting early signs, like unusual account behavior or changes in transaction patterns, to avoid financial losses.

- Effective fraud prevention involves adopting tools like multi-factor authentication, machine learning, and device tracking to reduce risks.

- Regular employee training and clear reporting procedures ensure that staff can act quickly when fraud is suspected.

- Implementing advanced technologies such as AI-powered monitoring can help businesses spot suspicious activity before it escalates.

Recognizing Fraud Behavior: Key Red Flags

Fraud often leaves behind clear signs if you know what to look for. Understanding fraud behavior is critical in identifying threats early, enabling businesses to prevent financial losses. Several indicators can point to suspicious activity, and recognizing them is the first step in effective fraud prevention. By staying vigilant and aware of common fraud patterns, your team can take swift action to reduce risks.

In this section, we’ll explore key red flags that suggest fraudulent behavior, breaking them down into customer profile anomalies, transaction irregularities, and other red flags that warrant closer attention.

Customer Profile Anomalies

One of the most common indicators of fraud is discrepancies or sudden changes in a customer’s profile. Fraudsters may create fake identities or hijack existing ones, and recognizing these shifts can prevent further damage. By carefully monitoring customer profiles, businesses can catch irregularities that indicate potential fraud.

- Multiple Accounts with Slight Variations: A customer using different but similar names, email addresses, or phone numbers across multiple accounts may be attempting to disguise their identity.

- Inconsistent Contact Information: Changes in contact details, such as addresses or phone numbers, that differ from previous records can be a sign of suspicious activity.

- Fake Identity Documents: Fraudsters may use forged documents or mismatched personal information to verify their identities. Ensure all documentation is authentic and up-to-date.

Suspicious Transaction Patterns

Transactions that fall outside of typical behavior are another warning sign. Fraudsters often try to move money quickly or in large volumes to evade detection. Monitoring transaction patterns closely can help identify suspicious behavior early on.

- Unusual Transaction Volumes: A sudden increase in the number or size of transactions could indicate that the account is being used for fraudulent activities.

- Transactions at Odd Hours: Uncommon times, such as late-night or early-morning transactions, especially from new locations, can be a red flag.

- Frequent Refunds or Chargebacks: If a customer consistently requests refunds or files chargebacks, it may suggest that they are using stolen payment details or engaging in fraudulent activities.

Behavioral Indicators

Fraudsters don’t just alter transaction behaviors; they also exhibit unusual patterns in their communication and interactions with your business. Being able to spot these red flags early can help prevent losses from going unnoticed.

- Urgency or Secrecy: A customer demanding immediate action or trying to keep details vague may be attempting to hide fraudulent activity.

- Reluctance to Provide Further Information: A customer who refuses to provide requested information or fails to verify their identity should be treated with caution.

- Unusual Pressure on Customer Service: Fraudsters may attempt to manipulate customer service agents into bypassing standard procedures or offering too much information.

Recognizing these key red flags can help businesses detect fraud in its early stages. The next step is to put in place systems to address these behaviors and prevent fraudulent activities from impacting your organization.

Also Read: Common Red Flags In Fraud Detection

9 Proactive Fraud Prevention Strategies

Once you've identified the signs of fraud, the next step is to implement strategies to prevent it from causing harm. Fraud prevention is about more than reacting to suspicious activity; it's about creating systems to detect and prevent fraud before it impacts your business.

Here are several key strategies:

- Multi-Factor Authentication (MFA): Requires customers to verify their identity through two or more methods, such as a password and a fingerprint scan.

- Biometric Verification: Fingerprint, facial recognition, or voice recognition adds an extra layer of identity verification.

- Device Fingerprinting: Tracks devices to spot suspicious logins or transactions from unfamiliar devices.

- AI-Powered Transaction Monitoring: AI analyzes transactions in real-time and flags suspicious activities, such as large transfers or changes in payment behavior.

- Machine Learning for Anomaly Detection: Machine learning models can detect subtle behavioral changes, helping to identify fraud patterns early.

- Regular Fraud Detection Training: Train employees regularly to recognize fraud indicators and report suspicious activities.

- Clear Reporting Procedures: Establish straightforward protocols for employees to report suspected fraud quickly and effectively.

- Separation of Duties: Assign distinct tasks, such as approval, authorisation, and record-keeping, to different employees to reduce the risk of internal fraud.

- Routine Audits: Conduct regular audits to identify discrepancies or unusual activities that may indicate fraud.

While prevention strategies are crucial, staying compliant with regulations is just as important to avoid legal complications.

Also Read: How to Avoid and Detect KYC Fraud

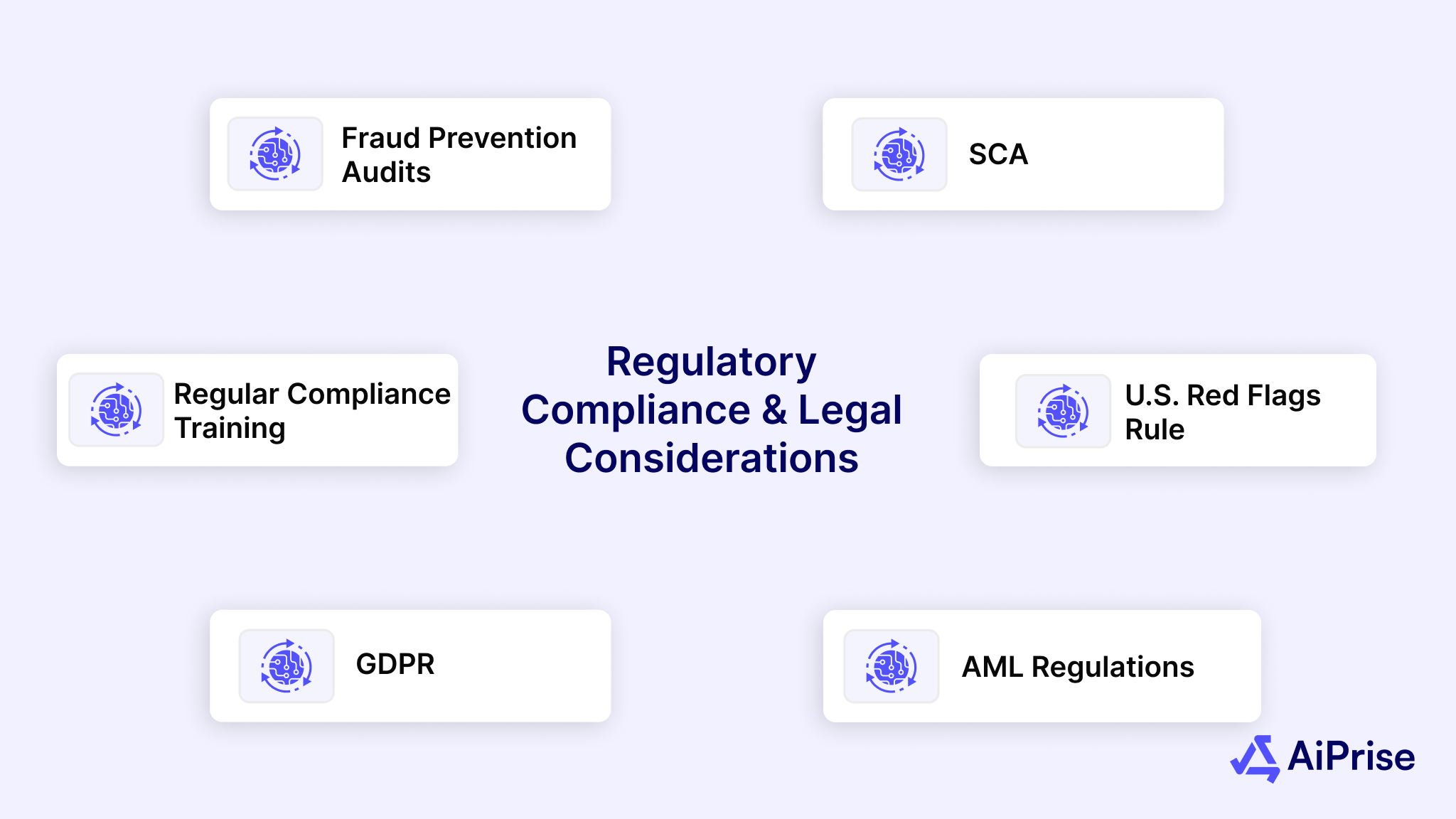

Regulatory Compliance and Legal Considerations

As fraud risks grow, staying compliant with regulations becomes essential. Compliance not only helps businesses protect customers but also reduces legal risks associated with fraudulent activities. Regulatory requirements are constantly changing, so businesses need to stay informed and proactive.

Here are some critical compliance aspects:

- Strong Customer Authentication (SCA): In the EU, SCA requires businesses to use multi-factor authentication for online payments, adding a layer of security.

- U.S. Red Flags Rule: Requires businesses to establish identity theft prevention programs to detect red flags that may indicate fraud.

- Anti-Money Laundering (AML) Regulations: Businesses must implement measures to detect and prevent money laundering, helping identify suspicious financial activity early.

- Data Protection Laws (GDPR): Protect customer data and ensure it’s handled in accordance with privacy laws, thereby avoiding potential legal consequences.

- Regular Compliance Training: Train employees on the latest regulatory changes to ensure your business meets all legal requirements.

- Fraud Prevention Audits: Regular audits help assess and improve your fraud prevention practices, ensuring ongoing compliance.

While maintaining compliance safeguards your business, implementing real-time monitoring systems helps detect and mitigate fraudulent actions instantly.

Also Read: Understanding The Five Pillars Of An AML Compliance Program

Real-Time Monitoring and Incident Response

Fraud can happen at any time, and responding quickly is crucial. Real-time monitoring allows businesses to detect suspicious activities as they occur, enabling a rapid response to prevent further damage.

Here’s how to set up effective monitoring and response systems:

- Transaction Monitoring: Track all transactions in real-time and flag any that deviate from a customer’s typical behaviour.

- AI-Powered Alerts: Use AI to identify unusual transactions and alert the team instantly, allowing for a quick response.

- Behavioral Analytics: Analyze customer behavior during transactions to identify inconsistencies that might suggest fraud.

- Clear Incident Reporting Process: Establish clear protocols for reporting suspicious activities, ensuring prompt and organized action.

- Dedicated Fraud Response Team: Set up a specialized team to handle fraud incidents and investigate quickly.

- Customer Communication: Notify affected customers promptly to maintain trust and ensure transparency during fraud investigations.

Real-time monitoring and quick response are crucial, and AiPrise offers a comprehensive set of tools to support these efforts.

Also Read: Importance and Process of Transaction Screening and Monitoring

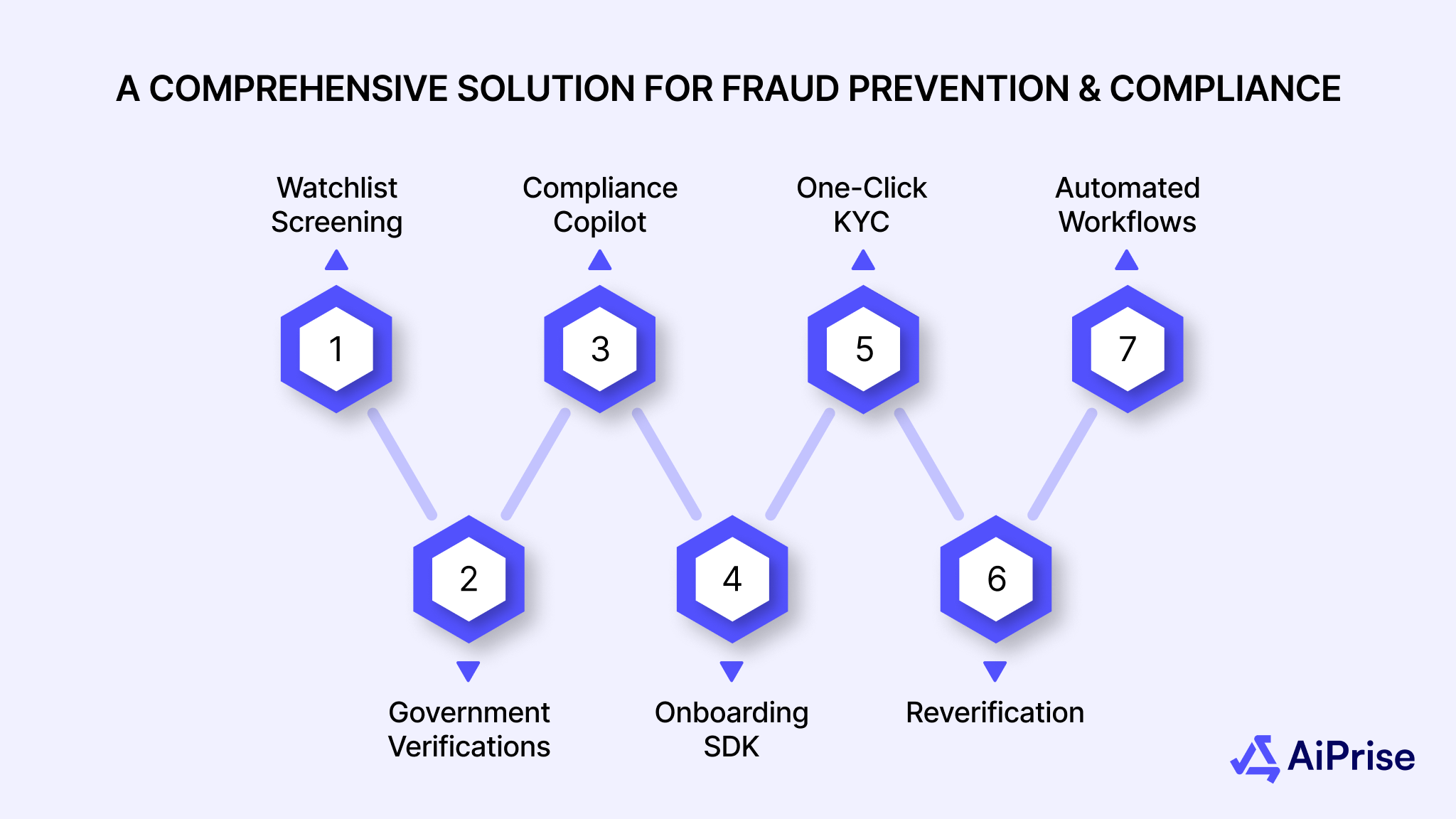

AiPrise: A Comprehensive Solution for Fraud Prevention and Compliance

AiPrise provides businesses with tools that enhance fraud detection and compliance. By incorporating advanced verification and monitoring tools, AiPrise helps companies to prevent fraud before it escalates.

Here are the key features of AiPrise that support fraud prevention and compliance:

- Watchlist Screening: Screens customers and transactions against global sanction lists to help businesses identify high-risk clients and comply with regulations.

- Government Verifications: Integrates with government databases to verify client identities against official records, reducing the risk of fraud.

- Compliance Copilot: AiPrise’s AI-powered Compliance Copilot helps reduce review times by up to 95%, making compliance processes faster and more accurate.

- Onboarding SDK: AiPrise’s SDK integrates KYC and AML checks into the client onboarding process, ensuring full compliance.

- One-Click KYC: Simplifies identity verification during onboarding, speeding up the process while ensuring compliance.

- Reverification: Helps businesses periodically reverify client information to maintain up-to-date customer profiles.

- Automated Workflows: Sets up automated fraud prevention workflows, reducing human error and ensuring compliance.

AiPrise’s tools can make fraud prevention easier and more effective, ensuring your business stays secure and compliant.

Conclusion

Fraud poses a significant risk to businesses, but with the right strategies and tools, it can be effectively prevented. By recognizing fraud patterns early, implementing proactive measures, and staying compliant with regulations, businesses can protect both their operations and customers. AiPrise offers comprehensive solutions that help detect fraud, ensure compliance, and simplify verification processes.

If you're ready to improve your fraud prevention strategy, Book A Demo today to see how our tools can help your business stay secure and compliant.

FAQs

1. How can businesses identify fraudulent activity in customer profiles?

Fraudulent activity in customer profiles can often be spotted through sudden changes in contact details or inconsistent personal information.

2. What are the most common types of suspicious transaction patterns?

Suspicious transactions often involve unusually large amounts, frequent refunds, or payments made at odd hours from new locations.

3. How does machine learning help in fraud detection?

Machine learning helps detect fraud by analyzing patterns in customer behavior and identifying deviations that suggest potentially fraudulent activities.

4. What legal regulations should businesses follow to prevent fraud?

Businesses must comply with regulations like Strong Customer Authentication (SCA), Anti-Money Laundering (AML), and data protection laws to mitigate fraud risks.

5. Why is it necessary for businesses to train employees regularly on fraud prevention?

Regular fraud detection training ensures that employees can quickly identify red flags and follow procedures to report suspicious activities effectively.

You might want to read these...

.png)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately