AiPrise

10 min read

November 24, 2025

Fintech Fraud Prevention: Effective Strategies and Solutions

Key Takeaways

Are you prepared to protect your business from the ever-evolving threat of fintech fraud?

In 2024, U.S. consumers reported over $12.5 billion in fraud losses, marking a 25% increase from the previous year. For fintech companies, this surge highlights the urgency of implementing strong fraud prevention strategies. Fraud not only leads to financial losses but can also damage customer trust, invite regulatory scrutiny, and increase operational costs. From account takeovers to synthetic identities, understanding and addressing these threats is essential for protecting your business, maintaining compliance, and fostering lasting customer relationships.

Quick Overview

- Fraud in fintech includes account takeovers, synthetic identity creation, payment fraud, and deepfake scams, each exploiting different system vulnerabilities.

- Fraud leads to financial losses, reputational damage, regulatory scrutiny, and increased operational costs.

- Use rule-based alerts, anomaly detection, behavioral analytics, and biometric checks to identify suspicious activity in real time.

- Strengthen identity verification, enforce KYC/AML standards, and ensure continuous monitoring to prevent fraud, while having clear response procedures for fraud incidents.

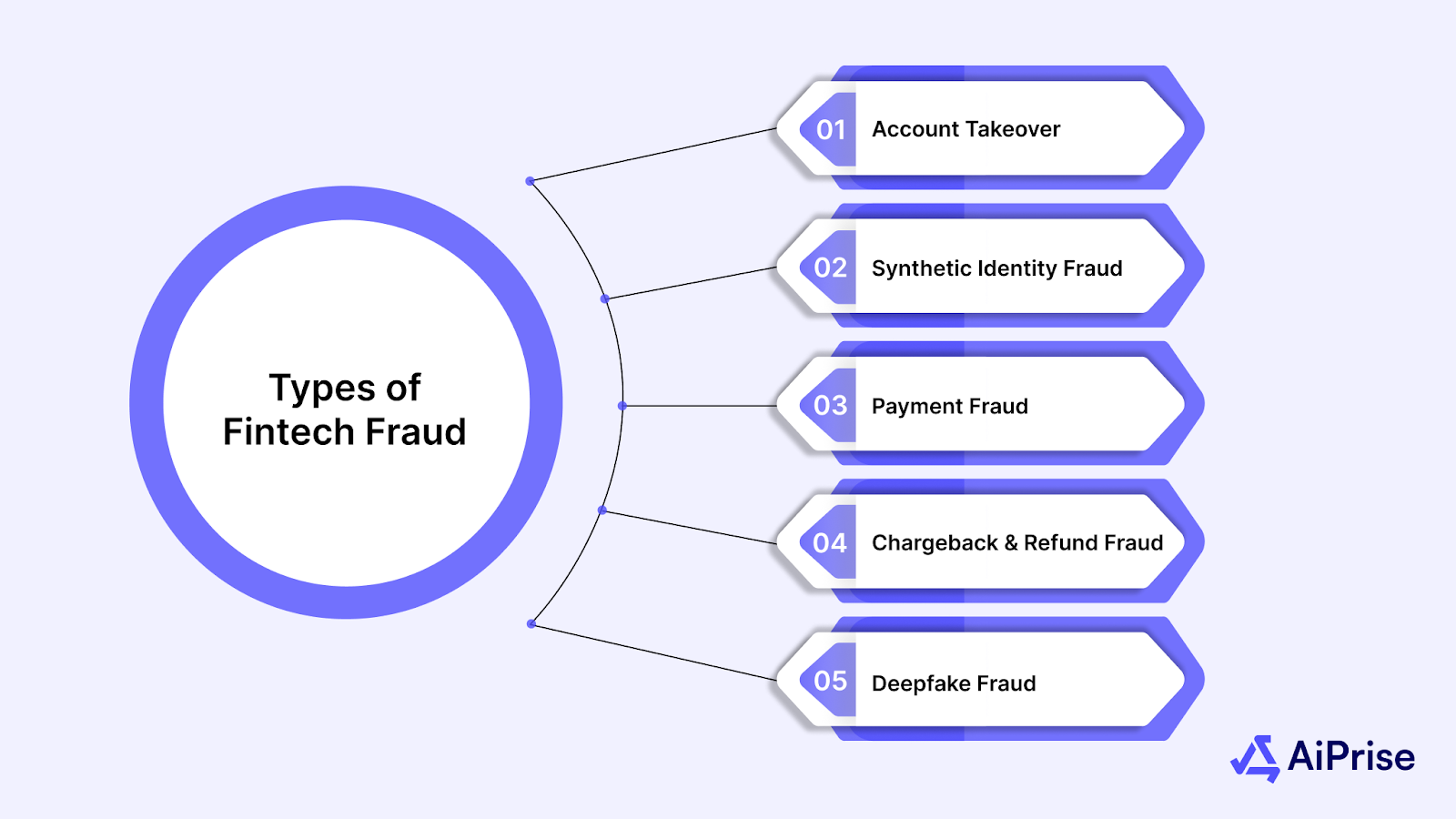

Types of Fintech Fraud

Fintech fraud takes many forms, each exploiting different gaps in digital finance. To build effective defenses, you need to understand the specific tactics that fraudsters rely on.

1. Account Takeover (ATO)

This happens when criminals gain unauthorized access to your customers’ accounts. By exploiting weak credentials or phishing scams, they can drain funds and steal sensitive information. ATO not only causes financial loss but also damages customer trust in your platform.

2. Synthetic Identity Fraud

Fraudsters combine real and fake data to create entirely new identities. These synthetic profiles often pass superficial checks, allowing criminals to open accounts, secure loans, or launder money undetected. For fintechs, this is especially dangerous because it can go unnoticed until losses pile up.

3. Payment Fraud

Payment fraud targets your transaction systems through stolen cards, unauthorized transfers, or push-payment scams. Attackers manipulate speed and automation to slip through detection tools. This type of fraud directly impacts your bottom line and erodes confidence in your payment services.

4. Chargeback and Refund Fraud

Fraudsters abuse refund policies or falsely dispute legitimate purchases. Each chargeback not only drains revenue but also triggers additional processing fees. Over time, excessive disputes can increase costs and damage relationships with payment processors.

5. Deepfake and Impersonation Fraud

With advances in AI, criminals now use deepfake technology to spoof identities during verification. Voice cloning and fake videos can trick both manual reviewers and automated systems. This emerging threat requires advanced biometric checks to counter.

After identifying the different fraud schemes, the next step is to understand the profound impacts these crimes can have on your business operations.

Also read: Online Identity Verification Methods: 7 Different Types

How Fintech Fraud Affects Businesses?

Fraud doesn’t just drain money; it shakes the foundation of your operations, from customer trust to compliance standing. Whether you’re running a bank, a payment gateway like PayPal, or a crypto exchange, the ripple effects of fraud can stall growth and invite costly consequences.

- Financial losses: You face direct theft when fraudsters exploit stolen credentials, open fake accounts, or abuse refund loopholes, for example, a crypto wallet is drained overnight, or a payment processor is compromised.

- Reputational damage: Customers lose faith fast when they see fraud slip through, whether it’s an insurance firm facing phishing scams or a crypto platform hit by account takeovers. Once trust is gone, user churn spikes.

- Regulatory scrutiny: A single compliance miss, like failing to meet KYC standards, can result in fines, penalties, or full-blown audits, especially for banks under strict AML rules. Regulators are quick to act when fraud isn’t controlled.

- Operational overload: Investigating fraud incidents pulls your teams away from core priorities. A payment provider managing hundreds of disputed transactions per day wastes valuable time that could be spent on scaling.

- Higher costs: Fraud drives up expenses through increased insurance premiums, chargeback reserves, and added security measures. For instance, payment processors often set aside large reserves when fraud rates rise.

The consequences of fintech fraud are far-reaching. Let’s now shift focus to the signs that might indicate when fraud is on the horizon, so you can act before it escalates.

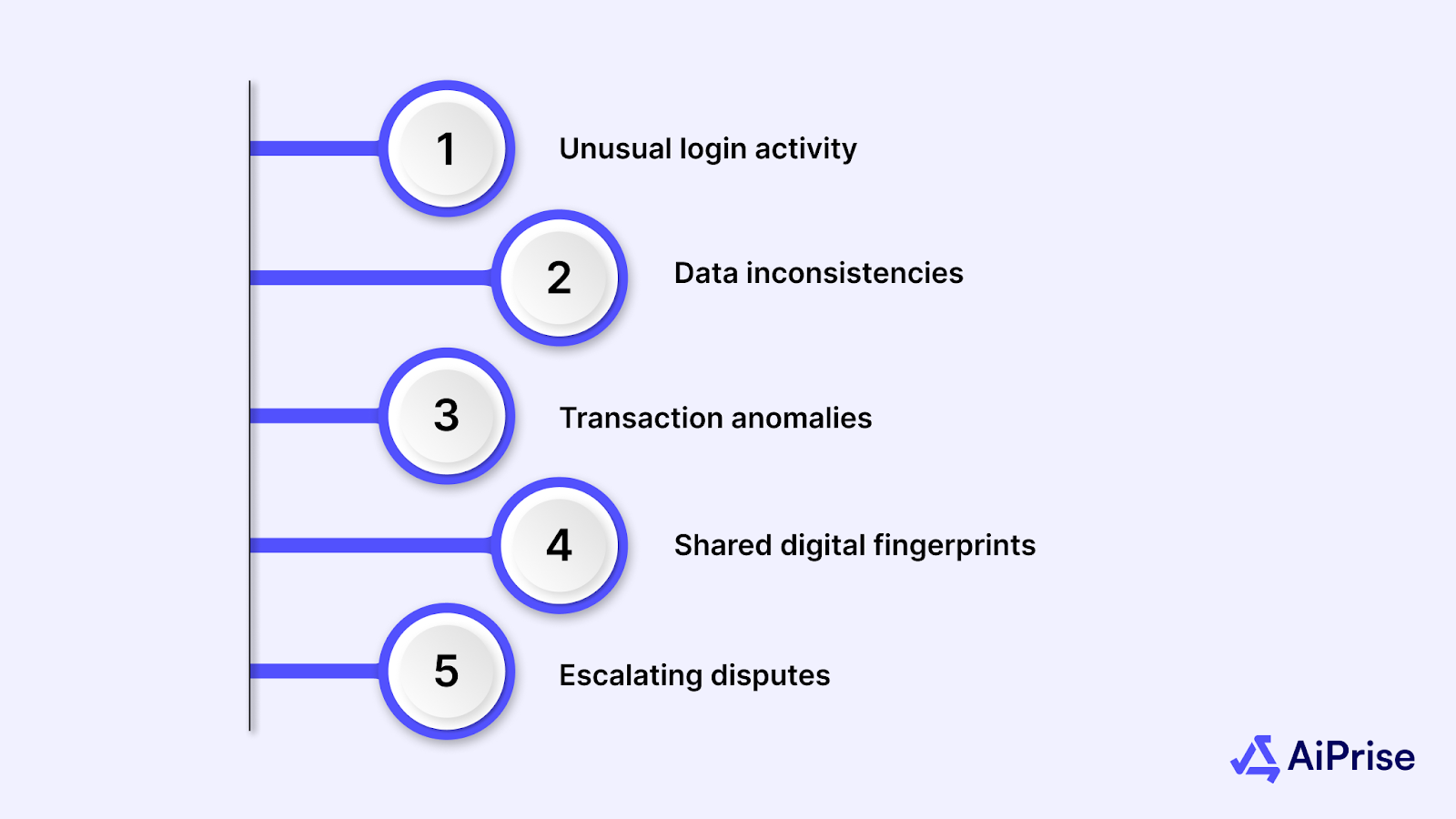

Signs of Potential Fintech Fraud Attempts

Spotting red flags early gives you the chance to stop fraud before it escalates. Below are some of the most common warning signals:

- Unusual login activity: Multiple failed attempts or logins from unfamiliar devices.

- Data inconsistencies: Mismatched addresses, phone numbers, or IDs.

- Transaction anomalies: High-frequency, small-dollar transfers that test your defenses.

- Shared digital fingerprints: Multiple accounts tied to the same device or IP.

- Escalating disputes: A sudden spike in chargebacks or refund requests.

Once you’re able to spot potential threats, the next step is figuring out how to detect them using the right tools and systems. Let’s take a look at how you can set up effective detection measures.

How to Detect Fintech Fraud?

Detection is about more than noticing unusual activity; it’s about using the right systems and tools to confirm, investigate, and stop fraud in real time. Implementing multiple layers of detection ensures that suspicious behavior doesn’t slip through the cracks. Here are the main techniques you can use to strengthen your defenses:

1. Rule-based alerts

These alerts trigger whenever a transaction exceeds predefined thresholds or breaks established rules. For example, if a single user suddenly tries to transfer an amount far higher than their typical activity, the system flags it immediately for review. Rule-based alerts act as your first line of defense against obvious fraudulent attempts.

2. Anomaly detection

Algorithms monitor patterns in user behavior and financial transactions to spot irregularities that don’t match historical trends. For instance, multiple logins from different countries within minutes can indicate account compromise. By continuously learning from past data, anomaly detection can identify subtle fraud attempts that human oversight might miss.

3. Behavioral analytics

This technique observes how users interact with your platform, including typing speed, mouse movements, touch gestures, or navigation patterns. Fraudsters often fail to replicate the subtle behaviors of legitimate users. For example, if a user suddenly starts navigating your payment portal in an unusual way, behavioral analytics can flag this activity for further investigation.

4. Graph analysis

Fraud is often not isolated; criminals operate in networks. Graph analysis maps the relationships between accounts, devices, IP addresses, and transactions to reveal hidden links. This helps detect coordinated attacks, such as multiple fake accounts funneling money to a single destination, which would be difficult to catch with traditional monitoring.

5. Liveness and deepfake checks

As fraudsters adopt sophisticated AI techniques like deepfakes, it’s crucial to verify that biometric data is genuine. Tools can confirm that facial scans, voice samples, or ID photos are real and captured in real time, preventing the use of manipulated or synthetic images. For example, a system can detect if someone is trying to bypass verification using a video replay instead of a live scan.

Once fraud is detected, timely prevention is the next step. Let’s explore some key strategies for halting fraud before it causes damage.

Also read: Understanding Fraud: Patterns and Prevention Strategies

How to Prevent Fintech Fraud?

Prevention is your best defense because it stops fraud before it impacts your system. By putting the right safeguards in place, you can reduce vulnerabilities and protect both revenue and reputation.

1. Strong Identity Verification

You need to enforce advanced onboarding that requires government-issued IDs, biometric checks, and database validation. This ensures you’re not letting synthetic or stolen identities slip through. Strong ID checks at the start cut down long-term fraud risks.

2. Enforce KYC and KYB Standards

KYC verifies individuals, while KYB validates the legitimacy of businesses. By collecting documents like incorporation papers and proof of beneficial ownership, you meet compliance requirements. These checks build trust with regulators and partners alike.

3. Multi-Factor Authentication (MFA)

Adding extra layers like SMS, authenticator apps, or hardware tokens significantly lowers account takeover risks. Adaptive MFA applies friction only when user behavior looks suspicious. This way, you balance user convenience with security.

4. Continuous Monitoring

Fraud doesn’t end after onboarding, so you must re-check identities regularly. Screening customers against updated sanctions lists or expired IDs helps you stay compliant. Real-time alerts catch fraudulent behavior before it causes major harm.

Even with solid prevention strategies, fraud may still find its way through. Knowing how to respond appropriately is crucial for minimizing the damage. Let’s discuss how you can manage fraud once it occurs.

Also read: Understanding Fraud Rings: How to Spot, Detect, and Prevent Them Safely

What Are Some Best Practices to Respond to Fintech Fraud?

Even with strong defenses, fraud can slip through your systems, and when it does, your response determines how much damage is contained. Here’s how you should react to protect your business and customers:

- Isolate the threat: Immediately freeze suspicious accounts or pause questionable transactions to prevent further losses. For example, if a payment processor notices a sudden spike in high-value transfers from a newly created account, halting those transactions can stop potential fraud in its tracks.

- Conduct investigation: Dive into logs, devices, and transaction histories to understand the scope and method of the attack. Tools like AiPrise can help you quickly verify identities and trace suspicious activities across accounts, making investigations more efficient and accurate.

- Recover and remediate: Reverse unauthorized charges whenever possible and notify affected customers to maintain trust. A cryptocurrency platform, for example, might roll back a suspicious transfer while alerting the user about the breach and next steps.

- Report activity: File Suspicious Activity Reports (SARs) or Suspicious Transaction Reports (STRs) with regulators as required by law. Payment providers, such as digital wallets, need to ensure compliance while providing a transparent record for regulatory audits.

- Feed insights back: Use the findings to update detection models, refine policies, and improve your defenses. For example, after investigating a fraud attempt, your system can flag similar behavioral patterns in future onboarding to prevent repeat attacks.

It’s also important to continuously refine your defenses based on past fraud events. Let’s see how AiPrise can help in strengthening your response and maintaining effective fraud detection and prevention systems.

Protect Your Business with AiPrise

AiPrise offers advanced tools to help you verify identities and assess business credibility, reducing exposure to fraud and compliance risks. Here’s why incorporating AiPrise into your processes can make a difference:

- KYC and KYB Verification: Ensure every individual and business you work with is legitimate by leveraging AI-driven checks that analyze IDs, documents, and business records.

- AML Monitoring: Detect and prevent money laundering activities with automated tools that screen transactions and flag suspicious behavior in real time.

- Biometric Authentication: Confirm identities with facial recognition, fingerprint scans, and voice verification, adding a secure layer beyond traditional documentation.

- Risk Assessment and Fraud Detection: Use data from over 100 sources, including government and financial registries, to identify high-risk clients and prevent fraudulent activity.

- Continuous Compliance Monitoring: Keep up with evolving regulations by tracking document expiration, sanction lists, and client transactions automatically.

- Seamless Integration: Easily embed AiPrise into your existing onboarding workflows to verify customers without slowing down operations, while reducing manual errors.

Final Thoughts

Fraud in fintech is an ever-evolving threat that can impact your revenue, reputation, and regulatory compliance if not addressed proactively. Understanding the types of fraud, recognizing warning signs, and implementing robust detection and prevention strategies are critical for staying ahead. By following best practices like stringent onboarding, continuous monitoring, and risk-based approaches, you can safeguard your business and maintain customer trust.

AiPrise provides the tools and technology to help you tackle these challenges with confidence. From AI-powered KYC and KYB verification to continuous AML monitoring and biometric authentication, AiPrise helps financial institutions, payment providers, and cryptocurrency platforms verify identities and reduce fraud risk efficiently.

Take control of your compliance and security today. Book A Demo to see how AiPrise can protect your business.

FAQ

1. Which technology is commonly used for fraud detection in fintech?

Artificial Intelligence (AI) and Machine Learning (ML) are commonly used for fraud detection in fintech. These technologies analyze large sets of transaction data in real-time, identifying patterns and anomalies that could indicate fraudulent activity.

2. What are the five key technologies in fintech?

The five key technologies in fintech include Artificial Intelligence (AI), Blockchain, Big Data, Cloud Computing, and Robotic Process Automation (RPA). These technologies help enhance security, streamline operations, and offer innovative financial solutions for businesses and consumers alike.

3. What are the 4 pillars of fraud risk management?

The four pillars of fraud risk management are prevention, detection, response, and monitoring. Financial institutions, payment providers, and cryptocurrency platforms use these pillars to establish comprehensive frameworks for identifying and mitigating fraud risks.

4. What is financial fraud prevention?

Financial fraud prevention refers to the strategies, processes, and technologies used to detect and prevent fraudulent activities in the financial sector. It involves safeguarding transactions, customer data, and systems from various types of financial fraud, including identity theft, phishing, and cybercrime.

5. What are the 4 R's to prevent fraud?

The 4 R’s to prevent fraud are Recognize, Respond, Report, and Recover. These steps guide institutions in identifying fraud risks, taking immediate action, reporting incidents, and recovering losses or restoring security after an event.

6. What are the 4 P’s of fraud?

The 4 P’s of fraud are Prevention, Detection, Response, and Prosecution. These principles are essential for financial institutions and payment providers to effectively mitigate fraud risks, ensuring a secure environment for customers and businesses.

You might want to read these...

.png)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately