AiPrise

12 min read

September 23, 2025

Understanding First-Party Risk and Fraud Management

Key Takeaways

First-party fraud is on the rise, and it’s costing businesses more than ever. In 2024, it accounted for 36% of all global fraud cases, a significant increase from 15% the previous year. This form of fraud, often perpetrated by the very customers who are supposed to be trusted, has become a major headache for companies across industries.

Whether it's chargebacks from consumers claiming they didn’t make a purchase or businesses faking financial records, first-party fraud presents significant risks to organizations. And the motivation behind it? Economic stress: 60% of first-party fraud offenders cite financial struggles as their primary driver.

As the lines between trustworthy customers and fraudsters blur, businesses must adapt and implement stronger safeguards to protect their finances, reputation, and customer relationships.

In this blog, we’ll explore the different types of first-party fraud, how it affects businesses, and the strategies you can use to protect your organization from this growing threat.

Key Takeaways

- First-party fraud involves customers or trusted insiders exploiting legitimate access for personal gain.

- Businesses must implement proactive measures like fraud detection systems, real-time monitoring, and transaction transparency to manage first-party risk.

- Educating customers about fraud, along with establishing clear policies on returns, refunds, and expenses, is crucial to prevent misuse.

- Regular audits, behavioral biometrics, and collaboration with financial institutions are key to strengthening fraud prevention.

- Taking action now can help businesses protect their finances and maintain customer trust.

What is First-Party Risk?

First-party risk refers to the potential for fraudulent activities or security breaches that originate from within an organization. Unlike external fraud, which comes from third parties such as cybercriminals or competitors, first-party fraud is carried out by trusted individuals within the company. These individuals may exploit their access to sensitive information, resources, or systems for personal gain, often using their knowledge of internal operations to bypass controls and avoid detection.

In the context of financial institutions, e-commerce, and payment services, first-party risk occurs when customers or merchants exploit their legitimate access to goods, services, or credit for malicious purposes. This type of risk is especially challenging because the perpetrators often appear as trusted or legitimate entities, making it harder to detect fraud.

To fully understand the magnitude of this risk, let's take a closer look at its scope and impact on businesses across industries.

The Scope and Impact of First-Party Risk

First-party risk might sound like a technical term, but it’s something every business needs to pay attention to. It’s about the risks that arise when someone uses their own identity to commit fraud or take advantage of a system. And while it may seem like a victimless crime, the truth is, it can lead to serious consequences for businesses.

Here’s how it can impact businesses:

- Financial Losses: First-party fraud can drain your profits quickly. Whether it’s through fake chargebacks, where a customer buys something and later claims they never received it, or by applying for loans with no intention of paying them back, these scams hurt the bottom line.

- Increased Costs: Combatting first-party fraud often means investing in technology and staff to monitor transactions. Businesses need to spend on fraud detection tools, conduct manual checks, and in some cases, even go through lengthy legal processes to deal with the fallout.

- Damage to Reputation: One of the most dangerous impacts of first-party fraud is the damage it does to a company’s reputation. If customers feel like their data isn’t being protected or that fraud is going unchecked, trust erodes. That can lead to fewer customers, lost business, and a tarnished brand.

- Legal and Compliance Risks: In some industries, failing to catch and address first-party fraud can result in legal consequences. For example, businesses in the financial sector are expected to follow strict laws around fraud prevention and can face fines or penalties if they don’t meet compliance standards.

- Wider Economic Impact: When businesses fall victim to first-party fraud, it doesn’t just hurt them—it can affect entire industries. If fraud becomes widespread, it creates instability in financial markets and makes everyone more vulnerable.

First-party risk is challenging to manage because the individual committing the fraud is using their own credentials, making it more difficult for businesses and financial institutions to differentiate between legitimate activities and fraudulent behavior. Consequently, businesses must be proactive and employ strong fraud detection and prevention measures to protect themselves from these risks.

Now that we know how first-party risk impacts businesses, let’s break down the various types of first-party fraud, each with its own set of risks.

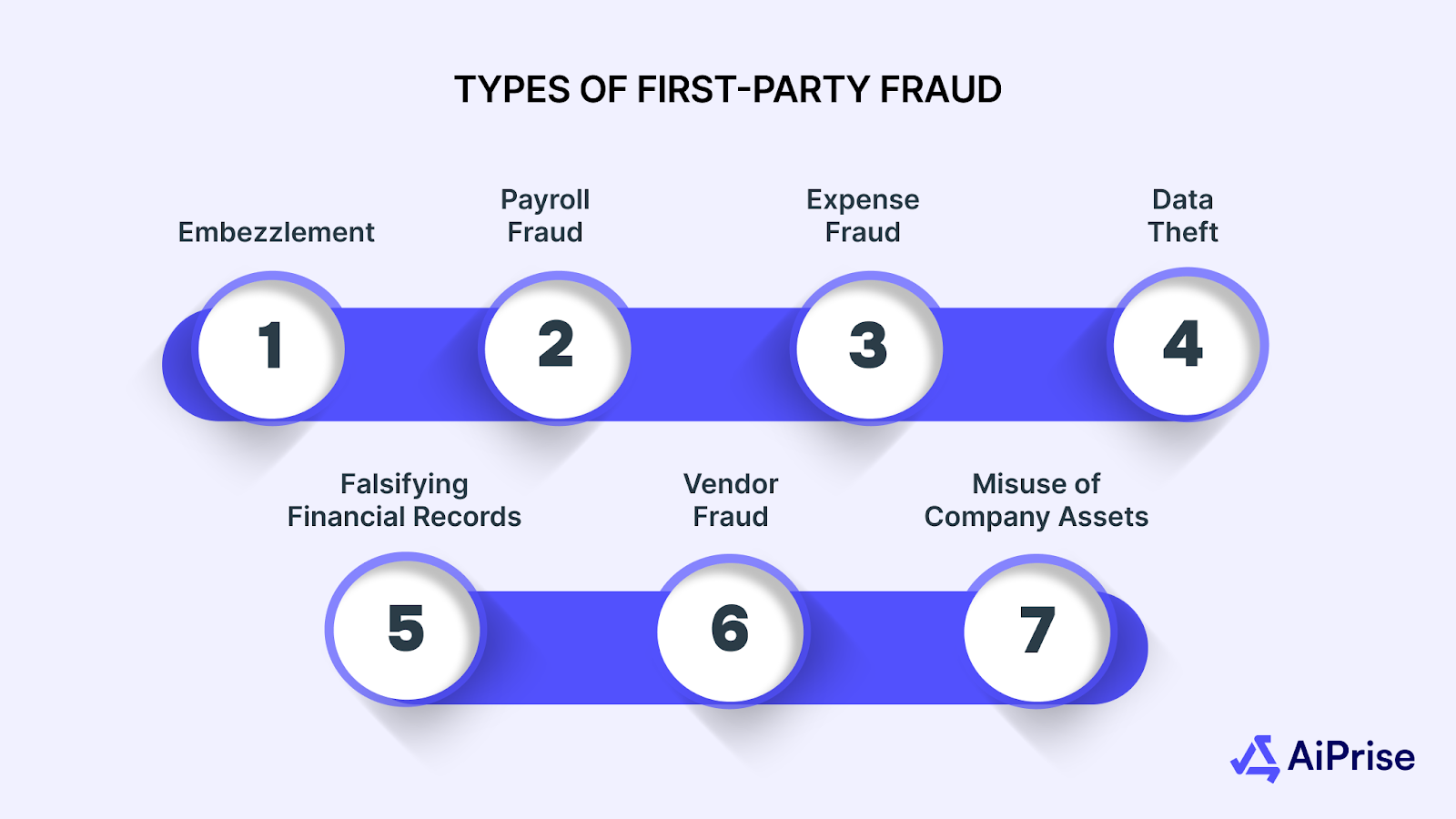

Types of First-Party Fraud

First-party fraud can take many forms, but all share one common thread: they are committed by trusted individuals within the organization. Unlike third-party fraud, where someone else’s identity is used, first-party fraud can be harder to detect because the fraudster’s credentials appear legitimate. Let’s learn the different types of first-party fraud and how they can affect businesses:

1. Embezzlement

Embezzlement occurs when an employee or trusted person steals funds or resources that they have access to, often over a long period. The individual may siphon off small amounts, which may go unnoticed initially, but over time, these thefts can add up to significant losses.

The common red flags include:

- Unexplained discrepancies in financial records

- Employees who appear to be living beyond their means

- Large sums of money that can’t be traced or accounted for

In 2018, a former Apple employee was sentenced to prison for embezzling over $17 million from the company during his seven-year tenure. He used his position to manipulate purchasing processes and divert funds into his personal accounts.

2. Payroll Fraud

Payroll fraud happens when an employee manipulates the payroll system to steal money. This could be done by creating fake employees, inflating hours worked, or collecting pay for hours not worked.

Common schemes include:

- Ghost Employees: Creating fictitious employees to collect salaries.

- Timesheet Fraud: Inflating hours worked or "buddy punching" (where one employee clocks in or out for another).

- Pay Rate Alteration: Unauthorized changes to pay rates.

3. Expense Fraud

Employees can take advantage of company expense reimbursement policies by submitting fake or inflated expense claims. This can range from simple exaggerations of actual expenses to entirely fabricated invoices for goods or services that were never purchased.

What to watch for:

- Frequent claims for personal expenses

- Repeated claims for meals, travel, or supplies that are difficult to verify

- Duplicate or fictitious receipts

4. Data Theft

Data theft is another type of first-party fraud, where an insider steals valuable information, such as financial records, trade secrets, or sensitive customer data. This can be done for personal gain, to sell the information, or to harm the company.

Signs of potential data theft:

- Unusual access to confidential information by employees

- Unauthorized transfer of sensitive data to personal devices or external storage

- Employees accessing data that is not relevant to their job responsibilities

5. Falsifying Financial Records

Employees or contractors in charge of financial reporting may falsify records to cover up misappropriations, manipulate profits, or hide losses. This form of fraud can mislead stakeholders, auditors, and regulators, leading to severe legal and financial consequences for the business.

Look out for:

- Inconsistent accounting entries or records

- Delayed or unusual changes to financial statements

- Employees resisting financial audits or questions about records

The Enron scandal is a notorious case where executives used accounting loopholes and special purpose identities to hide debt and promote profits, leading to one of the largest corporate bankruptcies in U.S. history.

6. Vendor Fraud

In vendor fraud, an employee may collude with a third-party vendor to inflate invoices, charge for goods or services not delivered, or divert funds intended for legitimate business expenses.

Common signs:

- Unexplained relationships between employees and vendors

- Unusually high or repetitive payments to the same vendor

- Irregularities in procurement and delivery logs

7. Misuse of Company Assets

Company assets such as vehicles, office supplies, or IT equipment can be misused by employees for personal gain. This can involve taking home company equipment, using company resources for personal projects, or even selling company assets without authorization.

Signs to watch for:

- Missing or unaccounted-for company assets

- Employees claiming excessive personal use of company property

- Unusually high repairs or replacements for office equipment or vehicles

Having explored the types of fraud, the next step is to discuss effective strategies for managing and mitigating first-party risks.

Mitigation Strategies and Tips for First-Party Risks

First-party fraud—often referred to as "friendly fraud"—occurs when customers exploit their relationship with a business for personal gain.

To effectively mitigate first-party risks, businesses need to adopt a proactive and comprehensive fraud prevention approach that combines technological solutions, process improvements, and cultural shifts.

1. Enhance Transaction Transparency

Clear and consistent transaction records can deter fraudulent behavior. Ensure that all transactions are well-documented and easily traceable. This transparency not only helps in identifying discrepancies but also builds trust with customers.

Implementation Tips:

- Provide detailed receipts and statements that clearly outline transaction information.

- Ensure that billing descriptors are easily recognizable to customers to reduce confusion.

- Implement a clear and consistent process for handling disputes and chargebacks.

2. Implement Real-Time Monitoring Systems

Utilize advanced monitoring tools to track customer activities in real-time. These systems can flag unusual patterns, such as rapid spending or frequent chargebacks, allowing for prompt investigation and response.

Implementation Tips:

- Use machine learning algorithms to pick out anomalies in transaction patterns.

- Set up alerts for strange activities, such as multiple high-value transactions in a short period.

- Regularly review and update monitoring criteria to adapt to emerging fraud tactics.

3. Utilize Behavioral Biometrics

Incorporate behavioral biometrics to analyze user interactions, such as typing speed and mouse movements. This technology can detect symptoms that may indicate fraudulent activities, even if the user’s identity appears legitimate.

Implementation Tips:

- Integrate behavioral biometric solutions into your authentication processes.

- Monitor for deviations from established user behavior patterns.

- Combine behavioral biometrics with other authentication methods for enhanced security.

4. Conduct Regular Audits

Periodic audits help in detecting inconsistencies and potential fraud. By reviewing transaction histories and account activities, businesses can identify red flags early and take corrective actions.

Implementation Tips:

- Schedule both regular internal and external audits to review financial records and transactions.

- Establish a process for investigating and addressing audit findings promptly.

- Use audit results to refine and improve fraud prevention strategies.

5. Educate Customers on Fraud Awareness

Inform customers about the risks of first-party fraud and encourage them to report suspicious activities. An educated customer base can serve as an additional layer of defense against fraudulent actions.

Implementation Tips:

- Provide resources and training to customers on recognizing and preventing fraud.

- Encourage customers to lodge complaints about any suspicious activities or discrepancies in their accounts.

- Offer incentives for customers who proactively participate in fraud prevention efforts.

6. Establish Clear Return and Refund Policies

Ambiguous return and refund policies can be exploited. Clearly define these policies and ensure they are communicated effectively to customers to prevent misuse.

Implementation Tips:

- Develop and publish clear return and refund policies on your website and at points of sale.

- Train staff to enforce these policies consistently and fairly.

- Monitor return and refund transactions for patterns that may indicate fraudulent activity.

7. Collaborate with Financial Institutions

Work closely with banks and their payment processors to share information about suspicious activities. This collaboration can help in identifying and preventing fraudulent transactions before they escalate.

Implementation Tips:

- Establish communication channels with financial institutions to report and discuss potential fraud cases.

- Participate in industry platforms and networks to stay informed about emerging fraud trends.

- Implement joint initiatives with financial institutions to enhance fraud prevention efforts.

8. Leverage Artificial Intelligence and Machine Learning

Implement AI and ML algorithms to analyze large datasets and detect patterns indicative of fraud. These technologies can adapt to evolving fraud tactics, providing a dynamic defense mechanism.

Implementation Tips:

- Invest in AI and ML solutions that are specifically designed for fraud detection.

- Regularly update and train AI models to improve accuracy and effectiveness.

- Combine AI and ML with traditional fraud detection methods for a comprehensive approach.

9. Maintain a Robust Incident Response Plan

Prepare for potential fraud incidents by having a clear and actionable response plan in place. This plan should outline steps for investigation, communication, and resolution to minimize damage.

Implementation Tips:

- Develop and record an incident response plan that carries roles, responsibilities, and procedures.

- Conduct regular drills and simulations to assess the efficiency of the plan.

- Review and update the plan time to time to address new threats and challenges.

With these mitigation strategies in mind, it’s clear that businesses need the right tools and systems to stay ahead of fraud. Let’s look at how businesses can tackle first-party fraud while ensuring compliance and safeguarding their reputation.

Build and Maintain Your Fraud Compliance with AiPrise

Managing fraud and ensuring compliance can be complex, especially when operating globally. AiPrise provides a reliable platform that simplifies the process of verifying identities, managing risk, and staying compliant with ever-evolving regulations.

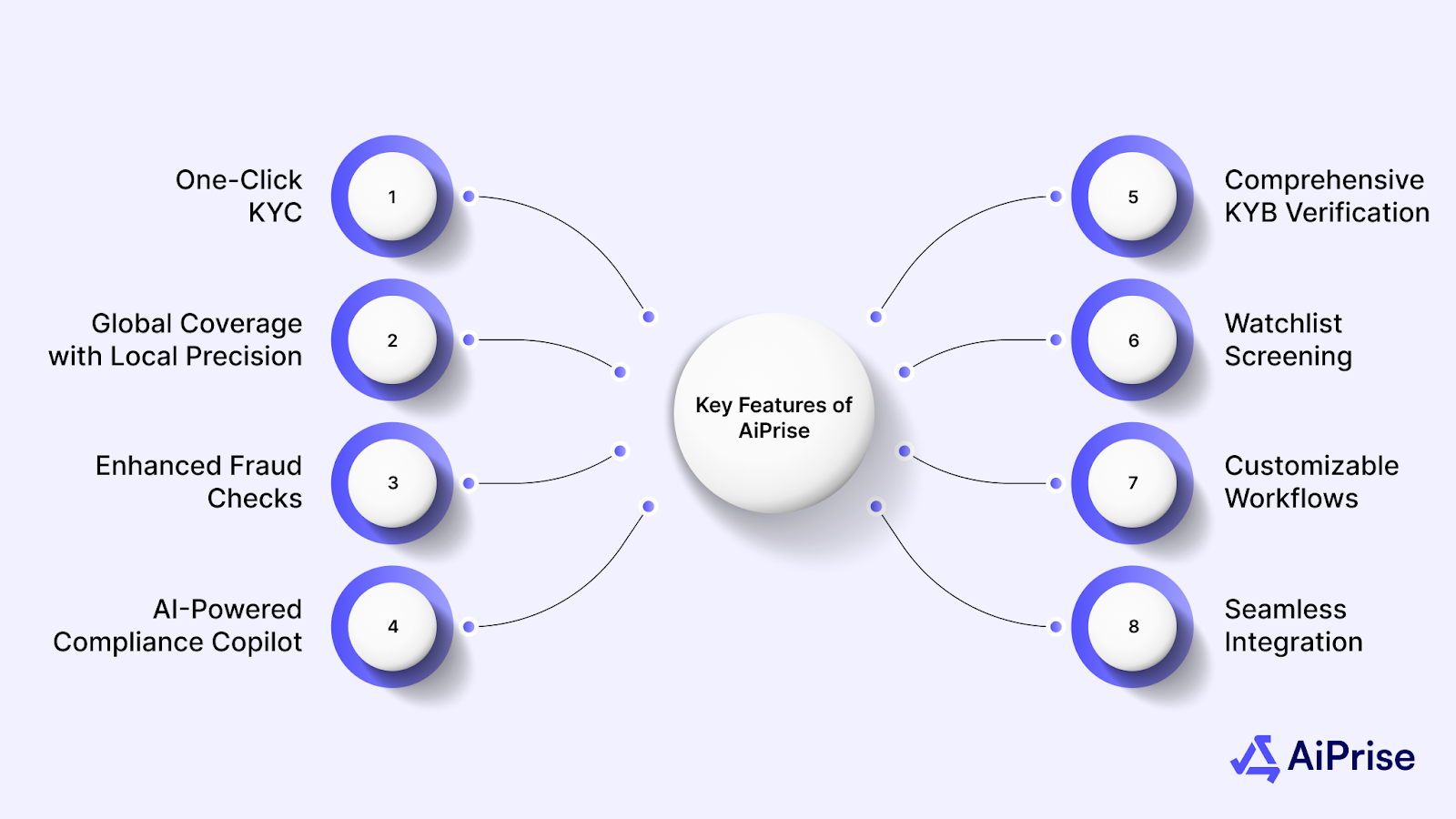

Key Features of AiPrise

- One-Click KYC: Simplify identity verification with just an ID number and a selfie, enhancing user experience and compliance.

- Global Coverage with Local Precision: Verify identities across 200+ countries, supporting local ID cards, passports, and driver's licenses.

- Enhanced Fraud Checks: Utilize advanced phone number, email, and device intelligence checks to detect and prevent fraud at onboarding.

- AI-Powered Compliance Copilot: Automate routine compliance tasks, reducing manual review time by up to 95% and ensuring adherence to global regulations.

- Comprehensive KYB Verification: Perform thorough business verification, including UBO checks, tax/VAT number validation, and online presence analysis.

- Watchlist Screening: Screen customers and transactions against global sanctions lists, PEPs, and adverse media to mitigate financial crime risks.

- Customizable Workflows: Design and manage end-to-end onboarding journeys with flexibility and precision, tailored to your business needs.

- Seamless Integration: Integrate AiPrise's solutions into your existing systems with ease, enhancing operational efficiency and scalability.

Don't let fraud and compliance challenges hold your business back. With AiPrise, you can streamline your processes, reduce risks, and build trust with your customers.

Conclusion

As fraud tactics become more sophisticated, businesses must adapt by integrating smarter, more efficient solutions that prevent fraud and build trust with customers. It’s time to shift the focus from just detecting fraud to actively preventing it. Businesses that stay ahead in the race will safeguard their assets, preserve their reputation, and build stronger, more secure customer relationships.

If you’re looking for a way to reduce fraud risk and ensure compliance, start by learning more about how intelligent verification tools can help protect your business.

AiPrise offers advanced solutions to help businesses prevent and detect first-party fraud. With our powerful AI and machine learning tools, you can ensure secure customer onboarding, reduce fraud risk, and maintain compliance effortlessly. Explore how advanced solutions can strengthen your fraud prevention strategy and secure your business's future. Book A Demo Today!

FAQs

1. What industries are most vulnerable to first-party fraud?

Industries such as finance, e-commerce, and healthcare are particularly vulnerable to first-party fraud due to the high volume of transactions, sensitive data handling, and reliance on trust between customers and businesses.

2. Can first-party fraud be committed by contractors or vendors?

Yes, contractors or vendors with legitimate access to a company’s systems or resources can also commit first-party fraud, such as inflating invoices or stealing confidential information.

3. What role does employee access play in first-party fraud?

Employees with unrestricted access to financial records, data, or internal systems are at higher risk of committing first-party fraud. Limiting access to sensitive details based on job responsibilities is key to reducing this risk.

4. How do businesses detect first-party fraud if the fraudster has legitimate access?

Businesses can detect first-party fraud by implementing monitoring systems that track unusual activities or behaviors, such as excessive refunds, unapproved data access, or discrepancies in financial reports.

5. What steps should a company take if it detects first-party fraud?

Upon detecting first-party fraud, companies should immediately conduct a thorough investigation, report the incident to the relevant authorities if necessary, and reassess their fraud prevention measures to avoid future occurrences.

You might want to read these...

.png)

.png)

.png)

.png)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately