AiPrise

9 mins read

July 8, 2026

AML Fines Explained: Key Facts and Examples

Key Takeaways

Staying compliant with anti-money laundering (AML) regulations is key to protecting your organization’s reputation and avoiding serious fines. The cost of non-compliance is far greater than you might expect, with fines and legal consequences that can have long-lasting effects.

Recently, OKX, a major cryptocurrency exchange, pleaded guilty to violating U.S. AML laws. They agreed to pay over $500 million in penalties for failing to prevent money laundering. This case highlights the serious risks faced by businesses in sectors like finance and cryptocurrency.

In this blog, we’ll discuss the consequences of failing to meet AML requirements, focusing on major fines and penalties. We’ll also look at key steps for AML compliance and introduce tools that help mitigate these risks.

Key Takeaways

- Anti-money laundering fines can reach billions, significantly impacting businesses financially and reputationally.

- Common causes for fines include poor customer verification, weak monitoring systems, and inadequate reporting.

- Major financial institutions like BNP Paribas and Goldman Sachs have paid huge fines for AML violations.

- Certain sectors, like banking and cryptocurrency, face more AML penalties due to higher risk exposure.

- AiPrise offers tools that help businesses automate AML compliance and reduce the risk of penalties.

What Are AML Fines and When Are They Issued?

Regulators issue AML fines to businesses that don't follow AML regulations. Companies that handle financial transactions, including banks, must monitor activity and report any suspicious behavior.

AML fines are typically issued when an organization fails to implement proper safeguards, like conducting thorough customer checks or monitoring transactions for signs of illegal activity.

Why Are AML Fines Issued?

Some common reasons businesses face AML fines include:

- Failure to perform customer due diligence where businesses don't verify customer identities and associated risks.

- Not monitoring financial transactions for suspicious activities or not having strong internal controls in place

- Not filing Suspicious Activity Reports (SARs) even if a business detects suspicious activity

- Non-compliance with international sanctions

- Lack of employee training

Industries with Higher AML Compliance Risk

AML enforcement actions are often associated with the following industries:

- Banks: Because they process large volumes of domestic and international transactions, have extensive customer networks and exposure to cross-border activity.

- Cryptocurrency Exchanges: Susceptible because of their anonymous nature and cross-border transactions.

- Gambling and Gaming Operators: Because they work with high volumes of transactions and there’s potential for anonymity.

- FinTechs and Payment Providers: Many of these businesses provide services that can be misused for money laundering, especially when dealing with large volumes of transactions.

AML Fines Around the World: Trends, Cases, and Consequences

Let’s take a closer look at some of the recent AML fines as well as a few older landmark ones.

1. BNP Paribas – $8.9 Billion Fine (2014)

In 2014, BNP Paribas, one of the world’s largest banks, was fined $8.9 billion by U.S. authorities. The bank had violated U.S. sanctions by processing transactions for countries like Sudan, Iran, and Cuba.

2. Goldman Sachs: $2.9 Billion Fine (2020)

Goldman Sachs faced a $2.9 billion fine in 2020 after being found guilty of enabling money laundering through its involvement in the 1MDB scandal. The scandal involved billions of dollars misappropriated from a Malaysian government-owned investment fund. The fine was part of a global settlement with various regulators to resolve criminal charges.

3. Danske Bank: Over $2 Billion Fine (2022)

Danske Bank was fined over $2 billion after an investigation found it allowed over $200 billion in illicit transactions. The fine resulted from poor oversight and weak controls in its Estonian branch.

4. HSBC: $1.9 Billion Fine (2012)

In 2012, HSBC was fined $1.9 billion for aiding money laundering by drug cartels and terrorist organizations. The U.S. Department of Justice found that HSBC’s internal controls failed to prevent the transfer of illegal funds.

5. UBS: $1.4 Billion Fine (2023)

UBS, a Swiss multinational investment bank, was fined $1.4 billion in 2023. The fine came after investigations revealed that the bank facilitated suspicious transactions, particularly in connection with clients in high-risk countries.

6. Block, Inc.: $80 Million Fine (2025)

Block, the company behind Cash App, agreed to pay an $80 million penalty in a multistate settlement with 48 state financial regulators.

Regulators found violations of BSA and AML requirements and also identified shortcomings in the company's compliance program. Alongside the financial penalty, Block agreed to hire an independent consultant to review its BSA/AML controls and address any deficiencies identified during the review.

7. Barclays: £42 Million Fine (2025)

The FCA fined Barclays more than £42 million for failures in managing money laundering risks across two separate cases.

In one case, Barclays opened a client money account for WealthTek without gathering enough information about the firm's business or regulatory permissions. Clients later deposited £34 million into the account. Barclays has also agreed to make a voluntary payment of £6.3 million to affected WealthTek clients.

In a separate case, the FCA fined Barclays £39.3 million for failing to carry out adequate due diligence and ongoing monitoring of Stunt & Co. During the banking relationship, the firm received £46.8 million from Fowler Oldfield, a multimillion-pound money laundering operation.

8. Coinbase Europe: €21.5 Million Fine (2025)

Ireland's Central Bank fined Coinbase Europe €21.5 million for not following AML and counter-terrorist financing (CTF) guidelines.

The regulators found that there were deficiencies in their transaction monitoring system. Due to this, 30 million transactions worth over €176 billion were not properly tracked.

Coinbase later reviewed the affected transactions and reported 2,708 suspicious transactions linked to money laundering, fraud, drug trafficking, cybercrime, and child sexual exploitation.

9. Binance: $4.3 Billion Settlement (2023)

Binance had to pay more than $4.3 billion to settle investigations by the U.S. Department of the Treasury over violations of the Bank Secrecy Act (BSA) and multiple sanctions programs.

Regulators found that Binance failed to implement effective AML and sanctions controls. They had allowed transactions involving terrorist groups, ransomware operators, and money launderers in sanctioned jurisdictions. As part of the settlement, Binance agreed to strengthen its compliance program and operate under an independent monitorship for five years.

10. TD Bank: $1.3 Billion Penalty (2024)

FinCEN imposed a record $1.3 billion penalty on TD Bank after concluding that the bank couldn't maintain a proper AML program for over a decade. The bank allowed suspicious activity linked to fentanyl trafficking, human trafficking, terrorist financing, and other financial crimes without timely reporting.

FinCEN also cited weaknesses in transaction monitoring and also large backlogs of unreviewed alerts. There was also inadequate oversight of peer-to-peer payment channels such as Venmo and Zelle and failures to detect suspicious activity involving the bank's own employees.

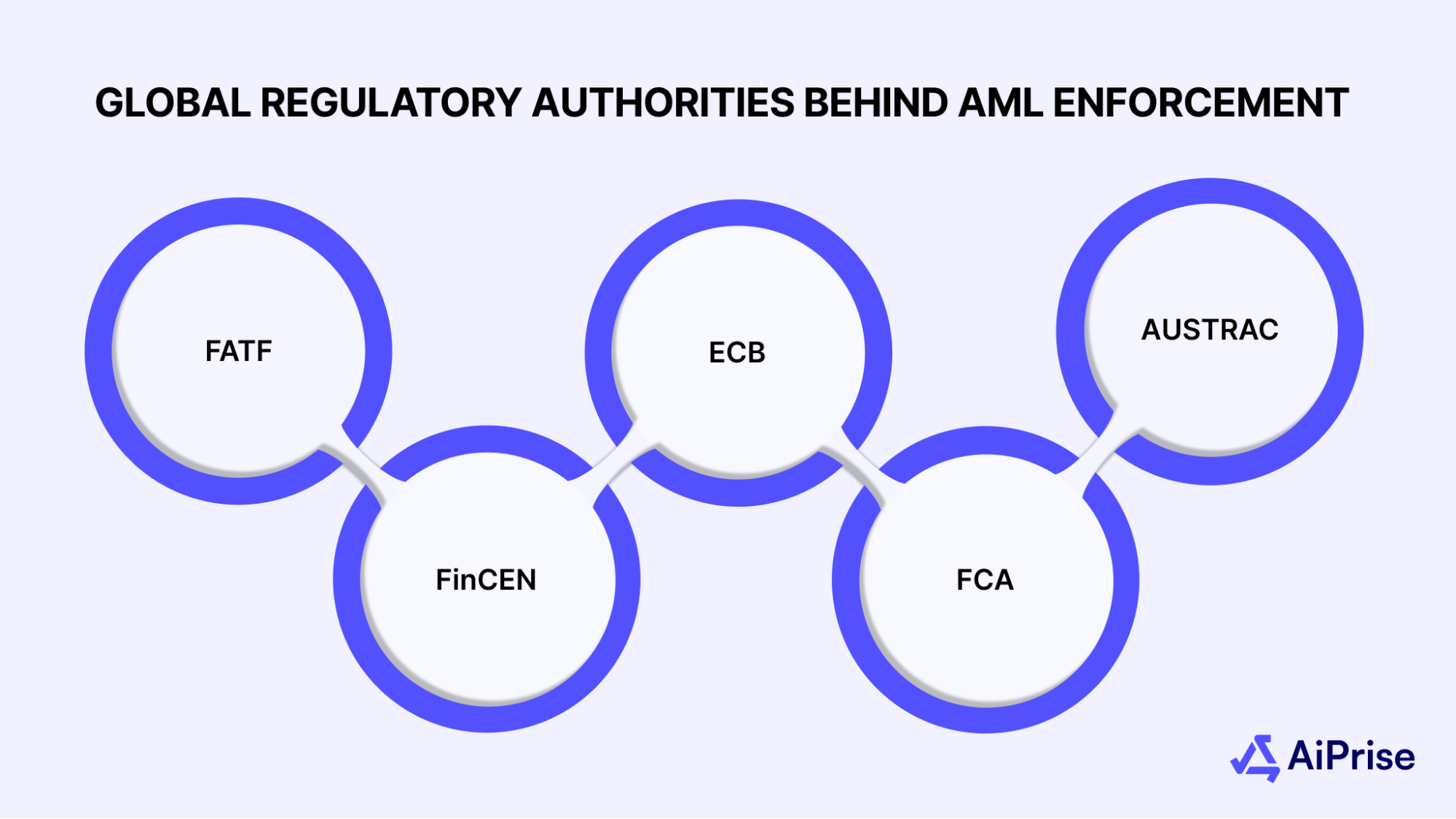

Global Regulatory Authorities Behind AML Enforcement

Several global regulators enforce AML laws, setting standards, investigating violations, and imposing fines.

Below are some of the most influential regulatory bodies behind AML enforcement:

- The Financial Action Task Force (FATF): FATF is a global organization that sets standards for preventing money laundering and terrorism financing. It monitors compliance across member countries and issues recommendations on how to improve AML frameworks.

- Financial Crimes Enforcement Network (FinCEN): A division of the U.S. Department of the Treasury, FinCEN enforces AML regulations in the United States. It monitors financial institutions, issues penalties for violations, and ensures that businesses comply with federal AML laws.

- European Central Bank (ECB): The ECB plays a critical role in overseeing AML regulations across the European Union. It sets regulatory frameworks and works with national authorities to monitor compliance across the region.

- The UK’s Financial Conduct Authority (FCA): The FCA regulates financial markets in the UK and ensures that institutions follow AML laws. It also has the power to fine those who don’t comply.

- The Australian Transaction Reports and Analysis Centre (AUSTRAC): AUSTRAC is responsible for regulating and ensuring compliance with AML and counter-terrorism financing laws in Australia. It monitors financial transactions and guides AML compliance for businesses.

Although regulatory authorities set the rules, businesses must take the next step by ensuring their processes are aligned with these standards.

Key Factors Behind AML Fines

Regulators weigh several factors before deciding an AML fine:

- Severity of the violations

- Duration of violations before they were addressed

- The amount of money involved

- Whether the organization has committed similar violations before

- Whether the organization cooperated during the investigation and took corrective action

- Whether the business had proper AML controls, transaction monitoring, and reporting processes in place

How AiPrise Helps Strengthen Your Compliance Tools

AiPrise offers advanced solutions designed to help businesses meet AML and KYC requirements. The platform integrates machine learning and AI to improve identity verification, enhance risk management, and ensure regulatory compliance.

Here are some of the key features that AiPrise provides to support your AML and KYC requirements:

- Comprehensive ID Crosscheck: AiPrise verifies customer identities using multiple data points, including government databases, MRZ, and barcode scanning.

- Government Verifications: The platform integrates directly with government databases, offering more reliable verification against official records.

- Case Management: AiPrise centralises AML investigations by allowing compliance teams to assign, track, document, and resolve alerts in one place.

- Watchlist Screening: AiPrise screens transactions against global sanction lists and watchlists, helping businesses stay compliant with international regulations and avoid high-risk transactions.

- Onboarding SDK: The platform offers a user-friendly SDK that enables businesses to integrate KYC and AML checks directly into their client onboarding process.

- Automated Workflows: AiPrise provides customizable, automated workflows to ensure that all necessary compliance steps are followed consistently, reducing the likelihood of errors and missed deadlines.

- One-Click KYC: AiPrise offers a one-click KYC solution that simplifies the verification process for businesses and their customers.

- Reverification: AiPrise enables businesses to periodically reverify client information, helping to detect changes in risk profiles and ensure that customer data remains current.

- Document Insights: The platform analyzes documents submitted by clients, ensuring that only valid and authentic documents are accepted and reducing the risk of document fraud.

Case Study: Keyrails + AiPrise

With a compliance team of fewer than five people, Keyrails was looking for a better way to manage customer onboarding and risk assessments.

Before AiPrise, the team was using multiple tools to verify documents, review KYC data, and conduct screening. This made the whole process slow and manual.

AiPrise brought document verification, sanctions screening, onboarding workflows, and risk assessments into a single platform. The company also configured its own customer risk model within the system to match its compliance requirements.

As a result, verification and compliance reviews dropped from taking several days to same-day or next-day completion.

Turn AML Compliance Into a Competitive Advantage

AML compliance is crucial for businesses to build trust and avoid hefty penalties. As the large fines against financial institutions show, failing to comply can cause serious financial and reputational harm. With increasing scrutiny on various industries, effective compliance measures are key to long-term success.

AiPrise offers a solution to help businesses stay ahead of regulatory requirements and prevent financial crimes. Its advanced KYC and AML tools simplify the compliance process and reduce risks. Whether you’re managing transactions, verifying identities, or screening for suspicious activity, AiPrise provides the support you need to stay compliant.

Ready to strengthen your compliance efforts and prevent costly fines? Book a demo with AiPrise today and explore how our automated compliance tools can help safeguard your business and improve operational efficiency.

FAQs

What are the consequences of non-compliance with AML regulations?

Non-compliance with AML regulations can lead to severe financial penalties, legal repercussions, and significant damage to a company’s reputation. Businesses may also face restrictions on their operations. In serious cases, regulators may suspend or revoke business licences, seize assets linked to criminal activity, and appoint independent monitors.

What are the 8 AML priorities?

The U.S. AML framework identifies eight priority areas for combating financial crime:

- Corruption

- Cybercrime

- Terrorist financing

- Fraud

- Transnational criminal organizations

- Drug trafficking

- Human trafficking and human smuggling

- Proliferation financing

Can organizations appeal AML fines?

Yes. In many jurisdictions, organizations can appeal AML fines if they believe the decision or penalty is unfair. The appeal process varies by country and regulator, and businesses are typically required to provide evidence to support their case.

How does the AML investigation process work?

A typical AML investigation follows these steps:

- Alert generation: A monitoring system or employee flags suspicious activity.

- Review: The compliance team examines the alert and gathers relevant information.

- Investigation: Analysts assess the customer's transactions and supporting documents.

- Case decision: If concerns remain, the organisation files a SAR, where required.

- Ongoing monitoring: The customer or account continues to be monitored.

What is the role of KYC in AML compliance?

KYC helps businesses verify the identity of their clients, assess risks, and ensure that they are not facilitating money laundering or other financial crimes.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately