AiPrise

18 min read

December 17, 2025

Advanced Payment Gateway Fraud Detection Strategies

.png)

Key Takeaways

In 2026, payment gateways sit at the center of how businesses accept money, yet fraud continues to be a top threat. On average, payment fraud activities accounted for roughly 3.5% of attempted transactions in Q2 2026, with traditional methods like credit and debit cards still being the most exploited vectors.

For you as a payment provider, fintech operator, or merchant, that means fraud is not just a data headache; it’s a direct hit on your revenue, customer trust, and compliance obligations. As fraudsters use AI, synthetic identities, and ever more sophisticated tactics, legacy rule-based systems struggle to keep pace.

The result is missed fraud, false positives that hurt conversions, and rising compliance pressure from regulators and partners. In this blog, you’ll learn why fraud detection matters today and the advanced strategies that modern payment gateways use to stay secure and competitive.

Key Takeaways - At a Glance

- Payment gateway fraud in 2026 targets transactions, identities, merchants, and compliance gaps, making single-layer controls ineffective.

- Advanced fraud detection relies on early risk signals, continuous monitoring, and context-aware decisions across the payment lifecycle.

- Strategies like device intelligence, anomaly detection, consortium data, and pre-authorization scoring help reduce fraud without hurting approvals.

- Common challenges such as false positives, scaling into new markets, and operational overload require adaptive and integrated risk controls.

- AiPrise strengthens fraud detection by unifying fraud intelligence with global KYC, KYB, and AML to improve accuracy, compliance, and scale.

What Makes Payment Gateway Fraud Detection Critical in 2026?

In 2026, you are no longer just processing payments. You are managing instant money movement, cross-border flows, embedded checkout experiences, and complex partner ecosystems.

Fraud detection now sits directly inside your payment performance, partner approvals, and customer experience. One weak control can expose you to network bans, partner churn, or sudden volume caps. If your fraud stack does not evolve with how payments move today, it becomes a growth blocker instead of a safety layer.

Here are the core reasons fraud detection is business-critical for you in 2026:

- Instant Payments Leave No Recovery Window: When you support real-time payouts or faster settlement rails, you lose the option to investigate later. You must decide correctly before money moves.

- Payment Orchestration Increases Blind Spots: If you route transactions across multiple PSPs or acquirers, inconsistent risk signals can hide coordinated fraud patterns unless detection is centralized.

- Embedded Finance Expands Your Risk Surface: When marketplaces or SaaS platforms embed your gateway, their user behavior becomes your fraud exposure, even if you do not control onboarding.

- Network and Card Scheme Scrutiny Is Tighter: High-risk ratios can trigger AiPrise programs, fee hikes, or even processing restrictions that directly limit your transaction volumes.

- Merchant Trust Depends On Approval Quality: Your merchants judge you by clean approvals, not just high acceptance. Poor fraud decisions push good merchants to competing gateways.

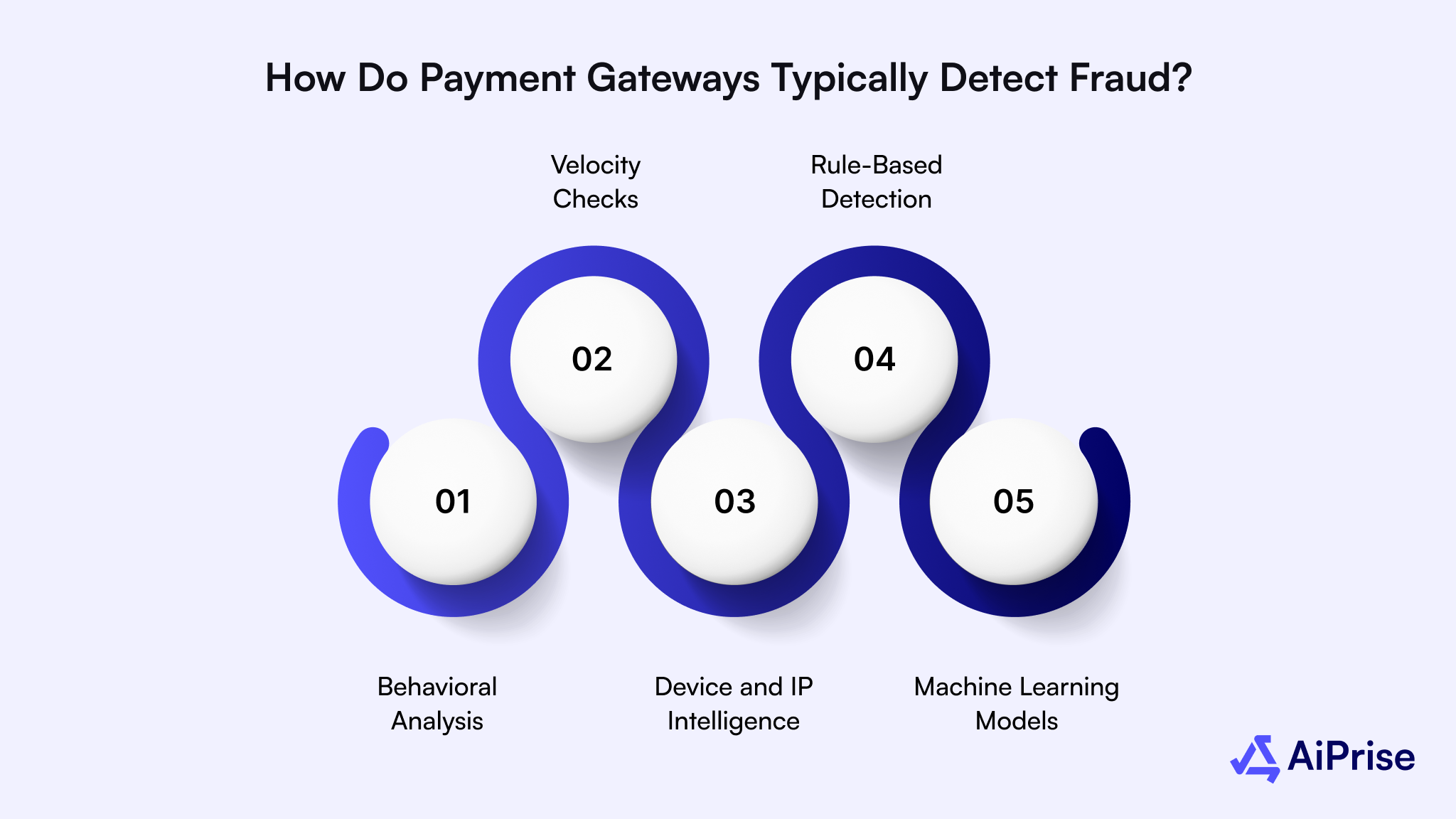

How Do Payment Gateways Typically Detect Fraud?

When you run a payment gateway, fraud detection happens across multiple checkpoints within the transaction flow. You are not relying on a single signal. Instead, you combine data from the moment a payment is initiated to the final authorization response.

Each layer answers a different risk question, such as who is paying, how they behave, and whether the transaction fits known safe patterns.

Below are the common ways you typically detect fraud today:

- Behavioral Analysis: You monitor how users interact during checkout, such as typing speed, retry behavior, or sudden changes in purchase flow, to spot abnormal intent.

- Velocity Checks: You flag unusual spikes, like multiple cards used from one account or repeated attempts within seconds, which often signal automated abuse.

- Device and IP Intelligence: You assess device attributes and network data to identify risky locations, anonymizers, or mismatched device histories.

- Rule-Based Detection: You apply predefined conditions, such as amount thresholds or blocked regions, to stop known fraud patterns quickly.

- Machine Learning Models: You use trained models that score transactions based on historical outcomes, adapting over time as new fraud patterns emerge.

Also read: KYC and AML in France: How Identity Verification Works

Understanding why fraud detection is crucial sets the stage for exploring the most effective strategies to protect payment gateways in 2026.

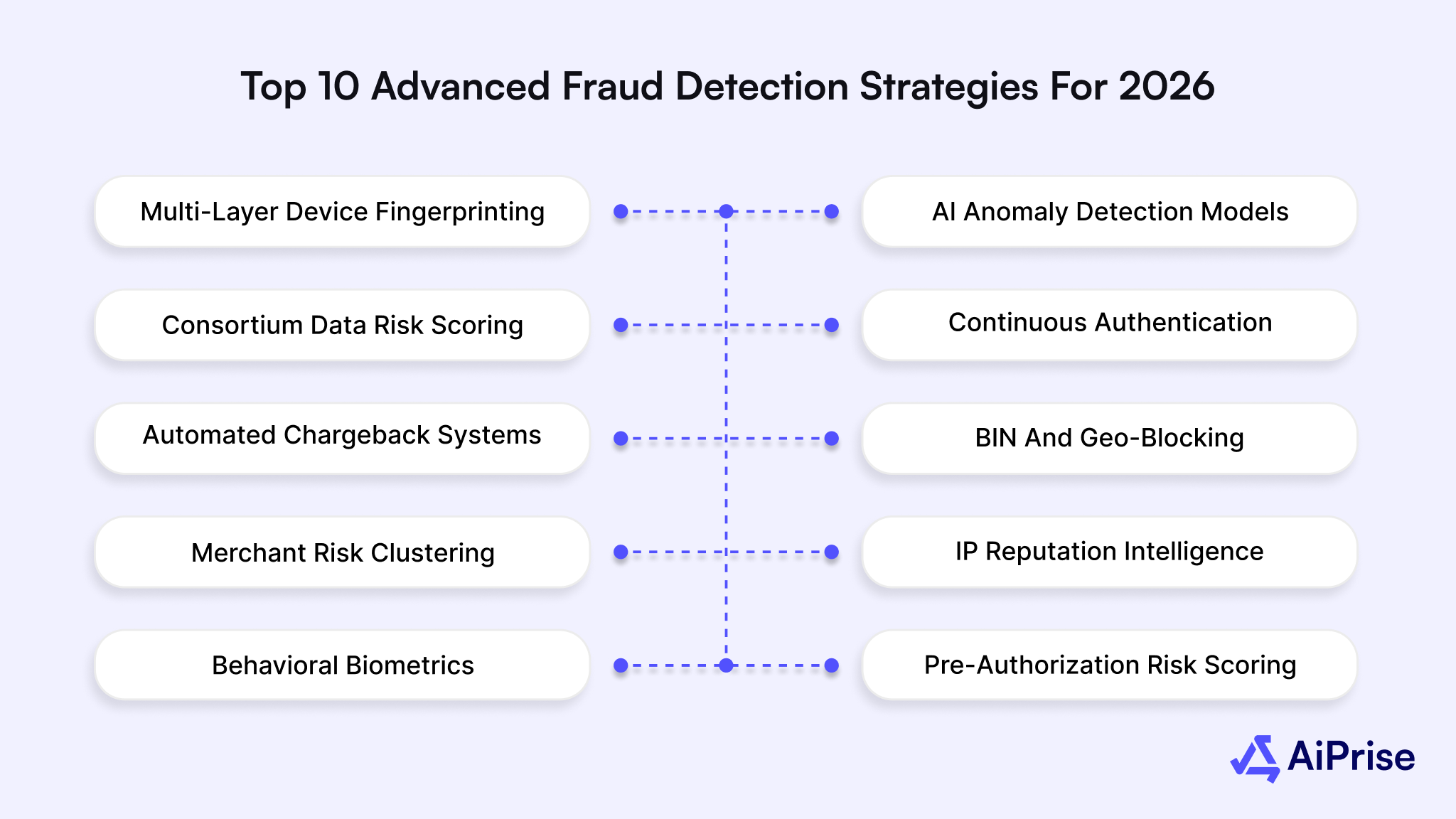

Top 10 Advanced Fraud Detection Strategies for 2026

In 2026, fraud prevention is no longer about stopping bad transactions alone. You are expected to protect your ecosystem without slowing growth, harming acceptance rates, or creating friction for legitimate users. Attackers now test your systems quietly, learning how your controls react before scaling attacks.

This shifts fraud detection from reactive blocking to proactive risk anticipation. To stay ahead, you need strategies that adapt in real time, learn across merchants, and align with how modern payment stacks operate across borders, channels, and payment methods.

Below are the advanced fraud detection strategies shaping payment gateway security in 2026:

Multi-Layer Device Fingerprinting

By 2026, single-signal device checks will no longer be enough to protect a payment gateway. Fraudsters regularly reset cookies, rotate devices, and spoof identifiers to appear new each time they transact. Multi-layer device fingerprinting gives you continuity across sessions, merchants, and payment attempts.

Below are the core elements that make multi-layer device fingerprinting effective for you:

- Hardware and Software Signal Correlation: Device attributes like OS version, browser configuration, screen resolution, and installed fonts are combined to form a stable identity. Even when one signal changes, the broader fingerprint remains recognizable across attempts.

- Session Persistence Across Transactions: Repeated payment attempts from the same device can be linked over time, even if accounts, cards, or emails change. This helps identify fraud testing behavior before an actual attack scales.

- Cross-Merchant Intelligence Within Your Network: Risky devices identified on one merchant account can be flagged instantly when they appear on another. This prevents fraud from hopping between merchants using the same gateway.

- Emulator and Virtual Machine Detection: Advanced fingerprinting identifies non-physical environments often used for automated fraud. This is critical when dealing with scripted attacks that bypass simple IP or browser checks.

- Adaptive Risk Weighting Based On Context: Device fingerprints are scored differently depending on transaction value, merchant category, and geography. This allows strong fraud control without unnecessary declines for low-risk payments.

AI Anomaly Detection Models

By 2026, fraud rarely follows known patterns long enough for static controls to catch it. Instead of repeating old tricks, attackers blend into normal transaction traffic and make small adjustments until something works.

AI anomaly detection models help surface these subtle deviations by learning what “normal” looks like across your payment flows. This matters when transaction volume is high and manual review is not an option. These models focus on unexpected behavior rather than predefined fraud rules.

Below are the key ways AI anomaly detection works for you:

- Baseline Transaction Behavior Modeling: Normal transaction patterns are learned for each merchant, payment method, and region. When activity deviates from these baselines, risk signals are raised even if no known fraud rule is triggered.

- Early Detection Of Fraud Testing Activity: Small-value transactions, unusual timing, or odd purchase combinations are flagged early. This helps stop fraud attempts before attackers move to higher-value payments.

- Adaptive Learning Without Manual Rules: Models adjust automatically as customer behavior changes, such as seasonal spikes or new payment features. This reduces the operational load of constant rule tuning.

- Cross-Feature Correlation At Scale: Multiple signals like transaction context, user behavior, and payment metadata are evaluated together. This reveals risks that single-signal checks often miss.

- Real-Time Risk Scoring For Instant Decisions: Anomaly scores are generated within milliseconds, allowing approvals or declines without slowing down checkout experiences.

Fraud patterns that blend into normal traffic are harder to catch at scale. AiPrise sharpens early detection through Fraud Risk Scoring that surfaces abnormal transaction behavior before losses accumulate.

Consortium Data Risk Scoring

Fraud rarely stays isolated to one gateway or one merchant for long. Once a tactic works, it spreads fast across platforms, regions, and payment methods. Consortium data risk scoring helps close this visibility gap by pooling anonymized fraud signals across multiple participants.

Below are the key ways consortium data risk scoring supports your fraud controls:

- Shared Intelligence Across Payment Networks: Risk signals from multiple gateways, PSPs, and merchants are combined to highlight known bad actors. Devices, emails, cards, or businesses flagged elsewhere surface instantly during transactions.

- Early Detection In Low-History Scenarios: New merchants, new geographies, or new payment methods often lack historical data. Consortium scoring fills this gap by applying external risk context from similar environments.

- Reduced Dependency On Single-Gateway Blind Spots: Patterns missed within one ecosystem become visible when correlated with broader industry activity. This helps detect coordinated fraud campaigns earlier.

- Dynamic Risk Weighting Based On Network Trends: Scores adjust as fraud activity rises or falls across the network. Sudden spikes in certain regions or industries are reflected without manual intervention.

- Improved Approval Confidence For Legitimate Traffic: Clean signals from the consortium help separate genuine customers from risky ones. This improves approval quality while maintaining strong fraud defenses.

Continuous Authentication

Static authentication checks are no longer enough when payment journeys stretch beyond a single moment. Risk can change after login, after checkout starts, or even between authorization steps.

Continuous authentication allows trust to be reassessed throughout the entire payment interaction. This matters when accounts stay active across devices, sessions, and channels. Instead of assuming a user remains legitimate, trust is earned and revalidated as behavior unfolds.

Below are the ways continuous authentication strengthens your payment security:

- Session-Level Trust Reassessment: Risk is evaluated continuously as actions occur, such as changing payout details or switching devices mid-session. Sudden shifts raise alerts before funds move.

- Behavior-Based Identity Confidence: Interaction patterns like navigation flow and transaction pacing help confirm the same genuine user remains in control. Deviations signal potential compromise.

- Step-Up Controls Only When Risk Rises: Additional verification is triggered only when behavior crosses risk thresholds. This avoids unnecessary friction for low-risk transactions.

- Protection Against Mid-Session Account Takeover: Even if access starts legitimately, unauthorized control can be detected before critical actions are completed. This limits damage from credential theft.

- Support for Long-Lived Payment Workflows: Subscription changes, delayed captures, or split payouts remain protected across extended timelines. Trust adapts as the transaction lifecycle evolves.

Automated Chargeback Dispute Systems

Chargebacks no longer affect only post-transaction operations. They directly influence your risk ratios, scheme monitoring status, and merchant retention. As volumes grow, manual dispute handling becomes inconsistent and slow, often missing critical deadlines or evidence requirements.

Automated chargeback dispute systems shift this from a reactive cleanup task to a structured risk control layer.

Below are the ways automated chargeback dispute systems support you:

- Evidence Assembly Without Manual Effort: Transaction logs, device data, delivery confirmation, and customer history are compiled automatically. This improves dispute quality while reducing operational workload.

- Deadline and Reason Code Management: Dispute timelines and scheme-specific rules are tracked automatically. Responses stay compliant even when handling large dispute volumes across regions.

- Root Cause Visibility Across Merchants: Chargeback trends are analyzed to identify recurring issues like unclear descriptors or refund gaps. This helps fix problems before ratios worsen.

- Higher Win Rates For Legitimate Transactions: Strong, consistent submissions improve success rates for valid disputes. This protects revenue while signaling control maturity to card networks.

- Early Warning Signals For Emerging Fraud: Sudden dispute spikes surface before fraud becomes visible in transaction data. This allows risk adjustments ahead of larger losses.

BIN And Geo-Blocking

As payment volumes expand globally, not every region or card issuer carries the same risk profile for your business. BIN and geo-blocking give you a controlled way to limit exposure without redesigning your entire fraud stack.

When applied with precision, these controls reduce high-risk traffic early in the flow. They are especially useful during market expansion, promotional spikes, or when specific fraud patterns concentrate around certain issuers or locations.

Below are practical ways BIN and geo-blocking help you manage risk:

- Targeted Issuer-Level Restrictions: Specific BIN ranges linked to repeated fraud can be limited or challenged. This prevents known risky card sources from draining operational resources.

- Country-Specific Risk Controls: Transactions from regions with inconsistent verification infrastructure can be blocked or routed through stricter checks. This allows controlled market entry without full exposure.

- Dynamic Controls During High-Risk Events: Temporary blocks can be applied during sales campaigns or fraud surges. This helps stabilize approval rates when attack volume spikes.

- Alignment With Merchant Risk Profiles: Different merchants tolerate different geographic risk levels. Controls can be adjusted based on business model and customer base.

- Reduction of Downstream Fraud Noise: Early filtering reduces unnecessary reviews and model load. This keeps advanced systems focused on genuinely complex risk decisions.

Merchant Risk Clustering

Not all merchants behave or grow in isolation. Risk often emerges in groups that share similar products, customer profiles, or traffic sources. Merchant risk clustering helps you move beyond one-by-one assessments and see patterns across your portfolio.

By grouping merchants with similar risk behavior, fraud controls become more proactive and easier to tune without penalizing healthy businesses.

Below are the ways merchant risk clustering strengthens your fraud strategy:

- Peer-Based Risk Benchmarking: Merchant behavior is evaluated against similar businesses rather than global averages. This helps identify outliers early without mislabeling normal growth as risk.

- Faster Detection Of Coordinated Abuse: Shared fraud tactics across related merchants surface quickly. This is common when the same traffic source or promotion attracts abuse.

- Smarter Onboarding And Monitoring Policies: New merchants inherit baseline controls based on cluster risk. This reduces manual reviews while keeping exposure controlled.

- Adaptive Controls For Scaling Merchants: Risk thresholds adjust as merchants move between clusters. This supports growth without sudden restriction shocks.

- Portfolio-Level Risk Visibility: Cluster insights highlight where overall exposure is building. This supports strategic decisions on pricing, reserves, or review capacity.

IP Reputation Intelligence

Network-level signals often reveal intent before transaction data does. IP reputation intelligence helps you evaluate where traffic originates and how it behaves across the internet.

Instead of reacting after transactions fail, IP intelligence lets you assess risk at the very first connection. It becomes a frontline control that filters out noise and protects downstream systems.

Below are the key ways IP reputation intelligence supports your fraud defenses:

- Identification of High-Risk Infrastructure: Traffic from known proxy services, data centers, or anonymizing networks is flagged early. This is common in scripted attacks that target checkout endpoints.

- Historical Abuse Pattern Recognition: IPs linked to past fraud across industries carry higher risk scores. This context helps prevent repeat abuse even when other details change.

- Geolocation Consistency Validation: Location signals are checked against payment and account data. Mismatches raise suspicion before authorization occurs.

- Bot and Automation Traffic Suppression: Abnormal request frequency and connection behavior reveal non-human activity. This reduces load on fraud models and review teams.

- Adaptive Trust for Clean Traffic: Stable residential or corporate networks build a positive reputation over time. This allows smoother approvals for legitimate users.

Behavioral Biometrics

Credentials and devices can be stolen, but behavior is much harder to fake consistently. Behavioral biometrics focuses on how actions are performed rather than what information is entered.

For payment gateways, this is valuable when protecting accounts, dashboards, and high-impact actions like refunds or payout changes. Risk assessment becomes continuous and invisible, which helps maintain smooth payment experiences.

Below are the key ways behavioral biometrics improves your fraud detection:

- Interaction Pattern Analysis: Typing rhythm, cursor movement, and touch pressure create a behavioral profile. Sudden changes can indicate unauthorized access.

- Detection of Human Versus Scripted Activity: Automated tools struggle to replicate natural interaction patterns. This helps block bots that bypass traditional controls.

- Account Protection Beyond Login: Risk is evaluated during sensitive actions, not just at authentication. This limits damage from compromised credentials.

- Low-Friction Security For Legitimate Users: No additional steps are required for trusted behavior. This protects conversions while increasing security depth.

- Stronger Defense Against Insider Abuse: Unusual behavior within trusted environments becomes visible. This supports internal risk monitoring without heavy controls.

Behavior alone does not always confirm who is behind a transaction. AiPrise adds identity assurance using KYC verification, connecting behavioral signals to verified user identities.

Pre-Authorization Risk Scoring

Fraud decisions are most effective when they happen before an authorization request ever reaches the network. Pre-authorization risk scoring allows you to evaluate intent and context early, when outcomes are still fully controllable.

By scoring risk upfront, exposure is reduced without increasing declines or slowing checkout flows.

Below are the ways pre-authorization risk scoring strengthens your payment decisions:

- Early Risk Visibility Before Network Costs: Risk is assessed before interchange fees or authorization attempts occur. This protects margins while filtering clearly risky traffic.

- Context-Aware Scoring Based on Payment Intent: Transaction purpose, amount patterns, and merchant behavior shape risk scores. This prevents one-size scoring across different use cases.

- Improved Routing and Authorization Strategy: High-risk transactions can be routed differently or challenged. This optimizes approval outcomes without unnecessary network exposure.

- Reduced Dependency On Post-Transaction Controls: Strong early decisions reduce chargebacks and downstream disputes. This improves overall system efficiency.

- Consistent Decisions Across High-Volume Traffic: Real-time scoring ensures stable outcomes even during traffic spikes. This supports scale without manual intervention.

After outlining the top strategies, it’s important to recognize the specific types of fraud that most frequently target payment gateways.

What Types of Fraud Target Payment Gateways the Most?

Payment gateways attract a wide range of fraud because they sit at the intersection of money movement, identity, and merchant activity. Attackers focus on gateways to test cards, abuse merchant onboarding, and exploit gaps between authorization and settlement.

For you, this means fraud is not limited to stolen cards alone. It can originate from compromised accounts, manipulated transactions, or even merchants misusing the platform.

Below are the most common fraud types targeting payment gateways:

Understanding the common fraud types helps clarify the essential features a modern payment gateway fraud detection system must include.

What Should a Modern Payment Gateway Fraud Detection System Include?

A modern fraud detection system is no longer a single tool plugged into checkout. It becomes part of how your gateway scales, launches new payment methods, and enters new regions. As transaction complexity increases, visibility and control matter more than raw blocking power.

The right system helps you balance risk, performance, and compliance without slowing innovation. It also gives internal teams clarity on why decisions are made, not just what the outcome is.

Below are the core capabilities your fraud detection system should include:

- Real-Time Decisioning: Risk evaluation happens within milliseconds, so transactions flow without delays. This is critical when supporting instant payments and high-volume merchants.

- Explainable Risk Outputs: Clear reasons behind decisions support audits, merchant conversations, and internal reviews. This reduces friction when declines are questioned.

- End-To-End Payment Stack Integration: Signals connect across checkout, authorization, payouts, and refunds. This prevents risk blind spots between transaction stages.

- High-Risk Pattern Libraries: Known fraud behaviors are continuously tracked and updated. This allows a faster response to emerging attack methods.

- Case Management and Audit Tools: Reviews, notes, and evidence are centralized. This simplifies compliance reporting and internal accountability.

Knowing the system requirements sets the stage for addressing the common challenges payment providers encounter in fraud detection.

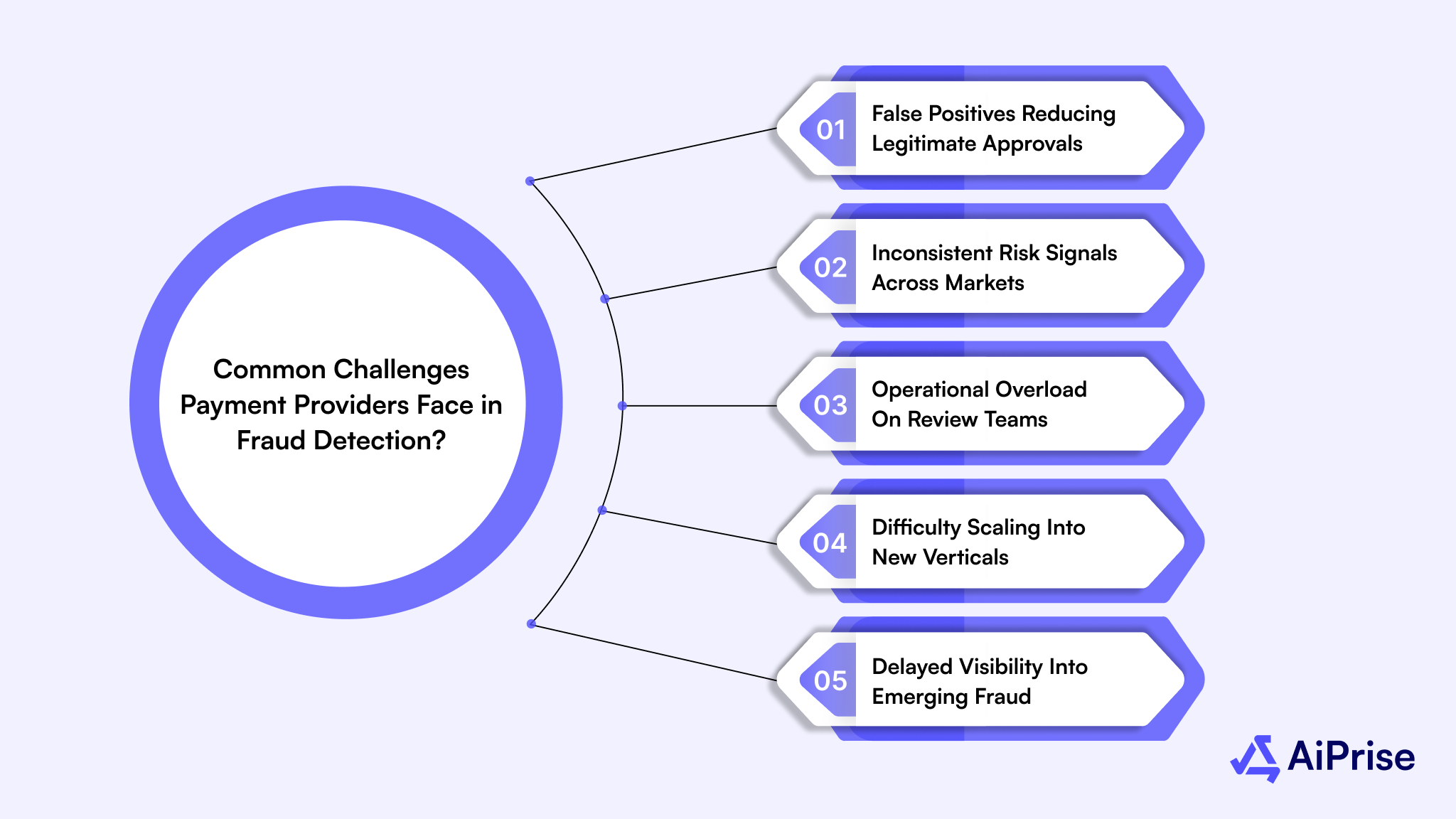

What Are the Common Challenges Payment Providers Face in Fraud Detection?

Fraud detection becomes harder as your payment business grows across merchants, regions, and payment methods. What works at low volume often breaks at scale. Risk signals increase, data sources multiply, and decisions must still happen instantly.

At the same time, merchants expect high approval rates and regulators expect strong controls. These pressures create gaps that fraud exploits unless challenges are addressed with practical fixes built into your operations.

Below are the most common fraud challenges you face, along with how to fix them:

- False Positives Reducing Legitimate Approvals: Overly strict controls block genuine customers.

- Fix this by using adaptive scoring that adjusts to merchant behavior instead of static thresholds.

- Inconsistent Risk Signals Across Markets: Different regions produce uneven data quality.

- Fix this by normalizing signals and applying region-aware risk logic.

- Operational Overload On Review Teams: High alert volumes slow investigations.

- Fix this by prioritizing alerts based on financial impact and confidence scores.

- Difficulty Scaling Into New Verticals: New industries bring unfamiliar risk patterns.

- Fix this by using peer-based benchmarks and historical analogs.

- Delayed Visibility Into Emerging Fraud: Fraud often appears after damage occurs.

- Fix this by monitoring leading indicators instead of waiting for chargebacks.

Also read: Compliance in Business in Singapore: What’s Changing

Understanding these challenges highlights how AiPrise can enhance fraud detection for payment gateways.

How AiPrise Strengthens Payment Gateway Fraud Detection

Fraud controls become truly effective when identity, behavior, and compliance signals work together instead of operating in silos. Payment gateways need support that extends beyond transaction scoring and into who is transacting, which businesses are involved, and whether activity aligns with regulatory expectations.

This is where deeper verification and risk intelligence make a measurable difference. AiPrise strengthens fraud detection by embedding identity trust, global coverage, and compliance intelligence directly into payment risk workflows.

Below is how AiPrise delivers concrete value to payment gateways:

- Automated Identity Risk Checks at Transaction Touchpoints: Identity signals are enriched at critical moments like onboarding, account changes, and high-risk payments. With AiPrise embedded into these flows, suspicious identities are flagged early using multi-source verification data.

- Global KYC and KYB Coverage for Merchant and User Trust: Merchant entities and end users are validated across jurisdictions using reliable global sources. AiPrise supports consistent verification even when gateways expand into new regions or onboard cross-border merchants.

- AML Screening For Transaction-Level Risk Control: Transactions and entities are screened against sanctions, watchlists, and adverse media. By integrating AiPrise AML checks, high-risk activity is surfaced before it escalates into regulatory exposure.

- Unified Fraud, KYC, KYB, and AML Intelligence Layer: Fraud signals, identity verification, business validation, and AML screening operate together within one risk framework. AiPrise connects these four core operations to reduce blind spots and improve decision accuracy across the payment lifecycle.

With these capabilities in place, we can see how AiPrise drives more effective and efficient fraud detection for payment gateways.

Conclusion

Payment gateway fraud in 2026 is no longer a single-layer problem. It sits across identity, transactions, merchants, and compliance, and every weak link compounds risk as volume scales. Relying on isolated tools or outdated controls makes it harder to protect approvals, maintain scheme trust, and support merchant growth.

AiPrise helps payment gateways strengthen this foundation by combining fraud intelligence with global KYC, KYB, and AML capabilities. This creates clearer risk decisions, better compliance alignment, and stronger protection across the entire payment lifecycle.

Ready to strengthen your fraud detection without slowing growth? Book A Demo to see how AiPrise supports payment gateways with smarter, identity-driven fraud prevention.

FAQs

1. How do payment gateways reduce fraud without increasing transaction declines?

Fraud is reduced by using adaptive risk scoring instead of hard blocks. When context, behavior, and identity signals are evaluated together, legitimate transactions pass smoothly while risky ones are stopped early. This improves approval quality rather than simply increasing rejection rates.

2. What is the difference between payment fraud prevention and fraud detection?

Fraud detection identifies suspicious activity in real time or after it occurs. Fraud prevention focuses on stopping risky transactions before money moves. In practice, you need both working together so early signals reduce exposure while detection handles edge cases.

3. How does fraud detection impact payment approval rates?

Well-designed fraud detection improves approval rates by filtering bad traffic before it reaches authorization. This keeps networks clean and reduces unnecessary declines. Poorly tuned systems do the opposite by blocking genuine users and damaging merchant trust.

4. Are fraud detection systems required for PCI DSS compliance?

PCI DSS focuses on protecting card data, not directly on fraud prevention. However, strong fraud detection supports compliance by reducing breach risk and misuse. Many payment partners and schemes also expect fraud controls as part of broader risk management.

5. How do payment gateways handle fraud for alternative payment methods?

Alternative payment methods rely less on card data and more on identity, device, and behavioral signals. Fraud controls shift toward account behavior, transaction context, and payout monitoring to manage risk across wallets, bank transfers, and real-time payments.

You might want to read these...

.png)

.png)

.png)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately