AiPrise

8 min read

March 4, 2026

Address Fraud Detection: Best Practices for Fintech & Banks

Key Takeaways

Address fraud detection has become a critical control point for fintech companies and banks where digital onboarding, regulatory scrutiny, and fraud exposure intersect daily. In 2025, the IRS reported approximately 12,200 undeliverable mail notifications to taxpayers due to outdated or incorrect address records, highlighting how inaccurate address data can disrupt communications and create compliance vulnerabilities.

When address information fails at even a basic validation level, it signals bigger risks, from identity manipulation and synthetic fraud to onboarding gaps that increase manual review costs. For compliance and risk leaders, this isn’t just about mail delivery; it’s about protecting customer trust, reducing operational friction, and avoiding regulatory red flags.

Strengthening address fraud detection helps you identify suspicious patterns early, prevent fraudulent account creation, and maintain accurate customer records across KYC and AML workflows. Understanding how to detect and prevent address fraud effectively equips your institution to close verification gaps, lower risk exposure, and build a more resilient fraud prevention framework.

Quick Overview

- Address fraud detection prevents identity manipulation, synthetic profiles, and onboarding gaps that expose banks and fintechs to compliance penalties and fraud losses.

- Effective detection combines AVS checks, postal and bureau databases, device intelligence, behavioral analytics, and real-time risk scoring.

- Layered verification, automated decisioning, document controls, and continuous rule updates reduce false positives while strengthening KYC and AML programs.

- Performance tracking through pass-fail ratios, escalation rates, fraud-linked accounts, and decision times ensures address controls remain accurate and accountable.

What Is Address Fraud in Financial Services?

Address fraud in financial services occurs when criminals manipulate, fabricate, or misuse address information to bypass identity verification controls. It often appears during digital onboarding, where mismatched residential data weakens KYC compliance and enables synthetic identity fraud. Weak address verification processes increase AML exposure, elevate fraud risk management costs, and create regulatory vulnerabilities across banking operations.

Why Detecting Address Fraud Matters for Fintech & Banks?

Detecting address fraud directly influences your ability to control fraud losses, maintain regulatory alignment, and safeguard onboarding integrity in a digitally exposed financial ecosystem.

Below are the core operational and compliance-driven reasons why strengthening address fraud detection should remain a strategic priority:

- Chargeback and dispute ratios increase when fraudsters exploit weak address verification during card-not-present transactions and remote onboarding flows.

- Customer Identification Program (CIP) failures triggered by inconsistent address data can expose gaps in KYC compliance and invite supervisory scrutiny.

- Synthetic identity fraud often relies on manipulated residential data, making weak address controls a gateway vulnerability within AML risk frameworks.

- Manual exception handling rises sharply when address mismatches are not resolved through automated fraud detection and data intelligence systems.

- Cross-border digital banking operations face heightened exposure when geo-location signals conflict with declared address records during onboarding.

- Poor address data hygiene disrupts downstream transaction monitoring systems, weakening fraud risk management analytics and behavioral anomaly detection.

Also read: The Role of Address Verification in Fraud Prevention

Recognizing the impact is only part of the equation; the real advantage comes from knowing which data signals reveal address manipulation early.

Sources & Signals Used in Effective Address Fraud Detection

Effective address fraud detection depends on layered intelligence signals that validate residential data across independent and high-confidence data ecosystems.

Below are the critical data sources and risk indicators that strengthen identity verification and fraud risk management frameworks:

- Address Verification Service (AVS) responses compare submitted billing data with issuer records, flagging partial or full mismatches during transaction authorization.

- National postal databases and change-of-address registries validate deliverability status and detect recently altered residential records linked to fraud attempts.

- IP geolocation analysis identifies inconsistencies between declared physical addresses and digital session origination points during remote onboarding.

- Device fingerprinting detects repeat fraud patterns when identical hardware identifiers appear across multiple high-risk address submissions.

- Utility record and credit bureau address histories expose short-term occupancy anomalies commonly associated with synthetic identity fraud schemes.

- Behavioral analytics engines correlate typing cadence, session velocity, and application sequencing with suspicious residential data entries.

- Sanctions screening and adverse media databases uncover high-risk entities using manipulated address information to bypass AML compliance controls.

When implemented through an AI-driven platform like AiPrise, these verification signals integrate seamlessly into automated KYC and AML workflows, strengthening fraud prevention without increasing onboarding friction.

Best Practices for Address Fraud Detection

Effective address fraud detection requires structured controls that reduce verification gaps without increasing onboarding friction or regulatory exposure.

Below are tactical, implementation-focused practices that strengthen fraud risk management across fintech and banking environments:

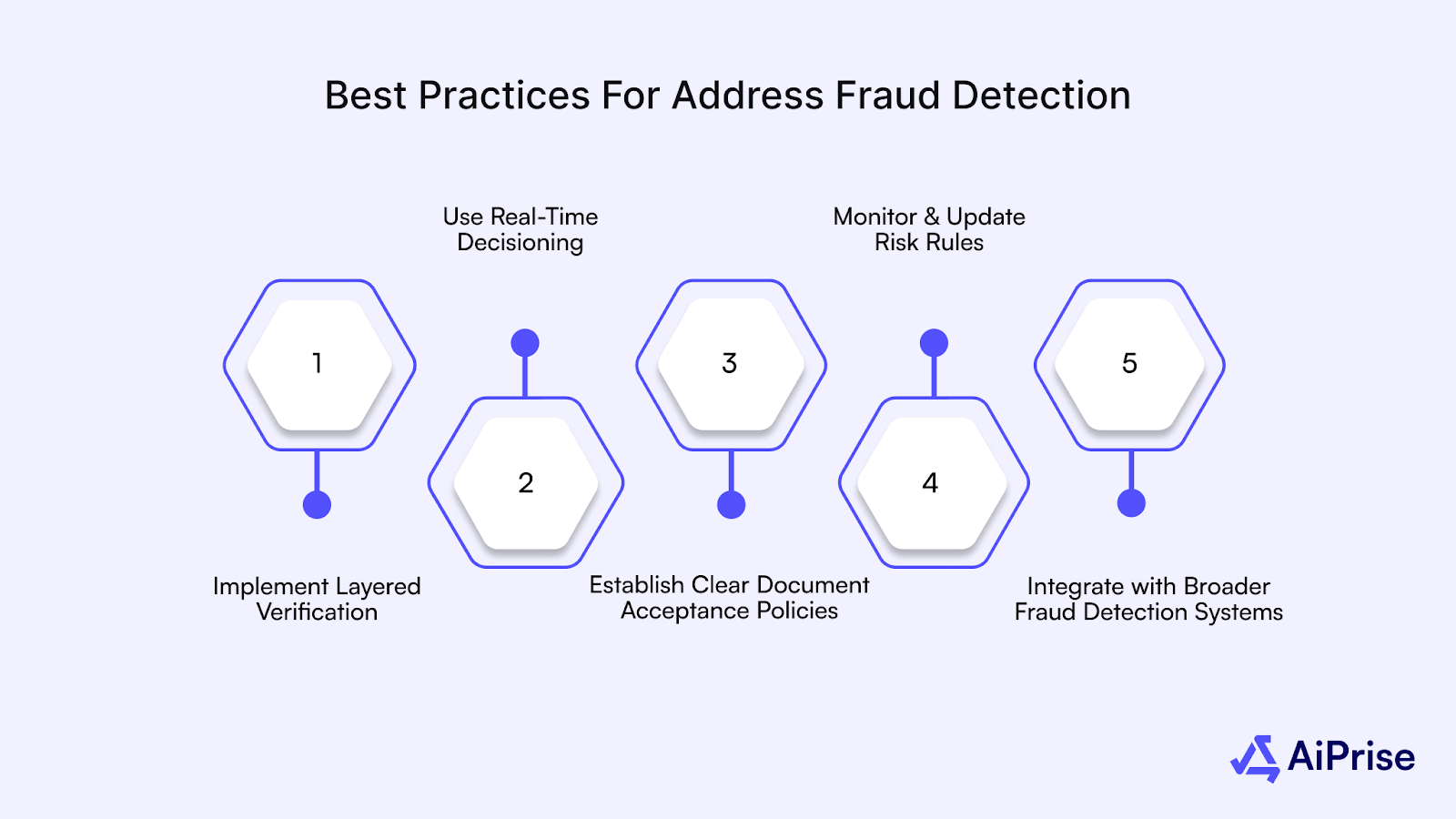

1. Implement Layered Verification

- Combine Address Verification Service (AVS) checks with document verification to validate billing and residential data simultaneously.

- Correlate government-issued ID records with declared addresses to reinforce KYC compliance and Customer Identification Program controls.

- Flag partial AVS mismatches early in onboarding workflows to prevent downstream transaction fraud and account takeover exposure.

- Cross-reference utility records or bureau address histories to detect synthetic identity indicators before account activation.

2. Use Real-Time Decisioning

- Deploy automated decision engines that accept, reject, or escalate applications based on data confidence thresholds.

- Integrate machine learning risk scores that analyze behavioral anomalies alongside address verification outcomes.

- Trigger dynamic step-up authentication when geolocation signals conflict with declared residential information.

- Route high-risk cases into structured case management queues with predefined compliance escalation protocols

3. Establish Clear Document Acceptance Policies

- Define approved proof-of-address documents such as utility bills, lease agreements, or regulated financial statements.

- Enforce recency thresholds to ensure submitted documents reflect current occupancy and valid residential status.

- Implement tamper-detection controls to validate document authenticity and prevent manipulated digital uploads.

- Standardize exception handling procedures to reduce inconsistent manual review decisions across compliance teams.

4. Monitor and Update Risk Rules

- Continuously recalibrate fraud detection thresholds based on emerging address manipulation techniques.

- Analyze false positive and false negative ratios to refine risk scoring accuracy across onboarding systems.

- Incorporate regulatory updates into AML and KYC rule frameworks without disrupting operational efficiency.

- Conduct periodic stress testing of address verification workflows against simulated fraud scenarios.

5. Integrate with Broader Fraud Detection Systems

- Link address verification results with transaction anomaly detection engines to strengthen fraud pattern recognition.

- Correlate behavioral fraud signals, including session velocity and device fingerprinting, with residential data inconsistencies.

- Synchronize identity verification results with AML monitoring systems to detect layered risk exposure.

- Deploy unified orchestration platforms such as AiPrise, which connect address verification, biometric authentication, sanctions screening, and real-time risk scoring into a centralized fraud intelligence dashboard.

Also read: Understanding Fraud: Patterns and Prevention Strategies

Implementation alone is not enough; different verification methods carry trade-offs that influence detection accuracy and operational cost.

Address Verification Methods and Risk Tradeoffs

Different address verification approaches offer varying levels of fraud detection strength depending on implementation depth and data intelligence coverage.

Below is a structured view of commonly used address verification methods, outlining where each performs well and where limitations may create risk exposure:

Selecting the right methods becomes far more powerful when they are embedded directly into your compliance architecture.

Integrating Address Fraud Detection into KYC & AML Programs

Address fraud detection must function as a core control within KYC and AML programs rather than operating as an isolated onboarding check.

Below are the operational integration points that ensure address verification strengthens compliance, transaction monitoring, and fraud risk management frameworks:

- Embed address verification checkpoints directly into Customer Identification Program workflows to prevent incomplete or inconsistent residential records.

- Align address risk scoring with customer due diligence tiers to apply enhanced verification for higher-risk profiles.

- Trigger enhanced due diligence reviews when repeated address discrepancies appear across linked applications or related entities.

- Feed verified address intelligence into AML transaction monitoring systems to improve anomaly detection precision.

- Map address verification outcomes to suspicious activity reporting thresholds when layered fraud indicators emerge.

- Maintain audit-ready logs of verification results to support regulatory examinations and internal compliance assessments.

- Integrate sanctions screening and politically exposed person checks with validated residential records to reduce investigation noise.

- Activate continuous monitoring controls to flag post-onboarding address changes that may signal emerging fraud exposure.

Integration must also be measurable, which means tracking performance indicators that show whether your controls are actually reducing risk.

Operational Metrics to Track

Tracking the right operational metrics ensures your address fraud detection framework delivers measurable impact across compliance, risk reduction, and onboarding efficiency.

Below are five performance indicators that help evaluate effectiveness and optimize fraud risk management outcomes:

- Address verification pass-to-fail ratio segmented by onboarding channel to identify emerging fraud concentration points.

- False positive rate associated with address mismatches to prevent unnecessary friction and revenue loss.

- Escalation rate to manual review triggered by residential data inconsistencies within KYC workflows.

- Fraud loss exposure is linked specifically to account openings with prior address verification anomalies.

- Average decision time for address validation within automated onboarding systems to monitor operational efficiency.

Also read: How to Avoid and Detect KYC Fraud

Measurement reveals gaps, and closing those gaps often requires technology that connects verification, monitoring, and risk scoring in one environment.

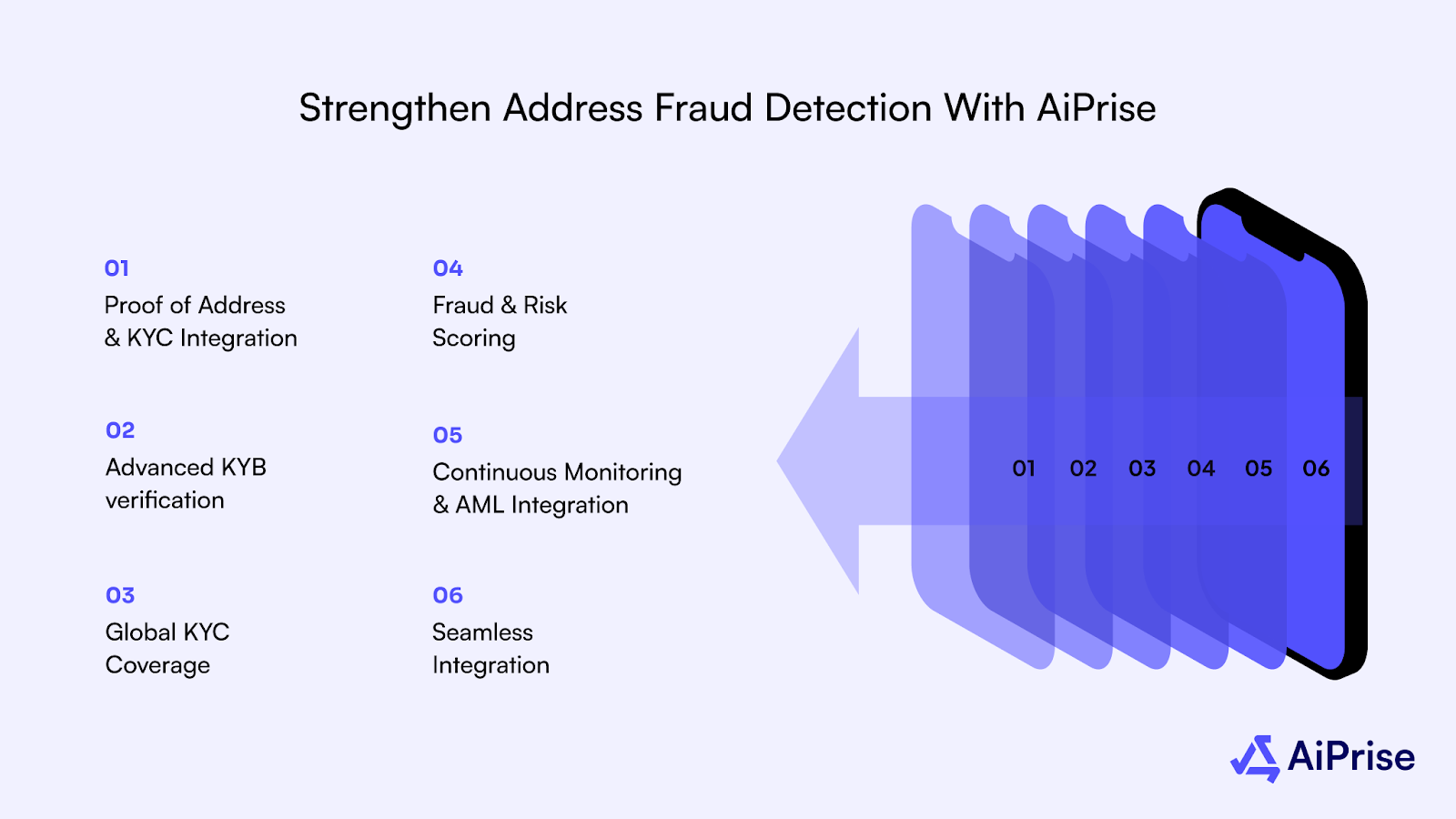

Strengthen Address Fraud Detection with AiPrise

Modern address fraud detection requires more than isolated verification checks; it demands an integrated, AI-driven compliance infrastructure.

Here’s how AiPrise supports banks and fintechs in operationalizing secure, scalable address verification within KYC and AML frameworks:

- Proof of Address & KYC Integration: Built-in proof of address verification enhances residential data accuracy within your identity and address verification processes.

- Advanced KYB verification to authenticate business addresses, ownership structures, and registry data during corporate onboarding.

- Global KYC Coverage: AiPrise’s AI-enabled identity verification combines document checks, biometric liveness, and risk signals to confirm address and identity across 220+ countries.

- Fraud & Risk Scoring: One unified risk score synthesizes address mismatches, behavioral signals, and AML flags to identify high-risk applicants earlier in the onboarding cycle.

- Continuous Monitoring & AML Integration: Real-time risk profiling and ongoing screening against sanctions, watchlists, and adverse media helps you maintain compliance even post-onboarding.

- Seamless Integration: APIs, case management tools, and automated workflows allow AiPrise to plug directly into your existing compliance stack without slowing operations.

Strengthening address fraud detection today positions your institution to reduce preventable losses, tighten compliance controls, and build long-term trust in every customer interaction.

Wrapping Up

Address fraud detection is no longer a secondary control; it is a foundational layer in protecting digital onboarding, regulatory compliance, and transaction integrity. Strengthening verification signals, aligning them with KYC and AML workflows, and continuously monitoring residential data ensures your fraud risk management strategy remains resilient against evolving threats.

AiPrise supports this by combining proof-of-address verification, AI-driven risk scoring, biometric identity checks, sanctions screening, and continuous monitoring into a unified compliance and fraud prevention platform.

Strengthen your address fraud detection strategy today and Book A Demo to see how AiPrise helps fintechs and banks reduce fraud risk while maintaining seamless onboarding experiences.

FAQs

1. What is address fraud detection in banking?

Address fraud detection in banking refers to the process of verifying residential information to prevent identity fraud, synthetic identities, and unauthorized account access during onboarding and transactions.

2. How does Address Verification Service (AVS) help prevent fraud?

AVS compares the billing address provided during a transaction with the address on file at the card issuer, helping identify mismatches that may signal fraudulent activity.

3. Is address verification required for KYC compliance?

Address verification is typically part of Customer Identification Program requirements under KYC regulations, helping institutions confirm a customer’s identity and residential legitimacy.

4. What documents are accepted for address verification?

Common proof-of-address documents include recent utility bills, bank statements, government correspondence, or lease agreements showing the customer’s current residential address.

5. How can fintech companies reduce false positives in address fraud detection?

Fintech companies can reduce false positives by combining AVS results with behavioral analytics, machine learning risk scoring, and multi-factor identity verification controls.

You might want to read these...

.png)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately