AiPrise

12 mins read

July 31, 2025

How to Identify Fraudsters: 4 Common Red Flags

Key Takeaways

Fraud remains one of the most pervasive threats to businesses worldwide. In fact, ACFE's 2024 Report reveals that more than $3 billion was lost to fraud, highlighting the urgency for businesses to enhance their fraud detection systems. Knowing how to identify fraudsters early can make all the difference in protecting your company's finances, reputation, and customer trust.

In this blog, we'll discuss common red flags that indicate potential fraud, strategies for identifying fraudsters, and how AiPrise helps streamline the fraud detection process for businesses.

Key Takeaways

- Fraud is a significant threat to businesses, with 5% of annual revenue lost to fraud globally, emphasizing the need for proactive fraud detection.

- Common fraud red flags businesses should look for include unusual behavioral patterns, inconsistent personal data, suspicious documentation, and irregular transaction activities.

- To identify fraudsters effectively, businesses must utilize AI, behavioral analytics, and cross-platform data verification to detect fraud early and minimize financial damage.

- AiPrise offers automated fraud detection, real-time monitoring, and global compliance features to help businesses outpace fraudsters.

Understanding Fraud and Its Impact on Businesses

Fraud not only impacts a company’s financial health but also its operational efficiency, compliance standing, and overall reputation. In fact, 5% of annual revenue is lost to fraud each year, as reported by the ACFE. For large organizations, this means billions of dollars in losses annually, threatening both their bottom line and their ability to stay competitive.

Companies suffering from fraud may face:

- Financial Strain: Ongoing fraudulent activities can undermine profitability, with some businesses suffering irreparable financial damage if fraud goes undetected for too long.

- Reputational Damage: Customers and partners lose trust in companies that have been compromised, often resulting in abandoned contracts and lost business.

- Regulatory Consequences: Non-compliance with fraud detection and prevention regulations can lead to hefty fines, lawsuits, and loss of licenses.

As fraud tactics become more advanced, businesses must evolve their fraud detection measures. Recognizing how to identify fraudsters early is crucial in preventing these risks and ensuring the integrity of operations.

Now that we understand the severe impact fraud can have on businesses, let’s explore some of the most common red flags that can help identify fraudsters before significant damage occurs.

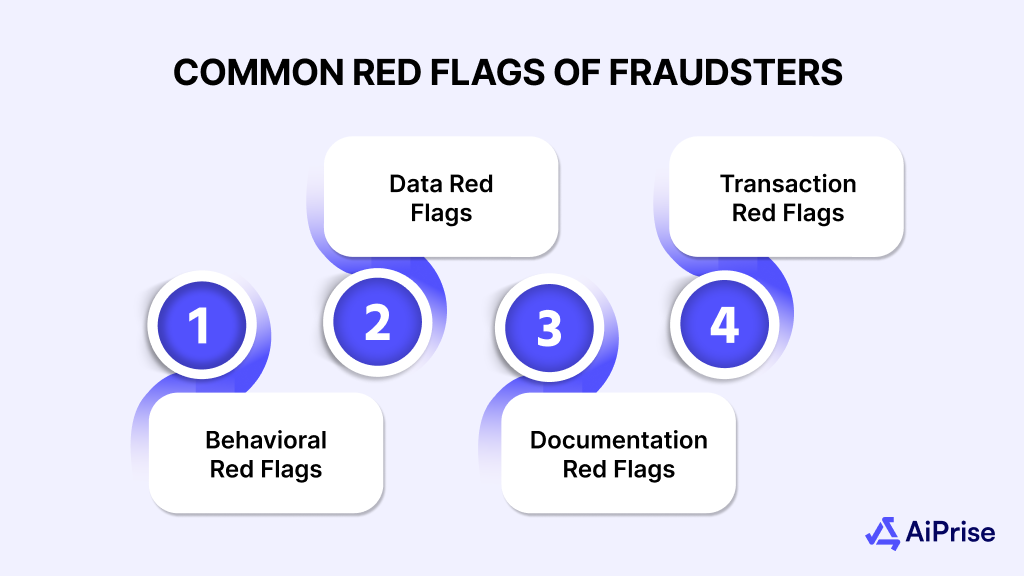

Common Red Flags of Fraudsters

Identifying fraudsters early is crucial to preventing financial loss and safeguarding a company’s reputation. While fraud can take many forms, certain red flags commonly indicate illicit behavior. By staying vigilant and monitoring for these signs, businesses can significantly enhance their protection.

Below are some of the most common red flags to look out for:

Behavioral Red Flags

Fraudulent behavior often manifests in how a user behaves on a platform or in their financial activities. Unusual activity or sudden changes in behavior can indicate that someone is attempting to exploit the system.

- Unusual Spending Patterns: A sudden surge in transactions or large-value purchases, especially from new accounts or existing ones, may indicate fraudulent activity.

- Frequent Logins from Unusual Locations: Logging in from unexpected locations or devices outside of normal activity patterns, especially during off-hours, can be a sign of a compromised account.

Data Red Flags

Fraudsters often provide inconsistent or incomplete information to mislead businesses. Look for mismatches or anomalies in the data provided.

- Mismatched Personal Information: Inaccurate or inconsistent details such as misspelled names, incorrect addresses, or mismatched Social Security numbers (SSNs) are major indicators of fraud.

- Multiple Accounts with Similar Data: Fraudsters sometimes create multiple fake accounts using similar or identical personal data (like email addresses or phone numbers), signaling fraudulent activity.

Documentation Red Flags

Fraudsters often attempt to submit falsified documents to complete their identity verification. Any discrepancy or oddity in submitted documents should raise concern.

- Altered or Forged Documents: Documents that appear altered, such as photos being distorted or fonts mismatched, may indicate forgery.

- Inconsistent Documentation: Mismatches between documents, like a different address on an ID and a utility bill, could suggest fraudulent intent.

Transaction Red Flags

The nature of transactions can often reveal fraud. Fraudulent transactions tend to follow a pattern, with the fraudster testing the system before completing the crime.

- Multiple Failed Attempts: Several failed login or payment attempts followed by a successful transaction may indicate the fraudster is testing credentials before completing their fraudulent activity.

- Unusual Payment Methods: Fraudsters often employ hard-to-trace payment methods, such as prepaid cards, wire transfers, or cryptocurrency, to complicate tracking their activities.

Here is a quick tabular representation of the common red flags mentioned above:

While recognizing these red flags is important, fraudsters are becoming increasingly sophisticated in their tactics. Let's explore some of the advanced techniques businesses can implement to proactively identify fraud and protect themselves from financial and reputational damage.

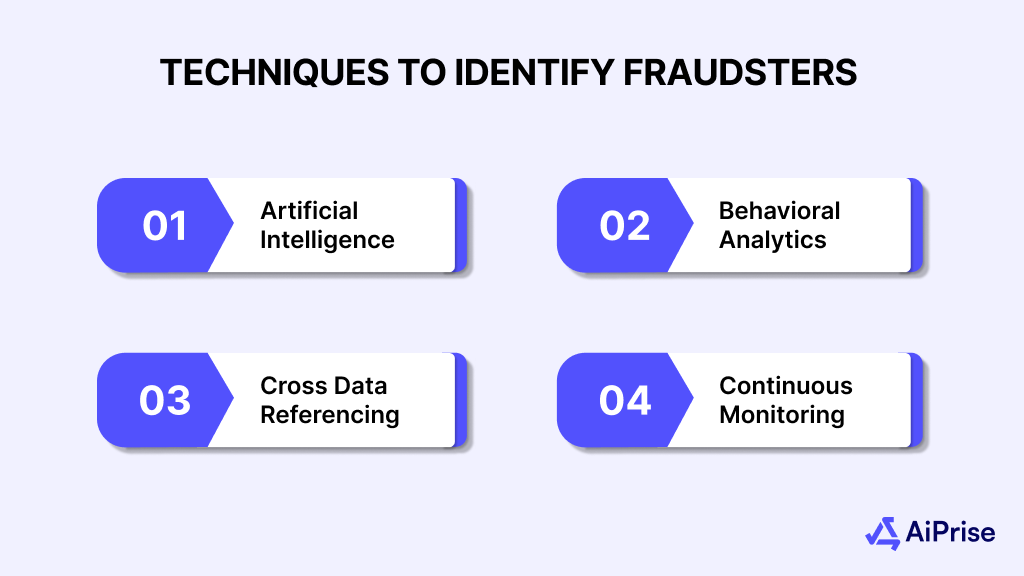

Advanced Techniques to Identify Fraudsters

As fraudsters continue to evolve their tactics, businesses must use advanced techniques to stay one step ahead. These techniques use cutting-edge technology and data analytics to detect suspicious activity in real-time.

Here are some of the most effective ways to identify fraudsters and protect your business:

Artificial Intelligence and Machine Learning

AI and machine learning are invaluable in identifying fraudsters. These technologies can analyze vast amounts of data in real-time, detect unusual patterns, and even predict potential fraudulent behavior before it occurs. For example, AI algorithms can learn from past fraud cases and continuously improve, ensuring that detection becomes more accurate over time.

- Anomaly Detection: AI can quickly spot inconsistencies in behavior, such as unusual spending or login patterns that deviate from a user's history, making it easier to flag fraud early.

- Predictive Analytics: By analyzing historical data, machine learning can predict fraud before it happens, allowing businesses to act before significant losses occur.

Behavioral Analytics

Behavioral analytics focuses on monitoring a user's actions over time to establish a "normal" behavior profile. By understanding typical user patterns, such as login frequency, time of activity, transaction amounts, and device usage, businesses can identify deviations that may suggest fraudulent activity.

- Real-Time Monitoring: By continuously tracking user actions, businesses can instantly detect any deviations from normal behavior and flag suspicious activity as it occurs.

- Risk Scoring: Behavioral analytics assigns a risk score to each user based on their activity. A sudden spike in a user’s risk score can trigger additional verification or a temporary account lock.

Cross-Referencing Data Across Multiple Platforms

Fraudsters often use multiple platforms to hide their identity or create fake accounts. By cross-referencing data from multiple trusted sources, businesses can verify that all information provided by the customer aligns correctly. This helps uncover discrepancies and identify fraudulent behavior.

- Third-Party Data Providers: Using data from multiple verified third-party sources, such as government databases, financial institutions, and credit bureaus, can help businesses confirm the authenticity of customer data.

- Global Data Verification: Cross-referencing customer data against international databases ensures that fraudsters attempting to use stolen identities are caught, even if they are from another country.

Continuous Monitoring and Reporting

Detecting fraud is not a one-time process but an ongoing effort. Continuous monitoring of transactions, login attempts, and account behavior is essential for staying ahead of fraudsters. Additionally, businesses need real-time reporting systems to act swiftly when fraud is detected.

- Real-Time Alerts: Continuous monitoring systems can send immediate alerts when suspicious activity is detected, enabling businesses to act quickly and mitigate risks.

- Automated Reporting: Automated fraud detection systems generate detailed reports, enabling businesses to analyze trends, spot emerging threats, and refine their fraud detection methods.

Now that we’ve explored how to identify fraudsters, it’s equally important to understand how to protect your business from these fraudsters. The next step is to implement proactive measures that can prevent fraud from occurring in the first place.

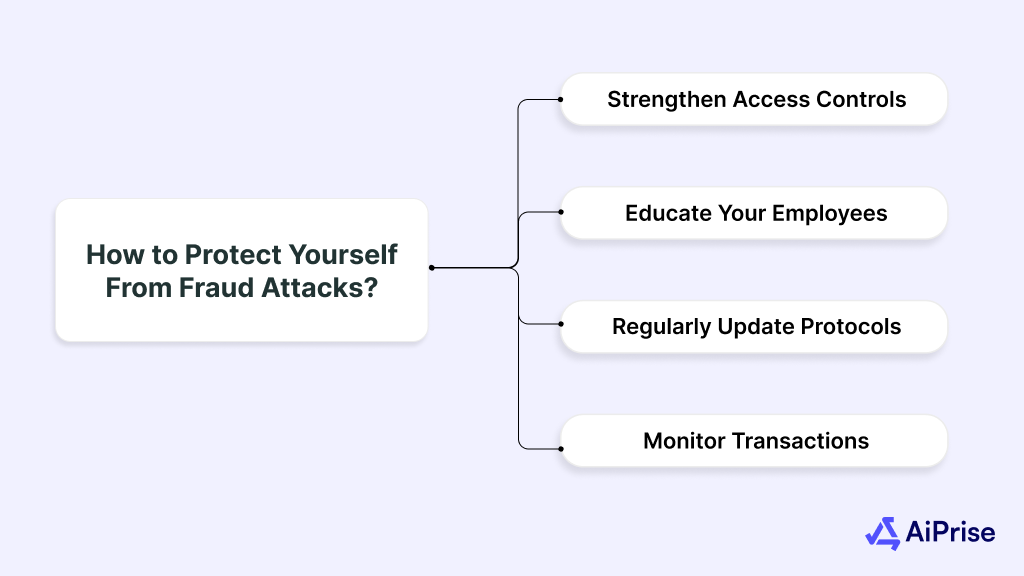

How to Protect Yourself From Fraud Attacks

Protecting your business from fraudulent attacks requires a proactive and multi-layered approach. By strengthening access controls, utilizing smart detection, and educating employees, organizations can significantly reduce their risk. Here are the actionable steps to safeguard your operations and ensure continuous protection.

Strengthen Access Controls

Implement multi-factor authentication (MFA) and strong password policies to ensure that only authorized users can access sensitive data and systems. This makes it more difficult for fraudsters to gain unauthorized access.

- Limit Access Based on Roles: Use role-based access controls (RBAC) to ensure employees only have access to the data they need for their job, reducing the risk of insider fraud.

Educate Your Employees

Fraud often occurs through insider threats or by exploiting employee mistakes. Provide regular fraud awareness training so employees know how to spot and report potential fraud.

- Phishing and Social Engineering: Train employees to recognize phishing attempts and suspicious communication from potential fraudsters.

Regularly Update Security Protocols

Keep all your security software, encryption protocols, and firewalls up to date. As fraudsters evolve their tactics, so must your defenses.

- Patch Vulnerabilities: Ensure regular updates to all systems to avoid security loopholes that fraudsters can exploit.

Monitor Transactions and Accounts Regularly

Set up a schedule for regular audits of transactions and accounts. This proactive approach can help spot any fraudulent activity early, saving the company from bigger losses.

- Automated Systems: Use automated systems and reporting to streamline periodic transactions and account audits, allowing for continuous oversight.

After discussing protective measures, the next step is ensuring your business is equipped with tools that effectively identify fraudsters. AiPrise offers a suite of tools designed to enhance fraud detection, providing businesses with the necessary resources to act swiftly and accurately when fraud is detected.

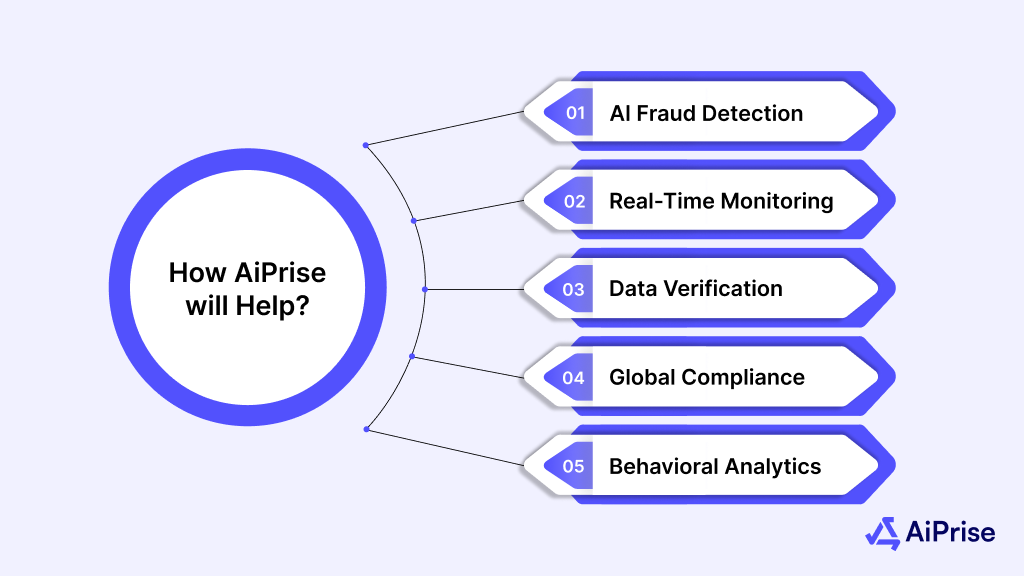

How AiPrise Helps Businesses Detect and Prevent Fraud

As fraud continues to evolve in complexity, businesses require advanced tools to identify, prevent, and mitigate risks effectively. Here is how AiPrise supports businesses in their fight against fraud, ensuring seamless detection and compliance with global regulations.

- AI-Powered Fraud Detection: AiPrise leverages AI and machine learning to analyze transactions in real-time, identifying fraud patterns and preventing financial losses before they occur.

- Real-Time Monitoring: With continuous monitoring, AiPrise flags suspicious activities as they happen, enabling businesses to take immediate action and reduce fraud risks.

- Cross-Platform Data Verification: AiPrise cross-references customer data with trusted third-party sources to ensure authenticity and uncover discrepancies, providing deeper fraud insights.

- Global Compliance: AiPrise simplifies compliance by automating AML, KYC, and fraud detection, ensuring your business stays aligned with evolving regulations globally.

- Behavioral Analytics and Risk Scoring: AiPrise uses behavioral analytics to track normal user patterns, with risk scoring to flag irregular activities for further investigation.

By integrating AiPrise’s solutions, businesses can strengthen their fraud detection, enhance compliance, and protect sensitive data with ease

Conclusion

Identifying fraudsters and protecting your business from fraud attacks is essential in today’s digital world. As fraud tactics become more sophisticated, businesses must stay vigilant, using advanced techniques like AI, machine learning, and behavioral analytics to detect fraudulent activity early.

Additionally, implementing strong security protocols and continuously monitoring transactions can significantly reduce the risk of fraud.

AiPrise provides businesses with the tools they need to stay ahead of fraudsters. With its AI-powered fraud detection, real-time monitoring, and global compliance features, AiPrise ensures that businesses can quickly identify and prevent fraud while protecting sensitive data.

To find out how we can help you identify fraudsters and protect your business, Book A Demo today!

FAQs

1. What are some common red flags of fraud?

Common fraud red flags include sudden changes in transaction behavior, frequent login attempts from different locations, inconsistencies in provided identity data, and the use of stolen or synthetic identities.

2. How do you detect fraudsters?

Fraudsters can be detected through AI-driven systems that analyze patterns in customer behavior, monitor anomalies, and cross-reference data from multiple sources. These systems flag suspicious activities like unusual spending, unexpected login times, or data inconsistencies.

3. How are most frauds identified?

Fraud is often identified through tips from employees or customers, automated monitoring systems, or behavioral analytics. In many cases, fraud detection tools that use AI and machine learning help flag suspicious activities early, allowing businesses to act before significant damage occurs.

4. How do fraudsters behave?

Fraudsters often display specific behavioral red flags such as living beyond their means, showing excessive secrecy, or taking risks that deviate from typical behavior. They might also make sudden, large financial transactions or attempt to bypass security measures.

5. How can AI help in detecting fraud?

AI analyzes large amounts of data in real time to spot unusual patterns and detect fraudulent activity early, often before significant damage occurs. It continuously learns from past fraud cases to improve its accuracy over time.

6. Why is continuous monitoring important in fraud detection?

Fraud is not always obvious right away. Continuous monitoring allows businesses to spot suspicious activity as it occurs, giving them the chance to react swiftly and minimize losses.

7. What is the role of employee training in fraud prevention?

Employee training helps staff identify potential fraud through social engineering, phishing, and other tactics. Educated employees are more likely to report suspicious activity, which can lead to early detection and prevention.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately