AiPrise

9 mins read

August 29, 2025

Cross-Border Payment Regulations: Global Compliance Guide

Key Takeaways

Moving money across borders is never as simple as pressing send. Every transaction has to pass through layers of regulation, covering anti-money laundering (AML), know your customer (KYC), sanctions checks, tax rules, and data privacy requirements. For businesses, even a small compliance gap can mean blocked payments, heavy fines, or reputational damage. Understanding cross-border payment regulations isn’t just about staying on the right side of the law; it’s what allows you to move funds reliably, avoid costly delays, and maintain trust with global partners. This guide breaks down the essentials: what these regulations cover, the common challenges businesses face, and the best practices that make international payments secure and compliant.

Key Takeaways

- Cross-border payment regulations require strict AML, KYC, tax, and sanctions compliance across multiple jurisdictions to prevent fraud and ensure transparency.

- Selecting fintech providers offers faster settlements, lower fees, and superior technology integration compared to traditional banks.

- Common challenges include regulatory fragmentation, high hidden costs, transaction delays, and currency volatility risks impacting payment efficiency.

- Best practices involve continuous regulatory monitoring, automated compliance tools, robust documentation, and strategic provider partnerships.

What Are Cross-Border Payment Regulations?

Cross-border payment regulations refer to the legal standards, compliance procedures, and operational guidelines that control how money moves between parties in different countries. These frameworks make sure every transaction meets requirements related to security, transparency, customer identity, and fraud detection, covering a wide range of payment types, wire transfers, ACH, cards, and mobile methods.

Cross-border payment regulations exist for the following reasons:

- Prevent financial crimes: Detect and deter money laundering, fraud, and terrorism financing.

- Protect consumer data and privacy: Safeguard information in compliance with local and international data laws.

- Ensure transparency and trust: Mandate clear reporting, cost disclosures, and transaction records for regulators and users.

- Enable global business: Standardize processes so companies can trade and pay across borders with confidence.

- Manage tax responsibilities: Help governments and businesses report, pay, and comply with international tax obligations.

Also Read: Understanding Regulatory Compliance: Definition And Requirements

Having outlined what cross-border regulations are and why they exist, the next step is to examine the major global frameworks that give these rules real weight and shape how international payments are managed.

Global Regulatory Frameworks Shaping Cross-Border Payments

International payments don’t move freely just because technology allows them to. They are funneled through overlapping layers of regulatory regimes, each carrying its own history, purpose, and enforcement muscle.

Some rules aim to fight crime, others to protect consumer privacy, and some to preserve national control over currency. Together, they form the backbone of modern cross-border payment compliance.

- FATF Standards: At the top of the chain are the Financial Action Task Force recommendations, which most jurisdictions use as their baseline. FATF doesn’t pass laws itself, but its blacklist of “high-risk” countries pressures governments and financial institutions worldwide to enforce strict AML and counter-terrorist financing checks.

- OECD and Tax Transparency: For businesses, tax reporting rules matter just as much as crime prevention. The OECD’s Common Reporting Standard (CRS) compels financial institutions to automatically share account information across borders, while the BEPS initiative closes loopholes that multinationals once used to shift profits. Both frameworks make tax compliance inseparable from cross-border payment planning.

- US Oversight: Because of the dollar’s dominance, US rules reach far beyond American borders. FinCEN enforces the Bank Secrecy Act’s recordkeeping and suspicious activity reporting, while OFAC sanctions lists can block a transaction between two non-US parties simply because it clears in dollars. In practice, nearly every international payment brushes against US regulatory oversight.

- European Directives: In Europe, PSD2 reshaped the payment landscape by mandating strong customer authentication and opening banking infrastructure to third parties. Alongside it, GDPR places strict guardrails on how payment providers handle personal and financial data, forcing compliance teams to think about both fraud and privacy at once.

- Regional Controls in Asia: Emerging markets add another layer of complexity. China maintains tight capital controls and requires state approval for large outbound remittances, while India’s FEMA restricts payments abroad by purpose and amount. Singapore, in contrast, has positioned itself as a fintech hub, balancing openness with rigorous AML enforcement.

- Sanctions and Global Watchlists: Finally, sanctions cannot be overlooked. Whether imposed by the UN, EU, US, or individual states, they can instantly freeze a payment flow. The burden falls on payment providers to screen every transaction in real time; failure to do so risks multimillion-dollar fines and reputational collapse.

Cross-border payments are shaped by a mix of international standards, regional directives, and national rules. Businesses that succeed treat compliance as a core function, not a formality. At the same time, execution depends on the specific actors, systems, and methods involved.

Key Components of Cross-Border Payments

Cross-border payments involve a complex ecosystem, each component critical for successful international transfers.

Let’s break down each piece for clarity and practical understanding:

Main Actors

- Payer: The individual or business initiating the transfer from one country.

- Payee: The recipient in a different country who receives the funds.

- Front-end Provider: Typically a bank, payment processor, or digital wallet that starts the payment flow.

- Correspondent/Intermediary Banks: These facilitate the transfer route when payer and payee banks don't have direct relationships; they form the backbone of global transactions, handling compliance, FX, and settlement steps.

- Card Networks: Visa, Mastercard, and others process card-based payments internationally, often adding currency conversion and compliance checks.

- Regulators: Central banks and national authorities establish the policies and oversee the entire transaction for AML, tax, and reporting standards.

Common Payment Methods

- Wire Transfers: Electronic transfers through SWIFT and other networks; trusted for large transactions but may involve intermediary banks and longer settlement times.

- International ACH/EFT: Electronic funds transfers using regional clearing systems; often used for salary payments and B2B transactions, offering cost efficiency and speed.

- Credit/Debit Card Payments: Card payments are processed through global networks, converted to the recipient's currency, and may incur additional fees, which can take longer to reconcile.

- Digital Wallets & Online Platforms: Digital wallets allow funds to move between countries quickly with built-in compliance tools and variable currencies.

- Cryptocurrency: Growing adoption for seamless peer-to-peer global payments; volatility and compliance concerns remain, but retailers increasingly use crypto.

Also Read: AML Compliance And Checks For Cross-Border Payments

Now that you understand the key players and components involved, let’s take a closer look at the exact process that facilitates seamless and secure money transfers across borders.

How Do Cross-Border Payments Work?

Cross-border payments involve a series of carefully coordinated steps to transfer funds from the payer in one country to the payee in another, all while complying with regulatory and operational requirements.

Here's a detailed breakdown of how these payments flow:

1. Payment Initiation

The payer authorizes the transaction using their preferred channel (bank transfer, card, digital wallet). The payment order includes details such as amount, currency, recipient information, and purpose.

2. Compliance Verification

Payment providers conduct mandatory checks, AML, KYC, and sanctions screening to verify both payer and payee identities and ensure the transaction does not violate regulations or risk profiles.

3. Currency Conversion

If the transaction involves different currencies, the payment provider or intermediary converts funds at prevailing foreign exchange (FX) rates. FX fees and spreads can vary significantly between providers.

4. Routing Through Correspondent Networks

When payer and payee banks do not have a direct relationship, correspondent or intermediary banks facilitate the transfer. These entities ensure secure transmission, compliance adherence, and settlement.

5. Settlement and Clearing

The funds settle in the payee’s bank/account after clearing all regulatory and operational hurdles. Settlement speed depends on the payment method; wire transfers may take 1-5 business days, while digital platforms can process faster.

6. Confirmation and Reporting

Both sender and recipient receive payment confirmation. In parallel, regulators require transaction reporting and record-keeping for audit and monitoring purposes.

Understanding the payment flow helps, but several key factors can make or break the speed, cost, and smoothness of your cross-border transactions.

Critical Factors Influencing Cross-Border Payment Performance

Several elements directly impact how efficiently and affordably cross-border payments are processed. Knowing these factors can help you optimize payment strategies and avoid hidden pitfalls. Key considerations include:

- Payment Method: Bank transfers usually take longer but are widely used; digital wallets and fintech platforms prioritize speed and cost efficiency.

- Regulatory Environment: Varies by country; stricter regimes mean longer processing and more documentation.

- Intermediary Layers: More correspondent banks increase costs and delays, reducing transparency.

- Currency and FX Volatility: FX management impacts settlement amounts and timing.

With a clear grasp of the factors that influence payment performance, it’s time to focus on proven practices that help businesses navigate cross-border payments smoothly and securely.

Best Cross-Border Payment Practices for Businesses

To ensure seamless, compliant, and cost-efficient international payments, businesses should implement the following focused best practices:

1. Develop a Comprehensive Compliance Program

- Establish formal Anti-Money Laundering, KYC, and sanctions screening policies tailored to your transaction volume and global footprint.

- Define clear roles and responsibilities for monitoring compliance and investigating suspicious activities.

- Regularly review and update the program to reflect regulatory changes and emerging risks.

2. Use Automated Compliance Tools

- Use software solutions for real-time KYC verification, sanctions screening, and transaction monitoring to minimize human error and speed up processing.

- Automate alerts for unusual payment patterns and automate regulatory reporting wherever possible.

3. Partner with Reputable Payment Providers

- Choose providers with a strong compliance infrastructure that supports cross-border regulatory requirements.

- Prefer those offering transparency on fees, FX pricing, and settlement times, plus integration with your internal systems for better data flow and control.

4. Regular Training and Auditing

- Continuously train finance, compliance, and operations teams on current cross-border regulations and threat trends.

- Conduct frequent internal audits to identify compliance gaps and inefficiencies.

5. Maintain Detailed Documentation

- Keep transaction records, due diligence files, and monitoring logs for a minimum of five years as required by most jurisdictions.

- Document decision-making processes for risk assessments, transaction approvals, and escalation protocols.

6. Optimize Currency and Payment Strategies

- Utilize multi-currency accounts and hedging strategies to minimize FX risks and costs.

- Consolidate payments where possible to reduce transaction fees and complexity.

Instead of navigating compliance alone, the provider you choose can make all the difference. The right partner determines how fast your payments move, how transparent the costs are, and how confidently you stay within regulatory boundaries.

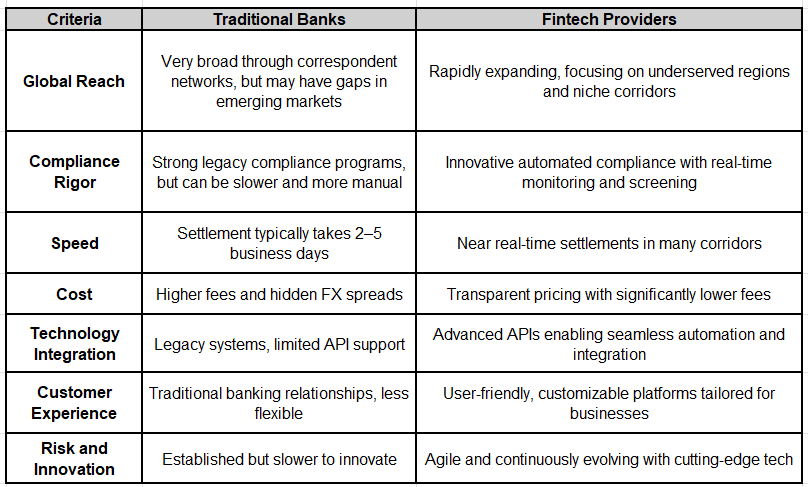

Bank vs. Fintech: Choosing the Right Payment Provider

Choosing the right payment provider is a critical decision that can impact your business’s cost, speed, and compliance when handling cross-border transactions. Both traditional banks and fintech firms offer unique advantages, but understanding their differences helps you pick the best fit for your specific needs.

Below is a detailed comparison highlighting why fintech providers are increasingly becoming the preferred choice for modern businesses.

After exploring the key factors and provider options, it’s time to understand how the right partner can simplify and secure your cross-border payment compliance.

How AiPrise Streamlines Cross-Border Payment Compliance and Onboarding

AiPrise specializes in helping businesses overcome the complexities of international payments through focused compliance and onboarding solutions tailored for global operations.

Here’s how AiPrise adds value with precision and efficiency:

- Automates KYC and AML checks with real-time, AI-driven identity verification to reduce manual workload and human errors.

- Continuously monitors transaction activity against up-to-date sanctions lists, tax regulations, and risk profiles.

- Facilitates cross-jurisdictional regulatory adherence by integrating diverse rule sets in one platform.

- Speeds onboarding with streamlined data collection that meets local and international regulatory standards.

- Supports multi-language and multi-jurisdiction functionality, optimizing user experience and reducing friction in new market entry.

- Enables customizable workflows to fit specific industry and client risk profiles.

Experience firsthand how AiPrise can transform your compliance and onboarding processes into strategic advantages. Click here to get started!

Wrapping Up

Cross-border payment regulations present complex challenges, but with the right knowledge and tools, businesses can confidently navigate compliance, reduce costs, and accelerate global growth.

Understanding regulatory frameworks, choosing the right payment provider, and implementing best practices are essential steps to avoid penalties, delays, and fraud.

AiPrise further simplifies compliance and onboarding, empowering your business to operate securely across multiple jurisdictions with ease.

Ready to transform your cross-border payment operations and stay ahead of regulatory demands?

Book A Demo with AiPrise today and experience seamless, compliant global payment processing designed to fuel your international expansion.

FAQs

1. What are the main risks of non-compliance with cross-border payment regulations?

Non-compliance risks include hefty fines, frozen accounts, legal sanctions, and severe reputational damage. It also leads to payment delays or rejections, disrupting cash flow and business operations globally. Regulatory bodies actively monitor transactions, increasing the chance of audits and penalties for non-compliant entities.

2. How do currency controls affect cross-border transactions?

Currency controls impose restrictions on foreign currency flows that can delay or restrict payments. Businesses may need prior approvals or must comply with limits on currency amount conversions. Failure to follow these controls invites penalties or transaction blocking, complicating international trade and financial planning.

3. Can blockchain technology fully replace traditional cross-border payment systems?

While blockchain enables faster, transparent, and lower-cost transfers, it faces challenges including regulatory uncertainty, scalability issues, and volatile acceptance across countries. Current blockchain solutions complement rather than replace traditional methods and require integration with existing systems to maintain compliance.

4. What role do sanctions lists play in cross-border payment compliance?

Sanctions lists flag individuals, entities, or countries restricted from receiving payments to prevent illegal financing and terrorism funding. Payment processors must screen every transaction against updated sanctions lists to avoid legal violations and financial penalties, ensuring secure and lawful cross-border transfers.

5. How often do businesses need to update customer KYC information for cross-border payments?

KYC updates are generally required annually or upon significant changes in customer status. Timely updates help detect suspicious activities early, maintain regulatory compliance, and reduce the risk of payment blocking or fines. Businesses must stay vigilant to changing client profiles and regulatory demands.

LinkedIn Snippet

Cross-border payments are no longer just a back-office task; they’re one of the toughest compliance hurdles in global business. FATF, OFAC, GDPR, and local currency rules overlap in ways that can stall cash flow, trigger fines, or block entire transactions.

The real edge comes from handling payments with precision: automating AML/KYC, managing FX risks, and choosing partners who prioritize both speed and compliance.

Our latest guide breaks down the regulations that matter most and how businesses can navigate them to keep international transactions secure and predictable.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately