AiPrise

12 min read

November 21, 2025

What Is Remediation in Banking and Its Process

Key Takeaways

Have you ever wondered how deep unseen compliance gaps might be impacting your bank’s bottom line and reputation? With the federal government estimating U.S. losses of $233 billion to $521 billion annually due to fraud, weak identification systems without KYC safeguards enable criminal activity. When you understand remediation in banking, including its process and real-world stakes, you’re better positioned to restore control, protect trust, and turn compliance into an advantage.

Quick Overview

- Remediation in banking is the structured process of identifying and fixing compliance gaps, control failures, and data inaccuracies to meet regulatory standards.

- It involves multiple stages, including issue identification, root-cause analysis, corrective action, and validation, to ensure long-term compliance and operational accuracy.

- Banks face recurring challenges like fragmented data, outdated documentation, and evolving regulations that complicate large-scale remediation efforts.

- Applying best practices such as risk-based prioritization, strong governance, and continuous monitoring helps restore compliance, rebuild trust, and prevent future regulatory issues.

What Is Remediation in Banking?

In banking, remediation refers to the systematic process of identifying, correcting, and validating issues in systems, controls, customer data, or processes that leave an institution exposed to risk. It typically arises when regulatory findings, audit gaps, system failures, or customer complaints reveal that something has gone wrong, and the bank must take action to fix it.

Remediation can encompass:

- Correcting outdated or incomplete KYC/KYB files

- Addressing AML/CTF control weaknesses

- Fixing system or process errors that caused customer harm

- Re-verifying customer identity or business counterparties

- Updating policies, training, and operations to prevent recurrence

Unlike one-off fixes, remediation in banking often involves large-scale program, complex data sets, and the requirement to demonstrate to regulators that the fix is effective and sustainable. Understanding what remediation involves is only the first step. To see why it matters, you need to look at the risks that come with ignoring it and the long-term stability that comes from doing it right.

Why Banking Remediation Is a Necessity?

You might wonder, if operations seem fine, why should remediation be a priority? The answer is simple: when small compliance gaps go unchecked, they quickly turn into costly, reputation-damaging problems that can disrupt your entire business.

- Regulatory risk and fines: Regulators expect you to act fast when compliance controls fail or customer harm is identified. Ignoring or delaying remediation can lead to heavy fines, enforcement actions, and ongoing regulatory scrutiny that disrupts your daily operations.

- Customer trust and reputation: Your customers expect clear communication and fair resolution when issues arise in their accounts. Inadequate remediation weakens trust, sparks public criticism, and can push long-term clients toward competitors who demonstrate stronger accountability.

- Operational risk: Weak data systems, outdated controls, and disconnected departments increase operational strain and cost inefficiency. A well-structured remediation program helps you fix those issues while strengthening your internal processes for sustainable performance.

- Business continuity and growth: Unchecked control failures or data gaps can stall your expansion into new products or markets. Strong remediation ensures you meet compliance demands, maintain customer confidence, and keep growth plans on track without unexpected regulatory roadblocks.

The value of remediation becomes even clearer once you understand how it actually works. Each phase of the process builds accountability, ensures accuracy, and demonstrates to regulators that your bank takes compliance seriously.

Also read: Comprehensive Guide to Embedded Banking and Finance

The Remediation Process in Banking

Every successful remediation program in banking follows a clear, methodical structure designed to correct errors without disrupting daily operations. When compliance gaps emerge, having a defined process helps you restore data integrity, meet regulatory demands, and maintain customer confidence. Here are the essential stages that make banking remediation effective, measurable, and sustainable:

Issue Identification

Your first step is identifying what triggered the remediation process: regulatory findings, audit issues, or customer complaints. You need to pinpoint exactly where and how controls failed before moving forward. A clear understanding of the root cause sets the foundation for every corrective action that follows.

Scope and Prioritization

Once you know what went wrong, determine which customers, accounts, or processes are affected. You’ll need to segment the impacted population based on risk severity, financial exposure, and potential reputational harm. This prioritization helps you focus resources efficiently and prevent small issues from turning into larger compliance risks.

Gap Analysis and Root-Cause Investigation

At this stage, you’ll compare your current processes against required standards to uncover where compliance gaps exist. For example, missing beneficial ownership data or untriaged AML alerts can reveal weak oversight areas. Identifying the underlying reasons behind these failures ensures your solutions address the root cause, not just the symptoms.

Data Review and Documentation

Remediation requires a deep review of customer files, onboarding data, and transaction logs across systems. During this process, you’ll identify missing or outdated documents, such as government-issued IDs, business registrations, or proof of address. Consolidating this data ensures your institution holds valid, verifiable records that meet both internal and regulatory requirements.

Corrective Action Planning

With your findings in place, it’s time to create an actionable plan to fix the identified issues. This involves updating policies, retraining teams, improving systems, or compensating impacted customers where necessary. Assign clear roles, establish timelines, and define metrics to measure your progress objectively.

Implementation

Now you’ll put your plan into motion, starting with targeted outreach to customers or business partners. This phase includes updating internal controls, fixing workflow errors, and ensuring all systems reflect the corrected data. Collaboration between compliance, IT, and operations teams is essential to maintain speed and accuracy.

Monitoring, Tracking, and Reporting

Continuous oversight keeps your remediation process accountable and transparent. You’ll track metrics such as files remediated, control issues resolved, and timelines met, ensuring steady progress. Regular reports to management and regulators, supported by dashboards and governance reviews, reinforce compliance credibility.

Validation and Closure

Before closure, independent validation ensures your remediation program has fully resolved the underlying issues and that controls function properly. Internal audit or third-party reviewers often confirm this step to satisfy regulatory expectations. Once validated, officially close the project, but maintain ongoing monitoring to prevent repeat issues.

The process may seem intensive, but it relies on one foundational element, documentation. Without accurate IDs, records, and audit trails, even the best remediation plan can fall short of compliance standards.

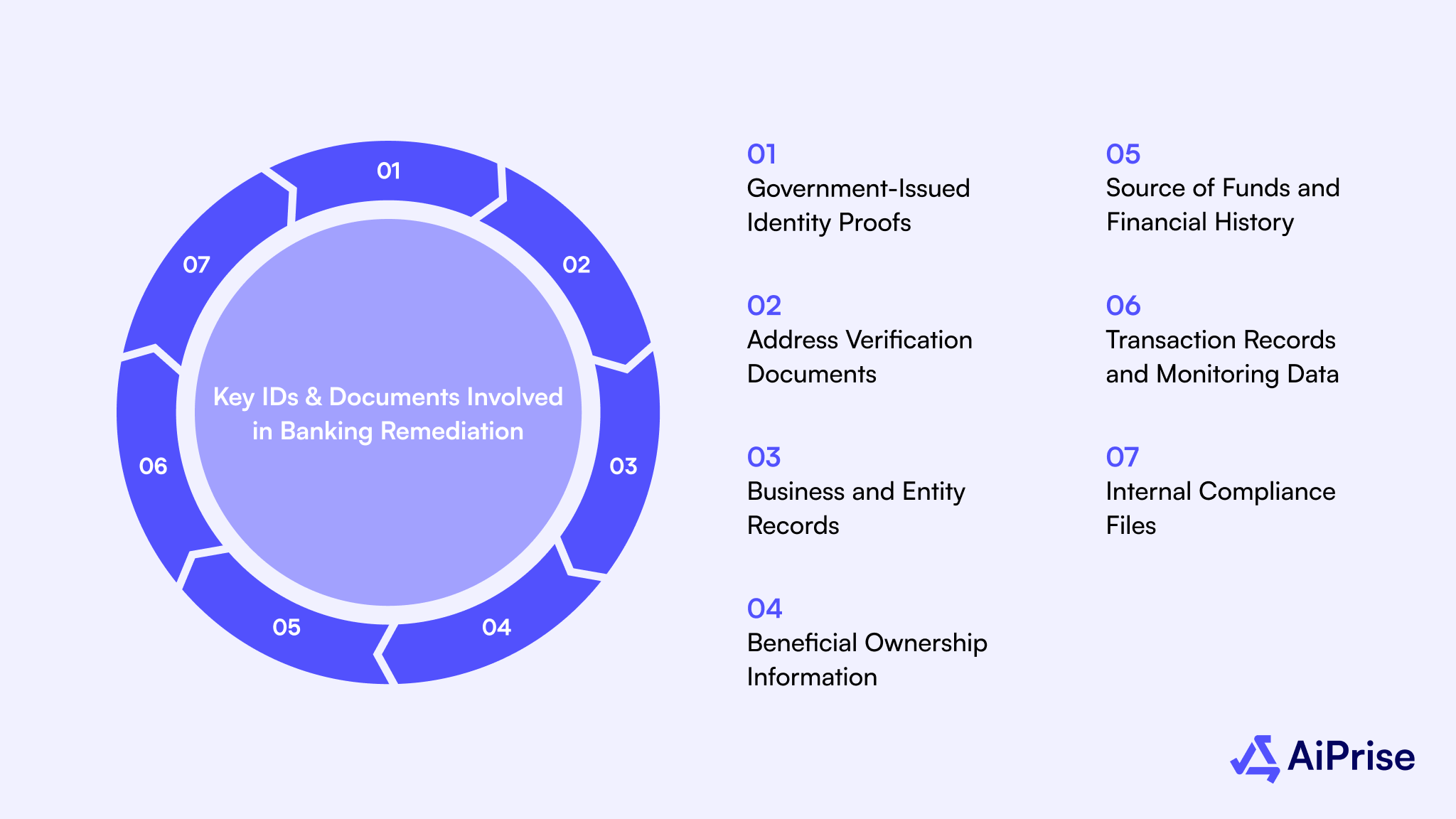

Key IDs & Documents Involved in Banking Remediation

Every remediation program depends on accurate and verifiable documentation. When regulators demand proof of compliance, your ability to present updated and authentic customer records determines how efficiently you can close the case. Below are the key documents you’ll need, layered by their purpose and verification depth.

Government-Issued Identity Proofs

Passports, driver’s licenses, or national IDs are the major parts of customer verification. During remediation, you often need to revalidate expired or low-quality IDs from legacy accounts. For instance, when several U.S. banks updated their KYC archives post-AML reviews, missing or outdated IDs were among the most common root causes of non-compliance.

Address Verification Documents

Banks rely on recent utility bills, rental agreements, or official correspondence to confirm customer residency. These records help detect duplicate or synthetic profiles and ensure that risk categorization aligns with geography. In remediation projects, unverified addresses frequently flag dormant or potentially fraudulent accounts that must be reviewed or closed.

Business and Entity Records

For corporate customers, remediation often involves cross-checking business registrations, incorporation certificates, and tax identification numbers. This helps validate a company’s legal existence and jurisdictional compliance. Financial institutions with multinational clients, like cross-border payment providers, often find that entity documentation gaps drive large portions of remediation workload.

Beneficial Ownership Information

Banks must identify the individuals who ultimately own or control a business. During remediation, you’ll often request shareholder lists or updated beneficial ownership declarations to meet FinCEN’s Beneficial Ownership Rule. Many institutions discovered after global AML reviews that earlier onboarding records lacked this transparency, prompting large-scale KYB remediation campaigns.

Source of Funds and Financial History

Where money comes from matters just as much as who owns it. Reviewing payslips, audited statements, or prior transaction data helps confirm that funds originate from legitimate activities. In high-risk cases, such as politically exposed persons (PEPs) or offshore entities, these checks are central to risk reassessment and AML remediation.

Transaction Records and Monitoring Data

- Detailed transaction histories reveal whether a customer’s activity matches their declared profile. During remediation, banks often revisit historical transaction patterns to detect missed anomalies or patterns of layering. This ensures past control failures are corrected and future monitoring rules are better calibrated.

- Internal Compliance Files

- Finally, every remediation program depends on a clean internal trail, policy updates, audit results, and communication logs that show exactly how the issue was addressed. These files provide evidence that your remediation actions were deliberate, documented, and regulator-ready. They also help demonstrate to auditors that corrective measures are embedded into your ongoing control environment.

Once your documentation framework is sound, the next step is understanding how remediation compares with similar corrective approaches, and why its scope extends far beyond routine corrections.

Also read: Fraud Detection and Prevention Strategies in Banking

How Remediation Differs from Correction and Rectification?

Understanding the distinction between remediation, correction, and rectification helps you apply the right response to each compliance issue. Here’s how these three approaches differ in purpose, scope, and long-term impact within banking operations:

This table helps clarify that remediation is broader in scope and strategic in nature, rather than simple correction or rectification. Recognizing these differences helps you choose the right course of action, because while correction resolves an issue, remediation ensures it never resurfaces.

Key Challenges Banks Face During Remediation

Banking remediation rarely unfolds smoothly; it’s complex, time-bound, and often reveals hidden weaknesses within existing systems. The obstacles below are the most common reasons remediation programs struggle to stay on track or deliver consistent results.

- Fragmented Customer Data: Information spread across legacy systems and departments creates inconsistencies that slow validation and cause repeated compliance errors. These data gaps make it difficult to prove regulatory accuracy when auditors request evidence.

- Outdated Documentation: Many customer records rely on expired or incomplete identification documents collected years ago. During remediation, tracking and updating this information at scale becomes a major operational burden.

- High Volume of Affected Accounts: Large institutions often find that control failures touch thousands of customer files simultaneously. Managing these volumes under strict timelines strains resources and exposes inefficiencies in workflow systems.

- Customer Non-Responsiveness: Some customers fail to respond to verification requests or provide missing details, especially for dormant or inactive accounts. This slows progress and can force banks to escalate or freeze unverified profiles.

- Constantly Changing Regulations: Evolving KYC and AML frameworks mean remediation plans often need mid-course corrections. What started as a compliance update can quickly expand into a full-scale revalidation exercise due to new guidance.

- Limited Skilled Personnel: Banks frequently face shortages of experienced compliance professionals who can manage remediation while handling ongoing operations. This leads to inconsistent data reviews and extended project timelines.

- Inconsistent Governance and Oversight: Without clear accountability, remediation programs risk delays, miscommunication, and duplicated efforts across departments. The absence of unified leadership often results in fragmented execution.

- Technology Limitations: Manual tracking tools and siloed systems make it difficult to measure progress or ensure version control. Incomplete automation increases the likelihood of reporting discrepancies and audit findings.

- Escalating Costs and Timelines: Unexpected data quality issues or additional regulatory demands can extend project duration and inflate budgets. For many banks, remediation quickly shifts from a compliance task to a financial strain.

Each challenge exposes areas that require better governance, clearer accountability, or smarter data management, all of which shape how effectively remediation achieves its goals.

Also read: How KYC Is Done In Banks: A Step by Step Guide

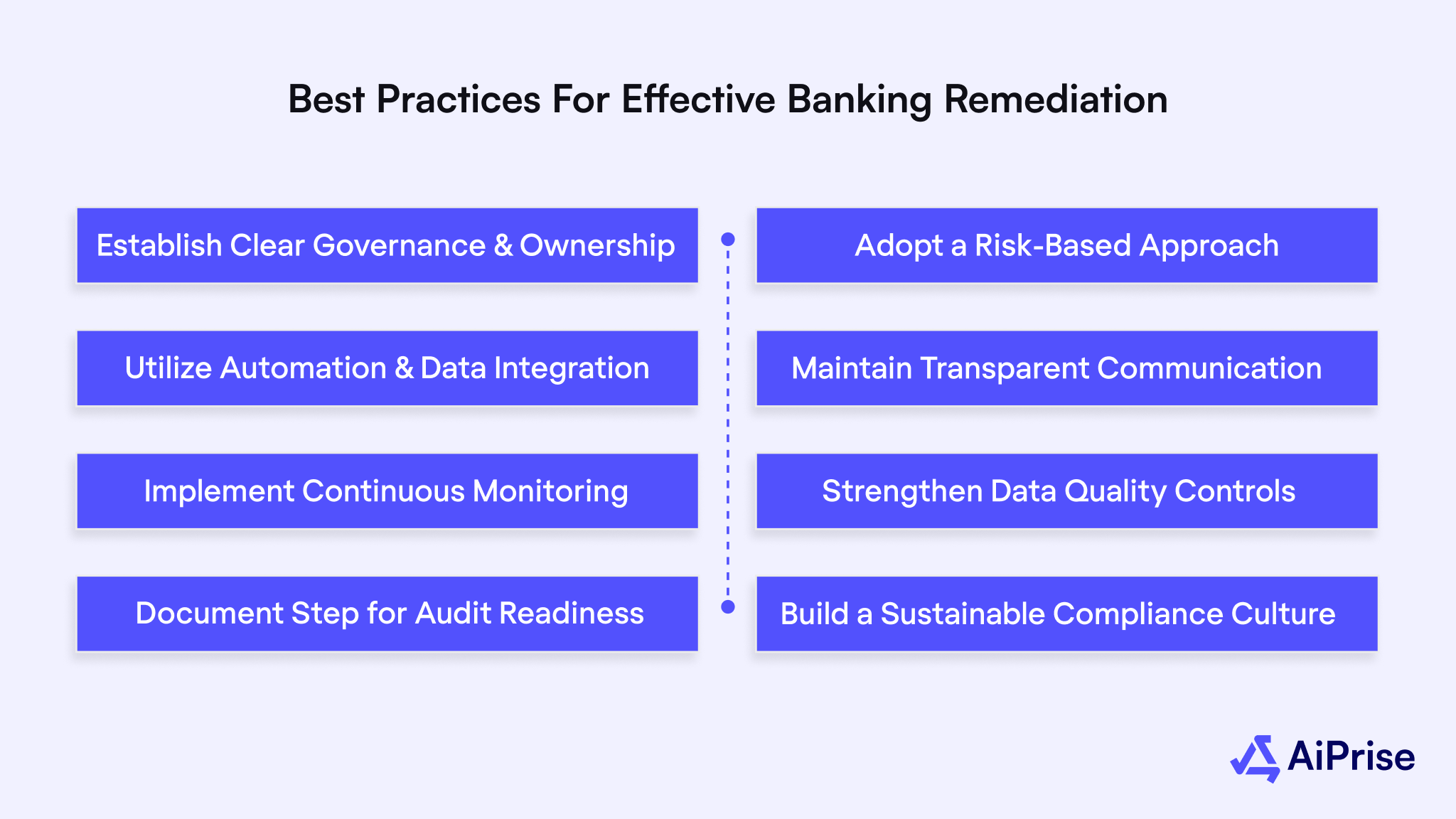

Best Practices for Effective Banking Remediation

Strong remediation programs don’t rely on quick fixes; they’re built on structure, accountability, and foresight. By adopting disciplined practices, you ensure that every corrective effort strengthens your institution’s compliance posture instead of merely patching gaps. Below are proven best practices that help banks deliver effective, consistent, and regulator-ready remediation outcomes.

1. Establish Clear Governance and Ownership

Every remediation program needs a well-defined command structure with accountability at both executive and operational levels. Appointing a steering committee and project leads ensures decisions are made quickly and responsibilities are transparent. This clarity prevents overlaps, eliminates delays, and builds regulator confidence in your control environment.

2. Adopt a Risk-Based Approach

Not every issue carries the same level of risk; prioritization is key. By segmenting customers, products, or accounts based on risk exposure, you can allocate resources where they matter most. This targeted focus accelerates timelines and ensures higher-risk areas receive immediate attention.

3. Utilize Automation and Data Integration

Automation helps you move faster and with fewer manual errors during large-scale remediation. Integrating KYC, AML, and customer data across systems creates a single, reliable source of truth. This unified data environment enhances accuracy, improves monitoring, and simplifies audit reporting.

4. Maintain Transparent Communication

Remediation involves multiple stakeholders, customers, regulators, and internal teams, all expecting clarity. Regular updates about progress, scope changes, and milestones keep everyone aligned and informed. Transparency not only prevents confusion but also strengthens credibility with oversight bodies.

5. Implement Continuous Monitoring and Validation

Once remediation is complete, monitoring shouldn’t stop there. Regular validation of controls ensures the same issues don’t resurface over time. By embedding continuous review cycles, you convert remediation from a one-time project into an ongoing assurance process.

6. Strengthen Data Quality Controls

Poor data quality is one of the most common triggers for remediation. Establishing rigorous standards for data entry, maintenance, and validation helps prevent future inaccuracies. When your data remains clean and traceable, compliance reviews become faster and less resource-intensive.

7. Document Every Step for Audit Readiness

Comprehensive documentation is your strongest defense during regulatory reviews. Detailed records of decisions, communications, and corrective actions prove that your bank acted responsibly and systematically. These logs not only satisfy auditors but also serve as internal learning tools for future improvement.

8. Build a Sustainable Compliance Culture

Remediation success depends on more than systems; it relies on people. Encouraging teams to view compliance as a shared responsibility helps prevent repeat failures. When every employee understands the “why” behind controls, remediation evolves into a proactive, organization-wide discipline.

With AiPrise supporting remediation, your institution can shift focus from chasing compliance gaps to maintaining a continuously verified and regulator-ready environment.

How AiPrise Helps Banking Remediation?

AiPrise plays a crucial role in helping banks execute remediation programs faster, more accurately, and with complete regulatory confidence. Its AI-powered platform streamlines verification, closes compliance gaps, and strengthens data integrity across large customer and account populations.

- Accelerated KYC and KYB Revalidation: AiPrise automatically identifies outdated or incomplete KYC and KYB files that require remediation. This ensures every customer or business record is verified, up to date, and regulator-ready.

- Accurate Document and Identity Verification: The platform uses OCR and AI to scan and authenticate government-issued IDs within seconds. It eliminates manual review delays that often slow large-scale remediation efforts.

- Biometric Reconfirmation for Legacy Accounts: Through facial recognition and liveness detection, AiPrise revalidates customer identities in dormant or legacy accounts. This helps banks ensure that every active profile belongs to a genuine individual.

- Continuous Risk Monitoring Post-Remediation: Once remediation is complete, AiPrise keeps monitoring customers for sanction list changes or risk pattern shifts. This ongoing surveillance prevents previously cleared accounts from reintroducing compliance risk.

- Automated Data Cleanup and Case Management: AiPrise integrates directly into existing banking systems to automate data correction, validation, and case tracking. This reduces manual errors and shortens remediation closure timelines significantly.

- Real-Time Fraud Detection and Alerting: By analyzing data from multiple trusted sources, AiPrise detects suspicious activities tied to remediated accounts. Its risk scoring engine ensures fraudulent behaviors are caught before they escalate.

- Scalable Support for Large Remediation Projects: Whether you’re updating millions of customer profiles or revisiting high-risk segments, AiPrise scales effortlessly. It delivers consistent accuracy across geographies and departments without slowing your compliance teams down.

Wrapping Up

Remediation in banking isn’t just about fixing what went wrong; it’s about proving long-term control and compliance maturity. When processes, data, and governance align, you build credibility with both regulators and customers. A structured remediation approach ensures your institution stays resilient, transparent, and prepared for future regulatory scrutiny.

AiPrise makes that transformation faster, smarter, and easier for modern banks. Its AI-driven verification, continuous monitoring, and automated workflows remove friction from large-scale remediation projects. With AiPrise, you can rebuild trust, restore compliance, and confidently move forward with a stronger, more secure banking ecosystem.

Book A Demo today to see how AiPrise can transform your banking remediation into a faster, smarter, and fully compliant operation.

FAQ

1. What does remediation in banking mean?

Remediation in banking refers to the process of identifying and correcting compliance, data, or control gaps within a financial institution. It ensures that customer records, policies, and systems meet regulatory standards and operate without risk exposure.

2. What is remediation in KYC?

KYC remediation involves reviewing and updating customer identity records to ensure they meet the latest compliance and documentation requirements. It typically includes re-verifying IDs, collecting missing information, and removing outdated or inconsistent data from the bank’s systems.

3. What is a remediation payment?

A remediation payment is compensation made to customers who were negatively affected by an error, system failure, or compliance lapse. Banks issue these payments to correct financial harm and demonstrate accountability to regulators and customers.

4. What does remediation mean on my bank statement?

When you see “remediation” on your bank statement, it usually refers to a refund or adjustment related to a past banking error. This could include fee reversals, interest corrections, or compensation from a regulatory remediation program.

5. What is the difference between KYC refresh and KYC remediation?

A KYC refresh is a routine review of customer information conducted periodically to keep data current. KYC remediation, on the other hand, is a corrective process triggered when compliance issues or data deficiencies are discovered and need immediate action.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately