AiPrise

6

September 3, 2025

How KYC Is Done In Banks: A Step by Step Guide

Key Takeaways

Banks rely on KYC to prevent fraud, meet regulatory standards, and maintain customer trust. Yet, balancing compliance with operational efficiency is increasingly challenging. Customers expect speed, while regulators demand accuracy. In a recent survey, over 90% of organizations considered switching banks due to KYC pain points.

This gap leaves banks caught in the middle, making it essential to understand how KYC is done in banks. In this blog, you’ll explore the entire KYC process, common challenges, and how modern AI and ML solutions can simplify compliance efficiently.

At A Glance:

- KYC helps banks prevent fraud, comply with regulations, and establish customer trust effectively.

- Banks follow a step-by-step KYC process of customer identification, document verification, risk assessment, and ongoing monitoring.

- Common challenges include high costs, slow verification, customer drop-offs, and evolving regulatory requirements.

- AI and ML solutions streamline verification, enhance fraud detection, and reduce manual compliance burdens.

- Choosing modern KYC solutions ensures scalability, accuracy, and efficiency for banks managing compliance pressures.

What Is KYC In Banking And How Do Banks Use It?

Before we get into the detailed process of how KYC is done in banks, let’s start with the basics. In banking, Know Your Customer (KYC) is the process used to confirm a client’s identity when they open an account. It helps banks verify that customers are exactly who they claim to be.

Banks don’t just use KYC at the start of the relationship; it continues throughout the customer lifecycle. Banks use KYC to:

- Confirm a customer’s identity with valid documents.

- Assess the risks of doing business with them.

- Spot unusual activity by comparing it to expected account behavior.

- Keep protection in place through regular identity checks.

Why Does KYC Matter For Banks?

KYC goes beyond meeting regulatory rules, acting as a safeguard that protects both banks and their clients.

For banks, KYC provides a framework to comply with anti-money laundering (AML) and counter-terrorist financing (CTF) regulations. Without it, institutions face penalties, reputational damage, and higher exposure to financial crime.

For clients, effective KYC ensures that institutions consider their financial profile before extending services such as loans, investments, or advisory products. This reduces the risk of unsuitable recommendations and protects long-term financial security.

Also Read: How Businesses Can Benefit from Free KYC Verification

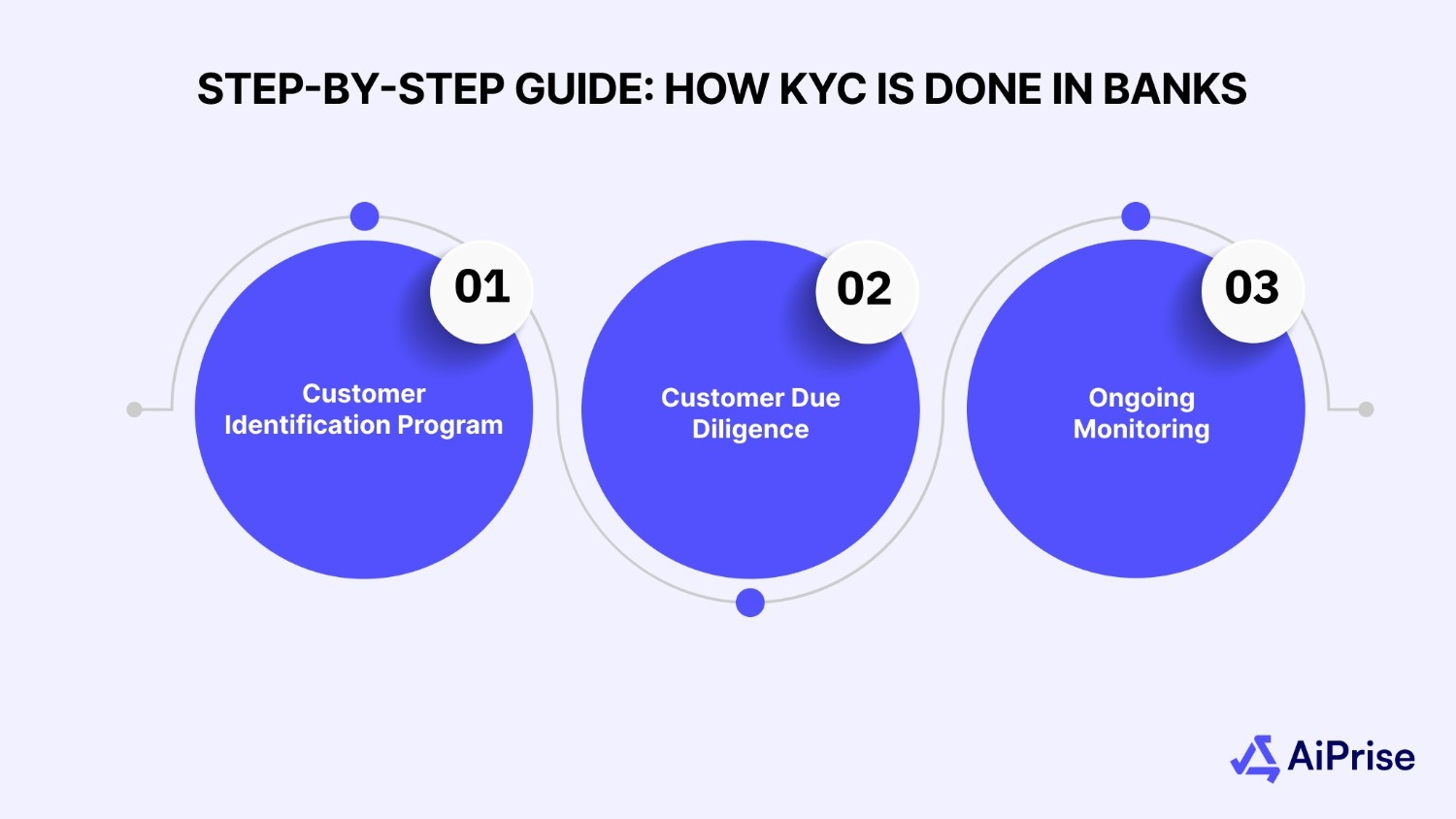

Step-by-Step Guide: How KYC is Done in Banks

KYC isn’t just a one-time verification. In the U.S., it starts when banks onboard new customers and continues through ongoing checks. Here’s how it usually works:

Step 1: Customer Identification Program (CIP)

The first step is verifying who the customer is. This includes collecting personal details such as name, address, date of birth, and government-issued ID numbers.

For businesses, banks request documents like incorporation certificates, partnership deeds, and business licenses. Regulators expect these processes to be clearly defined, standardized, and consistently followed across all customer types.

Step 2: Customer Due Diligence (CDD)

Once identity is verified, the next focus is on understanding the client’s risk level. This step helps banks determine the level of oversight required for each relationship.

- Standard due diligence: Basic checks applied to all clients, including location and transaction habits.

- Simplified due diligence: Used for lower-risk clients, requiring fewer checks while still monitoring activity.

- Enhanced due diligence: Applied to higher-risk clients, with more extensive verification, external database checks, and continuous review.

Step 3: Ongoing Monitoring

KYC doesn’t stop after onboarding. Banks must continuously monitor transactions and behavior throughout the client relationship.

This includes tracking unusual patterns, checking sanctions or politically exposed person (PEP) lists, and reviewing adverse media coverage. If new risks arise, the client’s profile is updated to reflect the change.

While the KYC process may look straightforward, the constantly shifting regulations and growing complexities make execution harder than expected.

Also Read: Understanding the Differences and Relationship Between KYC and CDD

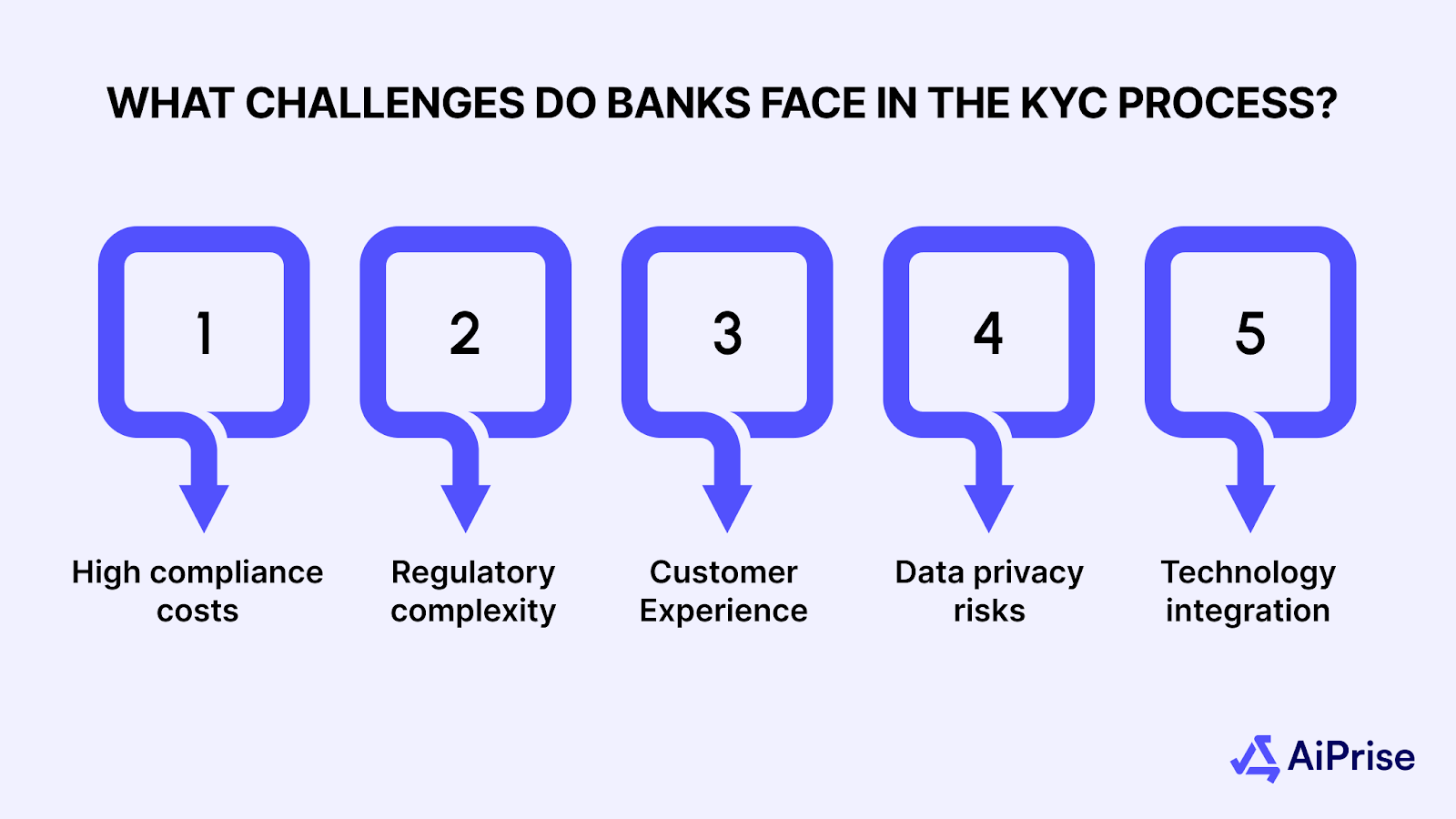

What Challenges Do Banks Face In The KYC Process?

Even with strict compliance frameworks, KYC is not without challenges. From mounting costs to customer experience, banks face significant obstacles like:

High Compliance Costs

Conducting due diligence requires significant manpower, advanced tools, and constant training. In 2024, most U.S. banks spent between $2,001 and $2,500 to complete a single corporate client KYC review. For high-risk clients, the resources required to verify, monitor, and periodically review accounts add up quickly, driving operational expenses even higher.

Regulatory Complexity

Regulatory requirements vary by jurisdiction and evolve constantly. For global banks, staying compliant across regions while keeping processes consistent is a major challenge, often leading to delays and high compliance costs.

Impact on Customer Experience

Extensive documentation and long verification times can frustrate customers during onboarding. Delays or repeated requests for information reduce satisfaction, damage trust, and often push clients toward competitors offering faster, more seamless KYC processes.

Data Privacy Risks

Banks handle large volumes of sensitive personal and corporate data. Ensuring strong safeguards and full compliance with data protection laws is a constant pressure point, especially when breaches can damage trust and reputation.

Technology Integration

Adopting advanced technologies like AI and automation is essential, but not always seamless. Legacy systems in banks often struggle with integration, requiring significant upgrades and investment. This gap slows digital transformation, limiting efficiency gains from modern KYC solutions.

These challenges highlight why traditional methods often fall short. So, how is KYC done in banks with modern technology? Let’s take a look.

How Are AI And Machine Learning Changing KYC In Banking?

KYC has always been resource-heavy, but AI and machine learning are making it faster, smarter, and more reliable. Here’s how they reshape KYC for financial institutions:

- Faster onboarding: AI scans vast data sources, verifies identities, and flags risks in real time. This reduces delays during onboarding, ensuring compliance without slowing customer acquisition or frustrating new clients.

- Reduced manual work: Machine learning eliminates repetitive verification tasks, minimizing errors and false positives. This allows compliance officers to focus their expertise on complex cases, instead of routine checks, improving decision-making.

- Simplified compliance: AI adapts to changing laws across jurisdictions by ingesting region-specific data sources. This allows banks to stay compliant globally while following a consistent risk-based approach in new markets.

Now that you know how AI is changing compliance, the next question is: how do you ensure you choose the right KYC solution? Keep reading to find out.

What Features Should Banks Look For In A Modern KYC Solution?

Picking the right KYC platform goes beyond ticking compliance boxes. Here are the essential features you should focus on when evaluating providers:

- Automation and scalability: A reliable KYC solution should automate monitoring and scale with increasing transactions. This ensures faster checks and consistent accuracy across customers in diverse jurisdictions.

- Seamless integration: The platform must integrate smoothly with existing systems through APIs. Real-time alerts and automated workflows reduce manual work and keep compliance processes flowing efficiently.

- Strong data protection: Encryption keeps customer information safe. By following AML data security rules, banks can protect sensitive details and maintain trust while handling large volumes of financial data.

KYC has moved beyond compliance to become a driver of trust and efficiency. With solutions like AiPrise, banks can accelerate onboarding, reduce fraud risks, and maintain compliance across regions, without compromising the customer experience.

How Aiprise Helps Banks Accelerate Their KYC Processes?

Banks face constant pressure to balance compliance, customer experience, and fraud prevention. AiPrise offers a comprehensive KYC suite designed to make this balance easier and more efficient.

With AiPrise, banks can:

- Global Coverage: Verify customers in 220+ countries with support for passports, IDs, and driver’s licenses.

- Verify instantly with government databases: Instantly match ID details and selfies against trusted government sources for faster onboarding.

- Proof of address verification: Quickly confirm customer addresses using trusted data sources to strengthen KYC checks.

- Watchlist and AML screening: Automate checks against sanctions lists, PEPs, and adverse media with continuous updates.

- Fraud detection: Block deepfakes, synthetic identities, and high-risk profiles through AI-driven checks.

- Case Management & Vendor Consolidation: Streamline investigations, reduce manual effort, and cut vendor complexity.

By combining advanced verification and fraud prevention, AiPrise helps banks make their KYC processes both regulation-ready and customer-friendly.

Summing Up

KYC in banking has evolved beyond basic identity checks. From initial onboarding to continuous monitoring, banks must adapt to regulatory shifts and operational challenges. Understanding how KYC is done in banks shows why balancing compliance, cost, and customer experience is so critical.

AI and machine learning help strike this balance by detecting fraud faster, cutting false positives, and automating routine checks without compromising compliance. For banks, the key lies in adopting solutions that don’t just meet regulations but also strengthen trust and efficiency at scale.

AiPrise helps institutions accelerate this journey with AI-powered KYC tools, real-time monitoring, and seamless integrations. Want to see how it fits into your processes? Book A Demo today.

FAQ’s

1. What is an example of a KYC in a bank?

A common example is when banks ask new customers to submit government-issued ID and proof of address before opening an account. This helps confirm identity and prevent fraudulent activity.

2. How long does it take to do KYC in a bank?

The timeline depends on the bank and verification method. In many cases, KYC processes may take up to a week.

3. Why do banks carry out KYC?

Banks perform KYC to verify customer identities, comply with anti-money laundering regulations, and reduce the risk of fraud or illegal financial activity. It also builds long-term trust with clients.

4. What happens when KYC is not done?

Without KYC, banks face regulatory fines, reputational damage, and even restrictions on operations. For customers, it can mean blocked transactions, frozen accounts, or being denied new services.

You might want to read these...

.jpg)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately