AiPrise

10 min read

December 3, 2025

KYC and AML in Qatar: Strengthening Identity Verification Standards

Key Takeaways

Tighter scrutiny across Qatar’s banking and fintech sectors has made compliance leaders increasingly anxious about missing red flags during onboarding and monitoring. Rising transaction volumes amplify this concern. In May 2025 alone, 1.645 million financial transactions worth QAR 2.586 billion were processed, with government oversight zeroing in on irregularities and suspicious activities. For many in finance, payments, and crypto, the pressure to keep every check watertight is real; one slip could mean steep penalties or frozen operations. Gaining a clear grasp of KYC and AML standards in Qatar helps your business stay compliant, streamline verification, and protect its reputation in a closely watched market.

Key Takeaways

- Qatar’s AML Law No. 20 of 2019 mandates stricter KYC, KYB, and AML checks to combat financial crime and protect the integrity of its banking system.

- Financial institutions, payment providers, crypto platforms, and DNFBPs must verify identities, report suspicious transactions, and follow risk-based compliance measures.

- Enhanced Due Diligence (EDD), e-KYC, and continuous monitoring are now core expectations, ensuring real-time fraud detection and transparency.

- Stronger verification standards and unified regulatory guidance from QCB and QFCRA are driving faster, safer, and more compliant onboarding across Qatar.

What Is KYC in Qatar?

KYC in Qatar refers to the process by which you verify the identity of individuals and businesses to meet regulatory requirements under the country’s AML/CFT law.

Here are the key elements you need to consider:

- Document verification for individuals using the Qatari National ID, ICAO-compliant passports, and proof of address that meet regulator standards.

- For businesses, you must obtain the Commercial Registration (CR), Memorandum of Association, beneficial ownership details, and proof of control before onboarding.

- Ongoing customer due diligence (CDD) that updates records, monitors transaction patterns, and flags changes in risk profile as required under Law No. 20 of 2019.

- Record-keeping of customer identification, transaction logs, and screening results for a period of 10 years in line with Qatari regulations.

With the groundwork of KYC understood, the next step is seeing how it fits into Qatar’s broader AML framework, the rules that govern every verification you perform.

What Are the AML Regulations in Qatar?

The AML regulations in Qatar set out mandatory obligations for you to prevent money laundering and terrorism financing, aligned with international standards under Law No. 20 of 2019.

Here are the crucial regulatory pillars:

- Adoption of a risk-based approach requires you to assess and document risks associated with customers, products, transactions, and jurisdictions.

- Customer due diligence (CDD) obligations when establishing business relations, conducting occasional transactions, or dealing with high-risk clients.

- Suspicious transaction reporting (STR) requirement where you must submit any suspicious activity to the Qatar Financial Information Unit (QFIU) and freeze funds if requested under the competent authority.

- Broad coverage, including financial institutions and Designated Non-Financial Businesses and Professions (DNFBPs) such as legal, real-estate, precious metals, and accountants, under the law’s scope.

Also read: KYC onboarding and AML considerations

Knowing the laws is one part; understanding who enforces them gives your compliance strategy real direction.

Who Enforces AML Compliance in Qatar?

Enforcement of AML compliance in Qatar is carried out by multiple regulatory bodies that oversee you depending on your sector and licence type.

Here are the key regulators you should engage:

- Qatar Central Bank (QCB) regulates banks, exchange houses, and payment service providers, and oversees AML/CFT instructions in the financial sector.

- Qatar Financial Centre Regulatory Authority (QFCRA) regulates firms operating in the Qatar Financial Centre (QFC) and implements AML/CFT rules aligned with Law 20 of 2019.

- The QFIU receives and analyses STRs, coordinates with law enforcement agencies, and supports the national risk assessment process under the national committee structure.

Knowing who holds you accountable clarifies the “why,” but understanding who must comply paints the complete picture.

Who Must Comply with KYC Requirements in Qatar?

Under Qatari regulation, you must comply with KYC requirements if you operate in sectors identified as high-risk or regulated for AML/CFT purposes.

Here are the entity types that must comply:

- Licensed banks, finance companies, money-exchange houses, payment service providers, and fintech firms registered under the jurisdiction of the QCB.

- Firms operating inside the Qatar Financial Centre (QFC) under QFCRA licensing, including international financial institutions and service providers to offshore clients.

- Designated Non-Financial Businesses and Professions (DNFBPs) such as real-estate brokers, precious-metals traders, accountants, auditors, and legal service providers, when they engage in relevant transactions.

- Virtual asset service providers (VASPs) and other emerging payment or digital asset firms that fall within the regulatory perimeter must apply the same KYC/AML controls.

Also read: How AI is Transforming AML Compliance

Once you know who must comply, the next question is when to step up due diligence, because not every customer carries the same level of risk.

When Is Enhanced Due Diligence (EDD) Required?

Enhanced Due Diligence applies when you identify heightened risk scenarios that cannot be adequately mitigated through standard customer due diligence measures.

Here are the situations calling for EDD:

- Customers with politically exposed persons (PEPs) status, non-resident clients, or clients from high-risk jurisdictions require deeper verification and ongoing monitoring.

- Complex ownership structures, large or unusual transactions, or clients whose business model raises suspicion of money-laundering or terrorism-financing risk.

- Use of new products or delivery channels that are vulnerable to misuse and where additional controls (such as source-of-fund checks, senior-management sign-off, and more frequent review) are mandated.

Once these risk layers are recognised, the next focus is on how Qatar is raising verification standards to make compliance stronger and faster.

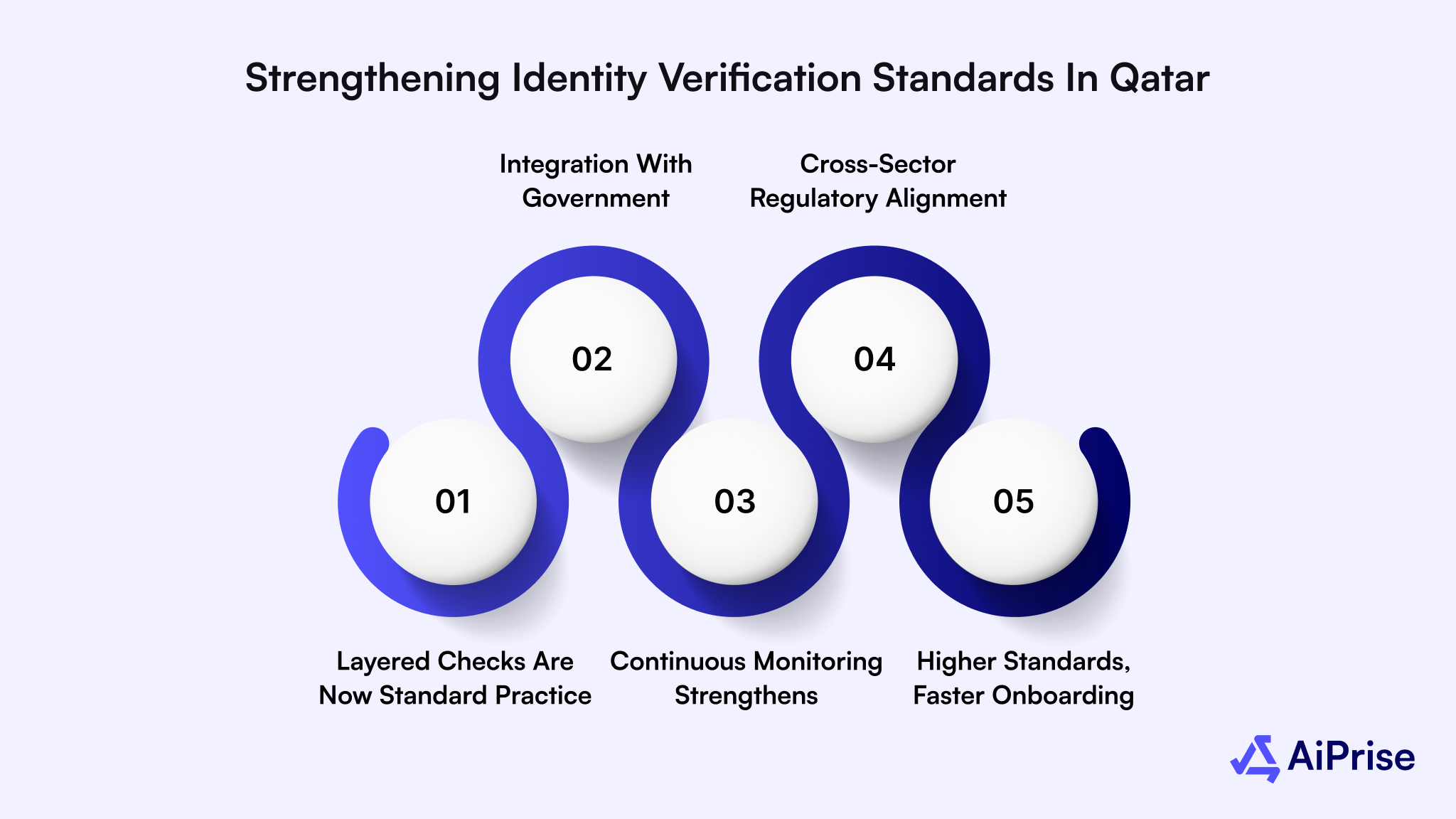

Strengthening Identity Verification Standards in Qatar

Strengthening identity verification standards in Qatar ensures that every transaction, customer, and business relationship meets the nation’s tighter AML/CFT Law No. 20 of 2019 requirements while protecting your institution from compliance gaps and reputational risk.

Here’s how the country’s approach is evolving and what you need to align with:

1. Multi-Layer Verification Is Now the Norm

Qatar’s updated AML framework encourages institutions to combine document, biometric, and behavioural verification to enhance accuracy. This multi-layer approach allows you to validate identities while instantly detecting fraudulent or mismatched data. Building such depth in verification helps your compliance function keep pace with regulators’ expectations and global standards.

2. Integration With Government and Global Databases

Cross-matching customer data with official government registries and international sanctions lists is now a regulatory expectation under the AML/CFT Law Qatar. By connecting your systems to these trusted databases, identity checks become faster, cleaner, and audit-ready. This integration also improves transparency and reduces the risk of onboarding high-risk or sanctioned clients.

3. Continuous Monitoring Strengthens Ongoing Compliance

Identity verification in Qatar no longer ends after onboarding; it extends through every transaction and customer lifecycle. Real-time monitoring allows you to flag unusual activity early and submit suspicious transaction reports within regulatory timelines. Embedding continuous oversight ensures compliance resilience and shields your operations from penalties.

4. Unified Regulatory Direction Across Sectors

QCB and QFCRA have aligned their verification standards to remove ambiguity between banking, fintech, and DNFBP sectors. This unified guidance helps you maintain consistent verification policies without conflicting interpretations during audits. Following these harmonised rules improves regulatory confidence and reduces procedural friction.

5. Higher Standards Deliver Faster, Safer Onboarding

Adopting rigorous verification standards accelerates onboarding by automating checks and reducing manual reviews. With fewer delays and accurate validations, customers experience smoother entry while your institution ensures full compliance. This balance between efficiency and control positions your business as a secure, trusted player in Qatar’s financial ecosystem.

Also read: Optimizing KYC Verification with Blockchain Technology

These elevated standards go hand in hand with technology, and that’s exactly where e-KYC becomes the new compliance backbone.

e-KYC and Technology Expectations

The shift to e-KYC in Qatar sets a new benchmark, so you must meet modern digital verification standards to remain compliant and competitive.

Here are the requirements and technology expectations:

- The QCB’s e-KYC Regulation mandates prior approval for remote onboarding, document scanning, biometric checks, and secure infrastructure before deploying digital verification.

- Multifactor authentication, NFC or OCR-enabled identity capture, liveness detection, and consent-based data collection in both Arabic and English are expected as part of verification tools.

- Continuous screening of clients against international sanctions/PEP lists, real-time monitoring, and audit trails that integrate into your broader AML programme and risk-management system.

Even with strong tech, ignoring enforcement can undo everything, so it’s worth knowing what non-compliance actually costs in Qatar.

Penalties and Enforcement: What Non-Compliance Looks Like

Failing to meet AML and KYC obligations in Qatar exposes you to substantial penalties, regulatory action, and reputational damage.

Here are the key risk outcomes you must guard against:

- Fines for legal entities can reach up to QAR 100 million under Law No. 20 of 2019, with additional daily fines or individual manager sanctions for non-compliance.

- Regulatory authorities may suspend licences, impose corrective orders, enforce management changes, or refer criminal action where money-laundering or terrorism-financing is proven.

- Serious reputational consequences for you include loss of business partnerships, exclusion from correspondent banking networks, and increased scrutiny by regulators and auditors.

Also read: Understanding Identity Management in KYC Processes

These consequences underline why Qatar’s AML reforms matter regionally, and how they compare with other Gulf jurisdictions tackling similar challenges.

Regional AML Depth for Qatar

Exploring how Qatar’s AML framework stacks up regionally offers you a perspective and highlights areas for improvement. Here’s how Qatar compares with selected neighbouring jurisdictions:

Regional context aside, institutions in Qatar still need tools that make compliance faster, safer, and more dependable, which is where AiPrise steps in.

AiPrise for Qatar: Secure Onboarding

AiPrise helps banks, payment platforms, marketplaces, and crypto firms in Qatar verify sellers and customers to meet AML Qatar requirements and Law No. 20 of 2019 while reducing onboarding friction.

Here are the Qatar-specific features and capabilities to strengthen your verification program:

- Local ID support for Qatari National ID, residence permits, and ICAO-compliant passports to ensure KYC checks meet regulator expectations.

- KYB workflows that validate Commercial Registration (CR) documents, incorporation certificates, and beneficial-owner data against global and local registries.

- Cross-reference checks with sanctions, PEP, and adverse-media lists to align with QFIU screening and FATF-driven expectations.

- One integration to multiple local vendors and fallback providers, improving verification reliability across Qatar’s regulatory landscape.

- Customizable onboarding flows (drag-and-drop, branded forms, save-and-resume) that cut drop-offs while keeping documentation audit-ready for QCB or QFCRA reviews.

- Risk-based decisioning with configurable rules to trigger EDD for PEPs, high-value flows, or clients from higher-risk jurisdictions.

- Continuous monitoring and automated alerts for changes in company status, ownership, or suspicious transaction patterns relevant to Qatar’s oversight.

- Government registry matching, where available, improves confidence in identity and business verifications for local compliance.

- Multi-point document verification (MRZ, barcodes, OCR cross-checks) combined with liveness and 1:N face match to deter spoofing and deepfakes.

- Dynamic risk scoring and backtestable models that let compliance teams tune thresholds to Qatar-specific risk appetite.

- Case management dashboard consolidating vendor results, audit trails, and investigator notes for faster suspicious transaction reporting to QFIU.

- Phone, email, and device intelligence to detect synthetic identities and reduce fraud exposure during remote onboarding.

- Geo-optimised KYC/KYB that respects local ID types, languages (Arabic/English,) and regional data privacy considerations.

- Fast UBO verification and structured EDD report generation to speed regulatory audits and reduce manual review time.

Wrapping Up

Qatar’s tightening AML and KYC regulations mark a clear shift toward stronger financial accountability, making reliable identity verification no longer optional but essential. Strengthening compliance processes now helps your institution avoid penalties, accelerate onboarding, and build trust in a closely monitored financial landscape.

AiPrise simplifies this transformation for Qatar-based businesses with advanced KYC, KYB, and AML solutions that automate checks, prevent fraud, and ensure full regulatory alignment. With one integration, you can future-proof onboarding, maintain continuous compliance, and confidently scale your operations across Qatar and beyond.

Book A Demo today to simplify compliance, prevent fraud, and strengthen KYC and AML verification in Qatar.

FAQ

1. What is Law No. 20 of 2019 on Combating Money Laundering and Terrorism Financing in Qatar?

It’s the primary AML/CFT law in Qatar that requires businesses and financial institutions to adopt a risk-based approach, conduct customer due diligence, and report suspicious transactions.

2. What documents are required for KYC in Qatar?

Individuals must provide a valid Qatari National ID or passport plus proof of address, while businesses must present a Commercial Registration certificate, beneficial-owner information, and official company documents.

3. Is Qatar considered a high-risk or grey-listed country for AML?

While Qatar has made substantive improvements in AML/CFT compliance, it remains under increased monitoring by the Financial Action Task Force (FATF) for further enhancements.

4. What are the penalties for money laundering non-compliance in Qatar?

Penalties under Qatar’s AML framework include substantial fines (which may reach up to QAR 100 million or more for entities) and possible criminal sanctions for serious violations.

5. Who must comply with KYC/AML requirements in Qatar?

All banks, finance companies, payment providers, virtual-asset service providers (VASPs), and designated non-financial businesses and professions (DNFBPs) operating in Qatar must comply with AML/KYC standards.

You might want to read these...

.jpeg)

.jpg)

.jpeg)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately