AiPrise

10 min read

January 8, 2026

10 KYC Onboarding Challenges and Best Practices to Fix Them

Key Takeaways

KYC onboarding sits at the intersection of growth, fraud prevention, and regulatory compliance. When it breaks down, the impact is immediate.

In 2024, Fenergo found that 67% of the organizations lost customers due to slow and inefficient onboarding and KYC processes.

For financial institutions, payment providers, and crypto platforms, this challenge is becoming harder to manage. Regulatory expectations continue to rise. Fraud tactics evolve quickly. Global expansion introduces different document standards and review requirements.

At the same time, customers expect onboarding to be fast and seamless.

Many KYC onboarding challenges are not caused by regulation itself, but by how onboarding workflows are designed and executed.

This guide explores the most common challenges and how regulated businesses can fix them without losing speed or control.

At a glance:

- KYC onboarding is a core compliance control that establishes customer risk, monitoring requirements, and regulatory alignment, not just identity verification.

- Most onboarding issues come from poor workflow design, including manual reviews, low-quality data, fragmented tools, and inconsistent risk decisions.

- Applying uniform checks to all users increases friction and misses risk. Risk-based onboarding is essential to balance speed, accuracy, and compliance.

- One-time checks, weak documentation, and unclear escalation paths create audit risk and leave teams exposed as customer behavior changes.

- Strong KYC programs focus on data quality at entry, clear risk rules, combined identity and fraud signals, defined escalation, and continuous monitoring.

- Platforms like AiPrise streamline KYC by unifying verification, fraud detection, risk-based step-ups, and audit-ready case management.

What Is KYC Onboarding?

KYC onboarding is the process of verifying a customer’s identity and assessing their risk before establishing a business relationship. In regulated environments, it serves as the foundation for meeting legal, regulatory, and internal risk requirements.

Beyond confirming who a customer is, KYC onboarding plays a broader role within compliance programs:

- Supports AML obligations by helping identify and assess potential financial crime risk at entry

- Reduces fraud by detecting identity misuse, impersonation, and synthetic identities early

- Establishes regulatory compliance by ensuring onboarding decisions align with jurisdiction-specific requirements

KYC onboarding is more than identity verification alone. It includes risk assessment, screening, documentation, and decisioning that determine how a customer is monitored over time.

When treated as a one-time check, gaps emerge. When designed as a structured control, KYC onboarding strengthens both compliance outcomes and operational efficiency.

Also read: What is KYC? A Simple Guide for Beginners

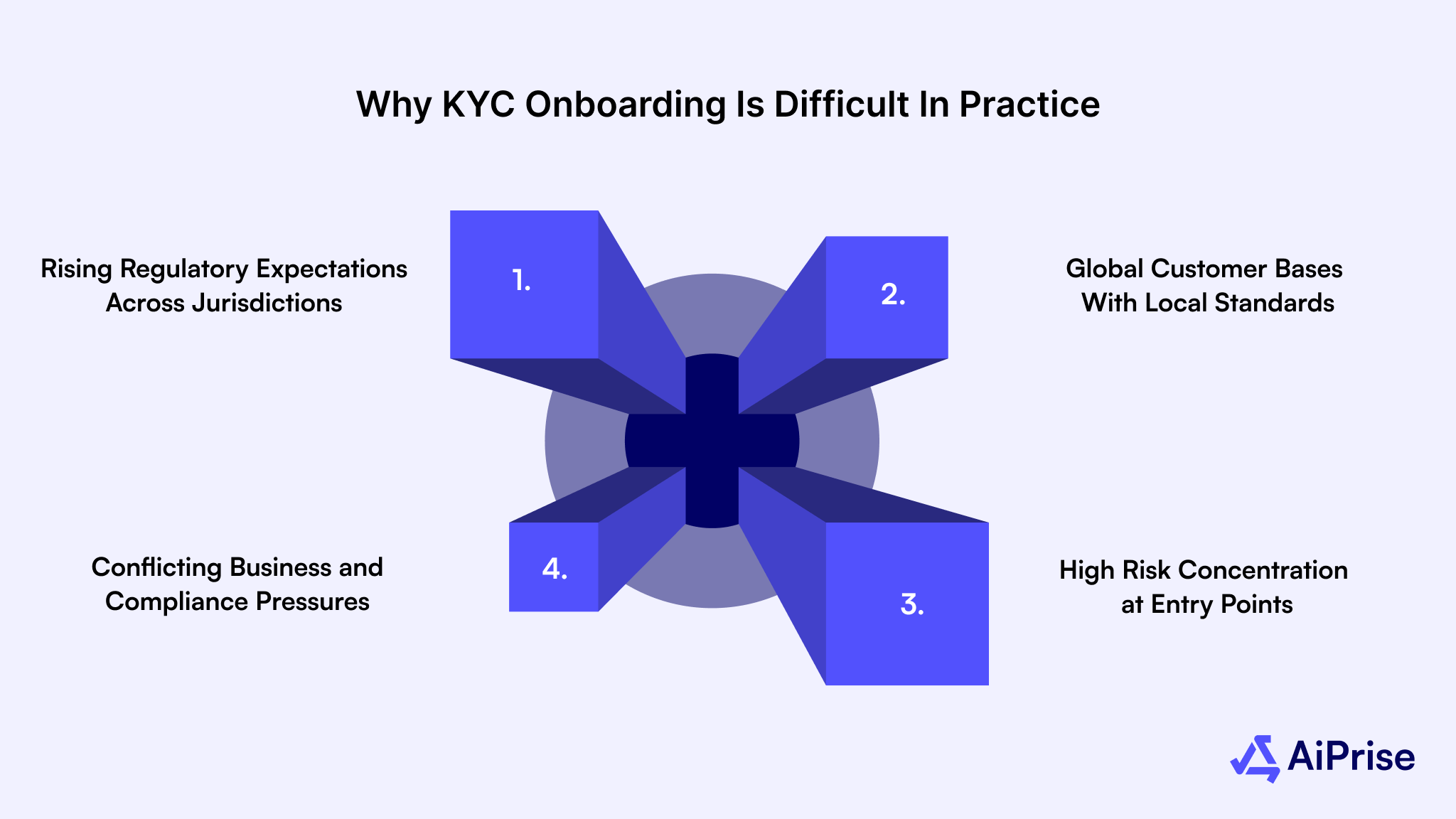

Why KYC Onboarding Is Difficult in Practice

KYC onboarding is not difficult because teams lack effort. It is difficult because regulated onboarding operates under competing constraints that are hard to balance at scale.

Several structural factors contribute to this complexity:

Rising Regulatory Expectations Across Jurisdictions

KYC requirements continue to expand, with local interpretations that vary by country. Businesses must meet jurisdiction-specific rules while maintaining consistent internal controls.

Global Customer Bases With Local Standards

Identity documents, address formats, and verification methods differ widely across regions, making it hard to apply a single onboarding model without adjustment.

High Risk Concentration at Entry Points

Onboarding is the primary point where identity misuse, impersonation, and account abuse occur, increasing scrutiny and review intensity.

Conflicting Business and Compliance Pressures

Growth teams push for faster onboarding to reduce abandonment, while compliance teams must apply thorough checks to manage regulatory and fraud risk.

These structural pressures explain why KYC onboarding remains one of the most complex areas of compliance, even for well-resourced organizations.

AiPrise helps regulated businesses manage these competing demands by bringing document verification, fraud detection, AML screening, and case management into a single KYC onboarding platform. This allows teams to apply risk-based checks consistently across regions while maintaining speed, accuracy, and audit readiness as they scale.

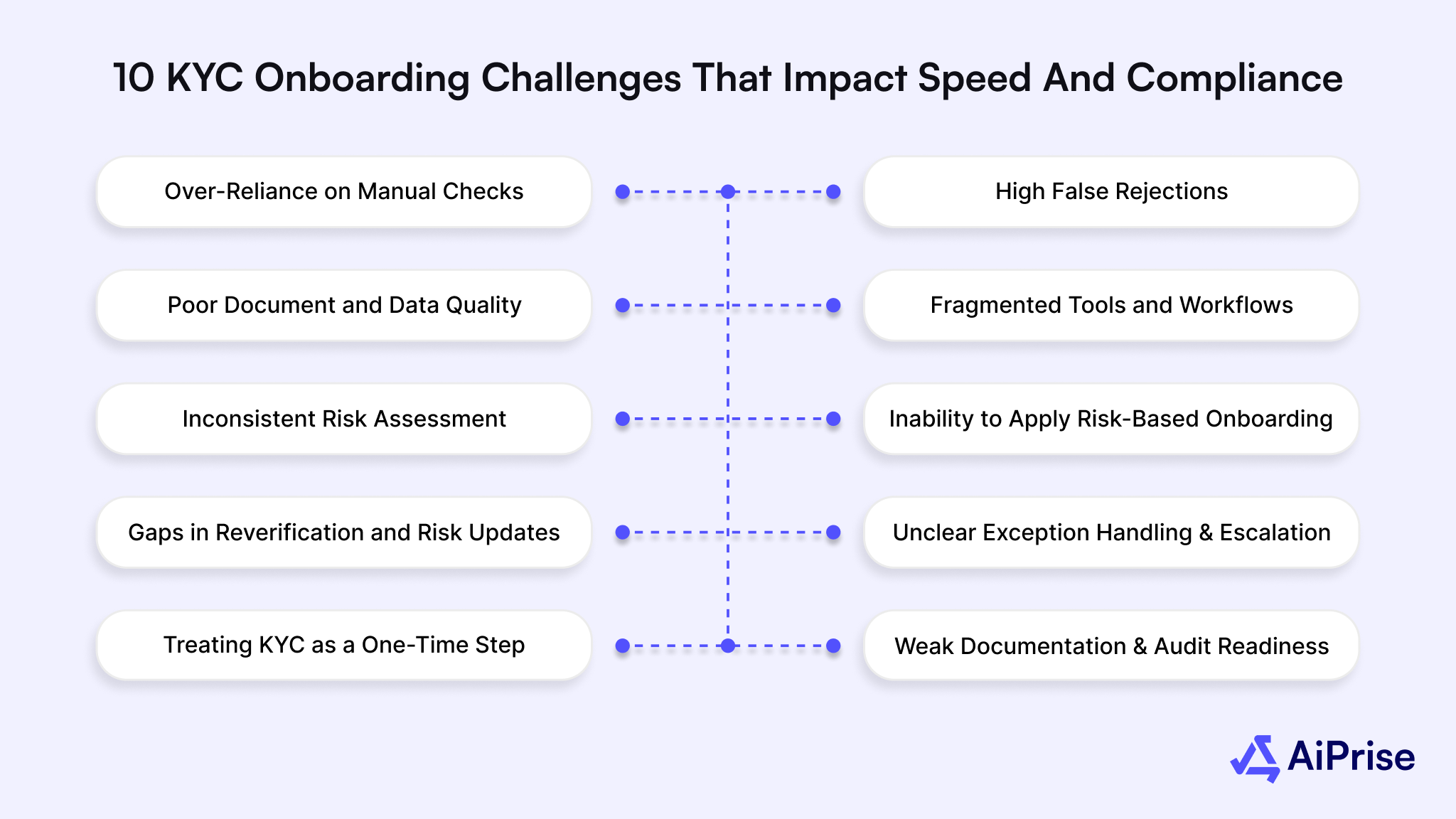

10 KYC Onboarding Challenges That Impact Speed and Compliance

Most KYC onboarding problems are not caused by regulation itself. They are caused by how onboarding workflows are designed, implemented, and scaled. Below are the most common challenges regulated businesses face, along with why they persist.

Over-Reliance on Manual Checks

Manual document review and subjective decisions dominate onboarding, creating delays, inconsistencies, and reviewer-dependent outcomes as volumes grow.

Why it persists:

- Manual reviews feel safer in the early stages

- Automation is introduced without clear risk rules

- Review volumes grow faster than team capacity

Impact:

- Longer onboarding times

- Higher error rates and inconsistent decisions

- Backlogs that delay legitimate customers

High False Rejections and Unnecessary Friction

Legitimate users fail onboarding due to rigid rules, minor data mismatches, and limited tolerance for regional document variations.

Common triggers:

- Poor image quality or lighting

- Formatting differences in names or addresses

- Region-specific document variations

Impact:

- Increased drop-offs and customer frustration

- Higher support and re-verification workload

- Lost revenue from abandoned onboarding

Poor Document and Data Quality

Incomplete forms, low-quality uploads, and inconsistent data capture reduce verification accuracy and increase downstream review effort.

Root causes:

- Unstructured forms and optional fields

- No upfront data validation

- Limited guidance for document uploads

Impact:

- Slower verification and more manual reviews

- Lower confidence in onboarding decisions

- Errors that carry into downstream monitoring

Fragmented Tools and Workflows

KYC, fraud, screening, and case management operate in separate systems, forcing manual reconciliation and limiting holistic risk visibility.

Operational consequences:

- Teams switch between tools to complete a single review

- Information is duplicated or manually reconciled

- Risk signals are reviewed in isolation

Impact:

- Missed connections and weak oversight

- Incomplete audit trails

- Higher operational complexity

Inconsistent Risk Assessment

Similar customers receive different outcomes due to unclear risk criteria, reviewer discretion, and uneven application across teams.

Why it happens:

- No standardized risk criteria

- Reviewer judgment varies with workload and experience

- Local teams apply different thresholds

Impact:

- Regulatory exposure during audits

- Difficulty defending onboarding decisions

- Loss of trust in internal controls

Inability to Apply Risk-Based Onboarding

Uniform checks are applied to all users, causing unnecessary friction for low-risk customers and insufficient scrutiny for higher-risk profiles.

Typical signs:

- Over-collection of documents for low-risk users

- Delayed escalation for higher-risk profiles

- No clear link between risk score and required checks

Impact:

- Unnecessary friction for legitimate users

- Inadequate scrutiny where it matters most

- Inefficient use of compliance resources

Gaps in Reverification and Risk Updates

Customer risk profiles are not reassessed after onboarding, leaving changes in behavior, location, or exposure unreviewed.

Missed triggers include:

- Changes in address or geography

- New products or transaction behavior

- Updated risk signals or regulatory requirements

Impact:

- Reliance on outdated customer data

- Increased exposure to emerging risk

- Weak alignment with ongoing AML expectations

Unclear Exception Handling and Escalation

Edge cases stall when escalation paths are undefined, increasing review time and creating inconsistent decision outcomes.

Common breakdowns:

- No defined escalation criteria

- Excessive back-and-forth between teams

- Reviews paused waiting for decisions

Impact:

- Longer onboarding timelines

- Inconsistent outcomes for similar cases

- Higher operational load on senior reviewers

Treating KYC as a One-Time Step

Onboarding approval is treated as final, with limited monitoring of customer risk as relationships and activity evolve.

Why this is risky:

- Customer behavior and risk profiles change

- New fraud patterns emerge post-onboarding

- Regulatory expectations extend beyond entry checks

Impact:

- Missed risk signals after approval

- Gaps in ongoing compliance coverage

- Increased scrutiny during regulatory reviews

Weak Documentation and Audit Readiness

Decisions lack a clear rationale and centralized records, making it difficult to defend onboarding outcomes during audits.

Typical issues:

- Missing rationale for approvals or rejections

- Incomplete logs across systems

- Difficulty reconstructing decisions months later

Impact:

- Challenges during audits and examinations

- Increased regulatory risk

- Loss of confidence in compliance processes

These challenges often reinforce each other. Manual reviews worsen delays. Poor data increases false rejections. Fragmented systems weaken oversight. Addressing KYC onboarding challenges requires fixing these root causes rather than adding more checks on top of broken workflows.

Also read: Top 10 KYC Failure Reasons and Their Solutions for 2025-26

How to Fix Common KYC Onboarding Issues

Effective KYC onboarding is not about adding more checks. It’s about designing workflows that apply the right level of scrutiny at the right time, consistently and at scale.

High-performing compliance teams focus on the following practices:

Design Risk-Based Onboarding Flows

Apply different onboarding paths based on customer risk instead of forcing every user through the same checks. This allows low-risk customers to move quickly while ensuring higher-risk profiles receive appropriate scrutiny.

What to do:

- Define low-, medium-, and high-risk customer categories

- Map required checks and documents to each risk tier

- Allow low-risk users to complete streamlined onboarding without unnecessary reviews

Enforce Data Quality at Entry

Ensure identity data and documents are complete and readable at submission. Strong data quality upfront reduces false rejections, manual reviews, and downstream rework.

What to do:

- Require mandatory identity fields and clear document uploads

- Add basic validation checks for completeness and readability

- Reject incomplete submissions early instead of pushing them to manual review

Define Clear Risk and Decision Rules

Establish consistent risk thresholds and escalation criteria so similar customers receive the same outcomes. Clear rules reduce reviewer subjectivity and audit risk.

What to do:

- Document risk thresholds and escalation criteria

- Standardize approval and rejection guidelines across teams

- Ensure reviewers follow the same decision logic regardless of region or workload

Combine Identity and Risk Signals

Assess identity verification alongside fraud and behavioral indicators rather than in isolation. This helps surface higher-risk profiles that basic checks may miss.

What to do:

- Review identity verification alongside fraud and behavioral indicators

- Cross-check inconsistencies before approving accounts

- Use combined signals to prioritize deeper review where needed

Establish Explicit Escalation Paths

Define clear ownership and timelines for edge cases. Structured escalation prevents reviews from stalling and keeps decisions consistent.

What to do:

- Define when a case must be escalated and to whom

- Set review timelines for escalated cases

- Limit back-and-forth by assigning clear ownership at each stage

Treat KYC as a Continuous Control

Move beyond one-time onboarding checks by reassessing risk over time. Ongoing reviews help catch changes in behavior, location, or exposure.

What to do:

- Set triggers for re-verification based on risk, behavior, or profile changes

- Schedule periodic reviews for higher-risk customers

- Update risk assessments when customers expand usage or enter new regions

Centralize Documentation and Audit Evidence

Capture decisions, applied controls, and rationale in one place. Centralized records make onboarding decisions easier to review and defend.

What to do:

- Record approval or rejection rationale for every case

- Store documents, risk scores, and reviewer notes in one system

- Ensure records can be retrieved quickly during audits or reviews

When these actions are applied together, KYC onboarding becomes easier to operate, easier to scale, and easier to defend under regulatory scrutiny.

How AiPrise Helps Address KYC Onboarding Challenges

Fixing KYC onboarding challenges requires more than adding isolated checks. Teams need a unified way to verify identities, assess risk, manage reviews, and maintain compliance over time.

AiPrise brings these capabilities together in a single platform designed for regulated businesses operating at scale.

AiPrise supports KYC onboarding by enabling teams to:

Unify KYC Checks in One Platform

Bring document verification, face liveness, AML screening, address verification, and fraud detection into a single workflow. This reduces tool fragmentation and manual reconciliation during onboarding.

Verify Global Identities Reliably

Verify over 12,000 ID document types from 220+ countries, with multi-point crosschecks against MRZ, barcodes, and government databases to improve accuracy and reduce false rejections.

Apply Risk-Based and Step-Up KYC

Start with basic verification and step up requirements only when risk indicators demand deeper scrutiny. This supports faster onboarding for low-risk users while maintaining strong controls for higher-risk cases.

Detect Fraud Early in the Onboarding Journey

Use face liveness checks, 1:N face match, and deepfake detection to prevent spoofing, duplicate accounts, and fraudulent onboarding attempts.

Maintain Continuous KYC and Reverification

Monitor document expirations, trigger reverification when risk signals change, and support ongoing KYC without restarting the entire onboarding process.

Centralize Case Management and Audit Trails

Manage escalations, track decisions, and maintain clear records through integrated case management, supporting audit readiness and regulatory reviews.

With this unified approach, AiPrise helps teams run KYC onboarding with greater consistency, control, and audit readiness.

Wrapping Up

KYC onboarding remains one of the most operationally demanding areas of compliance for regulated businesses. When workflows are poorly designed, the consequences surface quickly through delays, higher drop-offs, inconsistent risk decisions, and increased regulatory exposure. As regulatory expectations grow and fraud pressure intensifies, manual processes and fragmented systems struggle to keep up.

Effective KYC onboarding relies on risk-based design, strong data quality, clear decision rules, and continuous monitoring rather than one-time checks. These foundations help teams reduce friction without weakening controls and maintain audit-ready processes as they scale.

With this unified approach, AiPrise helps teams run KYC onboarding with greater consistency, control, and audit readiness. Book A Demo to see how AiPrise supports compliant onboarding at scale.

FAQs

Q. What is the onboarding process in KYC?

The KYC onboarding process involves verifying a customer’s identity, assessing their risk, and confirming eligibility before establishing a business relationship. It typically includes identity verification, document checks, watchlist screening, and an initial risk assessment to meet regulatory requirements.

Q. What are KYC issues?

KYC issues refer to problems that arise during onboarding, such as slow reviews, false rejections, poor data quality, inconsistent risk decisions, or weak documentation. These issues can lead to customer drop-offs, operational inefficiencies, and increased regulatory risk.

Q. What challenges do banks face in customer onboarding?

Banks often struggle with balancing speed and compliance, managing high volumes of manual reviews, handling global document variations, detecting fraud at onboarding, and maintaining consistent, audit-ready records across teams and regions.

Q. What are the 5 stages of KYC?

The five common stages of KYC include customer identification, identity verification, risk assessment, due diligence based on risk level, and ongoing monitoring to keep customer profiles up to date over time.

You might want to read these...

.jpeg)

.jpg)

.jpeg)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately