AiPrise

10 min read

November 28, 2025

Blockchain and KYC Solutions in the Insurance Industry

Key Takeaways

In the insurance industry, outdated Know Your Customer (KYC) processes can expose firms to significant risks. In 2024, the U.S. Department of Justice charged 193 defendants, including 76 licensed medical professionals, with healthcare fraud schemes resulting in over $2.75 billion in false claims. This highlights the pressing need for insurers to adopt more secure and efficient verification methods. Implementing blockchain KYC insurance solutions can address these challenges by providing tamper-proof records, faster identity verification, and automated compliance.

Key Takeaways

- Traditional KYC challenges in insurance are slow, error-prone, and costly due to manual checks, data silos, and evolving regulations.

- Blockchain improves KYC by ensuring secure, tamper-proof customer data with decentralized identity management and faster, automated verification.

- Blockchain benefits include reduced fraud, faster onboarding, better data security, and streamlined regulatory compliance, lowering operational costs.

- Use cases for blockchain in insurance include automating claims, enhancing policy administration, and securing KYC processes, driving transparency and efficiency.

Why KYC in Insurance Remains a Challenge?

In the insurance industry, Know Your Customer (KYC) processes are crucial for both compliance and managing risk effectively. Yet, many insurers struggle with traditional KYC methods, which can slow down operations and leave gaps in security. Here are the main challenges you’re likely to face when handling KYC in insurance:

- Manual Processes: If you’re still relying on manual data entry and document checks, you’re likely facing human errors, duplicated work, and delays that frustrate both staff and customers.

- Data Silos: When customer information is scattered across multiple systems or departments, it becomes difficult for you to get a complete view of their identity and risk profile.

- Regulatory Compliance: Keeping up with constantly evolving regulations can be overwhelming, and failure to comply could result in hefty fines or operational restrictions.

- Fraud Risk: Outdated KYC procedures increase your exposure to identity theft, duplicate claims, and other fraudulent activities that can significantly impact your bottom line.

- Customer Experience: Lengthy or repetitive verification processes make onboarding tedious for your customers, risking abandonment or negative brand perception.

Next, we’ll examine how blockchain can make a real difference in addressing these hurdles.

Also read: How to Avoid and Detect KYC Fraud

What Are the Benefits of Blockchain in Insurance?

Blockchain technology brings multiple benefits to insurers, transforming operations, compliance, and customer experience. Here are the key advantages you can leverage by implementing blockchain in your insurance business:

- Enhanced Security: Blockchain’s decentralized and encrypted ledger protects sensitive customer data from hacks and fraud, giving you confidence that information is secure.

- Operational Efficiency: Automated smart contracts streamline claims processing, policy issuance, and KYC checks, reducing manual effort and operational costs.

- Fraud Prevention: Immutable records and real-time verification significantly reduce fraudulent claims, duplicate applications, and identity theft.

- Improved Customer Experience: Faster onboarding, real-time claim settlements, and transparent policy tracking create a smoother, more reliable experience for your clients.

- Regulatory Compliance: Blockchain’s auditable and tamper-proof ledger makes it easier for you to comply with AML regulations, KYC standards, and other insurance-specific laws.

- Cost Savings: By reducing paperwork, manual verification, and claim disputes, blockchain lowers administrative costs and increases profitability.

These benefits show that blockchain is not just a technological upgrade; it’s a strategic investment that can help you stay competitive, compliant, and customer-focused. Let’s now take a look at specific areas where blockchain can truly transform how insurance companies operate.

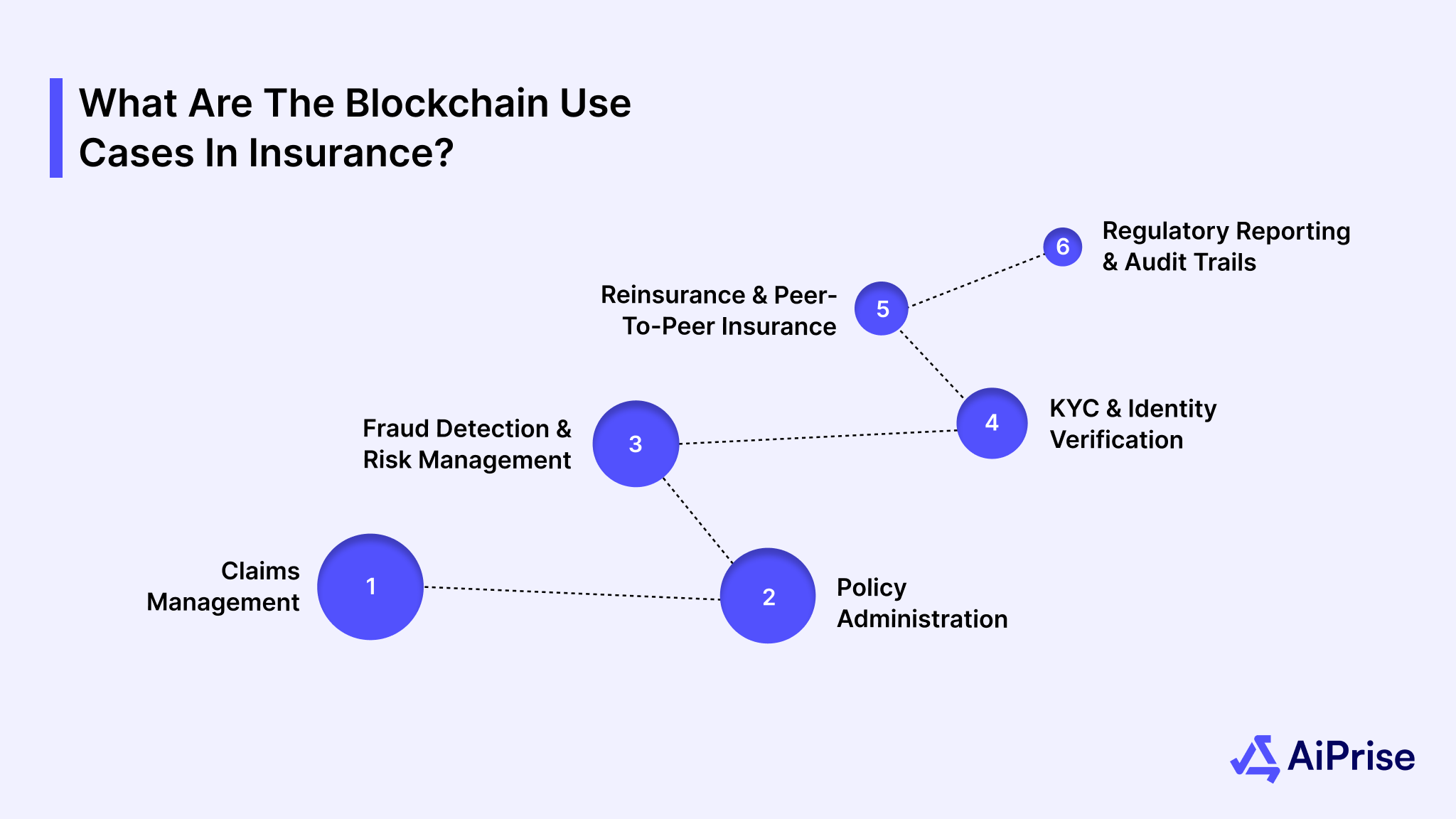

What Are the Blockchain Use Cases in Insurance?

Blockchain is no longer theoretical in insurance; it has real, actionable applications across multiple operations. Here are the most impactful use cases where you can implement blockchain today:

- Claims Management: Automate claims verification and settlement with smart contracts, reducing processing time from weeks to hours.

- Policy Administration: Streamline policy issuance, renewal, and updates on a secure blockchain platform, minimizing errors and enhancing transparency.

- Fraud Detection and Risk Management: Track and analyze customer behavior and claim history across a tamper-proof ledger to detect suspicious activity.

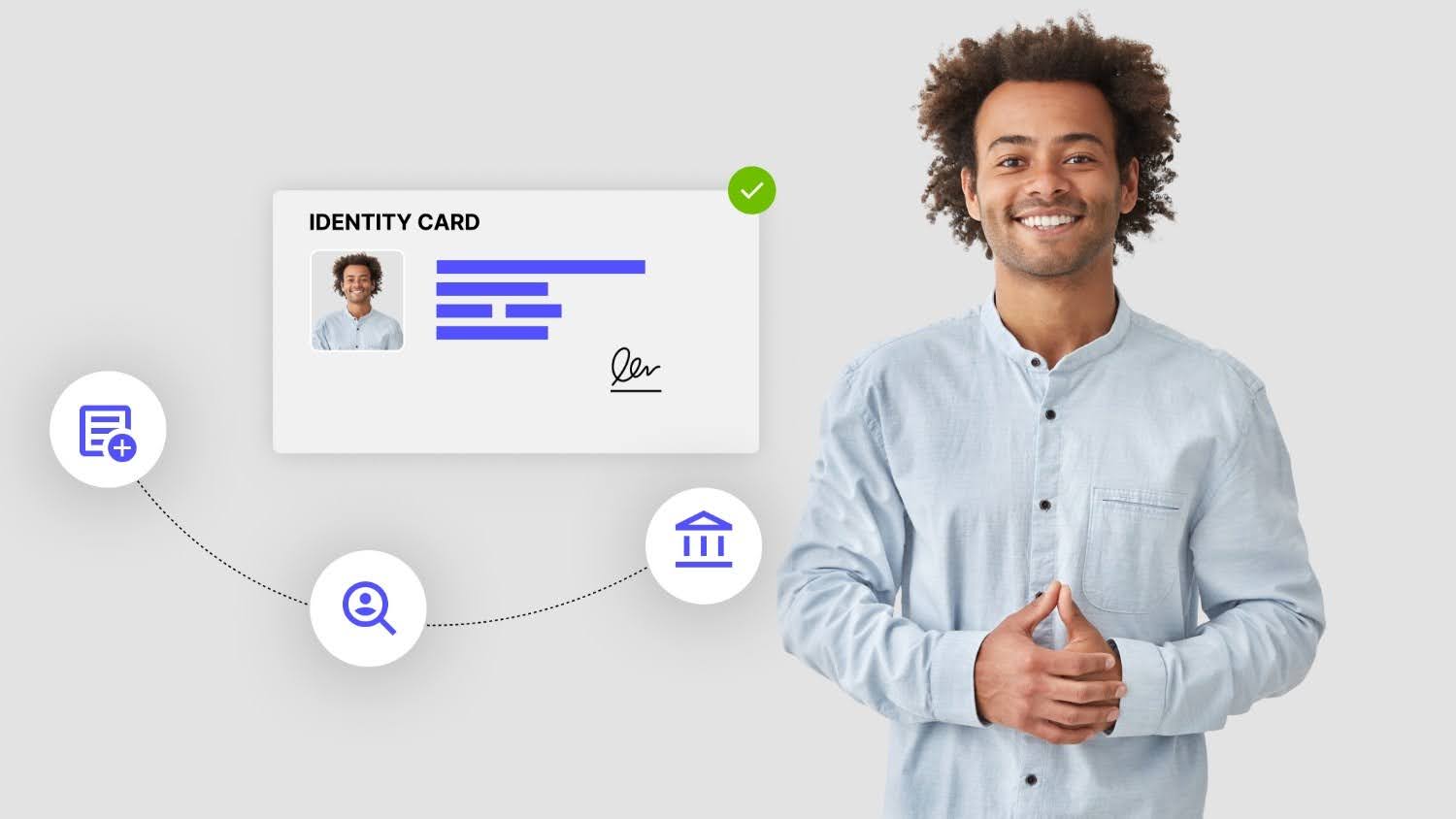

- KYC & Identity Verification: Use blockchain for faster, more secure verification of individual and business identities, reducing onboarding delays.

- Reinsurance & Peer-to-Peer Insurance: Share risk information securely with reinsurers or blockchain-enabled peer networks, improving trust and efficiency.

- Regulatory Reporting & Audit Trails: Automatically generate auditable reports for compliance purposes, ensuring regulators can verify your processes in real-time.

Next, we’ll take a deeper look at how blockchain specifically reshapes KYC processes in insurance.

Also read: 3 Essential Components of KYC

How Blockchain Reinvents KYC for Insurance?

Blockchain technology is transforming KYC processes in the insurance industry by offering security, transparency, and operational efficiency. Here are the key ways blockchain can solve traditional KYC challenges for your insurance business:

- Decentralized Identity Management: With blockchain, you can enable self-sovereign identities, giving customers control over their data while ensuring verified information. This reduces the need for repetitive document checks and makes onboarding faster and more secure.

- Immutable Records: Blockchain ensures that once identity data is recorded, it cannot be altered or tampered with, helping you maintain data integrity and build trust with regulators.

- Enhanced Security: Cryptographic encryption techniques protect sensitive customer data against breaches and unauthorized access, significantly lowering your exposure to fraud.

- Streamlined Processes: Smart contracts automate verification workflows, cutting KYC processing time from days to hours and reducing manual errors.

- Regulatory Compliance: Blockchain’s transparent and auditable ledger makes it easier for you to meet AML compliance and other regulatory standards without maintaining cumbersome paper trails.

But what does a blockchain-powered KYC system actually look like in practice? Let’s walk through its core components.

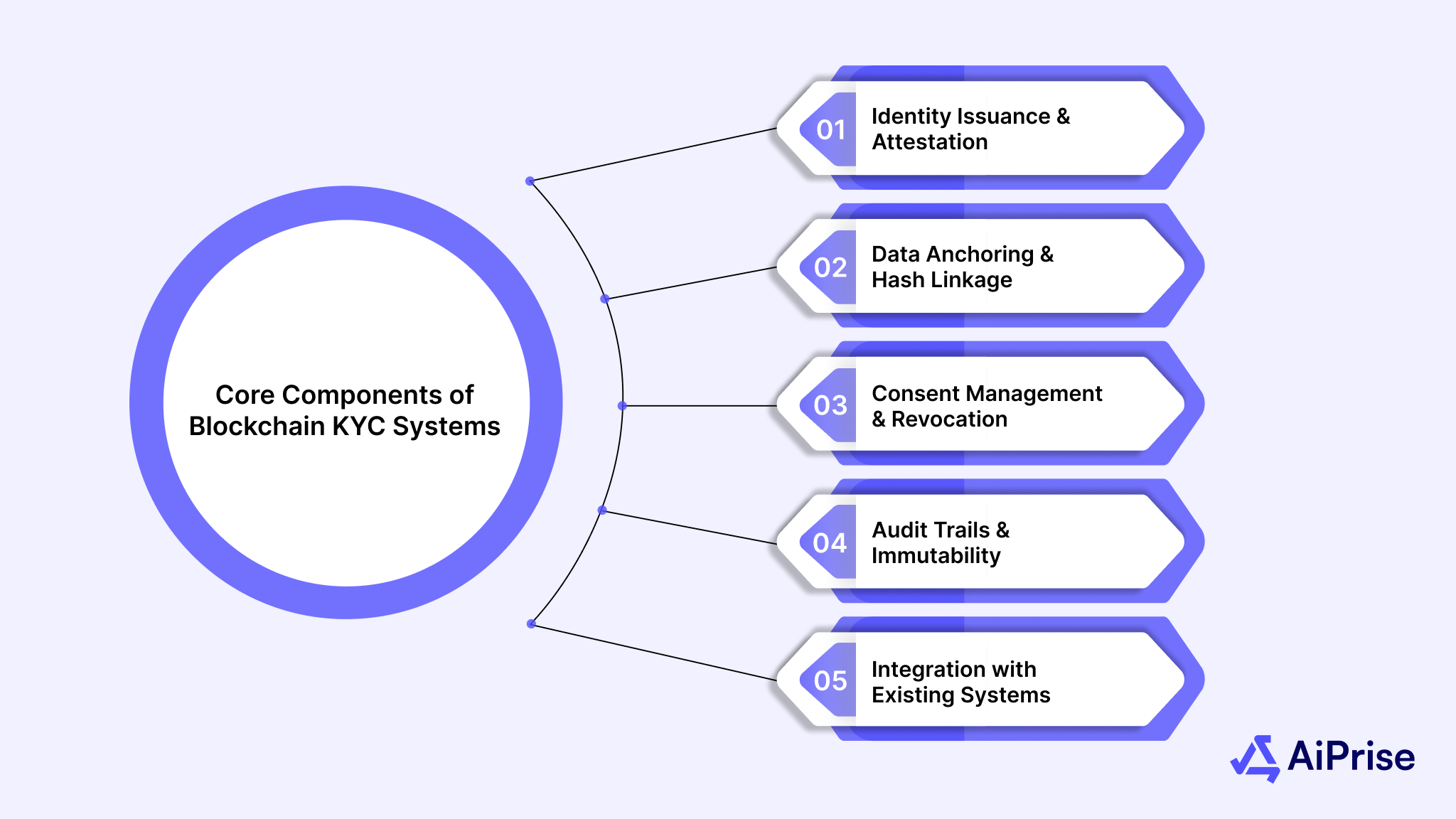

Core Components of Blockchain KYC Systems

Blockchain KYC systems rely on several critical components that ensure efficiency, security, and compliance. Here are the essential elements you need to understand to implement blockchain KYC effectively:

1. Identity Issuance & Attestation

Trusted authorities verify and issue digital identities, ensuring authenticity. Each identity is validated using government-issued IDs or biometric data, then recorded on the blockchain. This reduces the risk of fake accounts and streamlines verification for both you and your customers.

2. Data Anchoring & Hash Linkage

Customer data is hashed and anchored to the blockchain, ensuring integrity without exposing sensitive information. Hashing transforms data into unique digital fingerprints, allowing verification without compromising privacy. This approach safeguards your customer information while enabling seamless audits.

3. Consent Management & Revocation

Blockchain allows customers to control who accesses their data and under what conditions through smart contracts. You can track and enforce consent permissions automatically, giving your clients confidence that their personal data is used responsibly.

4. Audit Trails & Immutability

Every action within the KYC process is permanently recorded on the blockchain, creating an immutable and transparent audit trail. This helps you quickly verify compliance and reduces the risk of disputes or regulatory penalties.

5. Integration with Existing Systems

Blockchain KYC solutions can be integrated with traditional identity verification systems, allowing you to adopt new technology without overhauling your existing processes. This ensures a smooth transition and reduces operational friction.

With that in mind, let’s look at the specific documentation needed to perform KYC in insurance, so you can ensure you're meeting regulatory requirements.

Also read: Understanding KYC to Prevent Identity Theft

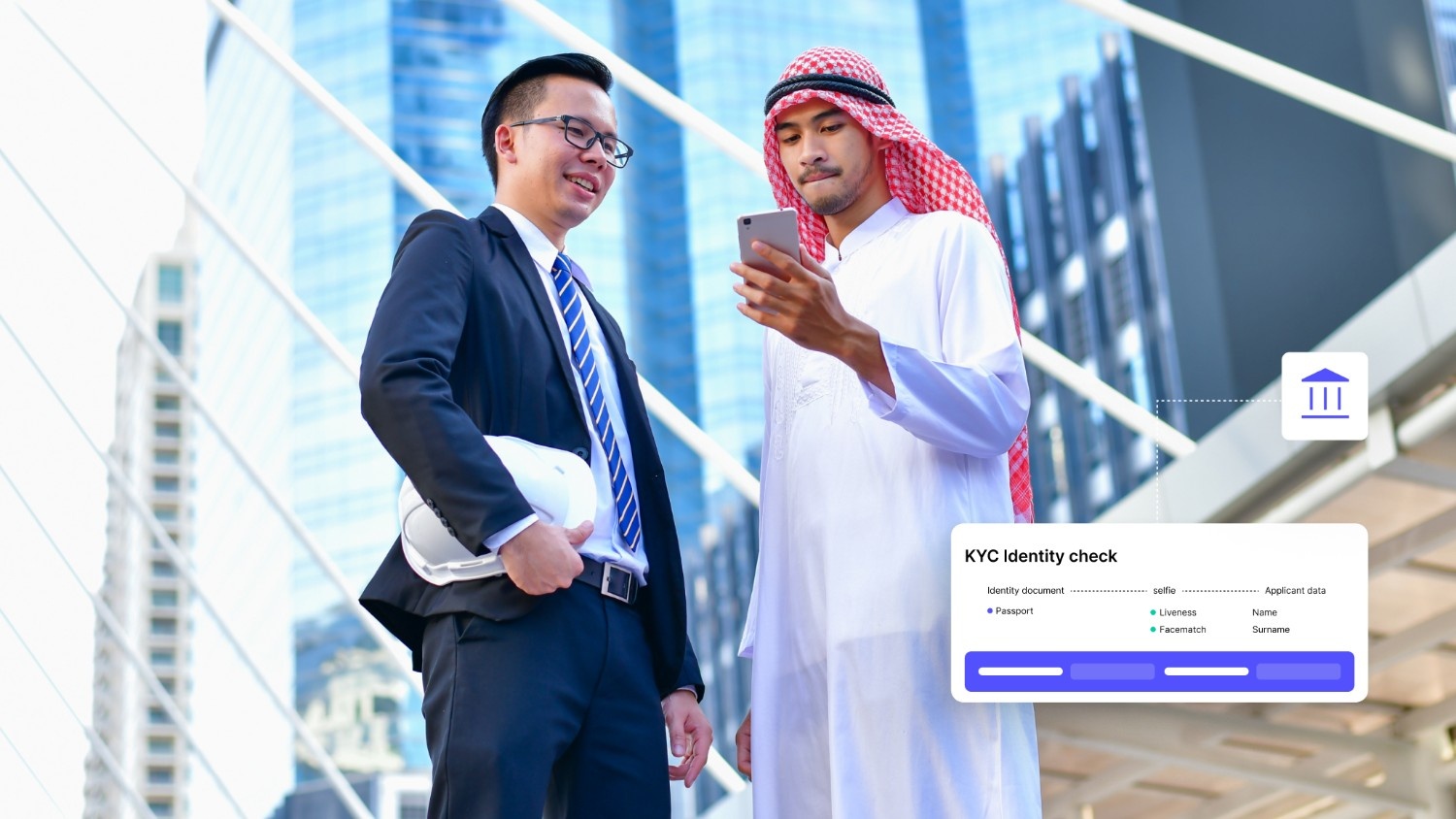

IDs & Identity Documents Required for KYC in Insurance

Verifying identities in insurance requires specific documents to comply with regulations and prevent fraud, especially when adopting blockchain KYC insurance solutions. Here are the types of IDs and documents you’ll typically need for KYC verification:

- Government-Issued ID: Passport, driver’s license, or national ID to confirm identity.

- Proof of Address: Utility bills, bank statements, or lease agreements to verify residency.

- Biometric Data: Fingerprint scans, facial recognition, or voice authentication to confirm identity in real time.

- Tax Identification Number (TIN): Necessary for AML compliance and tax reporting purposes.

- Corporate Documents: For business clients, articles of incorporation, partnership agreements, or company registration certificates.

Having these documents ensures that you meet regulatory requirements while reducing the risk of fraud. Once you’re familiar with the necessary paperwork, it’s helpful to compare how blockchain KYC stacks up against traditional KYC practices.

Traditional KYC vs Blockchain KYC in Insurance

To understand the real advantages of blockchain, compare traditional KYC methods with blockchain-based solutions:

This table shows why adopting blockchain KYC is essential for insurers aiming to reduce costs, improve security, and comply with regulations efficiently. Let’s discuss the challenges insurers must navigate when incorporating blockchain into their KYC systems.

Regulatory Considerations & Challenges

While blockchain offers strong advantages, it comes with regulatory considerations you must address. Here are the key challenges you need to keep in mind when implementing blockchain KYC:

- Data Privacy Laws: Ensure compliance with GDPR, CCPA, and local data protection regulations to protect your customers’ information.

- Jurisdictional Variations: Different countries have different rules for data storage, sharing, and digital identity recognition, which may complicate cross-border insurance operations.

- Standardization Issues: Lack of global standards for blockchain-based KYC can create interoperability challenges between insurers and third-party providers.

- Legal Recognition: Some jurisdictions may not yet recognize blockchain records as legally binding, which could affect dispute resolution or claims.

To manage these complexities, consider utilizing AiPrise's AI-powered KYC solutions. AiPrise offers a comprehensive platform that streamlines KYC and AML compliance while enhancing accuracy and speed.

AiPrise KYC and Risk Solutions for Blockchain-Based Insurance

When onboarding policyholders or corporate clients in blockchain-based insurance, ensuring identity and business verification is critical to prevent fraud and maintain compliance. Here are the key features of AiPrise that make KYC and risk management seamless for insurers:

- Document Verification: Quickly verify government-issued IDs, passports, and other critical documents to meet KYC standards. This reduces manual errors and accelerates policy issuance.

- KYB for Corporate Clients: Confirm ultimate beneficial owners and key stakeholders to prevent fraud and comply with AML regulations. Gain insights into complex ownership structures and hidden connections.

- Blockchain-Based Records: Record verification steps on tamper-proof blockchain ledgers, ensuring transparent and auditable trails for client onboarding and claims.

- Fraud and Risk Scoring: Assign dynamic risk scores using multiple data points, including identity details and online presence, to detect suspicious behavior early. Customize rules to match your insurance risk tolerance.

- Ongoing Monitoring: Continuously monitor clients and transactions, receiving real-time alerts for high-risk events, ownership changes, or document expirations. Stay proactive in compliance and fraud prevention.

- Global Coverage: Access verification services across 200+ countries, supporting local regulatory requirements while enabling smooth cross-border insurance operations.

Wrapping Up

The integration of blockchain KYC insurance solutions significantly enhances insurance operations, improving compliance, reducing fraud, and ensuring customer trust efficiently. By adopting these advanced verification methods, insurers can streamline onboarding, maintain regulatory standards, and minimize operational risks across multiple jurisdictions. Implementing blockchain KYC enhances security, transparency, and auditability in risk management.

AiPrise provides insurers with a powerful, AI-driven platform that simplifies KYC, KYB, and risk scoring while ensuring global compliance standards. With customizable workflows, continuous monitoring, and fast verification, AiPrise empowers insurers to focus on growth confidently.

Secure blockchain KYC onboarding with AiPrise. Book Your Demo to reduce fraud, ensure AML compliance, and simplify insurance verification.

FAQ

1. How is blockchain used in insurance?

Blockchain in insurance helps streamline claims processing, reduce fraud, and improve transparency. Securely storing data in immutable ledgers enables faster, more accurate verification of policyholder information and claims.

2. What is the blockchain in KYC?

Blockchain in KYC (Know Your Customer) is used to securely store and share verified customer data. It improves compliance, reduces fraud, and enables faster customer onboarding by providing a decentralized, tamper-proof system.

3. What is KYC insurance?

KYC insurance refers to the use of Know Your Customer (KYC) protocols in the insurance sector to prevent fraud, money laundering, and other financial crimes. It ensures insurance companies have accurate and verified customer information for regulatory compliance.

4. Is blockchain.com KYC?

Yes, blockchain.com, like most cryptocurrency platforms, implements KYC procedures to verify the identity of its users. This helps meet regulatory requirements and ensures the platform is used securely and legally.

5. Can I get my money back from Blockchain?

If you're referring to blockchain transactions, they are generally irreversible once confirmed. However, if you used a blockchain-based service like an exchange or wallet, the platform’s policies on refunds may apply, but it's crucial to verify all transaction details before sending funds.

You might want to read these...

.jpeg)

.jpg)

.jpeg)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately