AiPrise

10 min read

January 20, 2026

6 Best Practices for AML KYC Compliance at Scale in Fintech

Key Takeaways

Fintech teams are under pressure to onboard users faster while AML and KYC scrutiny keeps rising. Reviews pile up. Drop-offs increase. Compliance teams feel stretched. Growth slows. One question keeps coming up mid-process. How do you move fast without losing control?

As companies expand across borders, rules change, risk shifts, and static programs start to crack.

At scale means repeatable controls, audit-ready decisions, fewer false positives, and faster reviews. The best practices are clear. Use risk-based design. Layer KYC and KYB correctly. Monitor continuously. Reduce noise. Automate with oversight. Prove every decision.

The Best Practices That Actually Scale

- Treat AML and KYC as continuous controls across the customer lifecycle, not as one-time onboarding checks.

- Use risk-tiering to route review effort dynamically, allowing low-risk users to move fast and high-risk cases to deepen automatically.

- Structure KYC and KYB workflows in clear layers so every decision is consistent, defensible, and audit-ready.

- Reduce false positives through context-based alerting, using identity, behavior, and external signals before cases reach analysts.

- Apply automation and AI to repetitive tasks only, keeping human judgment central and every outcome clearly documented.

Knowing the best practices is one thing. Seeing where most programs break under real scale is another. This is where theory meets operational friction, and gaps start to show.

Why AML/KYC Programs Break As Fintechs Scale

You likely built your AML and KYC program to support early growth. It worked when volumes were low and reviews were manageable. As customer counts rise, transactions move faster, and cross-border exposure increases, those same controls start to fail. Bottlenecks form. Risk slips through. Audits get harder to defend.

The breakdown usually follows a clear pattern.

Where programs fail under scale

- Manual reviews don’t scale with volume: Review queues grow faster than headcount. Backlogs form. Decisions get rushed or delayed.

- Static rules miss changing risk: Fixed thresholds fail to react when customer behavior, geography, or product usage shifts.

- Fragmented tools create audit gaps: Identity checks, screening, and case notes live in different systems with no clean trail.

Traditional AML systems often generate false positive rates exceeding 95%, flooding your team with low-quality alerts and slowing real investigations.

Fragmented tools and noisy alerts make these failures harder to fix. AiPrise brings identity data, screening signals, and review logic into a single system, so risk decisions stay consistent as volume grows.

The US Baseline And How Verification Got Here

You are operating under expectations shaped largely by the US regulatory model. Identity verification started with in-branch document checks. It moved to online KYC as digital banking grew. Today, US regulators expect risk-based AML programs with continuous monitoring, not one-time checks.

Because US banks, payment rails, and partners set onboarding standards, their expectations influence global fintech compliance even outside the US.

What the US baseline emphasizes:

- Verifiable identity at onboarding.

- Risk-based customer segmentation.

- Ongoing monitoring and documented decisions.

- Clear audit trails for regulators and partners.

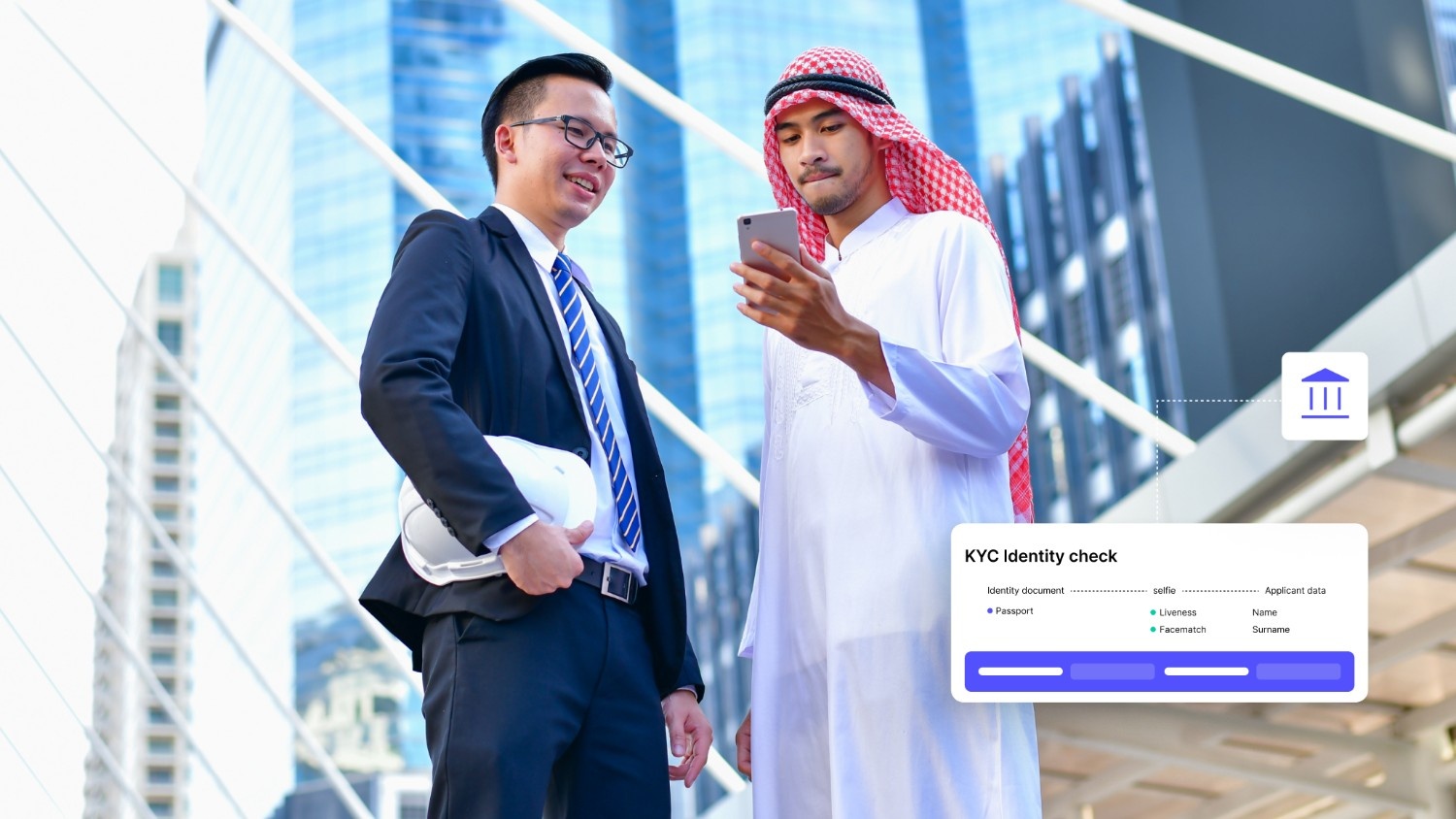

IDs And Data You Typically Need To Request

Scalable compliance starts with collecting the minimum data needed to establish identity. You expand only when risk indicators appear. Over-collection slows onboarding. Under-collection weakens controls.

Below is a practical baseline most programs rely on.

Individual identity data:

- Full legal name.

- Date of birth.

- Residential address.

- Government-issued ID.

- Selfie or liveness check, where applicable.

Business identity data:

- Legal business name and registration number.

- Jurisdiction of incorporation.

- Beneficial owners and control percentages.

- Directors and key officers.

The table below summarizes how these data sets are used across customer and business verification.

Requirements vary by jurisdiction, product type, and risk exposure. Your controls must adapt without rebuilding workflows each time.

Also Read: Navigating KYC, AML, and Identity Verification in the USA

Once you see where programs fail and what regulators expect, the next step is clear. You need an operating model built for changing risk, not fixed checklists.

Best Practice 1: Build A Risk-First Operating Model For AML/KYC Compliance

AML and KYC must function as a continuous control layer across the customer lifecycle. You cannot rely on onboarding checks alone once transaction volume, product access, and geographic reach expand. Risk changes over time, and your operating model must respond without slowing legitimate users.

A risk-first model stays effective by reacting to live signals rather than static assumptions.

Key triggers that should update risk ratings:

- Changes in product usage or transaction velocity.

- New or expanded geographic exposure.

- Ownership or control structure updates.

- Behavioral shifts that break expected patterns.

Design rules that keep controls scalable:

- Segment customers early based on risk exposure.

- Escalate reviews immediately when new risk signals appear.

- De-escalate when evidence supports a lower risk profile.

A Simple Risk Tiering Approach That Scales

Risk tiering helps you route effort where it matters most. You are not labeling customers permanently. You are deciding how much scrutiny is justified at a given point in time.

Below are the core inputs commonly used to assign and adjust tiers.

Common risk tiering inputs:

- Geography and jurisdictional exposure.

- Entity type, such as individual, merchant, or platform.

- Funding source and payment methods.

- Expected account activity and transaction behavior.

- Network signals are tied to related entities or accounts.

Lower-risk tiers move with minimal friction. Higher-risk tiers trigger deeper checks and closer monitoring.

Platforms like AiPrise support this approach by using continuous fraud detection and risk scoring across identity, behavior, and external signals, so risk profiles update in real time without rebuilding workflows.

Best Practice 2: Design KYC And KYB Workflows That Support AML/KYC Compliance

Your workflows must prove identity, establish context, and adapt when risk increases. You are building controls that hold up under audits, not just flows that pass onboarding. Weak structure leads to inconsistent decisions and poor documentation.

KYB deserves special attention. Complex ownership structures and incomplete UBO data create exposure that often surfaces after onboarding.

Effective workflows share a few core traits.

What scalable workflows must support:

- Identity verification that is consistent across regions.

- Contextual risk assessment tied to products and usage.

- Clear escalation paths when risk changes.

- Ongoing monitoring tied back to the original profile.

Also Read: KYC onboarding and AML considerations

Best Practice 3: KYC Flow That Holds Up Under Volume (CIP → CDD → EDD)

Customer Identification Program (CIP), Customer Due Diligence (CDD), and Enhanced Due Diligence (EDD) work best as layered controls. Each layer answers a specific compliance question and determines whether the next level of review is required. This structure keeps low-risk users moving while ensuring higher-risk cases receive the scrutiny regulators expect.

The table below shows what each layer establishes.

EDD typically activates when you see PEP exposure, sanctions proximity, high-risk jurisdictions, or unusual funding patterns.

If you need to verify users across risk tiers without slowing onboarding, AiPrise supports layered user verification from CIP through EDD.

Best Practice 4: Always-On Screening Without Breaking Reviews

Screening must run continuously, not just at onboarding. The challenge is avoiding alert overload while still catching meaningful risk changes. Poor match logic creates noise that slows investigations and frustrates teams.

You reduce review strain by tightening how alerts are generated.

Core screening layers to maintain:

- Sanctions lists

- Politically exposed persons

- Adverse media sources

- Internal watchlists

One control that matters most:

- Strong match logic with entity resolution to avoid duplicate and low-confidence alerts.

Best Practice 5: Reduce False Positives And Manual Workload At Scale

Alert volume grows faster than analyst capacity once you scale. Reviews back up. Good customers get delayed. Risk teams spend time clearing noise instead of investigating real issues. The fix is not more analysts. It is better signal quality before alerts reach a queue.

Pre-enrichment and context-based triage reduce noise by adding meaning early.

Signals that should shape alert quality:

- Identity attributes already verified during onboarding.

- Behavioral patterns tied to expected account activity.

- Device and session consistency across logins.

- External context from sanctions, PEP, and adverse media sources.

The table below shows the operational metrics that reveal whether noise is under control.

Best Practice 6: Case Management And Audit Trails That Regulators Trust

Defensibility comes down to clarity. You must show who made the decision, what evidence was reviewed, and how the conclusion was reached. Gaps in documentation create regulatory risk even when outcomes are correct.

Strong case management enforces consistency.

Controls regulators expect to see:

- Centralized case files with linked evidence.

- Decision notes explaining reasoning.

- Timestamps for reviews and escalations.

- Reviewer identity and approval history.

Sampling and routine QA reviews confirm decisions remain consistent as volume grows.

Also Read: Comprehensive Guide to AML Compliance in FinTech

Best Practice 7: Use Automation Responsibly In AML/KYC Compliance At Scale

Automation should remove repetition, not judgment. You use it to handle volume while keeping humans accountable for risk decisions. Poor automation hides logic and weakens auditability.

Responsible automation follows clear boundaries.

What automation should handle:

- Identity and document checks.

- Risk score updates from new signals.

- Alert routing and prioritization.

- Report and case file assembly.

Controls that keep automation defensible:

- Explainable rules and model outputs.

- Role-based access controls.

- Defined retention policies.

- Logged changes to workflows and rules.

Best Practice 8: Integrate AI Without Creating New Risk

AI works best where volume is high and decisions follow patterns. It should assist reviewers, not replace them. You use it to speed understanding, not override judgment.

Below are low-risk AI use cases most teams adopt first.

Practical AI applications:

- Document classification and data extraction.

- Entity resolution across records.

- Alert summaries for faster review.

- Drafting EDD reports from verified inputs.

High-risk approvals should always require human sign-off.

AiPrise applies automation where volume is highest, while keeping decision logic visible so compliance teams retain control and accountability.

Best Practice 9: Cross-Border Readiness As A Scaling Requirement

Global expansion breaks programs built for one country. Rules change. Data requirements shift. Local controls diverge. Rebuilding workflows for each region slows growth and increases error rates.

Scalable programs rely on modular design.

Controls that support cross-border growth:

- Workflow templates adjusted by jurisdiction.

- Centralized policies with local overlays.

- Consistent KYB and UBO data models.

This structure lets you expand faster without reworking compliance for every new market.

Also Read: Implementing Global KYC Compliance In 7 Steps

You now have the blueprint for what works at scale. The next question is how to run all of this without stitching together tools, teams, and workflows by hand.

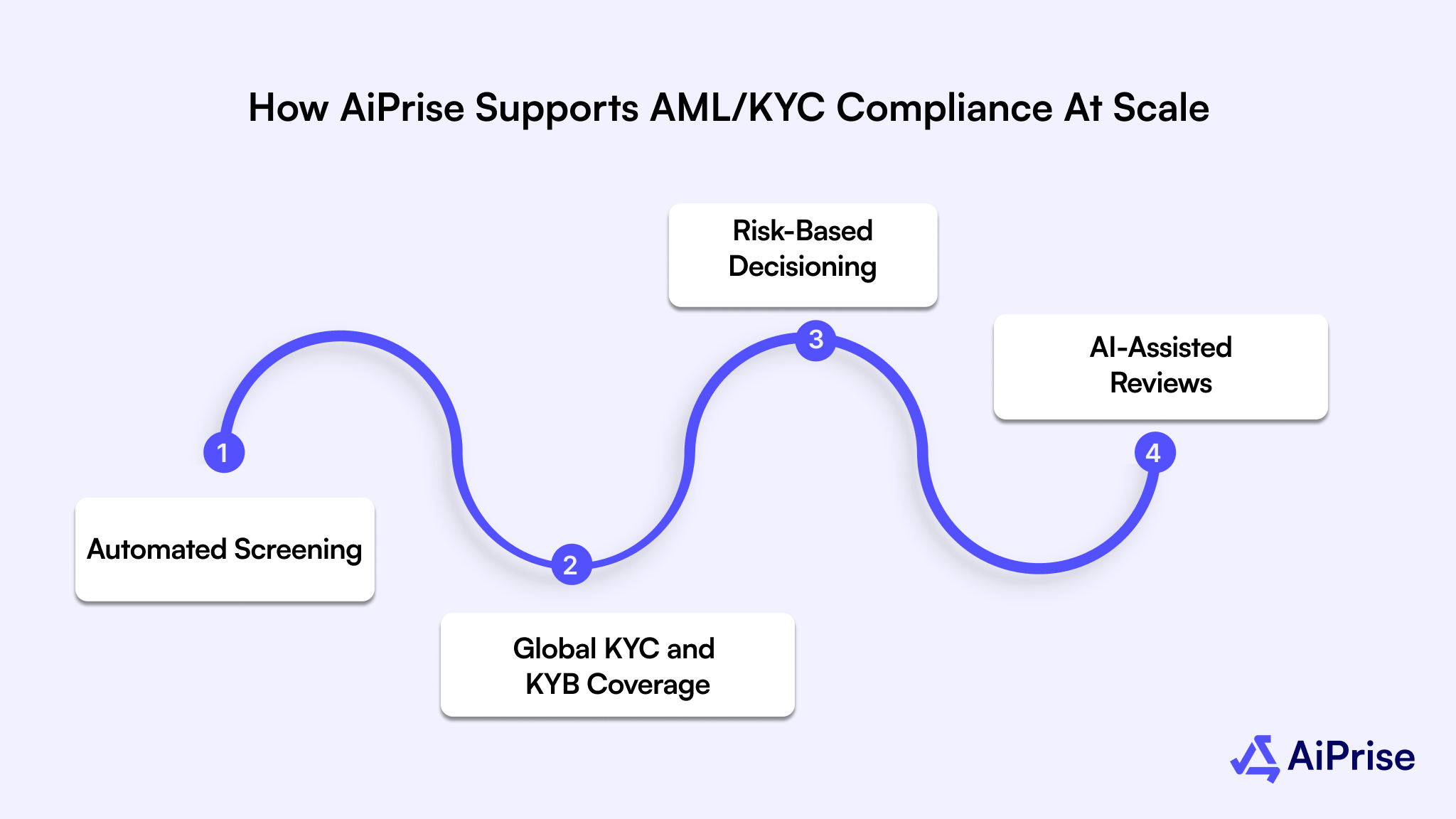

How AiPrise Supports AML/KYC Compliance At Scale

You face the same pressure points as most growing fintechs. Vendors vary by country. Reviews slow as volume rises. Fraud attempts concentrate on onboarding. AiPrise addresses these issues by acting as a compliance infrastructure rather than another point solution.

1. Automated Screening

Continuous checks across sanctions lists, PEP records, and adverse media keep risk visible as customers and businesses change over time. Watchlists, government data, and negative news sources are monitored in the background so you are not relying on point-in-time checks.

2. Global KYC And KYB Coverage

AiPrise verifies both people and businesses across jurisdictions using local and global sources. Proof of address, government records, and registry data help confirm that users and companies are real, active, and operating where they claim.

3. Risk-Based Decisioning

Custom workflows let you apply different review paths based on geography, product, and exposure. Low-risk users move through one-click KYC. Higher-risk entities trigger deeper KYB, UBO checks, and reverification without manual routing.

4. AI-Assisted Reviews

The Compliance Co-Pilot summarizes documents, highlights risk signals, and prepares case notes for analysts. Document insights and structured case views reduce time spent on clerical work while keeping human judgment in control.

5. Fraud And Risk Scoring

Identity, device, behavior, and external records feed into a live risk score. This helps you block bad actors early, before they turn into chargebacks, money movement, or regulatory exposure.

This combination gives you verified users, verified businesses, and audit-ready decisions as you scale across markets.

Final Thoughts

Scalable AML and KYC programs succeed when controls adapt as your business grows. Risk-tiering keeps reviews focused. Continuous monitoring catches change early. Lower noise protects analyst time. Defensible decisions hold up under scrutiny. Together, these practices turn compliance into a reliable operating function rather than a bottleneck.

If you are scaling into new markets or struggling with review volume, Book A Demo to see how AiPrise supports AML and KYC compliance at scale.

FAQs

1. How do you adjust AML and KYC controls during a sudden product launch or feature rollout?

You should run a pre-launch risk review tied to the new feature’s usage patterns and exposure points. Controls must activate at release, not after volume spikes.

2. What is the safest way to migrate AML and KYC programs when switching vendors or platforms?

You need parallel runs with preserved historical decisions and evidence. Migration plans should include validation checks before retiring legacy systems.

3. How can compliance teams prepare for regulator questions without knowing the audit scope in advance?

You maintain standardized decision records and clear ownership for every control. This allows rapid response regardless of audit focus.

4. What role should non-compliance teams play in AML and KYC execution at scale?

Product, operations, and support teams should follow defined escalation signals. This prevents risk blind spots outside compliance workflows.

5. How do you manage AML and KYC data retention without increasing security exposure?

Retention policies should align with jurisdictional timelines and restrict access by role. Archived data must remain searchable and tamper-resistant.

6. What signals indicate your AML and KYC program needs structural change, not tuning?

Rising exception handling, inconsistent reviewer outcomes, and delayed responses signal design limits. At that point, incremental fixes stop working.

You might want to read these...

.jpeg)

.jpg)

.jpeg)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately