AiPrise

15 mins read

June 17, 2025

Comprehensive Guide to AML Compliance in FinTech

Key Takeaways

Financial crime is becoming increasingly difficult to detect and easier to commit. For fintech companies handling high volumes of digital transactions, this poses a significant challenge: how to prevent fraud and money laundering without compromising operational efficiency?

That’s where fintech AML (Anti-Money Laundering) becomes essential. It is not just about ticking a compliance box. It's about protecting your platform, keeping regulators at bay, and ensuring customer trust as you grow.

Most fintech teams recognize the need for compliance controls. However, when it comes to selecting the right tools, understanding regional regulations, or scaling AML processes without introducing friction, things become complicated quickly.

This comprehensive guide clearly breaks down the essentials of fintech AML compliance, highlighting key strategies, common pitfalls, and how to build a robust and efficient framework that truly works.

What Is FinTech AML?

Anti-Money Laundering (AML) refers to the systems, processes, and regulations used to detect and prevent financial crimes, including money laundering, fraud, and terrorist financing. In the fintech space, AML assumes a more complex role due to the speed, scale, and digital nature of financial transactions.

Unlike traditional banks, which often have in-person onboarding and well-established compliance teams, fintechs operate in high-velocity environments where sign-ups, transactions, and verifications all occur digitally, often within seconds. This makes fintech platforms more vulnerable to abuse if AML measures are not tightly integrated into the product from the outset.

How FinTech AML Differs from Traditional AML?

While the goal of AML remains to prevent financial crime, the approach in fintech differs significantly from that of traditional banks.

When business onboarding breaks down, compliance and customer experience both suffer. Discover how AI accelerates onboarding while maintaining strict compliance.

What’s Driving the Need for Strong AML in FinTech?

Several market trends are pushing fintechs to build AML into their core operations:

- Rise of digital payments: Faster transactions mean less time to flag suspicious activity.

- Crypto and virtual assets: Higher anonymity, faster movement of funds, and regulatory gray zones.

- Embedded finance: Non-fintech platforms now offering financial products, raising AML obligations.

- Cross-border transactions: Different jurisdictions mean different compliance expectations.

Once you grasp the basics of AML in fintech, the next step is understanding why these platforms are uniquely vulnerable to financial crime.

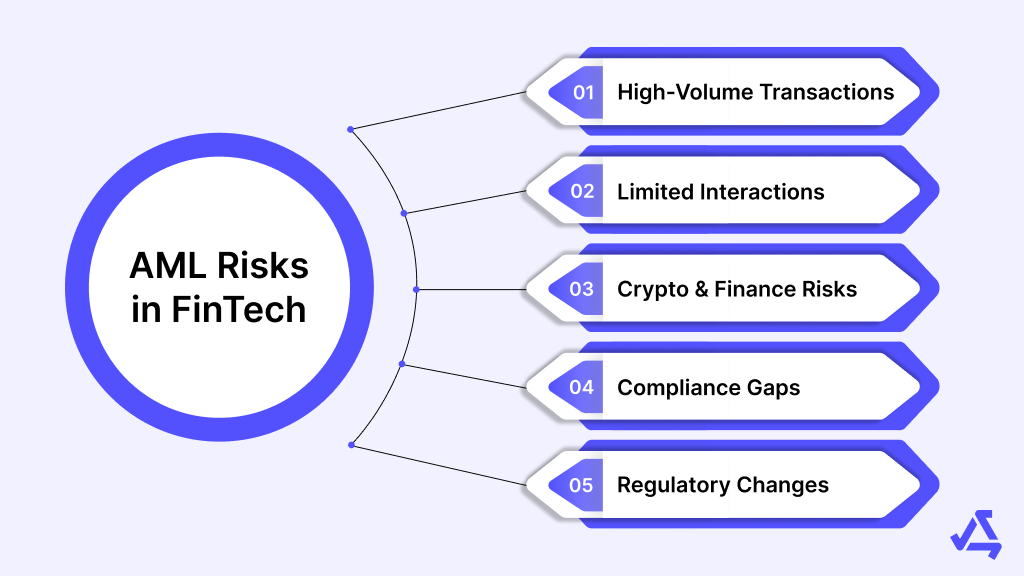

AML Risks in FinTech Models

Fintech companies are transforming the way people access and use financial services, offering speed, convenience, and global reach. However, that same innovation also introduces new vulnerabilities in the context of financial crime.

Here’s why fintechs face a different set of AML risks compared to traditional institutions.

- High Volume, Fast-Moving Transactions:

Fintech platforms often process thousands of small transactions in real time. Whether it’s peer-to-peer payments, instant lending, or crypto transfers, the speed and scale make it harder to catch suspicious patterns before the money moves. Criminals are aware of this and may deliberately exploit high-frequency, low-value transactions to evade detection.

- Limited or No Face-to-Face Interactions:

Most fintechs operate entirely online. There’s no branch visit, no physical ID check, no human touchpoint during onboarding. This creates a higher risk of fraudulent or synthetic identities slipping through, especially if the KYC process isn't robust. Verifying identity digitally is essential, but it becomes more complex without robust controls in place.

- Crypto and Embedded Finance Increase Anonymity:

Fintechs offering crypto wallets, exchanges, or embedded finance features face heightened AML challenges. Cryptocurrencies can offer greater anonymity and faster fund movement across borders. Embedded finance, where non-financial platforms offer financial products, introduces a layer of separation between the user and the regulated entity, making it harder to trace intent and activity.

- Startups Often Lack Dedicated Compliance Teams:

Early-stage fintechs prioritize growth, onboarding, and user experience. AML often comes later. But delaying compliance leaves gaps that can be exploited. Many startups lack in-house legal or risk expertise, leading to shortcuts in KYC processes or inadequate monitoring rules. As funding and user growth accelerate, so does the risk exposure.

- Regulations Are Constantly Evolving:

AML expectations are not static. Regulators frequently update their requirements, especially in areas such as cryptocurrency, beneficial ownership, and real-time monitoring. For fintech teams building global products, staying up to date across different jurisdictions is not just difficult, but also resource-intensive. A single misstep can trigger audits, fines, or even banking partner deactivation.

With these risks in mind, fintechs must move quickly from awareness to action. A well-structured AML compliance program is the first step in maintaining security and credibility.

AML Compliance Program: What FinTechs Need to Build?

AML compliance isn’t just a legal requirement; it’s a foundational layer of trust for any fintech offering financial products. Building an AML program from scratch may feel overwhelming, especially for early-stage teams, but starting with the core components can help fintechs stay ahead of both risks and regulations.

Here’s what a functioning AML program typically includes:

1. Clear Internal Policies and Procedures:

Your AML policies define how your fintech prevents, detects, and responds to suspicious activities. These aren’t generic documents; they need to reflect your business model, customer base, and risk exposure.

A well-written policy outlines the following aspects:

- How customers are onboarded and verified

- How transactions are monitored

- When and how to report suspicious behavior

- Roles and responsibilities within the team

It’s not enough to copy-paste a template. Policies must evolve as your product scales or expands into new markets.

2. Appointing a Compliance Officer:

Every fintech needs a designated AML compliance officer, even if it’s a shared role in early stages. This person oversees the day-to-day execution of your AML program and acts as the point of contact for regulators and banking partners.

Here are their main responsibilities:

- Ensuring your AML program is up to date

- Reviewing alerts and escalation processes

- Coordinating with legal, product, and engineering teams

- Leading audits or responding to regulatory requests

As your company grows, this role typically expands into a full compliance team or department.

3. Staff Training and Awareness

AML compliance isn’t limited to one department. Engineers, product managers, and customer support representatives must all understand what red flags look like and how to escalate them.

Regular training ensures the following:

- Frontline teams know how to spot suspicious behavior

- Internal handoffs (e.g., from support to risk) are smooth

- Teams stay updated on evolving threats, such as identity theft, crypto scams, or fraud rings.

Training should be documented and refreshed at least annually.

4. Independent Audits and Program Testing

Regulators expect fintechs to review their AML processes regularly, and not just internally. Independent audits are crucial for verifying whether your rules, workflows, and decisions are functioning as intended.

A solid audit may include these key components:

- Testing how well alerts are triggered and investigated

- Reviewing whether SARs (Suspicious Activity Reports) are filed when required

- Evaluating whether policies match actual practices

Audits should be risk-based and proportional to the scale of your product.

5. Preventing Misuse at Scale

A good AML program isn’t reactive; it’s designed to prevent misuse in the first place. This means thinking like a fraudster and identifying how your product could be exploited. Preventive strategies include:

- Strong customer risk scoring during onboarding

- Limiting transaction thresholds for unverified users

- Real-time fraud detection based on behavioral patterns

- Sanctions and watchlist screening before enabling features

These safeguards reduce the likelihood of your platform being used for laundering or terrorist financing without slowing down genuine users.

6. Compliance Should Be Built Into the Product, Not Bolted On

Too many fintechs treat compliance as a back-office function or post-launch fix. But the most effective AML programs are tightly integrated into product workflows:

- Risk checks during onboarding

- Flags triggered during fund transfers

- User reviews surfaced in internal dashboards

- KYC/EDD status synced with product access levels

This approach reduces operational friction, ensures faster response, and improves audit readiness. It also aligns with how regulators expect digital-first platforms to operate.

With the core compliance framework in place, the next step is to get identity verification and customer onboarding right, starting with KYC and CDD.

Customer Due Diligence (CDD) and KYC

Customer Due Diligence (CDD) is the first line of defense in any fintech’s AML process. It starts with verifying a customer’s identity through Know Your Customer (KYC) checks and continues with assessing risk and monitoring behavior over time.

Why Digital Identity Verification Matters?

Since most fintechs operate without face-to-face contact, strong digital identity verification is critical. A solid KYC process ensures you’re not onboarding fake identities or bad actors using stolen credentials. It also helps you build a risk profile from the start, which is essential for ongoing monitoring.

Steps in the KYC Process

Fintech KYC usually takes place through the following steps:

- Data Collection: Getting identity documents (ID, passport, proof of address), biometrics, and device metadata.

- Validation: Checking the authenticity of documents, running sanctions/PEP list screening, and verifying phone or email.

- Risk Scoring: Assigning a risk level to the customer based on origin, transaction intent, or profile.

- Ongoing Checks: Watching for changes in behavior or updated sanctions listings.

Global Standards Fintechs Should Know

If you’re serving users across borders, aligning your KYC with international frameworks is a must:

- FATF (Financial Action Task Force): Sets global AML/KYC principles like customer identification, ongoing monitoring, and enhanced checks for high-risk users.

- EU Guidelines (e.g., 6AMLD): Add clarity on liability, identity verification, and stricter penalties for AML breaches, especially relevant if your fintech supports users in Europe.

Outdated KYC processes can create risk blind spots from day one. See what to fix and how AML fits in.

While CDD and standard KYC are critical for everyday users, high-risk customers require a more thorough examination through Enhanced Due Diligence and adverse media screening.

Enhanced Due Diligence (EDD) and Adverse Media Screening

Some users pose higher risks, and for them, basic KYC isn’t enough. That’s where Enhanced Due Diligence (EDD) comes in.

When to Apply EDD?

EDD is triggered for high-risk users, which may include the following groups:

- Politically exposed persons (PEPs)

- Users from high-risk countries

- Customers with unusual transaction patterns

- Businesses in cash-heavy sectors (e.g., gaming, crypto exchanges)

EDD involves gathering additional information, such as the source of funds, business details, and reviewing adverse media.

Adverse Media Screening: What It Is and Why It Matters

Adverse media refers to negative news or allegations about a person or company. Some examples are as follows:

- Financial crime investigations

- Regulatory violations

- Links to fraud, corruption, or terrorism

Screening for this helps identify potential risks not found in standard databases. Tools using AI or NLP (Natural Language Processing) can scan global news, blogs, and legal notices in real time.

But as fintechs scale, manually handling EDD and media checks becomes unsustainable. This is where the right technology stack can make a big difference.

How FinTechs Can Use Technology to Strengthen AML?

As fintechs grow, so does the complexity of their compliance needs. Manual checks that worked for 1,000 users won’t hold up at 100,000. That’s where smart use of technology becomes critical, not just to meet AML requirements, but to do it at scale without slowing down operations.

- AI and Machine Learning for Behavior Detection and Identity Verification: AI models enable fintechs to detect unusual transaction patterns, identify mismatches in identity, and flag potentially risky behaviors more quickly. They adapt to evolving fraud tactics better than rule-based systems and reduce false positives at scale.

- Orchestration Platforms for End-to-End KYC and Compliance: Platforms like AiPrise centralize KYC, transaction monitoring, and SAR filing into one system. This reduces silos, speeds up onboarding, and helps compliance teams act on real-time risk signals across the customer lifecycle.

- API-First Integrations for Screening, Monitoring, and Reporting: APIs allow fintechs to plug compliance tools directly into their product flow. You can automate ID checks at signup, flag suspicious transactions instantly, and auto-generate audit reports—all without disrupting user experience.

- Automation vs. Manual Review: When to Use Both: Automation handles high-volume tasks like user screening or triggering alerts. But complex or high-risk cases often need manual review. A blended approach ensures speed without compromising on accuracy or quality of compliance.

- Single Vendor vs. Multiple Point Solutions: One end-to-end vendor simplifies integration, support, and data flow. However, some teams prefer mixing specialized tools. AiPrise supports both, offering modular services while enabling holistic compliance management if needed.

Once you’ve mapped out your tech needs, the next step is finding an AML partner that can actually deliver at your speed and scale.

What to Look for in an AML Vendor for FinTech?

Choosing the right AML tech partner is a make-or-break decision for fintechs. It affects how quickly you can onboard users, detect risks, and stay audit-ready.

Here’s what to look for in an AML vendor:

- Global Coverage: Your vendor should support compliance across multiple regions, especially if you operate cross-border. This includes local KYC laws, data residency rules, and multilingual support.

- Custom Workflows: All fintechs don’t follow the same flow. Your AML partner should let you tailor onboarding, verification, and monitoring processes to match your product and risk profile.

- Sanctions & PEP Lists: Real-time access to global sanctions, watchlists, and politically exposed persons (PEP) databases is essential. The broader and more frequently updated the data, the lower your risk exposure.

- Case Management Tools: Look for built-in dashboards that enable compliance teams to efficiently flag, investigate, and resolve alerts. A good case management system saves time during audits and streamlines internal reviews.

- Real-Time Screening: Your AML system should instantly screen transactions, users, and documents as they come in. Delays create compliance gaps and impact the user experience.

- Flexibility and Audit Support: Whether you’re early-stage or scaling fast, your AML tools should grow with you. Choose a vendor that provides full audit logs, customizable reports, and responsive support when regulators come calling.

How AiPrise Supports Scalable, Audit-Ready AML for FinTechs

Fintech companies often face tight deadlines, limited compliance resources, and fast-changing regulations. AiPrise helps address these challenges by automating core AML functions, allowing your team to focus on growth rather than manual checks.

Here’s how AiPrise helps fintechs build efficient, future-ready AML systems:

- Real-Time Sanctions & PEP Screening: Instantly checks users against global watchlists and PEP databases, reducing onboarding risks while maintaining a smooth user experience.

- AI-Powered Transaction Monitoring: Detects suspicious behaviors using a mix of rule-based logic and behavioral analysis. Risk scoring helps prioritize alerts for quick follow-up.

- Modular AML Tools via API: From KYC to SAR filing, fintechs can plug in only what they need. Compliance Co-Pilot integrates easily with your stack.

- Built-In Case Management: Investigate, document, and resolve AML alerts all in one place, keeping your audit trail clean and centralized.

- No-Code Rule Editor: Compliance teams can launch and update logic-based workflows without technical dependencies, ensuring agility as rules evolve.

AiPrise supports fintechs at every stage, whether you’re onboarding your first thousand users or scaling across markets with complex compliance needs.

Conclusion

As regulatory scrutiny tightens, fintechs can no longer afford to treat AML as a checkbox activity. A robust, well-integrated compliance program is now essential, not just to avoid penalties, but to win the trust of customers, partners, and regulators.

By investing in the right strategies and tools, fintechs can stay ahead of evolving threats, strengthen operational resilience, and scale with confidence. Solutions like AiPrise’s Compliance Co-Pilot make it easier to automate critical AML processes, adapt to regulatory changes, and maintain audit readiness, without slowing down innovation.

Book a demo with AiPrise to see how Compliance Co-Pilot simplifies AML for modern fintechs.

FAQs on AML Compliance for FinTechs

- What is AML in the context of FinTech?

AML (Anti-Money Laundering) in FinTech refers to the policies, technologies, and practices employed by financial technology companies to detect, prevent, and report financial crimes, including money laundering and terrorist financing. - How is AML different in FinTech compared to traditional banks?

FinTechs rely on digital channels, which means faster transactions, limited face-to-face contact, and greater reliance on automation, making AML programs more technology-driven and risk-adaptive than in traditional banking. - Why is AML compliance critical for FinTech companies?

Failing to comply with AML regulations can result in substantial fines, reputational damage, business restrictions, and even criminal investigations. It’s essential for gaining trust and operating legally in regulated markets. - When should FinTechs use Enhanced Due Diligence (EDD)?

EDD is required when dealing with high-risk customers, such as politically exposed persons (PEPs), those from high-risk jurisdictions, or users with large or complex transactions. - What are Suspicious Activity Reports (SARs)?

SARs are reports submitted to regulatory bodies when a company detects potentially suspicious behavior, such as unusual transaction patterns or inconsistent customer activity. - How can technology improve AML efforts in FinTech?

AI, machine learning, and orchestration tools help automate identity verification, detect behavioral anomalies, and manage compliance workflows more efficiently and at scale. - What are the penalties for non-compliance with AML regulations?

Penalties vary by jurisdiction but can include multi-million dollar fines, license revocations, operational bans, and even imprisonment for executives in extreme cases.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately