AiPrise

13 min read

October 9, 2025

Understanding Anti Money Laundering Policies and Their Importance

Key Takeaways

Money laundering is a serious and complex global issue that threatens the integrity of financial systems, businesses, and governments alike. It involves an illicit process of disguising the origins of large sums of money derived from criminal activities, such as drug trafficking, fraud, or corruption, to make them appear legitimate.

To combat this pervasive problem, countries and businesses have put in place compliance programs that aim to detect and deter money laundering activities. A strong money laundering policy is essential to safeguard the reputation of institutions and ensure the stability of the global financial ecosystem.

In this blog, we’ll delve into what money laundering policies are, why they are important, and the steps involved in implementing them effectively.

Key Takeaways

- Money laundering poses significant risks to financial systems and businesses, enabling criminal activities like fraud and terrorism financing. Preventing it is crucial for maintaining integrity in the global economy.

- AML policies are essential for businesses to detect, prevent, and report money laundering activities, ensuring compliance with legal regulations and protecting against legal, financial, and reputational damage.

- Aiprise offers advanced tools that streamline KYC, AML, and risk management processes, including government verifications, watchlist screening, case management, and AI-powered compliance to simplify staying compliant.

- Staying compliant with AML regulations is critical to avoid hefty fines, loss of licenses, or reputational damage. Aiprise helps businesses meet evolving regulatory standards with ease and efficiency.

- Continuous monitoring and updates are necessary to stay compliant. Aiprise’s platform supports real-time audits, document analysis, and periodic client reverification to ensure businesses stay ahead of regulatory changes.

What is Money Laundering?

Money laundering is the process of making illegally obtained money appear legitimate by concealing its true origin. Criminal organizations and individuals use this process to "clean" money generated through illicit activities like drug trafficking, terrorism financing, tax evasion, human trafficking, and corruption.

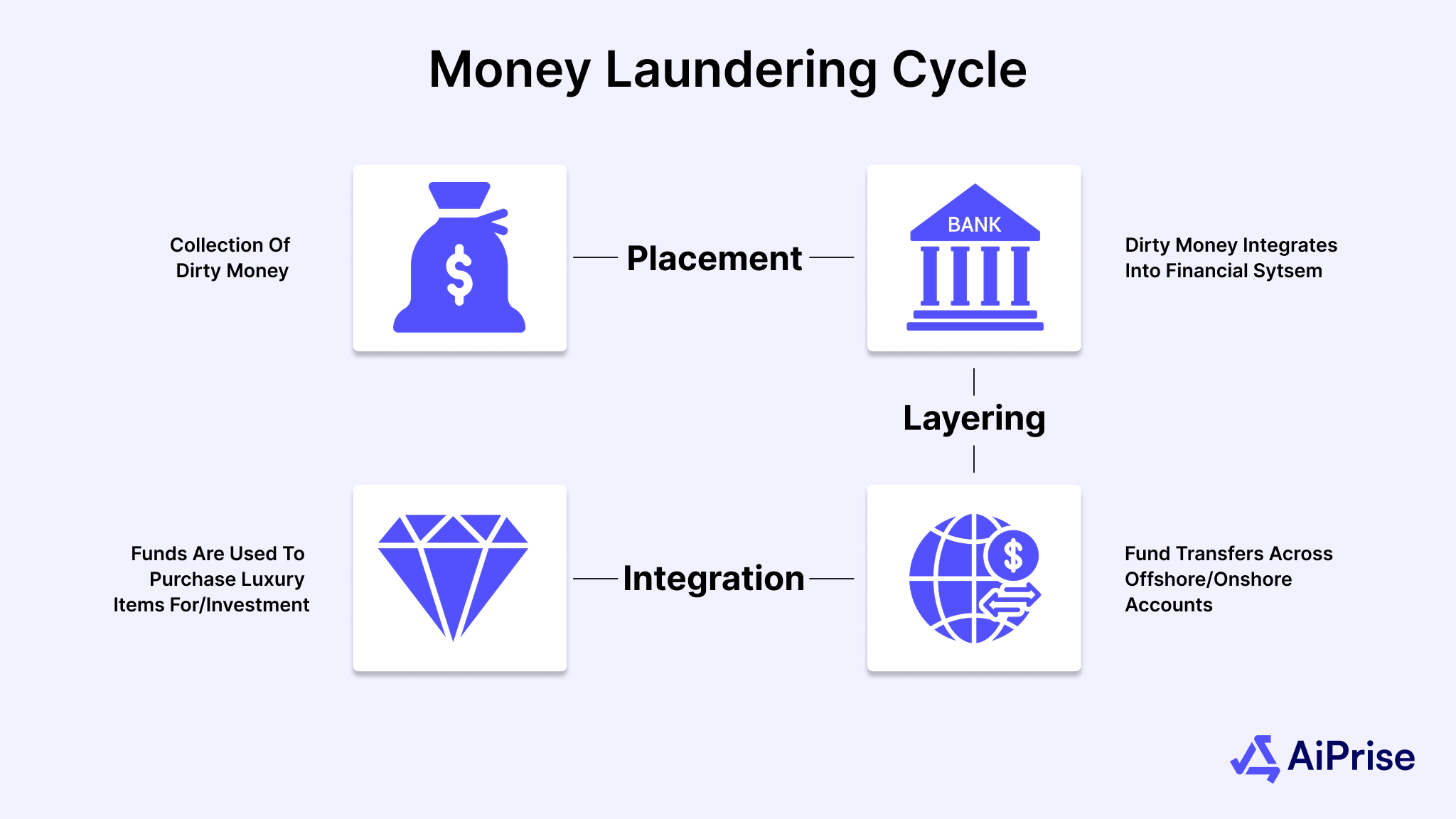

Money laundering typically occurs in three key stages:

- Placement: The first stage involves introducing the illicit funds into the financial system. This can be done through methods like bank deposits, purchasing assets, or other means that make the money seem like it came from a legitimate source.

- Layering: In this stage, the goal is to obscure the source of the funds by moving them through a complex series of financial transactions. This could involve transferring money between various accounts, using shell companies, or purchasing financial instruments. The purpose of layering is to create a trail that is difficult for authorities to trace.

- Integration: The final stage is where the laundered money is reintroduced into the legitimate economy. This might involve purchasing real estate, investing in businesses, or acquiring high-value goods. At this point, the money is considered "clean," as it appears to come from lawful sources, making it difficult to distinguish from legal earnings.

The impact of money laundering is far-reaching. It can distort markets, harm businesses, and erode the stability of financial institutions. It also facilitates other forms of organized crime, including terrorism, and can destabilize economies by diverting resources from legitimate investments.

Given the complexity and global scale of money laundering activities, financial institutions, businesses, and governments must take proactive steps to combat it.

That’s where a well-structured money laundering policy comes into play, ensuring organizations implement effective measures to detect and prevent these criminal practices.

Suggested read: How to Detect Money Laundering? All You Need to Know.

What is a Money Laundering Policy?

A money laundering policy is a set of procedures and guidelines that an organization adopts to prevent, detect, and report money laundering activities. It is a critical component of an institution's broader AML framework, serving as a blueprint for identifying and mitigating the risks associated with illicit financial activities.

The policy ensures that the organization complies with national and international regulations, thereby helping to protect the institution’s reputation, integrity, and operational stability.

A well-defined money laundering policy typically includes several key components:

1. Customer Due Diligence (CDD) and Know Your Customer (KYC) Procedures:

These procedures are designed to verify the identity of customers and assess the potential risk they pose in terms of money laundering. KYC involves collecting information such as identification documents and the nature of the customer’s business, while CDD goes further by continuously monitoring customer activity to detect suspicious transactions.

2. Risk Assessment:

A money laundering policy should include a process for assessing the level of risk associated with customers, transactions, and geographical regions. Institutions must classify customers and transactions based on the risk of being involved in money laundering activities. Higher-risk clients, for instance, may require enhanced due diligence.

3. Suspicious Activity Monitoring and Reporting:

Money laundering policies often include protocols for monitoring customer transactions for unusual or suspicious activity. Any red flags—such as large, unexplained transactions or cross-border transfers—should trigger an investigation and may require the filing of a Suspicious Activity Report (SAR) with regulatory authorities.

4. Employee Training:

Regular training is a key component of an effective money laundering policy. Employees must understand the risks of money laundering, recognize red flags, and know how to report suspicious activities. The training also helps ensure that staff stay updated on regulatory changes and emerging trends in financial crimes.

5. Record Keeping:

A robust policy should outline requirements for maintaining records of financial transactions, customer identification, and suspicious activity reports. These records must be easily accessible for review by authorities during audits or investigations and must be retained for a specified period, often several years.

6. Compliance Officer:

The appointment of a dedicated compliance officer or team is critical. This individual or group is responsible for overseeing the implementation of the money laundering policy, ensuring compliance with relevant laws, conducting internal audits, and coordinating with external authorities as needed.

A comprehensive money laundering policy not only helps institutions avoid legal and regulatory penalties but also fosters trust with customers and stakeholders by demonstrating a commitment to ethical business practices and transparency.

The Importance of Money Laundering Policies

Money laundering policies are essential for protecting financial systems, ensuring regulatory compliance, and safeguarding business reputations. Here's why these policies are crucial, backed by real-world data:

1. Protecting Against Financial Crimes

Money laundering enables a range of criminal activities, including drug trafficking, terrorism financing, and tax evasion. The UNODC estimates that money laundering accounts for $800 billion to $2 trillion annually, or 2% to 5% of global GDP. This underscores the global scale of the issue and the need for effective AML policies to prevent ilegal funds from entering the financial system.

2. Regulatory Compliance

Failure to comply with anti-money laundering regulations can lead to hefty fines and reputational damage. In 2020, global fines for non-compliance exceeded $10 billion, with major institutions like Deutsche Bank and Danske Bank facing significant penalties for inadequate AML practices. A strong policy helps organizations avoid these risks.

3. Safeguarding Reputation

Involvement in money laundering can severely damage a company’s reputation. ACAMS reports that institutions involved in scandals lose, on average, 6% of their market value. Implementing an effective money laundering policy helps protect business credibility and maintain customer trust.

4. Enhancing Financial Stability

Money laundering distorts financial markets and undermines economic stability. According to the World Bank, money laundering and related activities can cost economies significantly in lost revenue and diminished investor confidence. AML policies are vital for maintaining financial stability by detecting and preventing such illicit activities.

5. Supporting Global Security

Money laundering often funds criminal and terrorist activities. FATF highlights how groups like ISIS and Al-Qaeda have used laundered money to finance their operations. Robust money laundering policies help prevent the flow of illicit funds into these activities, contributing to global security.

6. Facilitating Risk Management

Effective money laundering policies enable businesses to assess and manage risks through Customer Due Diligence and KYC procedures. These measures help identify suspicious transactions and reduce exposure to financial crimes.

Strong money laundering policies are essential for ensuring regulatory compliance, protecting reputations, maintaining financial stability, and contributing to global security. Given the scale of money laundering, businesses must take proactive measures to combat this threat.

Key Elements of an Effective Money Laundering Policy

An effective money laundering policy should cover several critical areas to detect, prevent, and address illicit financial activities. These include:

1. Customer Due Diligence (CDD) and Know Your Customer (KYC)

CDD and KYC are essential for verifying customer identities and understanding their business relationships. These processes help assess risk and ensure that higher-risk clients undergo additional scrutiny, making it easier to detect suspicious activity.

2. Suspicious Activity Monitoring and Reporting

A strong policy includes systems to monitor transactions for unusual patterns and flags potential money laundering activities. When suspicious activity is detected, businesses must file a Suspicious Activity Report (SAR) with relevant authorities for investigation.

3. Risk-Based Approach

A risk-based approach tailors monitoring efforts to higher-risk clients and transactions, such as those involving politically exposed persons (PEPs) or high-risk countries, ensuring efficient allocation of resources to manage risks effectively.

4. Employee Training and Awareness

Ongoing training ensures that employees can identify and report suspicious activities. A well-informed workforce helps prevent money laundering by spotting red flags and taking appropriate actions.

5. Record Keeping and Documentation

Businesses must maintain detailed records of customer transactions and reports for several years. Proper documentation supports compliance with AML laws and ensures businesses can demonstrate their efforts during audits or investigations.

6. Independent Auditing and Monitoring

Regular internal audits and independent reviews are crucial for assessing the effectiveness of money laundering policies. These audits help identify gaps and ensure policies remain effective and compliant with changing regulations.

A comprehensive money laundering policy involves robust due diligence, monitoring, training, and auditing practices to prevent illicit financial activities and ensure compliance.

Also read: Methods for Effective Money Laundering Detection.

Global Standards and Regulations in Anti-Money Laundering (AML)

AML regulations are shaped by both international standards and national laws. Understanding these frameworks is crucial for businesses operating across borders.

International Standards: The FATF Recommendations

The Financial Action Task Force (FATF) sets the global benchmark for combating money laundering and terrorist financing. The FATF Recommendations, most recently updated in June 2025, outline a detailed set of measures that countries are encouraged to adopt in order to address and prevent illicit activities. These include:

- Risk-Based Approach: Countries should identify, assess, and understand the money laundering and terrorist financing risks they face, and take effective action to mitigate these risks.

- Preventive Measures: Financial institutions and designated non-financial businesses and professions (DNFBPs) should implement measures such as customer due diligence (CDD), record-keeping, and reporting of suspicious activities.

- International Cooperation: Countries should cooperate with each other to combat money laundering and terrorist financing, including sharing information and providing mutual legal assistance.

For detailed information, refer to the official FATF Recommendations: FATF Recommendations.

National Regulations: United States Example

In the United States, the Financial Crimes Enforcement Network (FinCEN) enforces AML regulations under the Bank Secrecy Act (BSA). Key components include:

- Suspicious Activity Reports (SARs): Financial institutions are required to file SARs when they detect suspicious transactions. These reports help law enforcement identify and investigate potential money laundering activities.

- Customer Due Diligence (CDD): Institutions must verify the identity of their customers and understand the nature of their business relationships to assess and mitigate risks.

For more information on FinCEN's requirements, visit: FinCEN SARs.

Adapting Policies to Local Jurisdictions

While international standards provide a foundation, businesses need to tailor their AML policies to comply with local regulations. This includes:

- Understanding Local Laws: Familiarize yourself with the specific AML requirements in each country where you operate.

- Implementing Appropriate Measures: Adapt your policies and procedures to meet local legal obligations while maintaining alignment with international standards.

By adopting policies that meet global and local regulations, businesses can safeguard their reputation and avoid costly legal issues. More importantly, they become part of a united front against financial crime. We'll now look at the consequences when you fail to implement these critical measures.

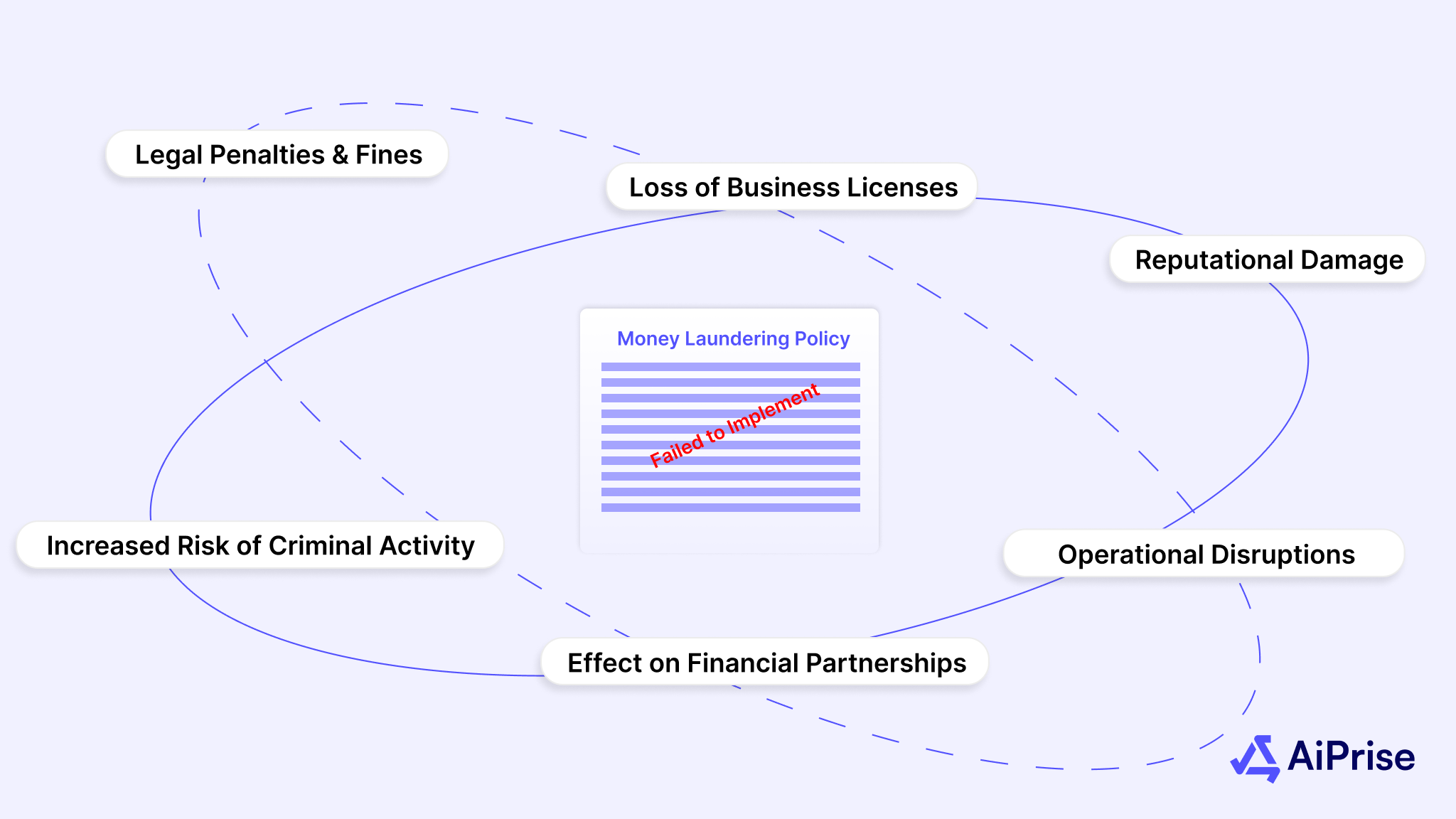

The Consequences of Failing to Implement a Money Laundering Policy

Failing to implement a robust money laundering policy can have severe and far-reaching consequences for businesses. The risks are not only legal and financial but also reputational, impacting the long-term viability and success of the organization. Here’s a breakdown of the potential consequences:

1. Legal Penalties and Fines

One of the most immediate and significant consequences of failing to comply with anti-money laundering regulations is the imposition of heavy fines. In 2020 alone, global fines for non-compliance with AML regulations exceeded $10 billion. Major institutions like HSBC, Standard Chartered, and Deutsche Bank have faced enormous financial penalties due to lapses in their money laundering controls. The cost of non-compliance can also include criminal charges, particularly for executives or officers responsible for the failure.

2. Loss of Business Licenses

Failure to adhere to AML regulations may result in the suspension or revocation of business licenses. This can effectively halt operations in certain markets, causing significant financial strain. The U.S. Treasury Department’s Office of Foreign Assets Control (OFAC), for example, can impose sanctions on businesses found to violate AML laws, including restricting access to the U.S. financial system.

3. Reputational Damage

The reputational impact of being associated with money laundering is perhaps one of the most damaging consequences. Even if a company is not directly involved in money laundering, being linked to illicit activities can erode trust with customers, partners, and investors. This loss is often compounded by a long-term decline in customer loyalty and business relationships.

4. Operational Disruptions

Dealing with the fallout from non-compliance can disrupt business operations. This can involve extensive investigations, audits, and internal restructuring. The time, resources, and attention required to handle legal proceedings, regulatory actions, and public relations crises can divert focus from core business activities, resulting in operational inefficiencies and lost revenue.

5. Impact on Relationships with Financial Partners

Financial institutions, including banks and investors, are often required to assess the AML compliance of their partners. If a business fails to meet these requirements, it may face challenges in securing funding, establishing banking relationships, or gaining access to financial services. In some cases, companies may even find themselves blacklisted by financial institutions, making it difficult to operate within the financial ecosystem.

6. Increased Risk of Criminal Activity

Failing to implement effective money laundering policies can inadvertently create an environment where criminal activity thrives. Weaknesses in a company's systems can facilitate the flow of illicit funds undetected, potentially exposing the business to involvement in further criminal activities, including fraud, corruption, and even terrorist financing.

By aligning with global and local regulations, businesses can protect their reputation, ensure compliance, and help combat money laundering. Now, let’s explore how businesses can continue refining their policies to stay ahead of emerging challenges.

Given the serious consequences of non-compliance, having a strong anti-money laundering policy is crucial for business protection and regulatory alignment. As regulations continue to evolve, staying vigilant is key. This is where platforms like Aiprise can help you streamline compliance, minimize risks, and safeguard your business.

How Aiprise Helps Businesses Avoid the Consequences of Non-Compliance

Aiprise offers a suite of advanced tools designed to help businesses stay compliant and prevent fraud. Its technology simplifies KYC, AML, and risk management processes, ensuring businesses can easily meet regulatory standards. Here are the key features Aiprise provides:

Real-Time Suspicious Activity Monitoring

Our AI-powered monitoring tools flag suspicious transactions in real time, allowing for quick action and timely Suspicious Activity Reports (SARs), keeping you compliant with regulatory expectations.

Aiprise’s easy-to-use case management tool helps businesses efficiently track and handle suspicious activities, ensuring that potential fraud cases are managed promptly and accurately.

The platform checks customers and transactions against global sanctions lists and watchlists, helping identify high-risk clients and transactions, ensuring compliance with international regulations.

Aiprise offers an easy-to-integrate onboarding SDK, allowing businesses to incorporate KYC and AML checks into their client onboarding process, simplifying verification while maintaining compliance standards.

Businesses can create automated workflows for their compliance processes, ensuring necessary steps are followed, reducing human error, and improving operational efficiency.

Aiprise’s one-click KYC solution streamlines identity verification for both businesses and clients, speeding up the onboarding process while meeting regulatory requirements.

Aiprise uses advanced technology to extract and analyze data from client documents, ensuring only valid documents are accepted and reducing the risk of document fraud.

Aiprise’s AI-powered Compliance Copilot reduces review times by 95%, enabling businesses to achieve faster, more efficient compliance processes from day one.

With these tools, Aiprise enables businesses to stay ahead of regulatory requirements and mitigate fraud risks. Its comprehensive suite ensures that companies remain compliant and protected against financial crimes.

Conclusion

As regulatory requirements continue to evolve and criminal methods become more sophisticated, organizations must remain vigilant in updating and strengthening their anti-money laundering frameworks. The investment in robust policies, systems, and training not only fulfills legal obligations but also contributes to the broader fight against financial crime and terrorism financing.

Success in anti-money laundering compliance requires ongoing commitment, adequate resources, and a culture of compliance throughout the organization.

Aiprise helps you build a culture of compliance through streamlined AML processes, reduce risks, and maintain a transparent and secure financial ecosystem.

Book A Demo today to see how our solutions can help your business.

Frequently Asked Questions (FAQs)

1. What is Anti-Money Laundering Policy (AML Policy)?

An Anti-Money Laundering (AML) policy is a set of regulations and procedures adopted by financial institutions and businesses to prevent, detect, and report suspicious money laundering activities.

2. What is Money Laundering?

Money laundering is the process of disguising the origins of illegally obtained money to make it appear legitimate. Criminals use money laundering to “clean” funds generated through illegal activities like fraud, drug trafficking, or corruption, making them difficult to trace.

3. What is the Prevention of Money Laundering Act of 2002?

The Prevention of Money Laundering Act (PMLA) of 2002 is an Indian law designed to combat money laundering and seize assets obtained through illicit activities.

4. How can Aiprise help my business stay compliant with AML regulations?

Aiprise streamlines AML compliance by automating KYC verifications, watchlist screening, and suspicious activity monitoring. With tools like case management and AI-powered compliance, Aiprise ensures that your business can easily meet regulatory standards and mitigate fraud risks.

5. How does Aiprise handle customer data privacy and security?

Aiprise uses advanced encryption technologies to protect sensitive customer data, ensuring compliance with global privacy laws like GDPR. The platform guarantees secure data storage and monitoring while maintaining high privacy standards.

You might want to read these...

.png)

.png)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately