AiPrise

12 min read

October 9, 2025

Key Components of BSA AML Risk Assessment

Key Takeaways

In the world of financial services, ensuring compliance with BSA/AML regulations is essential to prevent money laundering, fraud, and other illicit activities. With the rapid expansion of global financial markets, institutions are increasingly vulnerable to these risks.

A striking statistic from the World Bank reveals that an estimated $2.7 trillion is laundered annually. This underlines the growing challenge financial institutions face in preventing illicit transactions and maintaining the integrity of the financial system.

To address these challenges, financial institutions must implement a robust risk evaluation process. In this blog, we will examine the three fundamental components of BSA risk assessment, enabling businesses to effectively evaluate and manage risks in an increasingly complex regulatory environment.

Key Takeaways

- BSA/AML risk assessment is a foundational process for identifying and mitigating financial crime risks in businesses.

- The 3 fundamental components of risk assessment—customer, product, and transaction risks—are essential to ensuring compliance and protecting businesses from illicit activities.

- Having AI-powered fraud detection, customizable risk decisioning, and real-time monitoring can significantly enhance your risk assessment processes.

- Aiprise simplifies risk assessments with its comprehensive KYC/AML platform, offering global coverage, automated compliance, and AI-driven fraud scoring to help businesses operate securely and stay compliant.

- By adopting a robust risk assessment strategy, businesses can reduce their exposure to money laundering, fraud, and other financial crimes, while protecting their reputation and ensuring smooth operations.

Understanding BSA/AML Risk Assessment Fundamentals

A BSA/AML risk assessment serves as the cornerstone of every effective compliance program, providing the analytical foundation that guides policy development, resource allocation, and control implementation. This assessment establishes the foundation for a credit union's AML/CFT program, and this principle applies equally to all financial institutions.

Core Purpose of BSA/AML Risk Assessment:

- Identify potential money laundering and terrorist financing vulnerabilities.

- Evaluate the likelihood and impact of various risk scenarios.

- Determine appropriate controls and mitigation strategies.

- Guide resource allocation for compliance activities.

- Support regulatory examination and oversight requirements.

The assessment process requires institutions to systematically analyze their operations, customer base, products, and services to understand where risks may emerge and how they can be effectively managed.

With regulatory expectations continuing to evolve, a comprehensive understanding of risk assessment components has become more critical than ever for financial institutions.

Also read: Performing KYB Verification and Risk Assessment.

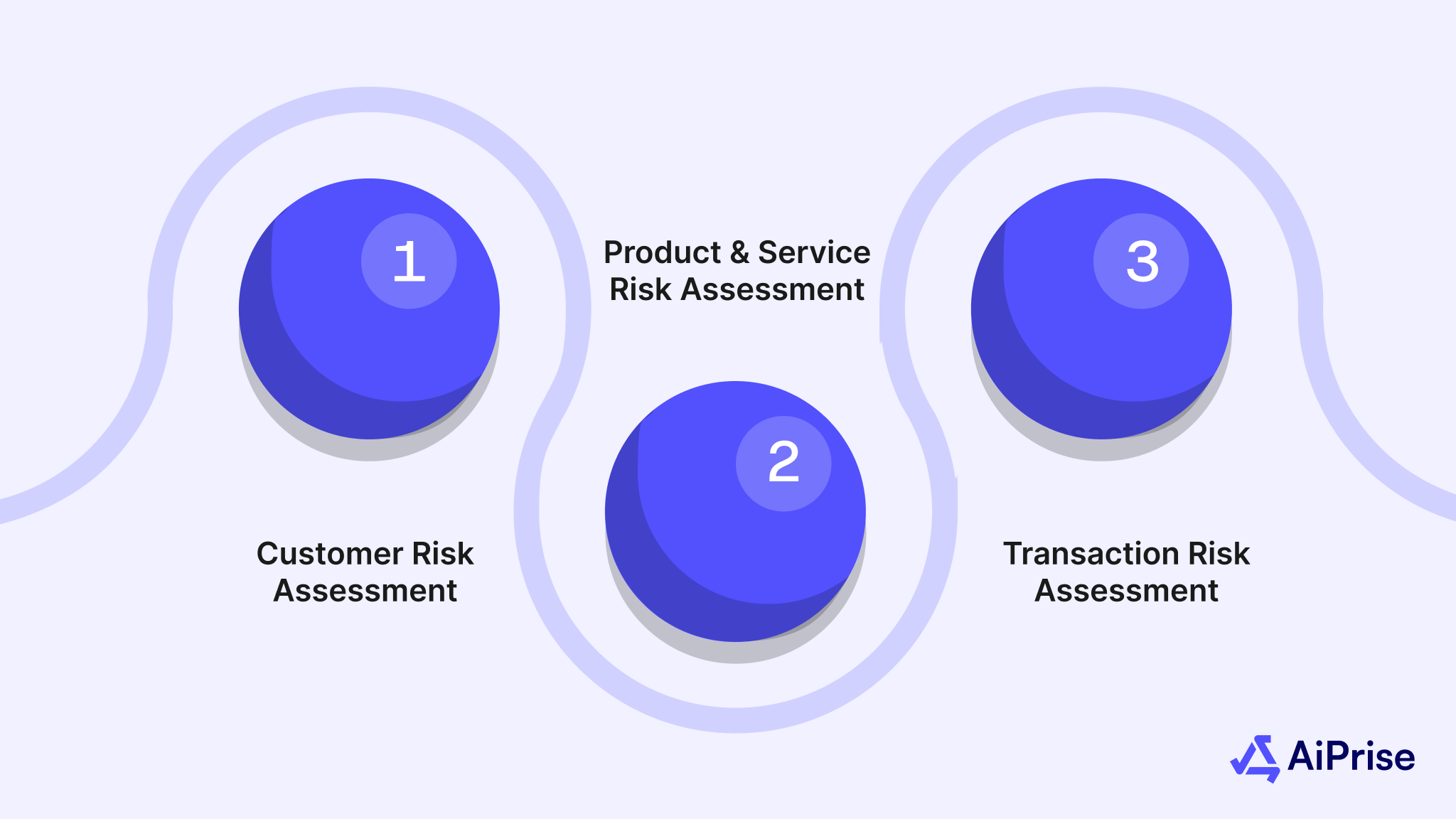

The 3 Fundamental Components of Risk Assessment BSA

The BSA/AML risk assessment framework centers on three fundamental components that work together to provide comprehensive risk coverage. These components form the basis for all effective risk assessment methodologies and ensure institutions address all critical areas of potential vulnerability.

Component 1: Customer Risk Assessment

The first key component of risk assessment is evaluating customer risk. This step is critical because understanding the risk profile of your customers helps you tailor your compliance efforts effectively, identifying those who pose a higher risk and may require enhanced scrutiny.

Why Customer Risk Assessment Matters:

The primary objective of a customer risk assessment is to assess the likelihood that a particular customer could be involved in money laundering, fraud, or other illicit activities. By categorizing customers based on various risk factors, financial institutions can allocate resources more efficiently and ensure a targeted approach to compliance.

Factors Influencing Customer Risk Level:

Several factors are taken into account when assessing a customer's risk profile, including:

- Geographic Location: Customers from high-risk jurisdictions—such as countries known for weak anti-money laundering laws or high levels of corruption—are typically considered higher risk. A customer from a country with a large informal economy or political instability might raise red flags.

- Business Type or Industry: Certain industries are more prone to money laundering due to their nature. For example, industries like gambling, remittance services, or high-value goods sales (e.g., luxury items) are more vulnerable to being exploited for money laundering purposes.

- Transaction History and Patterns: A customer’s transaction history is a key indicator. Unusual or inconsistent transactions, such as sudden large deposits or frequent international wire transfers to high-risk countries, could suggest suspicious activity.

Tools for Assessing Customer Risk:

Financial institutions utilize various tools and techniques to assess and monitor customer risk, including:

- Know Your Customer (KYC) Procedures: These are fundamental in gathering essential information about the customer, such as their identity, source of funds, and business activities.

- Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD): CDD provides a basic level of scrutiny for most customers, while EDD is used for higher-risk clients, involving deeper background checks, financial profiling, and ongoing monitoring.

- Risk Rating Models: Many institutions use automated systems to assign a risk rating to each customer based on the factors mentioned above. This helps prioritize compliance efforts and identify customers who may require more frequent reviews or enhanced scrutiny.

By effectively assessing customer risk, financial institutions can make more informed decisions, mitigate potential risks, and focus on the areas that matter most to their compliance strategy.

Component 2: Product and Service Risk Assessment

The second critical component in an AML risk assessment is evaluating the risk associated with the products and services your institution offers. Different financial products and services come with varying levels of exposure to money laundering and fraud. Understanding these risks is essential for designing an effective compliance strategy and ensuring that the right checks and controls are in place.

Why Product and Service Risk Assessment Matters:

Some financial products and services are inherently more susceptible to abuse than others. For example, services that involve large sums of money, international transfers, or anonymous transactions are often prime targets for illicit activities. By identifying high-risk products, institutions can take targeted measures to mitigate risks associated with these services.

Identifying High-Risk Products and Services:

Certain financial services and products present higher risks of being exploited for money laundering activities, including:

- Wire Transfers and International Payments: These services allow money to flow across borders quickly and often with less scrutiny. Large or frequent cross-border transfers, especially to or from high-risk countries, may raise red flags.

- Private Banking and Wealth Management: These services cater to high-net-worth individuals, who may be involved in complex transactions and structures that are difficult to track. As a result, private banking services are often a target for money laundering.

- Prepaid Cards and Cryptocurrency: Prepaid cards and digital currencies offer a degree of anonymity, making them attractive for individuals looking to hide the source of their funds. Cryptocurrency, in particular, is often used for illicit transactions due to its pseudonymous nature.

- Trade-Based Services: Trade finance, used for the financing of imports and exports, can sometimes be exploited to move illicit funds across borders under the guise of legitimate trade transactions.

Evaluating and Mitigating Product Risks:

To assess the risk of each product or service, financial institutions must analyze its inherent vulnerabilities. This can be done through:

- Risk-Based Approach: Products and services are evaluated based on how likely they are to be used for illegal activity. A risk-based approach helps allocate resources efficiently, focusing more on high-risk products while still maintaining oversight over low-risk ones.

- Monitoring and Surveillance: Ongoing transaction monitoring is crucial for identifying suspicious activities. For example, if a high-value customer makes an unusually large transaction using a product with high risk (like cryptocurrency or wire transfer), it should be flagged for further investigation.

- Control Measures: Financial institutions should implement adequate controls for high-risk products, such as enhanced KYC processes, additional transaction monitoring, and limits on high-risk transactions.

By evaluating the risks associated with their products and services, institutions can better understand where vulnerabilities lie and take the necessary steps to mitigate these risks.

Component 3: Transaction Risk Assessment

The third critical component in BSA/AML risk assessment involves monitoring and evaluating the risks associated with transactions. Monitoring transactions helps institutions detect suspicious activities that could indicate potential money laundering, terrorist financing, or other illicit activities. This component is crucial for enabling financial institutions to identify red flags in real-time and take prompt action to prevent illicit transactions.

Why Transaction Risk Assessment Matters:

Transactions are the most direct and visible indicators of illicit activities. Financial institutions must scrutinize each transaction, looking for patterns or signs of suspicious behavior. By assessing transaction risk, institutions can take timely action to stop potential criminal activity before it escalates.

Common Transaction Red Flags:

Certain transaction patterns can signal that something is amiss. These may include:

- Large or Unusual Transactions: Transactions that are unusually large compared to a customer's normal activity, especially when there is no clear business reason or justification for the transaction, could indicate money laundering.

- Multiple Small Transactions (Smurfing): A pattern of small transactions that are structured to evade detection, often referred to as "smurfing," can suggest an attempt to launder money by breaking up larger sums into smaller, less noticeable transactions.

- Cross-Border Transactions: Large, frequent, or complex cross-border transactions, especially when involving high-risk jurisdictions, can be a sign of suspicious activity. These transactions can easily obscure the true source or destination of the funds.

- Rapid Movement of Funds: A pattern where funds are quickly moved between accounts, often in a short period of time or to different countries, may indicate layering in the money laundering process.

- Transactions Involving High-Risk Countries: Transactions involving countries or regions that are considered high-risk due to weak anti-money laundering laws, corruption, or high levels of criminal activity should always raise concerns.

Tools and Technologies for Transaction Monitoring:

To effectively assess transaction risks, financial institutions use a variety of advanced monitoring systems and technologies:

- Transaction Monitoring Systems (TMS): These automated systems monitor real-time transactions for suspicious patterns and flag them for further investigation. Many systems use predefined rules to identify common money laundering activities, such as unusual transaction sizes or foreign transactions.

- Machine Learning and AI: AI-powered systems can learn from past suspicious activities and improve the detection of new, potentially illicit transactions by identifying hidden patterns in data.

- Suspicious Activity Reporting (SARs): Once a suspicious transaction is identified, it is reported through SARs, which are filed with the relevant authorities, such as the Financial Crimes Enforcement Network (FinCEN) in the United States. These reports provide important insights into potential criminal activities.

Transaction Risk Mitigation:

To effectively mitigate transaction-related risks, institutions should:

- Enhance Monitoring: Set up automatic alerts for transactions that deviate from normal behavior and ensure that these are thoroughly reviewed.

- Perform Ongoing Reviews: Regular reviews of customers' transaction histories can help spot patterns that indicate illicit activities. Monitoring must be an ongoing process, as new risks and tactics emerge frequently.

- Use Screening Tools: Screening tools can help identify suspicious links between customers and sanctioned individuals or entities, such as those on OFAC's Specially Designated Nationals List (SDN).

By monitoring and assessing transaction risk, financial institutions can quickly identify potential threats and prevent further criminal activities from entering the financial system.

Suggested Read: 6 Key Components of Anti Money Laundering Compliance Checklist

Essential Steps for BSA/AML Risk Assessment Success

Once the core components of the BSA/AML risk assessment (customer, product, and transaction risks) are understood, it’s important to implement a systematic process for ensuring that your risk assessment is effective. Here are the 7 essential steps to conduct a thorough risk assessment, stay compliant, and minimize financial crime risks:

Step 1: Gather All Relevant Data

The first step in conducting a risk assessment is to gather the necessary data from customers, products, services, and transactions. This includes customer profiles, transaction history, and product/service details. Ensuring that this data is up-to-date and accurate is key to identifying any potential risks.

Step 2: Identify and Categorize Risks

Next, you need to identify all the possible risks within your institution’s operations. This involves considering all risk factors associated with:

- Customers (geographic location, business type, politically exposed persons, etc.)

- Products and services (cryptocurrency, wire transfers, prepaid cards, etc.)

- Transactions (large/suspicious activity, international transfers, etc.)

Once identified, categorize the risks based on their potential impact and likelihood. High-risk customers or transactions should be flagged for more intensive monitoring.

Step 3: Assess the Severity of Risks

After categorizing the risks, assess their severity. High-impact, high-probability risks should be prioritized. For example, customers from high-risk jurisdictions or products like cryptocurrency exchanges may require more frequent and in-depth monitoring. This assessment helps allocate compliance resources effectively.

Step 4: Implement Mitigation Measures

For each identified risk, implement appropriate mitigation measures. For high-risk customers or products, this might mean enhanced due diligence (EDD) or implementing stricter KYC and AML procedures. Ensure your monitoring systems are robust and your compliance staff is well-equipped to handle the risk areas with the highest exposure.

Step 5: Conduct Regular Monitoring

Risk assessments should not be a one-time task. Implement continuous monitoring to track ongoing transactions and customer activities. This helps detect and address potential risks in real-time. Transaction monitoring systems can automatically flag suspicious activities and trigger alerts for review.

Step 6: Regularly Update the Risk Assessment

The financial market and regulations are constantly changing, so it's essential to update your risk assessment regularly. New risks emerge with technological innovations (like cryptocurrencies) and changing regulations. Make sure your risk assessment is dynamic and evolves with these changes.

Step 7: Report Findings and Take Action

Once you’ve conducted the risk assessment and implemented mitigation measures, the next step is to report your findings. This includes filing Suspicious Activity Reports (SARs) for any flagged activities and documenting the steps taken to address identified risks. Keep detailed records for future audits or regulatory inspections.

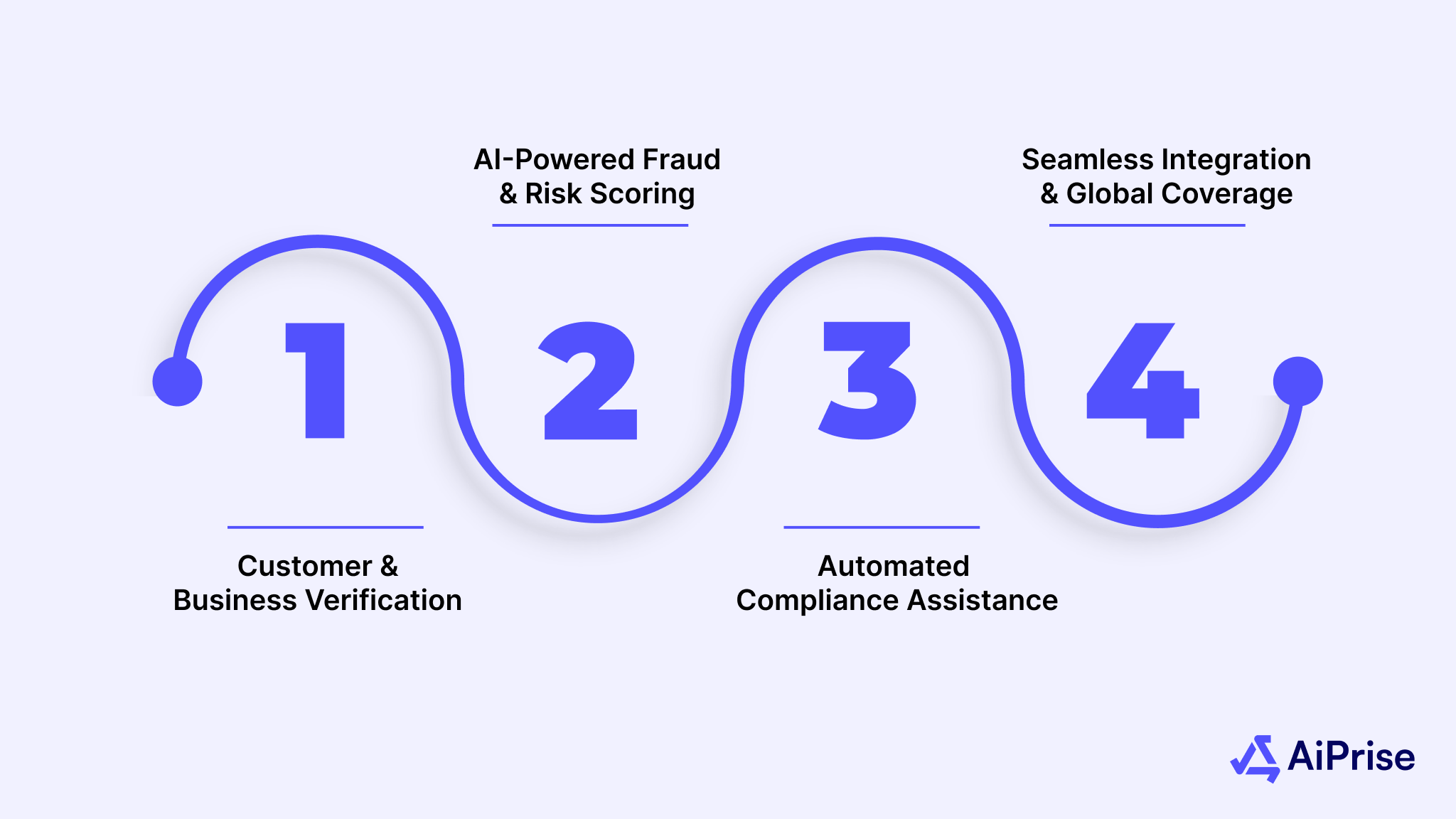

How Aiprise Helps Businesses Lead with Confidence Through Risk Assessment

Conducting a thorough BSA/AML risk assessment is crucial for businesses that want to stay compliant and avoid significant risks. Aiprise empowers businesses to confidently navigate this complexity through its robust suite of tools and features designed to streamline risk assessment, prevent fraud, and ensure regulatory compliance—all from a single platform.

This is how Aiprise strengthens risk assessments:

1. Comprehensive Customer and Business Verification

Aiprise provides reliable KYC and KYB solutions to ensure your customer and business information is verified, reducing the chances of engaging with high-risk entities. With global coverage and advanced fraud checks, Aiprise makes sure that you onboard only trusted and verified individuals and businesses.

2. AI-Powered Fraud and Risk Scoring

Aiprise takes a data-driven approach by analyzing over 100+ data sources and using machine learning to evaluate fraud risk at onboarding. The platform’s customizable rule engine allows businesses to tailor the risk scoring models to their specific needs and risk tolerance, providing a comprehensive and dynamic risk profile.

3. Automated Compliance Assistance

With Aiprise’s Compliance Co-Pilot, businesses can automate key compliance processes, reducing the time spent on manual reviews by up to 95%. This helps ensure that EDD and other critical compliance activities are completed efficiently and accurately. The platform also allows businesses to generate detailed EDD reports and monitor ongoing compliance effortlessly.

4. Seamless Integration and Global Coverage

Whether you’re operating in 220+ countries or handling cross-border transactions, Aiprise offers seamless integration with multiple global vendors, allowing businesses to scale quickly without sacrificing compliance standards. This ensures that your risk assessment process remains robust, even as your business expands internationally.

By offering automated KYC/AML verification, customizable risk decisioning, and real-time customer monitoring, Aiprise empowers businesses to proactively mitigate risks, safeguard their reputation, and stay ahead of evolving regulations.

Conclusion

A thorough BSA/AML risk assessment is a critical component of safeguarding your business against financial crimes, protecting your reputation, and ensuring operational integrity. By carefully assessing customer, product, and transaction risks, businesses can proactively prevent illicit activities and minimize their exposure to regulatory fines and legal complications.

With the help of powerful tools and innovative solutions like Aiprise, businesses can take their risk assessment processes to the next level.

Book a Demo with Aiprise today to see how our platform can help your business lead with confidence and stay compliant in the ever-changing financial market.

Frequently Asked Questions (FAQs)

1. What is BSA/AML risk assessment?

BSA/AML risk assessment is a process used by financial institutions to evaluate the risks of money laundering, fraud, and terrorist financing. It involves assessing customer profiles, products, services, and transactions to ensure compliance with anti-money laundering regulations.

2. Why is customer risk assessment important?

Customer risk assessment is crucial because it helps institutions identify potential threats posed by individuals or businesses. By evaluating factors such as geographic location, business type, and transaction history, financial institutions can better allocate resources and ensure appropriate compliance measures are in place.

3. How can Aiprise help with BSA/AML risk assessments?

Aiprise offers a comprehensive platform for KYC, AML verification, and fraud detection, utilizing AI-driven fraud scoring, customizable rule engines, and global coverage. This helps businesses efficiently assess and manage risk, stay compliant, and scale without complexity.

4. What are the key components of a BSA/AML risk assessment?

The key components include customer risk assessment, product/service risk evaluation, and transaction risk monitoring. Each component helps identify and mitigate different types of risks associated with financial crimes.

5. How often should a BSA/AML risk assessment be conducted?

Risk assessments should be an ongoing process. Institutions should conduct an initial risk assessment during customer onboarding and continue to review and update the assessment regularly.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately