AiPrise

8 min read

November 3, 2025

How Consent Orders Guide Stronger Banking Compliance Systems

Key Takeaways

Ever wondered how a single consent order can suddenly reshape your bank's compliance priorities overnight?

You face fines, operational limits, reputational damage, and stretched remediation budgets that drain strategic focus. In May 2025, the FDIC reported issuing twelve orders and two notices, including one consent order. Knowing these patterns helps you prioritize board accountability, independent testing, and stronger third-party controls now. Acting early reduces remediation costs, shortens restrictions, and restores stakeholder trust faster than reactive measures.

Quick Overview

- Consent order banking holds institutions accountable for compliance failures, driving stronger governance, structured remediation, and long-term oversight improvement.

- Regulators issue consent orders when repeated AML, KYC, or risk management lapses threaten financial integrity and operational soundness.

- These orders reshape compliance programs through stricter monitoring, documented accountability, and transparent communication across all business functions.

- Handling consent orders effectively requires organized action plans, interdepartmental coordination, and sustained commitment to regulatory reporting and risk management.

What Is a Consent Order In Banking?

In banking, a consent order is a formal agreement between your institution and a regulator requiring you to correct specific compliance weaknesses. It often follows repeated exam findings or serious violations in areas like AML, BSA, or risk management. A consent order banking situation demands structured remediation, regular reporting, and independent validation to prove sustainable compliance. Understanding how these orders work helps you anticipate regulatory expectations, strengthen oversight, and prevent future enforcement actions before they escalate.

Knowing what a consent order is sets the stage for understanding why regulators issue them, and what they’re trying to fix.

Purpose of Consent Orders

Consent orders exist to hold financial institutions accountable when compliance gaps threaten stability, transparency, or customer trust. They push you to strengthen oversight, update monitoring frameworks, and establish lasting governance improvements. Here are the key reasons regulators issue consent orders:

- Regulators step in when recurring audit findings reveal deep compliance or operational control weaknesses within your institution.

- Enforcement actions often arise when AML, KYC, or BSA systems fail to detect suspicious activity or prevent financial misconduct.

- A consent order banking case, such as the CFPB’s 2025 action against Wise US Inc., highlights regulators’ growing focus on due diligence and AML compliance.

- Leadership accountability becomes mandatory through enforced board oversight, independent validation, and ongoing remediation updates.

- Regulators aim to restore stakeholder confidence and ensure your operations align with evolving national and global compliance expectations.

Once a consent order is issued, it doesn’t just address one issue; it reshapes your entire compliance structure from the inside out.

Also read: How KYC Is Done In Banks: A Step by Step Guide

How Consent Orders Reshape Compliance Programs?

Consent orders drive a complete transformation of compliance programs by enforcing structure, accountability, and measurable improvement. They help you rebuild trust while closing regulatory gaps and preventing repeated audit failures. Here are the core changes these orders trigger:

1. Strengthened Oversight and Governance

Board oversight becomes far more active under a consent order banking directive, ensuring every compliance function is clearly supervised. Senior leadership must review remediation progress regularly, document accountability, and demonstrate measurable control improvements to regulators. This shift reduces blind spots in decision-making and creates a governance model that’s transparent, accountable, and resistant to future compliance breaches.

2. Formalized Risk and Compliance Frameworks

Consent orders require your institution to document every compliance process, escalation route, and remediation step in clear operational terms. Detailed frameworks replace informal practices, ensuring risk assessment, monitoring, and escalation protocols are traceable and auditable. This structure helps your compliance team maintain consistency and respond faster to regulatory examinations or external audit reviews.

3. Enhanced Monitoring and Testing

Continuous monitoring becomes a regulatory expectation, demanding stronger transaction surveillance and independent validation of implemented fixes. Testing cycles must now verify effectiveness, not just completion, ensuring sustainable remediation rather than short-term compliance activity. This helps your team detect weaknesses early and correct them before they evolve into material regulatory violations.

4. Improved Vendor and Third-Party Oversight

Consent order banking directives frequently target gaps in vendor management and third-party due diligence frameworks. Institutions must reassess their external partners’ compliance readiness, update risk rating models, and implement real-time performance tracking. These steps ensure external vendors adhere to the same governance standards as internal departments, reducing exposure to secondary compliance risks.

5. Defined Accountability and Documentation

Each department receives explicit accountability metrics, and every corrective action must have supporting documentation for examiner review. This level of detail ensures no remediation step is missed and creates a lasting compliance record for regulatory validation. Strong documentation also accelerates future audits, minimizes penalties, and strengthens your institution’s defense against reputational risks.

Understanding how these transformations happen makes it easier to see where consent orders stand among other enforcement actions.

Understanding How Regulators Enforce Banking Compliance

Every enforcement tool serves a specific purpose, but consent order banking actions usually point to deeper compliance and governance weaknesses. Recognizing how these differ from other regulatory measures helps you assess issue severity, plan remediation effectively, and strengthen oversight. The table below outlines these distinctions clearly:

Once enforcement is in motion, the focus shifts to execution, and that’s where banks often encounter their toughest challenges.

Also read: Comprehensive Guide to Embedded Banking and Finance

Challenges Faced During Consent Order Banking

A consent order often pushes your compliance program into unfamiliar territory, exposing operational, strategic, and cultural challenges. Understanding these obstacles helps you anticipate regulatory demands and prepare your teams for sustained oversight. Here are the key challenges you’re most likely to encounter:

- Managing simultaneous remediation projects strains your internal resources and stretches compliance staff beyond capacity.

- Aligning multiple departments under one remediation plan becomes difficult when accountability and ownership are unclear.

- Meeting regulator-imposed deadlines adds pressure, especially when remediation depends on third-party consultants or technology vendors.

- Gathering accurate data across systems for progress reports turns into a major hurdle without strong integration and documentation.

- Sustaining leadership attention throughout a long remediation process proves challenging once immediate regulatory pressure subsides.

- Coordinating communication with regulators requires precision, as inconsistent updates can weaken supervisory confidence in your progress.

- Embedding new control frameworks into daily operations often takes longer than planned due to legacy systems or staff resistance.

- Maintaining team morale during intense regulatory scrutiny becomes tough when staff face extended workloads and limited flexibility.

- Budgeting for extended compliance remediation, technology upgrades, and independent reviews can disrupt broader business objectives.

These challenges make it clear why a structured action plan is essential for keeping remediation on track.

Compliance Readiness Checklist for Consent Orders

When your institution enters a consent order banking phase, you must act quickly, stay organized, and prove measurable progress. A structured checklist keeps you focused, ensures accountability, and helps your teams meet every regulatory requirement efficiently. Here’s what you should prioritize:

- Conduct a full gap analysis to understand the exact compliance deficiencies identified by regulators.

- Establish a remediation committee that defines clear responsibilities, deadlines, and escalation paths across departments.

- Document each corrective action carefully so you can provide complete evidence during regulatory progress reviews.

- Integrate compliance dashboards that help you track remediation milestones and report updates accurately.

- Assign independent reviewers to validate remediation outcomes and give your board credible assurance.

- Centralize your communication with regulators to maintain clarity, consistency, and transparency throughout the process.

- Keep your AML, KYC, and risk assessment frameworks current with your products, customers, and operational scope.

- Strengthen your transaction monitoring systems so alerts capture evolving risk patterns and compliance triggers.

- Involve senior leadership frequently to reinforce accountability and visible governance commitment.

- Allocate sufficient budgets for technology improvements, independent audits, and external compliance expertise.

- Train your teams to interpret enforcement terms precisely and align operations with remediation goals.

- Store all documentation, reports, and communication records securely to demonstrate steady, verifiable progress.

Having a checklist ensures order and accountability, but having the right tools can make remediation faster and easier.

Also read: 3 Essential Components of KYC

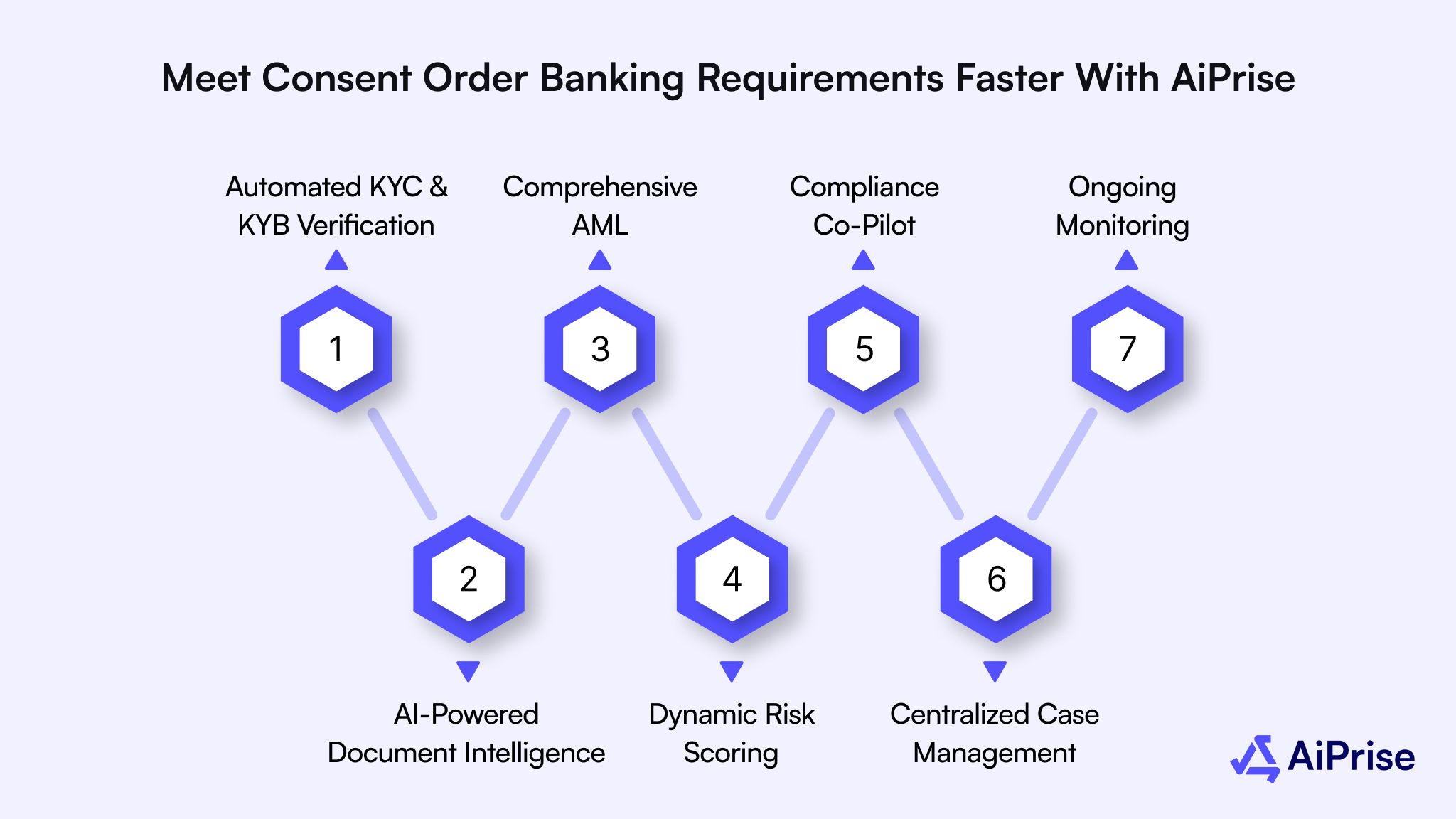

Meet Consent Order Banking Requirements Faster with AiPrise

Respond to regulatory consent orders confidently with AI-powered compliance automation built for financial institutions under remediation. Here’s how AiPrise helps your bank close gaps, accelerate reporting, and prove sustainable compliance to regulators:

- Automated KYC and KYB Verification: Validate customers and businesses instantly using 100+ data sources to meet enhanced due diligence mandates.

- AI-Powered Document Intelligence: Extract, cross-check, and verify details from ID documents, incorporation records, and ownership proofs within seconds.

- Comprehensive AML and Sanctions Screening: Continuously monitor users, entities, and transactions against global watchlists to prevent repeat compliance failures.

- Dynamic Risk Scoring and Fraud Detection: Detect suspicious behavior early through AI-driven analysis of device, behavioral, and transaction patterns.

- Compliance Co-Pilot for Remediation: Slash review time with AI-assisted case analysis, auto-generated EDD reports, and policy gap summaries for regulatory reporting.

- Centralized Case Management: Log all remediation steps, attach supporting evidence, and track deadlines from a unified compliance dashboard.

- Ongoing Monitoring and Alerts: Maintain continuous oversight of high-risk clients to demonstrate long-term regulatory readiness and control sustainability.

Wrapping Up

A consent order marks a turning point where your institution must transform oversight, strengthen internal systems, and rebuild regulator trust. Meeting every commitment requires organized execution, transparent reporting, and sustainable governance that continues long after the order closes. Treating remediation as a strategic reset, not a penalty, helps you restore compliance confidence and operational stability faster.

AiPrise equips you to achieve that transformation with automated verification, AI-powered monitoring, and regulator-ready documentation workflows. Its unified platform streamlines remediation tracking, enhances audit transparency, and ensures continuous compliance across your global operations. With AiPrise, you can close consent order requirements faster, strengthen long-term governance, and future-proof your institution against recurring compliance risks.

Book A Demo today to see how AiPrise simplifies consent order remediation, automates compliance workflows, and restores regulator confidence faster.

LinkedIn Snippet

A single consent order can change how your bank operates overnight, forcing leadership to fix oversight gaps and rebuild compliance trust. From stricter AML and KYC frameworks to real-time monitoring, regulators are tightening expectations across every line of defense.

Learn how U.S. institutions are strengthening governance, improving documentation, and managing remediation smarter through data-driven compliance systems.

#ConsentOrderBanking #Compliance #BankingRegulations #AML #KYC #RiskManagement #RegTech #FinancialCompliance #Governance #BankingOversight #AiPrise

FAQ

1. What triggers a consent order in banking?

A consent order is typically triggered when regulators identify recurring compliance failures, weak internal controls, or serious violations that haven’t been resolved through prior supervisory actions.

2. How long does a consent order remain active?

A consent order stays in effect until the regulator verifies that all required corrective actions have been completed and validated, which can take months or even years, depending on complexity.

3. What happens if a bank fails to meet consent order requirements?

Failure to comply can result in civil penalties, activity restrictions, leadership changes, or further enforcement actions, including cease-and-desist directives.

4. Are consent orders public?

Yes, most consent orders issued by agencies like the FDIC, OCC, or Federal Reserve are publicly available through their enforcement databases.

5. How does a consent order impact a bank’s operations?

It can restrict growth, delay new product approvals, and require extensive reporting, redirecting significant resources toward compliance remediation and oversight.

6. Can consent orders apply to fintechs or non-bank entities?

Yes, regulators can issue consent orders to any financial entity under their jurisdiction, including payment companies and fintech partners involved in regulated activities.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately