AiPrise

11 min read

December 17, 2025

A Guide to AML Requirements for Payment Processors in 2026

Key Takeaways

Payment processors may not face the same regulatory scrutiny as banks or traditional financial institutions, but they remain accountable for the transactions they handle on behalf of customers.

Meeting anti-money laundering (AML) obligations is not only a legal requirement, but a core part of the AML requirements for payment processors, critical for operational resilience and maintaining customer trust.

This guide breaks down four essential AML requirements for payment processors, with a focus on how automated compliance frameworks can help firms effectively manage risk and ensure responsible onboarding.

Key Takeaways

- Payment processors must meet strict AML rules, including KYC, CDD, real-time monitoring, and risk-based controls across all customer transactions.

- Rising enforcement means processors face major fines, licensing risks, and reputational damage for weak identity checks or poor AML oversight.

- Automation helps processors streamline onboarding, detect suspicious activity instantly, and maintain audit-ready AML documentation.

- High transaction volumes, multi-jurisdiction rules, and advanced laundering tactics make manual AML processes ineffective and risky.

- AiPrise unifies identity verification, behavioral analytics, and risk scoring to help processors identify threats early and stay compliant.

Understanding AML Requirements for Payment Processors

For payment processors, AML requirements encompass the policies, processes, and tools needed to prevent financial systems from being misused for money laundering or terrorist financing. These obligations reflect the broader compliance responsibilities of payment processors, which extend beyond onboarding to continuous transaction oversight, reporting, and risk governance.

Given the global nature of payments, processors must align with laws and standards specific to their operational regions, including the U.S. Bank Secrecy Act (BSA), the EU’s 5th and 6th AML Directives, and international FATF recommendations.

Know Your Customer (KYC)

KYC forms the foundation of an AML framework. Payment processors are responsible for verifying the identities of clients, whether individuals or businesses, during onboarding. This process involves collecting identifying information, authenticating documents, and screening against sanctions lists or Politically Exposed Persons (PEPs).

A thorough KYC setup not only mitigates fraud and financial crime but also provides a baseline for ongoing risk management.

Transaction Monitoring

Monitoring customer transactions is an ongoing requirement to identify unusual or suspicious activity. Processors can leverage rule-based systems, AI-driven analytics, or a combination of both to detect anomalies.

Indicators of concern include sudden transaction surges, payments to high-risk regions, or repetitive low-value transfers designed to avoid detection. Timely alerts enable faster investigation and regulatory reporting while reducing false positives.

Customer Due Diligence (CDD)

CDD goes beyond initial identity checks to maintain continuous oversight of customer activity and risk profiles. Processors should scale their due diligence based on the risk associated with each customer.

High-risk clients, such as those operating in sensitive sectors or high-risk jurisdictions, may require Enhanced Due Diligence (EDD) measures to ensure compliance and prevent abuse.

Risk Assessment

A risk-based approach allows payment processors to prioritize compliance efforts according to the level of exposure. This involves analyzing customer types, transaction patterns, and geographic factors to classify risk, then applying controls proportionate to the identified threat.

Effective risk assessments help streamline compliance efforts while maintaining regulatory alignment.

Together, these form the core AML requirements for payment processors operating in high-volume, multi-jurisdiction payment environments.

By implementing robust KYC, transaction monitoring, ongoing CDD, and risk-based controls, processors can detect suspicious activity early, reduce financial crime exposure, and maintain trust while staying aligned with regulatory expectations.

Suggested Read: How to Spot a Fake Identity: A Guide to Combating Synthetic Fraud

AiPrise helps payment processors stay AML-compliant and reduce financial crime risk. Its Fraud and Risk Scoring solution evaluates customer behavior, transaction patterns, and high-risk activity in real time. It enables teams to meet AML obligations, intervene before violations occur, and safeguard operations.

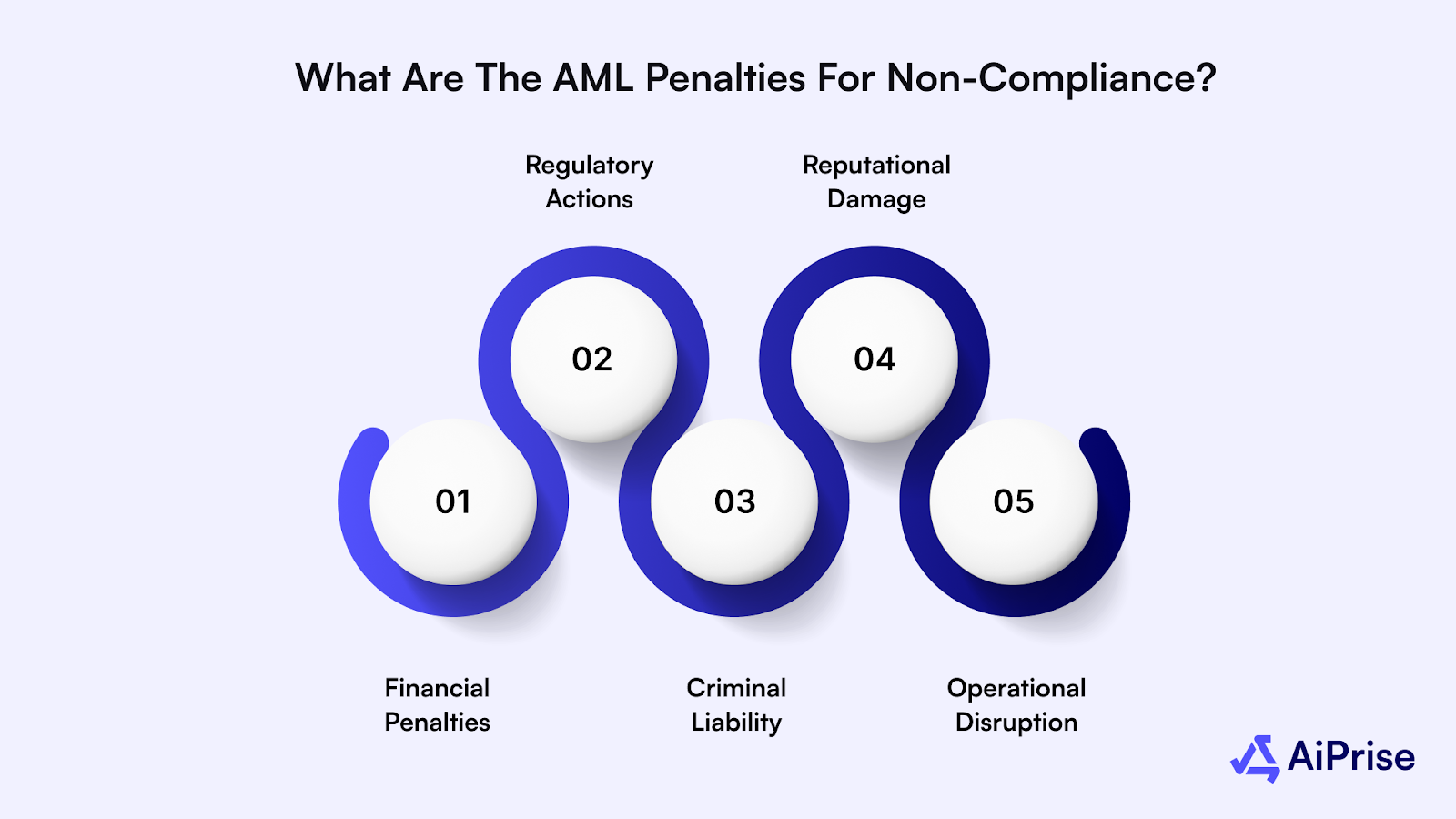

What are the AML Penalties for Non-Compliance?

Failing to meet AML obligations can carry serious financial, operational, and reputational consequences, underscoring the compliance responsibilities of payment processors under global regulatory frameworks.

Regulators are increasingly vigilant, and enforcement actions are becoming more frequent and severe.

Key impacts include:

Financial Penalties

Firms can face multi-million-dollar fines for weak monitoring, inadequate KYC, or failure to file Suspicious Activity Reports (SARs).

2024 marked a sharp surge in AML enforcement, with regulators issuing US$3.3 billion in fines across eight cases, compared to just one major fine totaling US$186 million in 2023.

Regulatory Actions

Non-compliance may result in license suspension, restrictions on business operations, or mandatory remediation programs.

Regulators can impose ongoing audits or require third-party reviews to ensure compliance standards are met.

Criminal Liability

In severe cases, executives and compliance officers may face personal liability or criminal charges for willful neglect or complicity in AML violations. Even unintentional lapses can attract scrutiny if regulators determine that controls were insufficient or poorly implemented.

Courts and enforcement bodies increasingly evaluate whether senior management exercised adequate oversight, meaning that fostering a strong compliance culture and documenting due diligence are critical defenses against potential criminal exposure.

Reputational Damage

Publicized enforcement actions can erode customer trust and investor confidence. When a payment processor or financial business is cited for AML violations, clients may question the integrity of their transactions, while investors and partners may reconsider engagement or funding.

Damage to reputation can also hinder partnerships with banks, fintech platforms, and payment networks.

Operational Disruption

Compliance failures often trigger stricter oversight and operational restrictions, slowing onboarding, transaction processing, or cross-border payments.

Increased scrutiny can also lead to higher operational costs and resource allocation to remediate gaps.

Staying proactive with identity verification, transaction monitoring, and risk-based controls helps avoid penalties, prevent operational disruption, and maintain trust across your ecosystem.

Also Read: How AI is Transforming AML Compliance

With a clear understanding of AML penalties, let’s look at how you can implement and automate AML compliance.

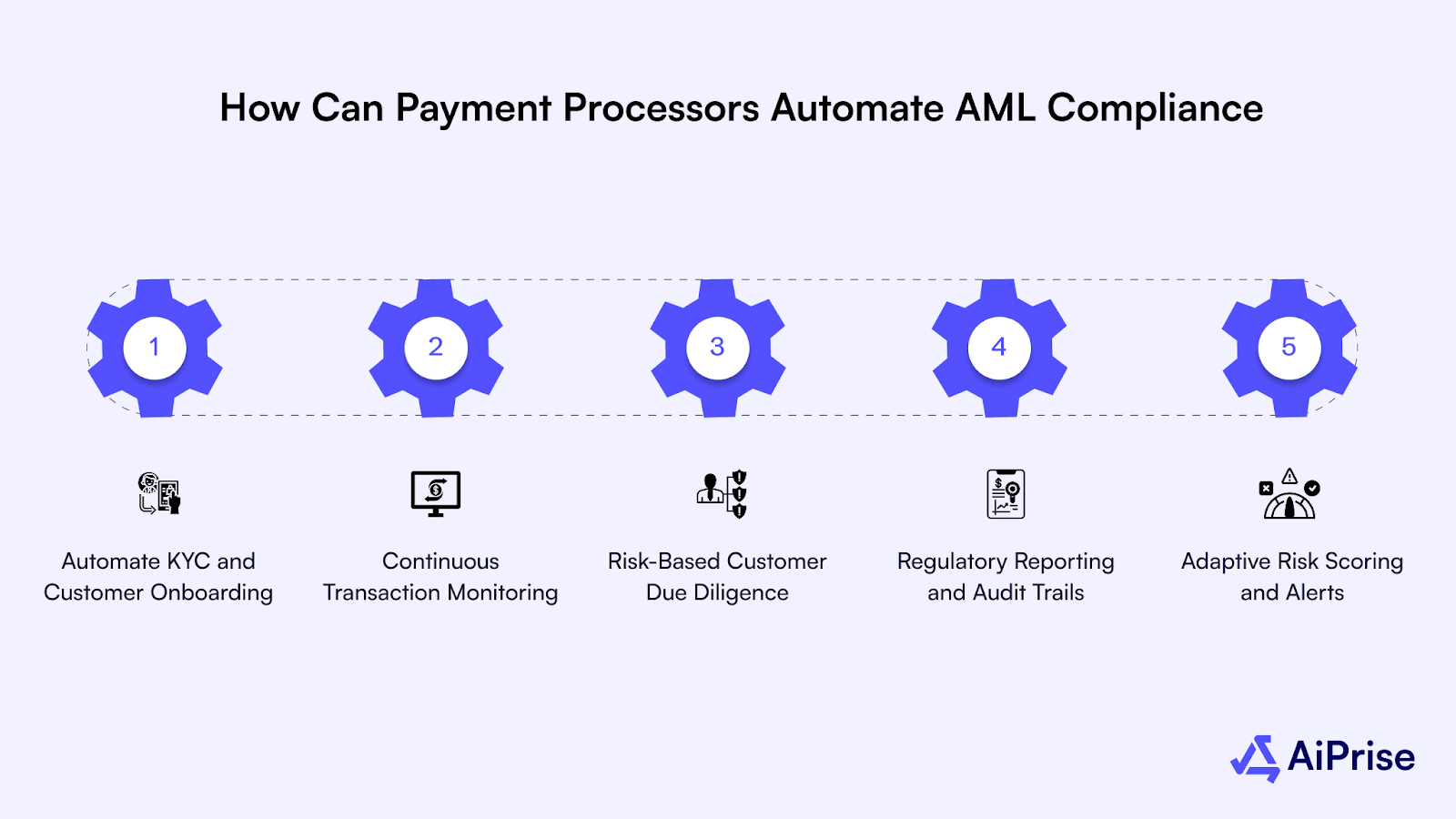

How Can Payment Processors Automate AML Compliance

As regulatory expectations grow, payment processors and financial businesses face increasing pressure to maintain strong AML compliance for payment firms without slowing operations. Automation provides a scalable solution, combining AI, machine learning, and real-time analytics to detect risk and ensure compliance.

Here’s how you can set it up:

Automate KYC and Customer Onboarding

Modern AML programs start with efficient, accurate onboarding. AI-powered identity verification tools can validate IDs, cross-check watchlists, and assess risk scores instantly.

This reduces human error and accelerates onboarding for legitimate customers. Platforms like AiPrise integrate identity verification with behavioral analysis to flag high-risk accounts even at the first interaction.

Continuous Transaction Monitoring

Automation enables real-time monitoring of payments, transfers, and account activity. Machine learning models detect anomalies such as unusual transaction volumes, patterns indicative of mule activity, or high-risk cross-border transfers.

Alerts are generated automatically for compliance teams to review, reducing false positives while ensuring suspicious activity is escalated promptly.

Risk-Based Customer Due Diligence (CDD)

Automated systems can apply tiered due diligence depending on the customer’s risk profile. High-risk accounts such as those in sensitive geographies, high-value industries, or with complex ownership structures can trigger Enhanced Due Diligence (EDD) workflows.

By combining AI-driven insights with historical data, platforms like AiPrise help teams focus resources on the highest-risk customers without slowing routine transactions.

Regulatory Reporting and Audit Trails

Automation ensures that Suspicious Activity Reports (SARs) and other compliance filings are accurate, timely, and complete.

Systems can automatically compile relevant transaction data, customer identifiers, and alerts into a report-ready format, maintaining audit trails for regulators. This reduces manual workload and ensures consistency across jurisdictions.

Adaptive Risk Scoring and Alerts

AI-driven engines continuously update risk scores based on emerging threats, transaction behaviors, and external intelligence.

Payment processors can set rules and thresholds that dynamically adjust to new fraud trends, enabling proactive compliance rather than reactive remediation.

Automating AML compliance allows payment processors to reduce operational burden, improve detection accuracy, and maintain regulatory alignment.

Now that you know how to establish AML compliance, let’s look at some of the challenges payment processors face with AML compliance and how to solve them.

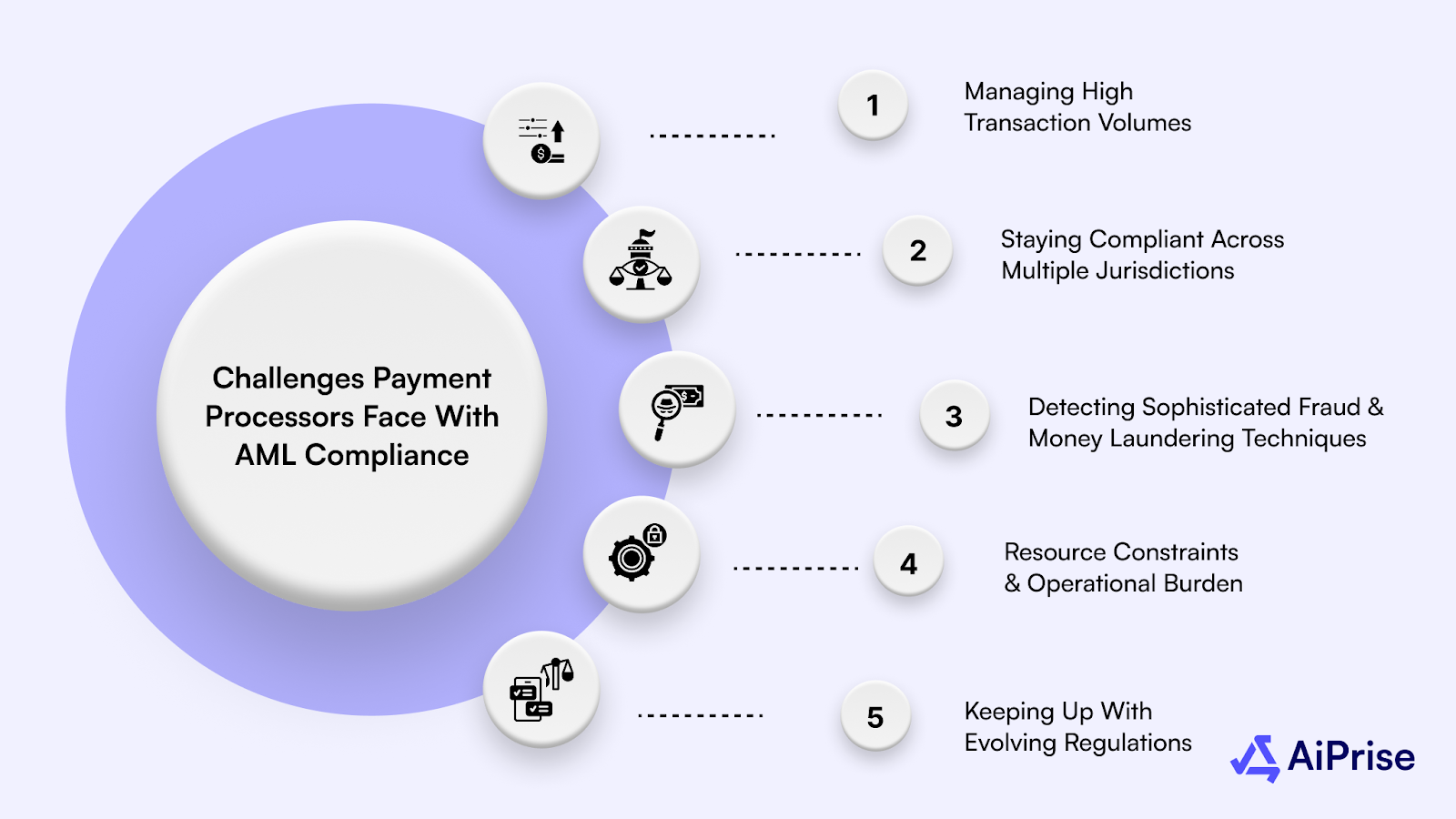

Challenges Payment Processors Face with AML Compliance

Payment processors operate in a complex regulatory landscape. While they may not be traditional financial institutions, acting as conduits for transactions exposes them to significant AML obligations.

Many firms struggle with compliance due to evolving regulations, high transaction volumes, and increasingly sophisticated fraud tactics.

Here are some of the challenges to look for:

- Managing high transaction volumes: Real-time payments, cross-border transfers, and embedded finance significantly increase transaction throughput. Manual review processes cannot scale at this pace, creating detection gaps and increasing the risk of missed suspicious activity or regulatory penalties.

- Staying compliant across multiple jurisdictions: Cross-border payment activity exposes processors to multiple AML regimes, including the Bank Secrecy Act (BSA) in the U.S., EU AML Directives, and FATF recommendations. Maintaining consistent controls, reporting standards, and policies across regions is complex and resource-intensive.

- Detecting sophisticated fraud and money laundering techniques: Criminal networks increasingly use AI-generated identities, device spoofing, layered transactions, and coordinated mule networks to bypass traditional controls. Static KYC checks and basic rule-based monitoring are no longer sufficient to identify these threats.

- Resource constraints and operational burden: Small and mid-sized payment processors often lack large compliance teams. Reviewing alerts, conducting enhanced due diligence, and maintaining audit-ready documentation can quickly overwhelm limited resources.

- Keeping up with evolving regulations: AML regulations and enforcement expectations continue to change. Delayed policy updates or outdated controls can result in non-compliance, regulatory scrutiny, and reputational damage.

Also Read: How Banks Utilize Machine Learning For Fraud Detection

Best Practices for Managing AML Compliance at Scale

To address challenges effectively, payment processors are increasingly adopting technology-driven, risk-based AML frameworks designed to scale with transaction growth and regulatory complexity.

Here are some best practices payment processors can follow:

- Automate transaction monitoring: AI-powered monitoring systems analyze transactions in real time to detect unusual patterns, velocity anomalies, and high-risk behaviors. Automated alerts enable faster investigations and reduce reliance on manual review.

- Centralize compliance across jurisdictions: Unified compliance platforms help processors manage rules, watchlists, reporting workflows, and risk scoring across regions. This ensures consistent adherence to global AML standards without slowing onboarding or payments.

- Use behavioral and device intelligence: Advanced behavioral analytics, device fingerprinting, and network-graph analysis help identify suspicious activity that traditional checks miss. These tools are critical for detecting mule activity, synthetic identities, and coordinated fraud rings.

- Reduce manual workload through automation: Automating document verification, sanctions screening, alert triage, and SAR preparation reduces operational strain. This allows compliance teams to focus on high-risk investigations and strategic oversight rather than repetitive tasks.

- Adopt adaptive risk scoring and continuous monitoring: Dynamic risk engines continuously update customer and transaction risk profiles based on behavior, geography, and emerging threats. Continuous monitoring ensures controls remain aligned with current AML requirements as regulations evolve.

Alongside these best practices, payment processors, fintechs, and banks also need systems that spot suspicious activity early, verify customer identities accurately, and flag high-risk transactions before compliance or financial risks escalate.

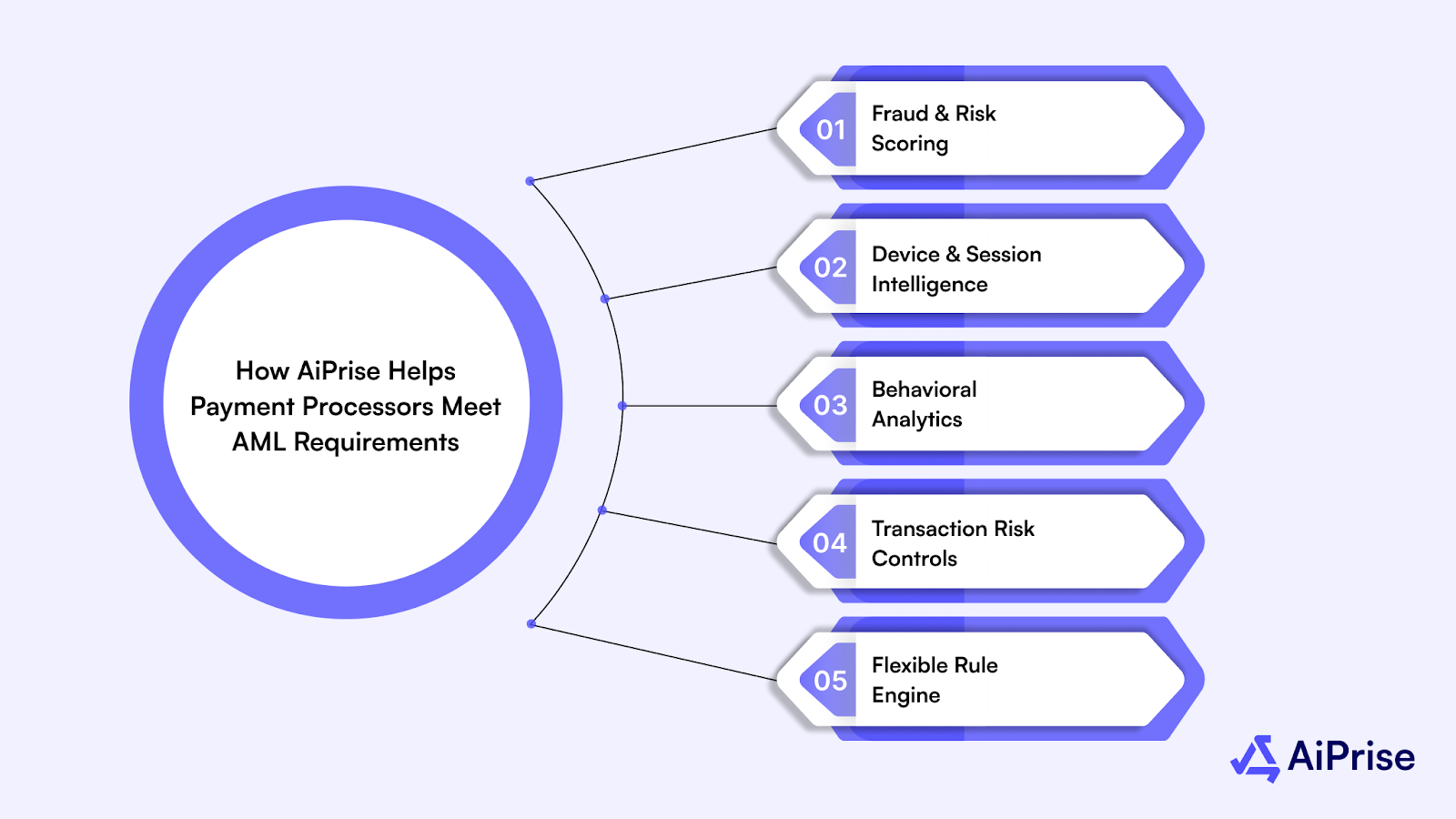

How AiPrise Helps Payment Processors Meet AML Requirements

Financial institutions, fintech platforms, and payment processors need tools that identify suspicious activity, verify customer identities reliably, and flag high-risk transactions before they escalate into regulatory issues or financial loss.

In 2026, effective AML compliance requires visibility across onboarding, devices, customer behavior, and real-time transaction flows. AiPrise unifies identity verification, behavioral analytics, and risk scoring into a single orchestration layer, giving compliance and risk teams a faster, clearer way to identify potential AML violations tied to users, payment methods, and transaction networks.

The platform enables firms to intervene early, preventing regulatory breaches, money-laundering exposure, and operational disruption.

With AiPrise, payment processors can:

- Fraud & Risk Scoring: Assess customer risk at onboarding and across the lifecycle using 100+ signals, including identity data, device info, behavior patterns, IP intelligence, corporate registries, and adverse media. This flags high-risk clients, synthetic identities, and mule activity early.

- Device & Session Intelligence: Detect compromised devices, browser spoofing, emulator use, VPN abuse, and remote-access tools often used to bypass KYC and transaction monitoring controls.

- Behavioral Analytics: Monitor session behavior, interaction patterns, and anomalies to spot social-engineering attempts, coordinated fraud rings, and suspicious user activity.

- Transaction Risk Controls: Apply transaction-level checks, including source-of-funds validation, counterparty scoring, velocity limits, cooling-off periods, circular-flow detection, and automated holds for suspicious transfers.

- Flexible Rule Engine: Configure automated workflows and detection rules aligned with AML policies, regulatory obligations, and internal risk thresholds without slowing legitimate customers.

AiPrise gives payment processors end-to-end visibility and adaptive controls across identity, behavior, devices, and transactions, helping teams meet AML requirements efficiently while keeping trusted clients moving.

Book A Demo to see how AiPrise strengthens AML compliance, reduces regulatory risk, and ensures operational resilience.

Wrapping Up

AML obligations are becoming more complex as digital payments expand, customer onboarding accelerates, and cross-border activity increases. Payment processors now face increasing pressure to verify identities thoroughly, assess customer risk accurately, and detect suspicious activity long before it reaches the banking system. For many organizations, achieving effective AML compliance for payment firms now depends on automation, continuous monitoring, and unified risk intelligence.

AiPrise delivers unified AML intelligence by combining automated KYC, customer due diligence, and continuous transaction monitoring into one platform. By uncovering risk signals early and maintaining real-time visibility across users, behaviors, and payment flows, it helps processors strengthen compliance, reduce exposure, and support safer operations with greater confidence.

Talk to Us Today to see how AiPrise helps payment processors meet AML requirements, minimize regulatory risk, and safeguard every stage of the transaction lifecycle.

FAQs

1. Do payment processors need to verify the identity of their merchants and end users?

Yes. While primary responsibility often lies with the merchant, regulators increasingly expect processors to understand both the businesses they onboard and the types of end users those businesses serve. This helps identify hidden risks like high-chargeback operations, unregistered money services, or shell merchants.

2. How often should payment processors refresh KYC information?

Refresh cycles depend on customer risk level. Low-risk merchants may require periodic reviews every one to three years, while high-risk or fast-growing businesses may need more frequent reassessments. Sudden spikes in volume or new product lines also trigger ad-hoc reviews.

3. What types of transactions typically trigger AML red flags for payment processors?

Common triggers include payments routed through multiple intermediaries, unusually high refund patterns, repeated cross-border micro-transactions, mismatches between declared business type and transaction behavior, and merchants suddenly processing far above their normal volumes.

4. Are payment processors required to maintain an AML officer or a dedicated compliance team?

Most jurisdictions expect processors to appoint a designated AML officer responsible for policy oversight, SAR/STR filing, staff training, and ensuring systems meet regulatory standards. Even smaller processors must show clear ownership of compliance functions. This role is a core part of the compliance responsibilities of payment processors, even for smaller or fast-growing payment platforms.

5. How can payment processors demonstrate AML compliance during audits or bank partner reviews?

Clear documentation is essential. Processors should maintain evidence of KYC procedures, monitoring rules, investigation logs, SAR filings, risk assessments, and automated controls. Many firms use platforms like AiPrise to centralize these records and provide audit-ready reporting.

You might want to read these...

AiPrise

11 mins read

How Compliance Copilot is Revolutionizing Risk Management and Compliance Monitoring

Discover how Compliance Copilot, an AI-powered platform, is transforming risk management and compliance monitoring. Learn how it proactively detects risks, automates tasks, and keeps businesses compliant with real-time regulatory updates across global jurisdictions

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately