AiPrise

Loading...

January 7, 2026

AML Nigeria: A Practical Compliance Guide For Businesses

Key Takeaways

How prepared is your business to tackle money laundering risks in Nigeria? Between 2018 and 2023, the country’s risk index for money laundering and terrorist financing hovered around 6.9 points, highlighting the persistent threat.

Are your current controls enough to detect suspicious transactions and meet regulatory expectations? Falling behind in AML compliance can lead to regulatory fines, reputational damage, and operational disruptions. At the same time, overly strict checks may frustrate customers and slow growth. And striking the right balance is no easy task.

That’s why this blog guides you through AML Nigeria regulations, explaining key requirements and obligations for your business. Stick around till the end for a practical checklist to ensure full compliance.

Key Takeaways:

- Nigeria’s AML legal framework consists of the MLPA, CBN guidelines, EFCC, and NFIU oversight requirements.

- Key AML elements focus on customer due diligence, reporting suspicious transactions, maintaining records, and staff training.

- Non-compliance can lead to fines, license revocation, criminal prosecution, and reputational damage for businesses.

- Common challenges include weak enforcement, limited resources, complex transactions, and insufficient staff awareness.

- Best practices emphasize risk-based strategies, technology-driven monitoring, thorough training, and strong internal controls for compliance.

Nigerian AML Legal And Regulatory Framework

Nigeria’s fight against financial crime relies on a mix of laws, regulators, and enforcement bodies that work together to monitor suspicious activity. If you want a solid compliance program, you first need to understand the rules that shape AML Nigeria obligations.

Here is a clear breakdown to guide you:

Money Laundering (Prohibition) Act

This is the main law that outlines how institutions should detect and prevent money laundering. It shapes most verification and reporting duties.

Key requirements include:

- Conducting identity checks for all customers.

- Reporting suspicious activity to the NFIU.

- Performing risk assessments for high-risk clients.

- Applying penalties for aiding or ignoring laundering activity.

Terrorism (Prevention) Act

This law focuses on stopping the movement of funds linked to terrorism. It supports national and global security efforts.

Key requirements include:

- Reporting transactions tied to suspected terrorism financing.

- Freezing assets when directed by authorities.

- Verifying customers linked to sensitive sectors or jurisdictions.

Central Bank of Nigeria Guidance

The CBN sets operational rules for institutions that manage financial activity. These rules push organizations to maintain strong controls.

Key requirements include:

- Adopting risk-based onboarding procedures.

- Updating KYC for all active customers.

- Screening transactions across the customer lifecycle.

- Keeping clear records for audits and compliance reviews.

Nigerian Financial Intelligence Unit

The NFIU reviews suspicious activity reports and passes intelligence to law enforcement. It sits at the center of Nigeria’s AML reporting process.

Key responsibilities include:

- Collecting and reviewing suspicious transactions.

- Sharing intelligence with domestic and global partners.

- Supporting complex investigations with data insights.

Economic and Financial Crimes Commission

The EFCC handles major enforcement activities. It investigates, prosecutes, and disrupts financial crime networks.

Key responsibilities include:

- Pursuing money laundering and fraud cases.

- Working with the NFIU on investigations.

- Leading high-value, high-risk financial crime probes.

With the legal structure in place, your next step is understanding the core elements that make an AML program work every day.

Also Read: Methods for Effective Money Laundering Detection

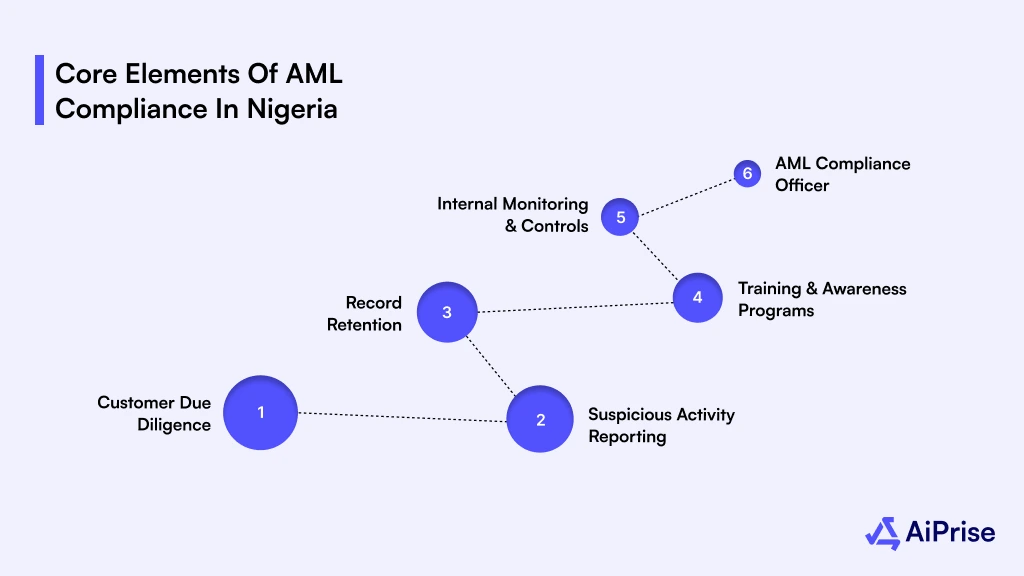

Core Elements Of AML Compliance In Nigeria

Staying compliant with AML Nigeria laws isn’t about “ticking regulatory boxes,” but about building a system that detects risks before they escalate into serious issues. And while the rulebook feels long, the day-to-day compliance structure actually comes down to a few core pillars every institution must get right.

Customer Due Diligence

CDD starts the moment someone tries to open an account. It helps you confirm identities, understand a customer’s background, and gauge how risky their activity might be.

CDD usually involves:

- Verifying identity documents from reliable sources

- Running background checks to understand behavioral patterns

- Assigning a risk category based on customer type and activity

- Applying enhanced checks for PEPs and other high-risk users

Quick note: High-risk customers require more than basic verification; institutions must understand their source of funds and expected activity patterns.

Suspicious Activity Reporting

Once an activity looks unusual, you must determine if it has a legitimate explanation. If not, an STR should go to the NFIU within seven days. Common triggers:

- Transaction sizes or volumes that do not match the customer profile

- Unusual cash activity with no clear business purpose

- Sudden cross-border transfers without supporting documentation

Record Retention

Every transaction tells a story, and regulators expect you to keep those details. Good records support investigations and help protect your institution.

You should store:

- Identification documents

- Account opening forms

- Transaction logs and receipts

- Communication and approval trails

Remember: Regulators expect these records to be accessible quickly during audits or investigations.

Training and Awareness Programs

Compliance is only as strong as the people running it. Regular training helps your staff catch risks earlier and report them correctly.

Training should cover:

- Real-world examples

- Clearly defined reporting responsibilities

- Refreshed staff knowledge at regular intervals

- Red flags for specific products or channels

Internal Monitoring and Controls

Controls and monitoring systems help you catch activity patterns that humans may miss. These systems reduce error and improve response time.

Effective monitoring involves:

- Automated systems for unusual transaction alerts

- Review cycles for high-risk accounts

- A clear escalation path for suspicious activities

- Oversight by a qualified AML Compliance Officer

AML Compliance Officer

You also need someone who owns the full program. The AMLCO guides risk assessments, ensures reporting accuracy, and reviews operational processes. This role works best with clear authority and access to senior leadership.

With the core elements in place, it is time to look at what happens when you ignore or delay AML responsibilities.

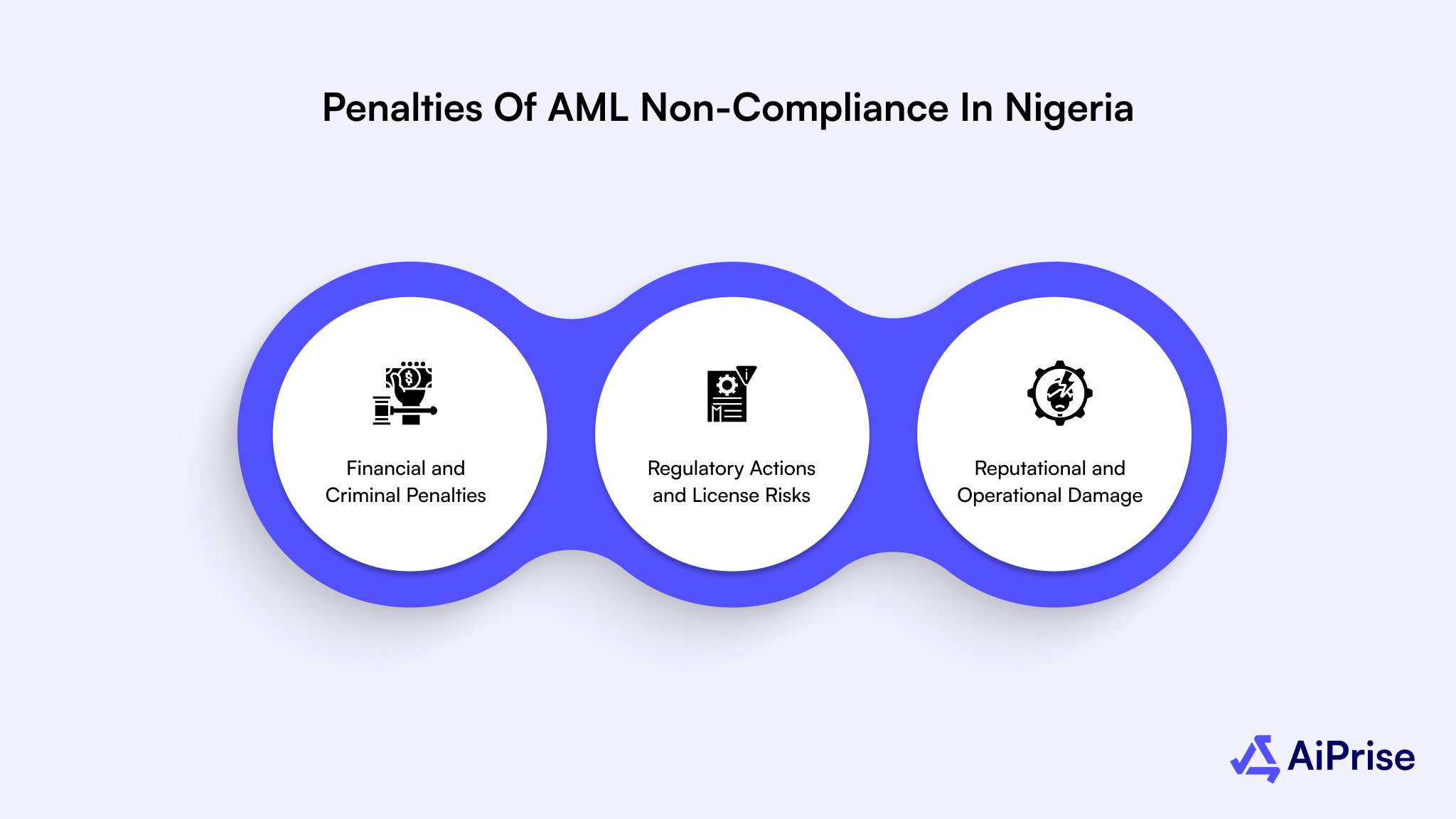

Penalties Of AML Non-Compliance In Nigeria

Non-compliance comes with more than financial risk. Regulators take violations seriously, and failing to do so can quickly escalate into penalties that disrupt your operations and damage customer trust.

Financial and Criminal Penalties

- Regulators can impose heavy fines when institutions skip required controls or ignore reporting duties. These penalties often scale based on the severity and frequency of violations.

- Beyond fines, individuals involved in willful breaches may also face criminal prosecution. This includes possible imprisonment for enabling, ignoring, or participating in money laundering activities.

Regulatory Actions and License Risks

- When non-compliance becomes systemic, regulators may suspend or revoke a company’s license. This affects banks, fintechs, payment platforms, and any business operating under a regulated framework.

- Such actions also trigger enhanced audits and supervisory reviews. Institutions may be required to overhaul their entire compliance program before resuming full operations.

Reputational and Operational Damage

- Public exposure of AML violations can erode customer trust and make investors hesitant to engage. Once reputational damage starts, rebuilding credibility often takes years.

- Operationally, the business may face increased scrutiny, onboarding delays, or loss of key partnerships. These disruptions reduce market confidence and weaken long-term growth prospects.

When the stakes are this high, even minor misses can hit hard. So what exactly makes AML compliance tough in Nigeria? Let’s dig into the core challenges.

Also Read: Understanding The Five Pillars Of An AML Compliance Program

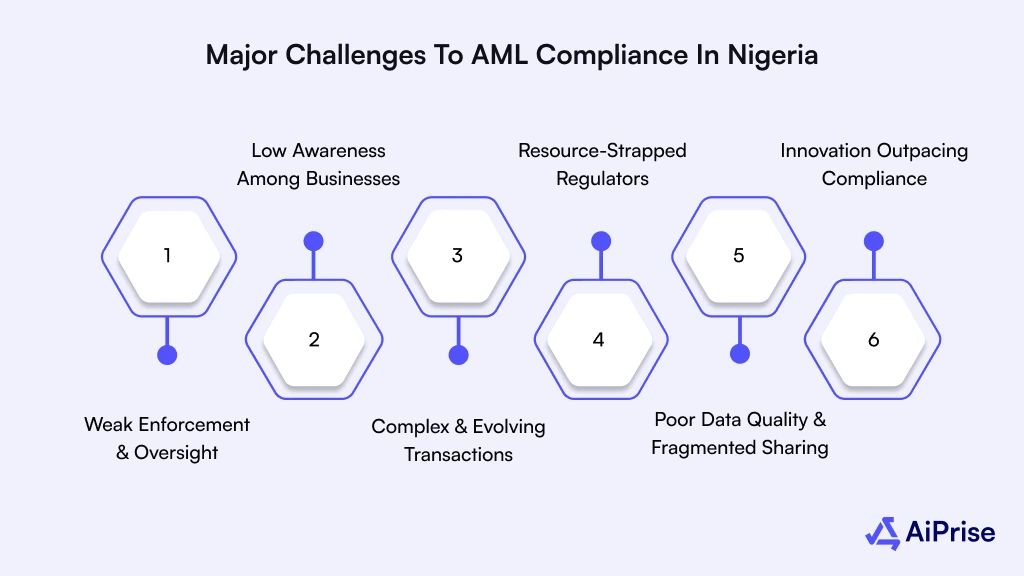

Major Challenges To AML Compliance In Nigeria

Even with strong regulations, Nigerian institutions still face pressure when trying to meet AML Nigeria expectations. These challenges often drain resources and slow down decision-making. Here are the key issues:

- Weak Enforcement & Oversight: Enforcement remains inconsistent due to corruption, slow processes, and limited accountability. This weakens deterrence and creates gaps between regulation and reality.

- Low Awareness Among Businesses: Many organisations, especially SMEs and informal-sector players, don’t fully understand AML rules. Without training, teams easily miss risks or make avoidable compliance mistakes.

- Complex and Evolving Transactions: Digital payments, crypto, and cross-border flows make suspicious activity harder to spot. Criminals use these channels to hide patterns and exploit system blind spots.

- Resource-Strapped Regulators: Agencies often operate with limited staff, outdated tools, and constrained budgets. This slows investigations and reduces overall enforcement capacity.

- Poor Data Quality & Fragmented Sharing: Incomplete KYC records and inconsistent reporting formats break visibility across channels. Weak data makes risk detection slower and less accurate.

- Fast Innovation Outrunning Compliance: Fintech growth moves faster than many compliance teams can adapt. New risks emerge before systems and processes are ready to manage them.

Wondering how you can stay compliant when these challenges keep shifting? That’s when you turn to practical AML best practices.

Struggling to keep up with complex AML Nigeria requirements and rising false positives? AiPrise helps you detect real risks faster, streamline KYC/KYB checks, and stay compliant without slowing your operations.

AML Best Practices For Nigerian Businesses

To strengthen your AML controls, you need practical methods that fit your risk profile. Here are strategies that help you stay ready as requirements grow:

Strong, Tailored AML Program

A solid AML program starts with understanding your business risks and creating controls that match them. Generic programs rarely catch evolving threats, so specificity is key.

- Tip: Conduct regular risk assessments and update your AML program to reflect your institution’s unique customer and transaction profiles.

Risk-Based Strategies with Technology Support

Prioritize resources where the risk is highest using technology. AI and machine learning can help detect suspicious activities faster and reduce false positives.

- Tip: Implement risk-scoring models and automated transaction monitoring to focus efforts on high-risk customers and transactions.

Ongoing Training and Practical Awareness

Staff awareness is critical to spotting red flags early. Short, frequent sessions keep staff alert, informed, and ready to act when something looks off.

- Tip: Run role-specific AML training twice a year so every department knows the red flags that apply to their daily work.

Also Read: Anti Money Laundering and Procurement Risk in Insurance Sector

AML Compliance Checklist For Financial Institutions

Use this table as a quick audit tool for your compliance program and identify areas that need attention:

Streamline AML Nigeria Compliance With AiPrise Solutions

Maintaining strong AML Nigeria compliance requires more than checking boxes. Financial institutions need real-time insights into customer and business activities, seamless risk detection, and clear audit trails. AiPrise combines these capabilities into a single, unified platform, helping teams prevent fraud, monitor transactions, and meet regulatory obligations with confidence.

Core features that support compliance:

- Global KYC / KYB Coverage: Verify customers and businesses worldwide, including local documents, to strengthen AML Nigeria compliance and reduce onboarding risks.

- Watchlist Screening: Screen against 5,000+ global and local lists, minimizing false positives while prioritizing high-risk AML transactions efficiently.

- Government Verifications: Authenticate users using official registries, maintain clear, auditable records, and stay aligned with AML regulatory requirements.

- Risk-Based Decisioning: Apply dynamic scoring and custom rules to identify high-risk transactions and customers, enhancing AML monitoring and prevention efforts.

- Compliance Co-Pilot: Use AI-powered tools for EDD report generation, document analysis, and faster reviews to support effective AML programs.

With AiPrise, your AML program becomes more reliable, efficient, and aligned with regulatory expectations.

Final Thoughts

Compliance with AML Nigeria isn’t just about following rules, but about building trust and protecting your business from financial crime. Strong systems help detect suspicious activity before it escalates.

Many institutions struggle with complex transactions, evolving regulations, and operational gaps. Implementing structured programs and ongoing staff training can significantly reduce risk exposure.

For smoother, more efficient compliance, AiPrise helps streamline screening, monitoring, and reporting. Book A Demo today to enhance detection, reduce risks, and strengthen your AML program.

FAQs

1. What is AML in Nigeria?

AML in Nigeria sets guidelines for financial institutions to prevent money laundering and terrorist financing. These regulations are enforced under the Central Bank of Nigeria (CBN) to ensure compliance.

2. Is Nigeria a high-risk country in AML?

Nigeria was previously flagged for strategic AML deficiencies but is no longer on the FATF high-risk list. The country continues to strengthen its compliance framework to meet international standards.

3. Why is money laundering a problem in Nigeria?

Illicit funds distort economic indicators, complicating government policy and planning. They also reduce tax revenue and deprive the country of vital financial resources.

4. What are the types of money laundering in Nigeria?

The main types are placement, layering, and integration. These often involve cash deposits, real estate, shell companies, or digital platforms to disguise illicit funds.

You might want to read these...

AiPrise

11 mins read

How Compliance Copilot is Revolutionizing Risk Management and Compliance Monitoring

Discover how Compliance Copilot, an AI-powered platform, is transforming risk management and compliance monitoring. Learn how it proactively detects risks, automates tasks, and keeps businesses compliant with real-time regulatory updates across global jurisdictions

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately