AiPrise

11 min read

January 7, 2026

AML Oman Guide: Key Regulations And Compliance Steps

Key Takeaways

Keeping up with financial crime risks is getting harder every year. New customer behaviors, faster payment channels, and cross-border activity often push your team to react instead of plan. Have you ever felt that your controls should work better, even when you follow every rule?

You are not alone. Many regulated businesses in Oman face growing pressure to detect threats early while still delivering a smooth user experience. Missing a red flag can hurt your reputation, but tightening checks too much can slow customer growth. How do you strike the right balance without overwhelming your compliance team?

This blog walks you through the key AML Oman requirements and what they mean for your business. You’ll find the core rules, key obligations, sector-specific duties, and smart strategies to build a reliable compliance program. Let’s dive in.

Quick Look:

- Oman’s AML framework is shaped by Royal Decree 30/2016, CBO rules, CMA guidelines, and NCFI oversight.

- Core AML elements include KYC, monitoring, reporting duties, and strong risk assessment processes.

- Non-compliance can lead to heavy financial penalties and serious regulatory action against institutions.

- Businesses must follow clear onboarding, screening, monitoring, and reporting controls to stay compliant.

- Strong AML strategies focus on risk assessments, technology adoption, accurate UBO checks, and leadership-driven compliance.

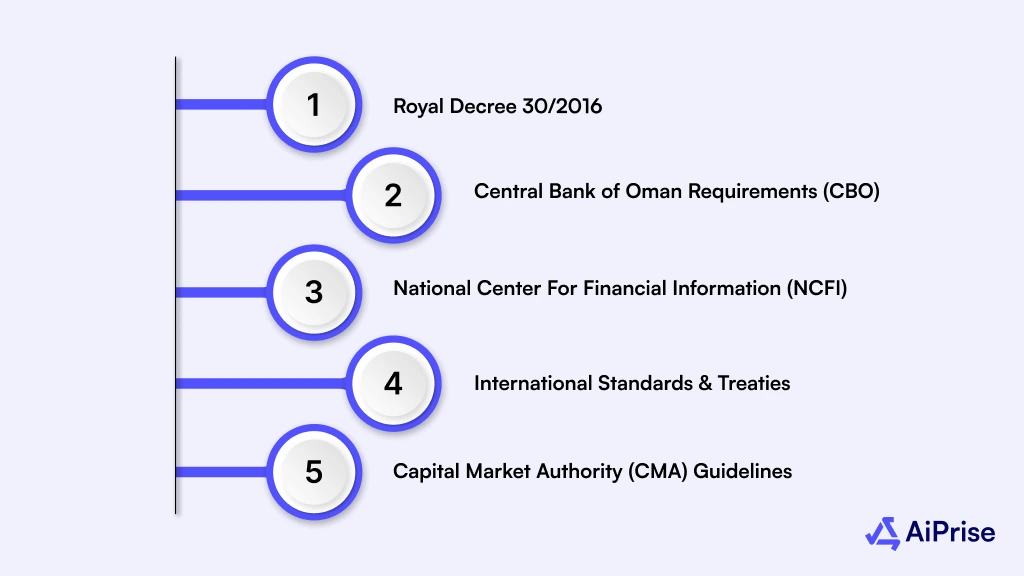

Key Legal And Regulatory AML Foundations

Before you build an effective compliance program, you need a clear view of the rules that guide AML Oman requirements. These laws shape the way you verify customers, monitor activity, and respond to suspicious behavior. Below are the core regulations that influence your daily compliance decisions:

Royal Decree 30/2016

This decree defines money laundering, outlines penalties, and sets your core duties. It applies to financial institutions and several non-financial sectors.

- Criminalization of money laundering and terrorism financing

- Mandatory customer verification and updated record keeping

- Required suspicious activity reporting to the NCFI

- Power to freeze or confiscate assets tied to illegal activity

Central Bank of Oman Requirements (CBO)

The Central Bank issues detailed rules for banks, payments firms, money exchange providers, and similar entities. These rules guide your day-to-day compliance program.

- Appointment of a Money Laundering Reporting Officer

- Regular audits and documented risk assessments

- Screening during onboarding and throughout customer lifecycles

- Strong monitoring workflows for high-risk activity

National Center For Financial Information (NCFI)

The NCFI acts as Oman’s Financial Intelligence Unit and receives all suspicious activity reports. It works with regulators and foreign FIUs during investigations.

- Reviewing and analyzing suspicious transaction reports

- Sharing intelligence with domestic and global partners

- Maintaining operational independence to protect case data

International Standards and Treaties

Oman follows global AML expectations, which influence your internal policies and screening steps.

- Meeting FATF recommendations for customer verification and reporting

- Following UN Security Council instructions tied to terrorism financing

- Freezing assets of sanctioned persons when required

Capital Market Authority (CMA) Guidelines

The CMA provides sector-level guidance for businesses operating in Oman’s securities and investment space.

- Specific instructions for securities and investment entities

- Clear responsibilities for customer due diligence

- Mandatory reporting of suspicious activity to the NCFI

- Requirements for proper documentation and internal controls

With these rules in mind, you now have a clearer view of the legal base that shapes compliance.

Next, let’s move into the core elements that help you build a practical AML program.

Core Elements Of AML Compliance In Oman

Once you understand the laws behind the system, you may wonder how these rules translate into your daily responsibilities. These elements guide how you manage risk, verify customers, and report unusual behavior under AML Oman requirements.

RBA: Risk-Based Approach

You start with a clear view of where your risks come from. This helps you assign the right controls to the right areas.

- Identify customer, product, and geographic risks.

- Prioritize high-risk transactions and profiles.

- Review and update assessments at set intervals.

CDD/EDD: Customer Due Diligence

You verify customers before you establish or maintain a relationship. When risk increases, you apply additional checks.

- Collect and validate identity documents.

- Confirm beneficial ownership details for businesses.

- Conduct deeper checks for high-risk clients, including source-of-funds reviews.

STR: Suspicious Transaction Reporting

When activity looks unusual, you escalate and document it promptly. This is one of your most important duties.

- Report transactions that do not match known customer behavior.

- Avoid any action that alerts the customer.

- Send reports to the NCFI without unnecessary delays.

RK: Record Keeping

Your records help investigators trace activity and confirm customer details. Regulators expect consistent documentation.

- Keep identification documents, business profiles, and onboarding details.

- Store transaction data and internal review logs.

- Maintain records for a minimum of ten years.

TC: Training and Internal Controls

You strengthen your program by training employees who interact with customers or handle high-risk tasks.

- Provide recurring training across customer-facing and compliance teams.

- Assign a responsible MLRO to manage reporting and controls.

- Conduct internal audits to test program effectiveness.

While these core AML elements apply across industries, how each business implements them can vary significantly. This is where sector-specific obligations come into play.

Also Read: 6 Key Components of Anti Money Laundering Compliance Checklist

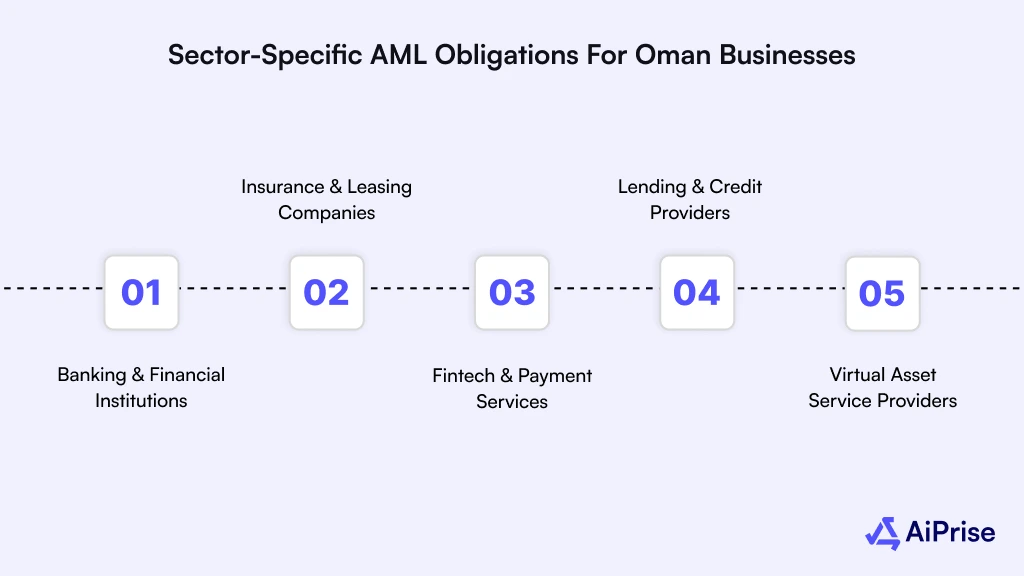

Sector-Specific AML Obligations For Oman Businesses

Different industries in Oman face unique risks, so your duties go beyond general requirements. You need to shape your program around how customers use your services, how funds move, and where the biggest risks appear.

Here’s a quick breakdown of what each industry needs to focus on:

1. Banking and Financial Institutions

Banks manage broad customer segments and high-volume transactions, which increases exposure to suspicious behavior and cross-border risks. Your obligations include:

- Enhanced due diligence for high-risk customers like PEPs, offshore entities, or clients transacting at unusually high frequencies.

- Ongoing transaction surveillance using automated monitoring to detect unusual patterns.

- Cross-border transfer scrutiny, especially when dealing with high-risk jurisdictions.

- Mandatory STR filing when transactions lack economic rationale.

Example: A client suddenly starts sending repeated overseas transfers to new regions. You review the transactions, document your findings, and file an STR after confirming inconsistencies.

2. Insurance & Leasing Companies

Insurers face risks tied to irregular claim activity and premium movements that may hide illicit funds. Your obligations include:

- Risk-based onboarding checks for policyholders, especially for investment-linked or high-value policies.

- Beneficiary verification to prevent policies from being used to hide ownership of illicit funds.

- Monitoring for early policy cancellations, a known ML tactic to convert illicit money into “clean” refunds.

- Watch for unusual premium payments, such as lump-sum cash deposits.

Example: A new customer files a high-value claim within days of buying a policy. You investigate the claim history, confirm red flags, and escalate it to compliance for reporting.

3. Fintech and Payment Services

Fintech platforms process fast, high-volume transactions that can mask structured or coordinated activities. Your obligations include:

- Digital KYC checks that confirm identity before allowing transactions.

- Real-time monitoring to detect rapid-fire payments or sudden volume spikes.

- Screening for transfers involving sanctioned regions or risky sources.

- Reporting activity that shows possible structuring or mule account use.

Example: A user sends dozens of small payments within minutes. You pause unusual activity, run enhanced checks, and escalate the behavior as potential structuring.

4. Lending and Credit Providers

Lenders face risks from false applications, income misrepresentation, and unusual repayment behaviors. Your obligations include:

- Identity and financial verification before credit approval.

- Review of repayment patterns to catch unexplained or sudden cash deposits.

- Checks for loan stacking or multiple simultaneous applications.

- Reporting repayment patterns that appear inconsistent or suspicious.

Example: A borrower repays a loan quickly through multiple cash deposits. You verify the source of funds, identify gaps, and report the activity as suspicious.

5. Virtual Asset Service Providers (VASPs)

VASPs manage fast digital transfers that may involve anonymous wallets or complex movement patterns. Your obligations include:

- Verification of wallet owners before enabling transactions.

- Blockchain monitoring to detect rapid, high-risk, or layered transfers.

- Screening for wallet addresses linked to sanctions or illicit activity.

- Reporting digital activity that suggests mixing, layering, or unusual flows.

Example: A customer receives crypto from several unfamiliar wallets within minutes. You trace the transactions, confirm risk indicators, and file a report.

Penalties Of AML Non-Compliance

Ignoring AML Oman requirements can push businesses into serious trouble. Regulators expect firms to maintain strong controls, update internal systems, and respond quickly to unusual activity. When these expectations are not met, the consequences can be costly and long-lasting.

Below is a clear breakdown of what non-compliance can invite:

Key Penalties You Should Know:

- Heavy fines that may range from moderate amounts to penalties reaching OMR 500,000 based on the violation.

- Imprisonment for individuals who intentionally assist in money laundering or ignore critical duties.

- License suspension or full revocation for entities that repeatedly fail to meet regulatory obligations.

- Asset seizure or freezing when funds or property are linked to suspicious activity.

- Management-level consequences, including the disqualification of directors or compliance officers involved in breaches.

- Public disclosures that may harm credibility and affect long-term business prospects.

- Administrative actions, such as written warnings, follow-up inspections, or increased scrutiny.

As you can see, the impact goes far beyond fines. So can you stay on the right side of compliance? Let’s see.

Also Read: Understanding The Five Pillars Of An AML Compliance Program

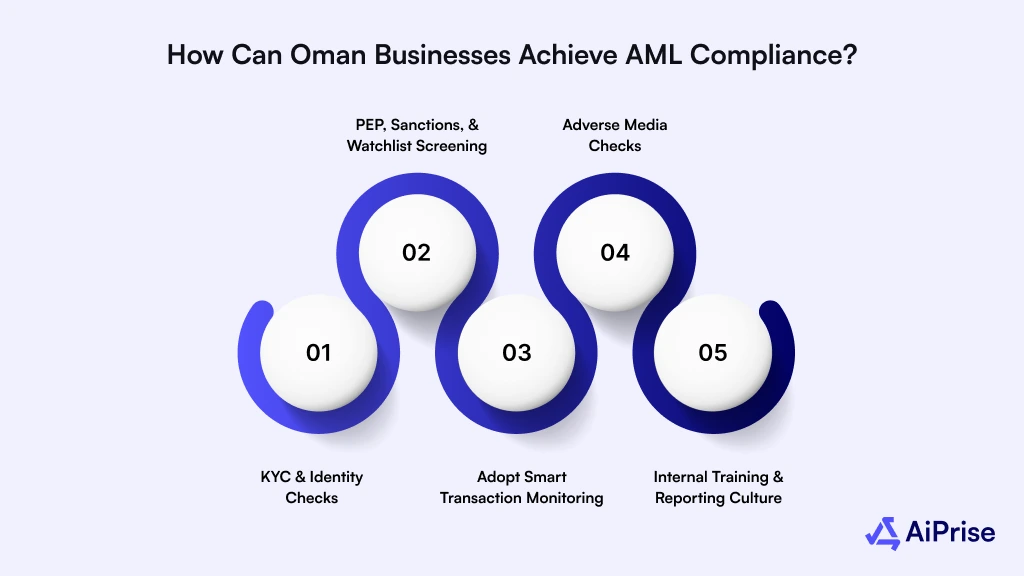

How Can Oman Businesses Achieve AML Compliance?

Creating a strong compliance program isn’t about copying regulations word-for-word. You need to design controls that actually work in your business model. Here’s how organizations can approach compliance the smart way:

Know Your Customer (KYC) and Identity Checks

You need to know exactly who you’re dealing with.

- Capture and verify customer identity documents.

- Validate the purpose of the relationship.

- Assign a risk level to each customer.

- Apply enhanced due diligence to high-risk profiles.

- Understanding customers’ business activities and expected transaction behavior.

Quick Tip: Use digital onboarding tools that automate ID verification to reduce human error and accelerate customer screening.

PEP, Sanctions, and Watchlist Screening

Keep customers and partners away from restricted lists.

- Screen against global and regional sanctions lists during onboarding.

- Re-check customers on a regular schedule.

- Monitor for sudden status changes like new PEP designations.

Adopt Smart Transaction Monitoring

A simple view of what effective monitoring looks like:

Adverse Media Checks

Early risk signals often appear in news or online sources before regulators intervene.

- Use structured tools to scan global sources, not just simple online searches.

- Look for fraud allegations, criminal investigations, or regulatory actions.

- Track negative media involving key individuals or entities.

Internal Training and Reporting Culture

A compliance program works only when your team understands how to spot red flags.

- Train staff on AML red flags and reporting steps.

- Promote internal reporting without fear.

- Make policies easy to understand and readily available.

Now that you know what strong compliance looks like, let’s talk about the challenges that you might encounter.

Looking for a simpler way to stay compliant without adding more manual work? AiPrise helps you automate KYC, run powerful watchlist checks, and cut false positives with AI so your team can focus on real risks.

What Challenges Hinder AML Compliance?

Even with clear guidelines, many companies still struggle to meet AML Oman requirements. These issues usually arise from operational gaps rather than intent.

Common Challenges

- Outdated systems that cannot detect real-time suspicious activity.

- Manual checks that slow down investigations and increase human error.

- High false-positive alerts that consume time and distract teams from real threats.

- Inconsistent data inputs across different branches, platforms, or departments.

- Limited compliance staff, especially in small to mid-sized companies.

- Poor integration between onboarding systems and monitoring tools.

- Insufficient cross-border visibility, particularly for businesses dealing with international clients.

With these barriers in mind, financial institutions need structured, long-term strategies to stay compliant and efficient.

Also Read: Comprehensive Guide to AML Transaction Monitoring Scenarios

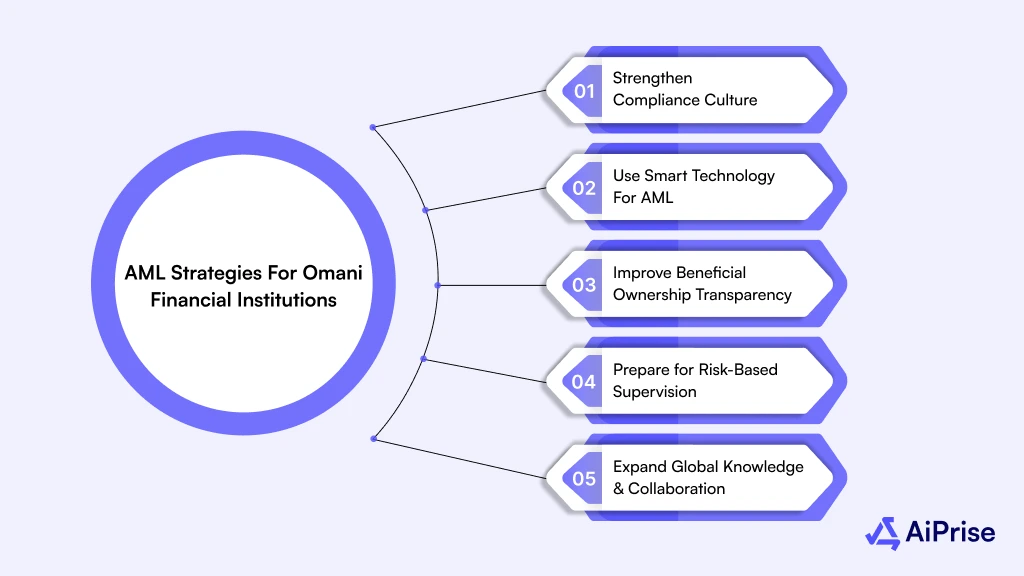

AML Strategies For Omani Financial Institutions

Since banks and financial service providers face higher scrutiny, their AML strategy must be stronger, clearer, and more agile. This section breaks down how your institution can build a future-ready approach to financial crime prevention:

Strengthen Compliance Culture

- Encourage leadership teams to set clear expectations.

- Align daily operations with compliance objectives.

- Allow employees to submit concerns anonymously.

- Review policies regularly so they stay relevant.

Use Smart Technology For AML

- Use automated transaction monitoring tools.

- Implement machine learning systems that reduce false positives.

- Integrate e-KYC for smoother onboarding.

- Connect monitoring tools across all customer touchpoints.

Improve Beneficial Ownership Transparency

- Maintain updated records for all beneficial owners.

- Request supporting documents to verify identities.

- Compare customer-provided data with trusted external sources.

- Flag unusual ownership structures or frequent changes.

Prepare for Risk-Based Supervision

- Conduct independent AML audits.

- Maintain a documented risk appetite statement.

- Implement remediation plans for identified gaps.

- Align risk scoring models with CBO expectations.

Expand Global Knowledge and Collaboration

- Join workshops and events hosted by MENAFATF or similar bodies.

- Learn from regional control failures and success cases.

- Stay aligned with global correspondent banking expectations.

Together, these strategies help you build a stronger AML program that stays aligned with Oman’s evolving expectations.

How Aiprise Supports Smarter AML Compliance In Oman

Staying compliant with AML Oman regulations is getting tougher, especially with evolving risks and complex verification requirements. But staying ahead of these requirements doesn’t have to slow down your operations.

AiPrise helps businesses stay compliant while maintaining smooth customer experiences. The platform integrates identity verification, fraud detection, and ongoing monitoring in one platform.

How AiPrise supports compliance:

- Global KYC/KYB Coverage: Verify both individuals and businesses across 200+ countries using trusted local and international data sources.

- Watchlist Screening: AiPrise’s AI reduces false positives, saving each analyst 20+ hours monthly and focusing on legitimate alerts.

- Government Verifications: Maintain compliance with regional AML and KYC regulations, with clear, auditable records for all acceptance decisions.

- Risk-Based Decisioning: Assign risk scores, apply enhanced due diligence to high-risk clients, and implement custom rules to prevent fraud and suspicious activity.

- Continuous Monitoring: Automated ongoing monitoring detects PEPs, sanctions, and unusual behavior, allowing your compliance team to respond quickly and stay ahead of potential risks.

- AI-Powered Compliance Co-Pilot: Use AI to analyze large documents, generate EDD reports, and reduce manual review time, boosting efficiency and accuracy in compliance workflows.

- Customizable Onboarding Flow: Design onboarding journeys to match your business needs while maintaining regulatory compliance and reducing friction for legitimate customers.

Aiprise helps teams stay compliant, reduce risk and build trust with a smoother AML experience.

Wrapping Up

Meeting AML Oman requirements takes steady effort, strong internal controls, and the right tools to support your team. When you understand the regulations and build processes that match your business model, you reduce risk and improve the way you manage customers and transactions. The goal is not just compliance but long-term trust with partners and regulators.

If you want smarter ways to handle verification and screening, AiPrise can help. You get fast KYC, strong watchlist checks, and reliable monitoring in one platform. Book A Demo to see how it fits your workflow.

FAQs

1. Is Oman a high-risk country for AML?

Oman faces notable money laundering and terrorist financing risks due to cross-border activity, regional instability, and its largely cash-driven economy. However, the country continues to strengthen its controls to address these vulnerabilities.

2. Is Oman a sanctioned country?

No. Oman is not subject to any international sanctions, although businesses must still conduct screening as part of standard compliance practices.

3. Is Oman a FATF member?

Oman is a member of MENAFATF and also part of the Gulf Cooperation Council, which collectively aligns it with FATF standards and international AML expectations.

You might want to read these...

AiPrise

11 mins read

How Compliance Copilot is Revolutionizing Risk Management and Compliance Monitoring

Discover how Compliance Copilot, an AI-powered platform, is transforming risk management and compliance monitoring. Learn how it proactively detects risks, automates tasks, and keeps businesses compliant with real-time regulatory updates across global jurisdictions

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately