AiPrise

8 min read

January 8, 2026

What GENIUS Act Stablecoin Compliance Requirements Mean for Issuers

Key Takeaways

Stablecoin issuance in the US is no longer just a product decision, as the GENIUS Act stablecoin compliance requirements now directly affect licensing, reserves, disclosures, and how you operate at scale. For payment-focused stablecoin issuers, regulatory uncertainty creates real pain points, including delayed launches, banking friction, rising compliance costs, and growing risk of enforcement or loss of market trust.

Many teams struggle to translate legal language into operational decisions, making it harder to design reserve strategies, reporting processes, and AML controls that regulators will actually accept. Understanding the GENIUS Act requirements clearly helps reduce risk, plan compliant growth, and build issuer confidence before regulators, partners, and customers at long-term scale.

At a Glance

- The GENIUS Act introduces clear US rules for stablecoin issuers covering licensing, reserves, audits, disclosures, and financial crime controls.

- Payment-focused stablecoin issuers targeting US users must comply, including offshore entities offering redemption or settlement services.

- Issuers must maintain one-to-one, liquid reserves, undergo regular audits, and meet ongoing reporting and transparency obligations.

- Stablecoin issuance now requires bank-grade AML, KYC, transaction monitoring, and operational controls embedded into daily workflows.

What is the GENIUS Act?

The GENIUS Act is a proposed US federal framework designed to regulate stablecoin issuers by setting clear rules around licensing, reserve backing, transparency, and ongoing oversight. It aims to close regulatory gaps by treating payment-focused stablecoins more like financial instruments, rather than unregulated crypto products.

For stablecoin issuers, the Act defines what compliant issuance looks like and removes ambiguity that previously increased operational and enforcement risk.

Why the GENIUS Act Is Important for Issuers?

The GENIUS Act fundamentally changes how stablecoin issuers must approach compliance, risk management, and long-term operational planning.

Here are the core reasons this regulatory shift directly impacts your stablecoin issuance strategy and business sustainability.

- Regulatory ambiguity is replaced with enforceable stablecoin rules, increasing accountability and reducing flexibility for experimental issuance models.

- Stablecoin issuer compliance expectations now align more closely with traditional financial institutions rather than loosely regulated crypto platforms.

- Banking relationships become dependent on demonstrable compliance maturity, directly affecting liquidity access and payment network participation.

- Compliance failures carry higher reputational risk, making trust preservation a commercial priority rather than a legal afterthought.

- Early alignment with GENIUS Act stablecoin compliance requirements positions issuers favorably with regulators, partners, and institutional customers.

Also read: Identity Verification Solutions for Stablecoin Companies

Understanding its importance leads naturally to a more practical concern: whether your stablecoin model is directly covered by these requirements.

Which Stablecoin Issuers Fall Under the GENIUS Act?

The GENIUS Act defines specific issuer categories that must comply based on stablecoin design, usage, and market exposure.

Here’s how to determine whether your stablecoin issuance model falls within the Act’s regulatory scope.

- Payment-focused stablecoins intended for transactions, settlements, or remittances are explicitly covered under the GENIUS Act provisions.

- Issuers targeting US users remain subject to compliance obligations, even when operational headquarters are located offshore.

- Fiat-backed stablecoins face stricter oversight compared to algorithmic models, due to redemption promises and reserve expectations.

- White-label issuers and intermediaries may share compliance responsibility depending on operational control and customer interaction.

- Misclassifying issuer status increases enforcement risk, especially when stablecoins integrate with regulated payment or banking infrastructure.

For issuers that fall within scope, compliance begins with understanding the licensing expectations tied to lawful operation.

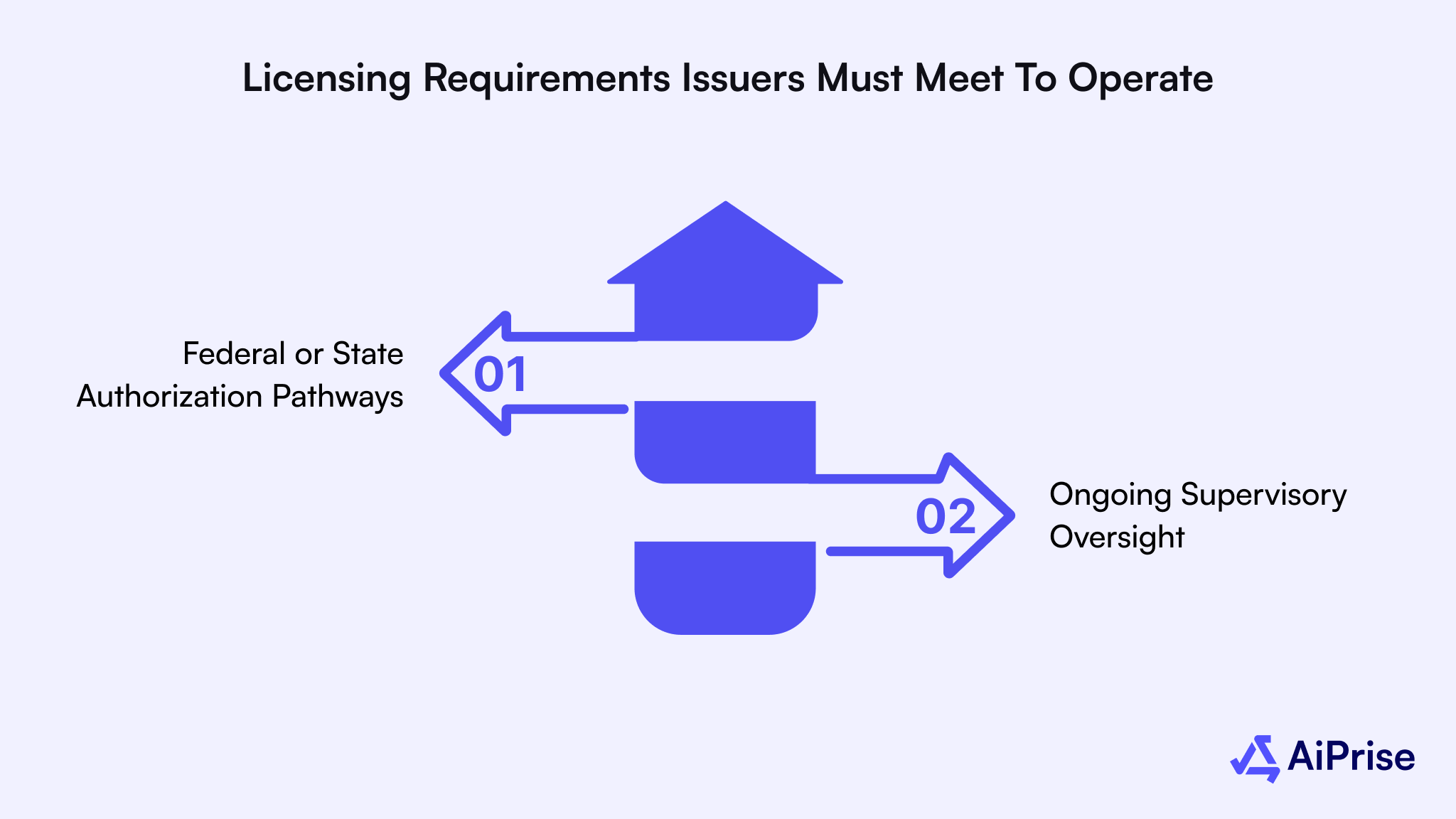

Licensing Requirements Issuers Must Meet to Operate

Licensing under the GENIUS Act formalizes stablecoin issuance as a regulated financial activity requiring ongoing supervisory approval.

Here’s how licensing expectations apply in practice, depending on your operational structure and regulatory exposure.

Federal or State Authorization Pathways

Stablecoin issuers must obtain authorization through approved federal or state regulatory channels before offering tokens domestically. Licensing determines supervisory authority, examination frequency, and reporting obligations throughout the issuance lifecycle. Failure to secure appropriate authorization may restrict market access and trigger enforcement actions across multiple jurisdictions.

Ongoing Supervisory Oversight

Licensing approval introduces continuous regulatory supervision rather than one-time compliance verification during onboarding stages. Regulators expect governance accountability, documented controls, and executive ownership of compliance outcomes. Operational changes, reserve modifications, or expansion plans may require regulator notification or approval.

Also read: Navigating KYC and Compliance Risk in the Stablecoin Space

Licensing is only one part of compliance, and reserve management often becomes the most scrutinized obligation for issuers.

Reserve Rules That Redefine Stablecoin Backing

Reserve requirements under the GENIUS Act directly affect liquidity management, profitability, and redemption reliability for issuers.

Here are the reserve obligations reshaping how stablecoin backing must be structured and maintained.

- Stablecoins must maintain one-to-one backing using high-quality liquid assets capable of supporting immediate redemption requests.

- Acceptable reserve assets typically include cash, short-term US Treasuries, or equivalent government-backed instruments.

- Yield-seeking reserve strategies are restricted, limiting exposure to market volatility and speculative investment risks.

- Reserve segregation from operating funds becomes mandatory, reducing misuse and improving audit transparency.

- Inadequate reserve disclosures increase regulatory scrutiny and may undermine user confidence during market stress events.

Beyond reserves, regulators focus closely on how issuers prove financial health through audits and ongoing reporting.

Audit and Reporting Expectations Under the GENIUS Act

Audit and reporting requirements transform compliance into a continuous operational obligation rather than periodic documentation exercises.

Here’s what ongoing audit readiness and regulatory reporting mean for your stablecoin operations.

- Issuers must conduct regular third-party audits to validate reserve sufficiency, asset quality, and redemption coverage.

- Reporting frequency increases, requiring timely disclosure of financial health, reserve composition, and compliance controls.

- Audit findings may trigger remediation timelines, forcing operational adjustments under regulatory supervision.

- Inconsistent reporting practices raise red flags for regulators, partners, and banking institutions evaluating issuer risk.

- Continuous monitoring systems help maintain compliance alignment between audits, inspections, and regulatory examinations.

For issuers managing these audit and reporting demands, AiPrise supports compliance by centralizing verification records, risk decisions, and monitoring logs in an audit-ready environment aligned with regulatory expectations.

Financial transparency alone isn’t enough, as regulators also expect strong controls against financial crime.

AML and KYC Expectations for Stablecoin Issuers

AML and KYC obligations position stablecoin issuers closer to regulated financial institutions than technology platforms.

The table below outlines how GENIUS Act stablecoin compliance requirements apply to identity verification and financial crime controls.

Also read: How to Navigate KYB for Stablecoin Companies

These requirements don’t exist in isolation, and they directly influence how compliance shows up in daily operations.

What Compliance Looks Like in Day-to-Day Operations?

GENIUS Act compliance reshapes everyday workflows, affecting onboarding speed, cost structures, and internal coordination.

Here’s how operational reality changes once stablecoin issuer compliance becomes mandatory and ongoing.

- Customer onboarding timelines may increase without automation, affecting growth velocity and user experience expectations.

- Compliance teams require closer alignment with engineering and product functions to prevent workflow bottlenecks.

- Cross-border users introduce additional complexity when US compliance standards must be applied globally.

- Manual compliance processes struggle to scale, increasing operational costs as transaction volumes grow.

- Proactive compliance design reduces rework, remediation costs, and regulatory intervention risks over time.

Once operational impact is clear, the next step is understanding how technology can support compliance execution.

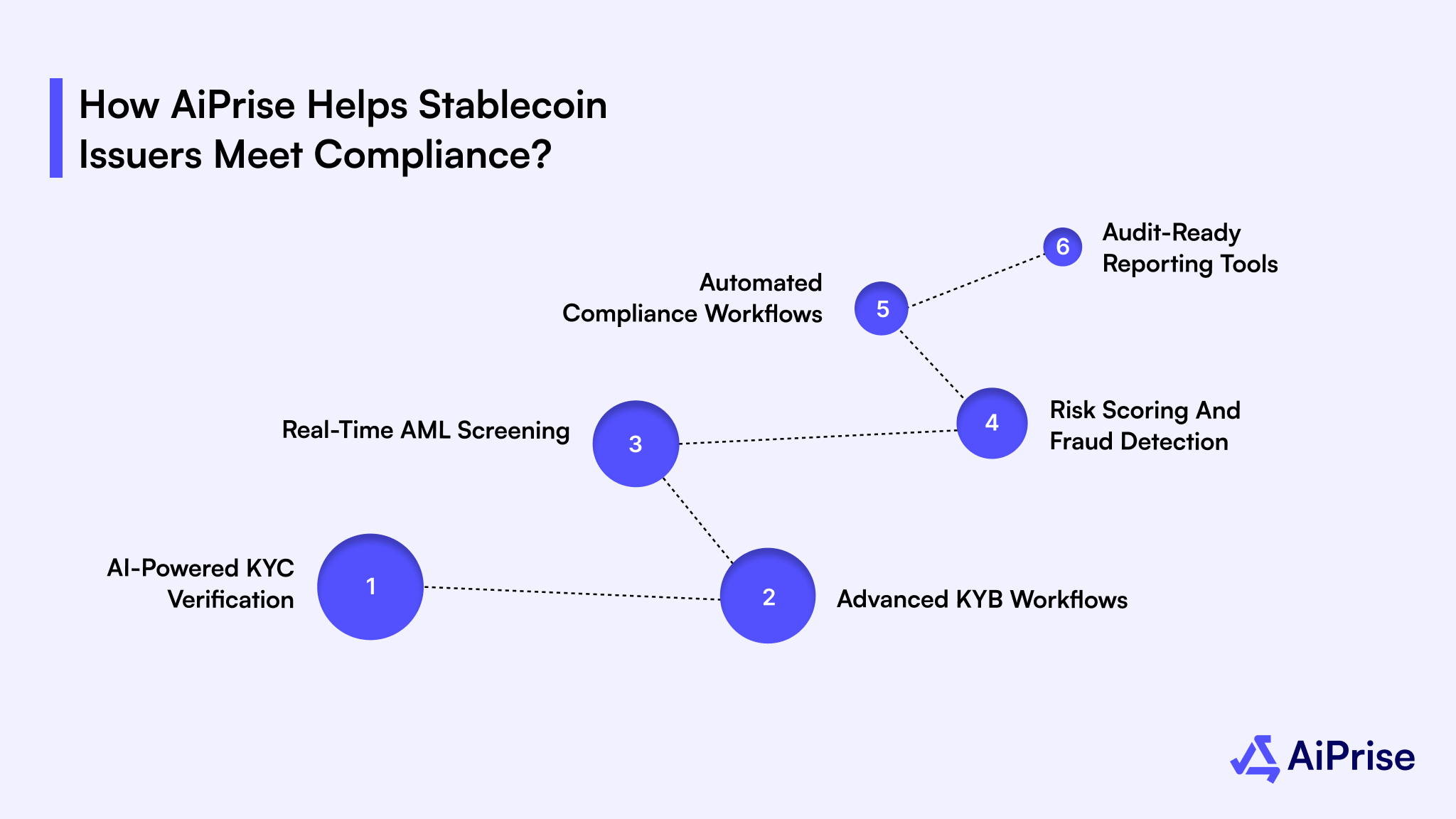

How AiPrise Helps Stablecoin Issuers Meet Compliance?

AiPrise enables you to operationalize GENIUS Act stablecoin compliance requirements by automating identity verification, risk management, and ongoing regulatory controls.

Here’s how AiPrise’s core products and services support stablecoin issuer compliance at scale without slowing growth or onboarding.

- AI-powered KYC verification helps you verify individual users using government-issued IDs, biometrics, and fraud detection signals.

- Advanced KYB workflows allow you to validate business entities, beneficial owners, and corporate structures across global jurisdictions.

- Real-time AML screening enables continuous monitoring against sanctions lists, watchlists, and adverse media throughout customer lifecycles.

- Risk scoring and fraud detection help you assess customer and transaction risk dynamically using machine learning models and trusted data sources.

- Automated compliance workflows reduce manual reviews by integrating verification, monitoring, and case management into a single platform.

- Audit-ready reporting tools ensure verification records, risk decisions, and monitoring logs remain accessible for regulatory examinations and audits.

By centralizing compliance operations, AiPrise helps you reduce operational friction, maintain regulatory confidence, and scale stablecoin issuance responsibly.

Wrapping Up

Stablecoin issuance under the GENIUS Act is no longer about reacting to regulation, but about designing compliance into your operating model from the start. When you clearly understand GENIUS Act stablecoin compliance requirements, you reduce uncertainty, control risk, and create a foundation for sustainable growth in the US market.

This is where AiPrise helps by turning complex compliance obligations into scalable, automated workflows that support issuance without slowing operations.

Book A Demo to see how the right compliance infrastructure can support your stablecoin strategy while meeting GENIUS Act expectations with confidence.

FAQs

1. What are the GENIUS Act stablecoin compliance requirements?

GENIUS Act stablecoin compliance requirements define licensing, reserve backing, audits, disclosures, and AML controls for issuers operating in the US.

2. Who must comply with the GENIUS Act?

Any stablecoin issuer offering payment-focused tokens to US users must comply, regardless of operational headquarters location.

3. Are stablecoin reserves mandatory under the GENIUS Act?

Yes, issuers must maintain one-to-one reserves using high-quality liquid assets to support immediate redemption obligations.

4. Do stablecoin issuers need KYC and AML programs?

Stablecoin issuers must implement robust KYC and AML programs comparable to those used by regulated financial institutions.

5. How does the GENIUS Act impact stablecoin issuance costs?

Compliance increases upfront operational costs but reduces long-term regulatory risk, banking friction, and enforcement exposure.

You might want to read these...

AiPrise

11 mins read

How Compliance Copilot is Revolutionizing Risk Management and Compliance Monitoring

Discover how Compliance Copilot, an AI-powered platform, is transforming risk management and compliance monitoring. Learn how it proactively detects risks, automates tasks, and keeps businesses compliant with real-time regulatory updates across global jurisdictions

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately