AiPrise

13 min read

November 20, 2025

Understanding Regulatory Risk in Banking: Key Concepts and Examples

Key Takeaways

In early 2024, a major North American bank was fined over $3 billion for failing to report suspicious activity. It was not an isolated case. That year, U.S. regulators issued over $4 billion in fines, making up 90% of all global banking penalties. These numbers highlight a sharp truth: regulatory risk in banking is more severe and costly than ever before.

For compliance officers, risk managers and executives, this is not just a financial issue. A single compliance failure can lead to crushing penalties, lost licenses or broken customer trust. Nearly 9 in 10 community bankers now rank regulation as a top concern, tied only with rising funding costs.

So what exactly is regulatory risk in banking? How can institutions identify, assess and control it across jurisdictions? And what lessons can be drawn from recent enforcement trends?

This article explains the key concepts, with real-world examples to help make sense of the growing pressure.

Key Takeaways

- Regulatory risk is critical: Non-compliance with regulations can lead to massive fines, operational restrictions, and reputational damage.

- Complex regulations require proactive management: Financial institutions need to stay ahead of evolving regulations, such as AML, KYC, and data privacy laws.

- Technology plays a pivotal role: Using RegTech solutions, including AI-driven risk profiling and automated reporting, helps banks reduce errors and improve compliance efficiency.

- Real-world consequences are severe: High-profile cases like Wells Fargo and Danske Bank show that regulatory failures can result in billions in fines and long-term reputational damage.

- Mitigating regulatory risk requires continuous monitoring: With the right tools, such as automated monitoring systems and AI-powered case management, banks can identify and address risks before they escalate.

What is Regulatory Risk in Banking?

Regulatory risk in banking refers to the potential for financial loss, legal penalties, or reputational damage that arises from non-compliance with laws, regulations, or supervisory expectations. These can be domestic or international and often evolve rapidly in response to new risks, market dynamics, or political shifts.

Banks must comply with a range of regulatory obligations, including:

- Anti-Money Laundering (AML)

- Know Your Customer (KYC)

- Basel III and capital adequacy standards

- Consumer protection laws

- Data privacy regulations (e.g., GDPR, CCPA)

- Stress testing and prudential regulation

- Sanctions compliance

A failure in any one of these areas can trigger enforcement action, financial penalties, operational restrictions, and long-term reputational harm.

Key Categories of Regulatory Risk:

Suggested read: AiPrise Recognized In The RegTech100: Leading The Charge In Regulatory Technology Innovation For 2025

Major Regulatory Areas Banks Must Monitor

Understanding what regulatory risk in banking means is only the beginning. The real challenge lies in staying on top of the fast-evolving regulatory domain, where compliance requirements vary across jurisdictions and are frequently updated in response to emerging risks.

From global banking giants to regional institutions, all banks must navigate a complex web of oversight. Below are the core areas of regulatory focus that banks must continuously monitor and manage:

To truly grasp the impact of these compliance requirements, we must examine instances where they were violated.

Real-World Examples of Regulatory Risk in Banking

Understanding regulatory risk in theory is one thing, but the consequences become crystal clear when viewed through the lens of real-world enforcement actions. In recent years, several major financial institutions have faced massive penalties for compliance failures, ranging from anti-money laundering (AML) lapses to data privacy violations and sanctions breaches.

Here are some of the most notable examples from 2023 and 2024:

- A major North American bank was fined $3 billion in 2024 for failing to detect and report suspicious activity, marking one of the largest AML-related penalties in recent history.

- A leading European global bank incurred a €1.2 billion (~$1.3 billion) fine in 2023 for violations of the EU’s General Data Protection Regulation (GDPR), highlighting the growing weight of data compliance.

- A well-known Asian financial group was penalized $500 million for mis-selling investment products to vulnerable senior citizens, triggering widespread scrutiny of their customer due diligence.

- A U.S.-based digital bank paid $245 million in 2024 for weak KYC/AML controls in its crypto services, amid a surge in regulatory focus on digital assets.

- A Swiss bank’s subsidiary faced a $360 million penalty for sanctions violations and failure to properly screen politically exposed persons (PEPs).

These cases show how regulatory failures can result in billion-dollar penalties, reputational damage and long-term operational setbacks.

According to FinCEN’s Year in Review for FY 2024, U.S. financial institutions filed over 4.7 million suspicious activity reports (SARs)—a slight increase from 4.6 million the previous year. This steady rise reflects growing pressure on banks to detect, report and respond to emerging risks, especially in sectors like digital assets and cross-border payments.

To avoid similar outcomes, banks must take a proactive approach. That begins with knowing how to identify and measure regulatory risk effectively.

Suggested read: How Banks Utilize Machine Learning For Fraud Detection.

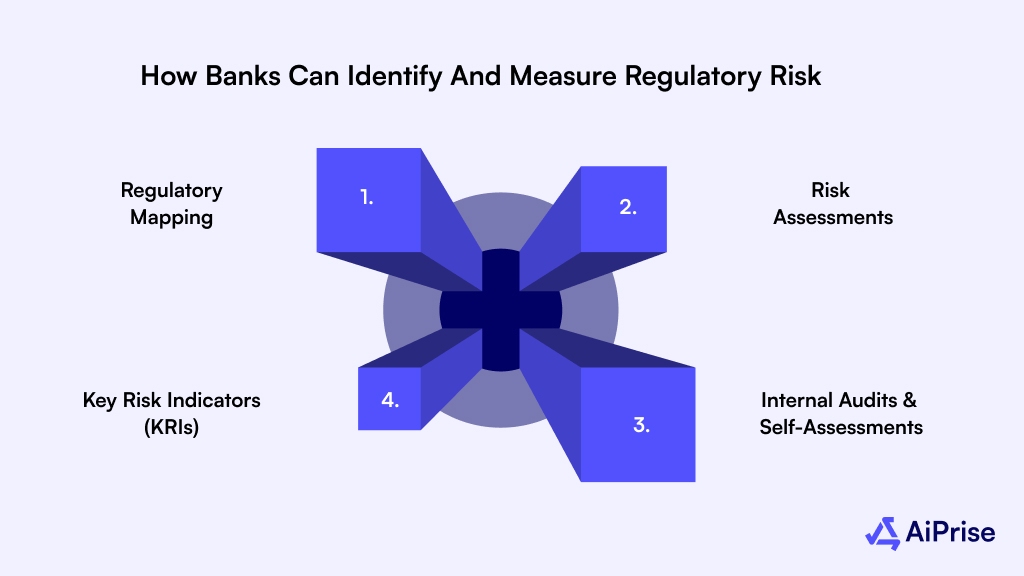

How Banks Can Identify and Measure Regulatory Risk

Recognizing regulatory risk early allows financial institutions to proactively address compliance gaps — rather than reactively manage crises. But identifying these risks isn’t always straightforward, especially in complex, multi-jurisdictional operations.

Here’s how banks can systematically identify and measure regulatory risk in 2024 and beyond:

1. Regulatory Mapping

Banks must maintain an up-to-date inventory of all applicable regulations by jurisdiction, business unit, and product line. This includes:

- AML/CTF obligations (e.g., FinCEN, FATF, MAS)

- Consumer protection laws (e.g., GDPR, CCPA)

- Sanctions regimes (e.g., OFAC, EU, UN)

- Prudential requirements (e.g., Basel III, Dodd-Frank)

Regular mapping ensures banks are aware of new or amended regulations before enforcement actions occur.

2. Risk Assessments

Regulatory risks should be assessed as part of enterprise risk management (ERM), with scoring based on:

- Likelihood of non-compliance (e.g., due to legacy systems or manual workflows)

- Impact of violation (e.g., financial penalties, license revocation, reputational loss)

- Control effectiveness (i.e., how strong your current frameworks are)

These assessments help prioritize risk mitigation efforts and resource allocation.

3. Key Risk Indicators (KRIs)

KRIs allow banks to monitor early warning signs that could signal rising compliance risk, such as:

- Increasing number of compliance breaches or exceptions

- Delays in Suspicious Activity Report (SAR) filing

- Low completion rates in mandatory training

- High turnover in compliance roles

- Alert backlogs in transaction monitoring systems

By setting thresholds, banks can escalate issues before they snowball.

4. Internal Audits and Regulatory Self-Assessments

Banks should conduct regular audits and control tests focused specifically on regulatory obligations. Many regulators now expect institutions to perform self-assessments — essentially simulating an external exam — and report findings internally.

This not only helps fix weak points but also demonstrates a proactive compliance culture.

Now that we understand how to detect regulatory risk, let’s explore how banks can effectively mitigate it using tools, culture, and technology.

How Banks Can Mitigate Regulatory Risk

Identifying risk is only half the battle; the real challenge lies in reducing exposure without disrupting core banking operations. In today’s environment, regulatory risk mitigation requires a mix of strong governance, agile systems, and a deeply embedded compliance culture.

Here’s how leading banks are staying ahead:

1. Build a Robust Compliance Framework

A strong compliance management system (CMS) includes:

- Clear policies and procedures mapped to regulatory requirements

- Dedicated compliance officers with authority and independence

- Regular training for employees across departments

- Monitoring and testing of controls and internal audits

- Reporting mechanisms for issues and escalation

This framework ensures consistency in regulatory interpretation and response.

2. Use Technology and Automation

Regulatory tech (RegTech) has become essential in mitigating compliance risk:

- Automated transaction monitoring reduces false positives

- Natural Language Processing (NLP) helps parse regulatory updates in real-time

- AI-based case triage accelerates SAR filing and investigation timelines

- Digital onboarding tools ensure KYC/AML accuracy and speed

- Workflow automation enforces policy adherence and documentation

According to Deloitte, banks using advanced RegTech solutions can cut compliance costs by up to 30% and reduce operational errors significantly.

3. Strengthen Governance and Oversight

Board and senior management involvement is critical. Regulators now expect:

- Regular compliance updates at the board level

- Risk appetite statements that cover regulatory risks

- Clear roles, responsibilities, and escalation paths

- Oversight of third-party compliance (e.g., fintech partners, vendors)

Strong governance not only mitigates risk but also protects executive accountability.

4. Build a Culture of Compliance

Culture is often the root cause of non-compliance. Banks should:

- Reward compliance-positive behavior

- Incorporate ethical decision-making into leadership training

- Embed compliance into everyday workflows — not as a checkbox, but as a shared value

According to PwC, 71% of organizations expect to launch digital transformation initiatives within the next three years that will require compliance support.

With mitigation strategies in place, it’s worth examining what happens when these systems break down — through real-world examples of regulatory risk in action.

Real-World Cases of Regulatory Risk: What Happens When Compliance Fails?

While robust compliance frameworks and technology solutions can minimize regulatory risk, lapses still occur — and the consequences are often severe. Looking at real-world examples, we can see how regulatory failures spiral into monumental financial and reputational damage.

These high-profile cases serve as stark reminders of why managing regulatory risk is imperative for the banking sector.

Case 1: Wells Fargo’s Fake Account Scandal (2016)

One of the most infamous regulatory breaches in recent banking history, Wells Fargo was fined over $3 billion for creating millions of fake accounts to meet aggressive sales targets. The violations spanned multiple regulations, including consumer protection laws and fair lending rules, resulting in:

- A settlement fine with U.S. regulators

- A major reputational hit and loss of customer trust

- A need for an overhaul of internal sales practices and compliance oversight

Key Takeaway: Even a single compliance failure, if widespread enough, can lead to billions in fines and years of recovery.

Case 2: Danske Bank Money Laundering Scandal (2018)

Danske Bank was found to have processed €200 billion in suspicious transactions through its Estonian branch between 2007 and 2015, involving Russian oligarchs and other high-risk clients. This scandal led to:

- €26 billion in penalties and fines

- Criminal investigations by U.S. and EU authorities

- A major restructuring effort and the departure of several senior executives

Lesson Learned: Regulatory risk isn’t just about financial penalties — it’s also about a massive erosion of trust in the institution.

Case 3: HSBC’s AML Failures (2012)

In 2012, HSBC was fined $1.9 billion for failing to monitor transactions that could potentially fund terrorism and money laundering activities. Despite being subject to intense regulatory scrutiny, the bank’s AML compliance programs failed to detect large-scale illicit transactions.

This case set a significant precedent for regulators’ expectations in AML enforcement.

Key Takeaway: Even major banks with robust compliance systems in place can fall victim to regulatory violations if those systems aren’t properly maintained or updated in line with evolving risks.

These cases demonstrate that reactive compliance isn’t enough. As financial institutions face growing regulatory complexity and oversight, it’s critical to be proactive in identifying, measuring, and mitigating risks.

Let's see how banks are using cutting-edge technology to stay ahead of compliance demands and reduce regulatory risk exposure.

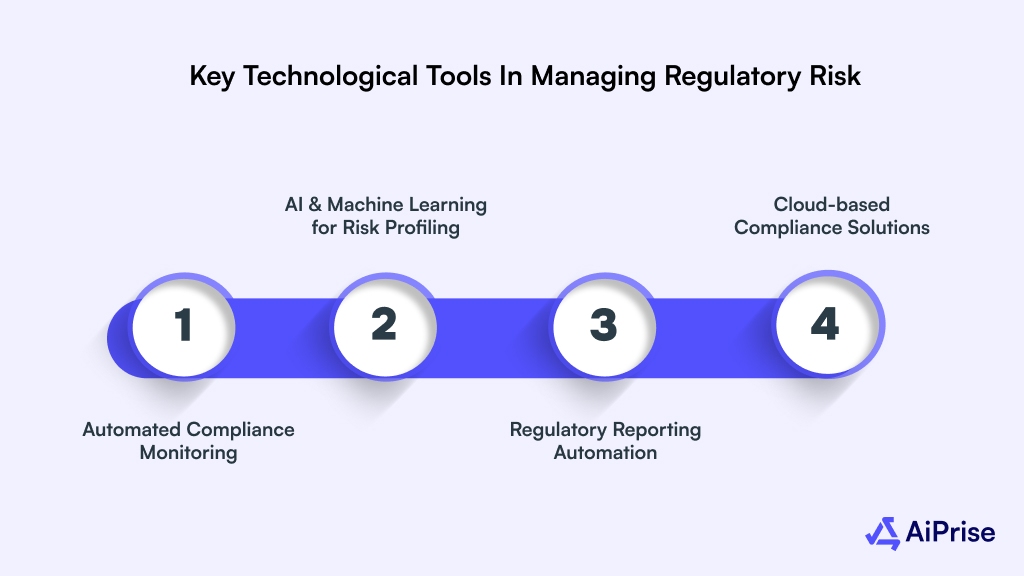

The Role of Technology in Regulatory Risk Management

As regulatory frameworks grow more complex, the traditional, manual approach to compliance simply can't keep up. Technology has become an essential ally in helping banks not only manage but mitigate regulatory risk in real-time.

Banks are increasingly adopting RegTech solutions, specialized technology designed to streamline compliance, automate processes, and ensure real-time monitoring. These tools allow institutions to respond to regulatory changes faster and more efficiently than ever before.

Key Technological Tools in Managing Regulatory Risk

- Automated Compliance Monitoring

Real-time monitoring of transactions for AML, KYC, and sanctions compliance is now automated in most leading banks. This ensures that suspicious transactions are flagged instantly, reducing human error and minimizing delays.

- AI & Machine Learning for Risk Profiling

AI-driven tools help assess client risk profiles quickly and accurately. These tools can analyze vast amounts of data to detect patterns and trends that humans might miss, improving the quality of risk assessments.

- Regulatory Reporting Automation

Automated reporting tools help financial institutions ensure compliance with reporting requirements, whether they be for AML, KYC, or GDPR. These tools reduce the time spent preparing reports and eliminate the risk of human error in regulatory filings.

- Cloud-based Compliance Solutions

With cloud solutions, banks can scale their compliance efforts without massive infrastructure investments. These platforms are continuously updated to keep up with the latest regulatory changes, ensuring banks never fall behind.

Benefits of Technology in Managing Regulatory Risk

- Faster Response to Regulatory Changes: Automated systems can quickly adapt to changes in regulations, making compliance more agile.

- Cost Efficiency: Banks can save significantly by automating tasks that would otherwise require large teams of compliance officers.

- Improved Accuracy: Automation minimizes human error, reducing the risk of non-compliance penalties.

- Real-Time Data Access: With digital solutions, banks have 24/7 access to their compliance data, enabling them to detect and respond to risks instantly.

Now, with the proper tools in place, let’s look at how AiPrise helps banks take proactive steps to manage regulatory risk while ensuring seamless compliance.

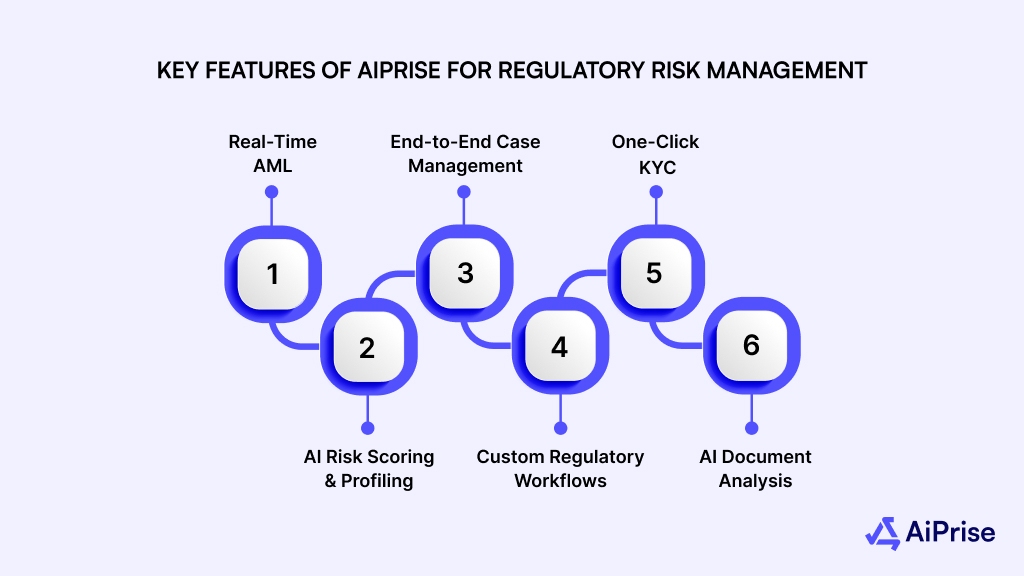

How AiPrise Helps Minimize Regulatory Risk in Banking

AiPrise provides financial institutions with advanced solutions to navigate the complexities of regulatory risk. By combining automation, real-time data analysis, and cutting-edge technology, AiPrise offers a seamless way for banks to maintain compliance and stay ahead of potential risks.

Key Features of AiPrise for Regulatory Risk Management:

- Real-Time AML

AiPrise ensures instantaneous AML checks, enabling banks to identify suspicious activity or high-risk clients in real time. With pre-built integrations to global sanctions lists and financial crime databases, AiPrise offers a comprehensive approach to compliance.

- AI-Driven Risk Scoring & Profiling

AiPrise uses machine learning to assess the risk of individual clients, monitoring behavior patterns and flagging anomalies that could indicate regulatory concerns. This helps banks make informed decisions, reducing manual reviews and mitigating risks.

- End-to-End Case Management

Banks can manage compliance cases end to end using AiPrise’s centralized dashboard. It supports real-time tracking, audit trails and automated workflows for escalations and reporting.

- Custom Workflows for Regulatory Needs

AiPrise allows compliance teams to design workflows that reflect their specific regulatory obligations—local or international. From document collection to risk checks, banks maintain full control.

- One-Click KYC

For low-risk customers, AiPrise enables instant verification using just a selfie and ID number. This reduces onboarding friction without compromising compliance accuracy.

- AI-Powered Document Insights

Advanced AI extracts and analyzes data from uploaded documents, allowing faster reviews and flagging of inconsistencies or potential fraud indicators.

AiPrise helps banks meet global compliance standards while reducing operational burden and regulatory exposure. It enables financial institutions to stay audit-ready, adapt quickly to policy changes and focus on what matters most—risk mitigation and customer trust.

Want to see how AiPrise supports fast, secure onboarding in high-growth banking environments?

Explore our compliance tools for neobanks

Conclusion

Regulatory risk in banking is a critical factor that affects a bank’s financial health, operational stability, and reputation. As regulations become more complex, it’s essential for banks to adopt a proactive approach to manage risk.

Technology, such as automated transaction monitoring and AI-driven risk profiling, is helping banks streamline compliance, reduce errors, and stay ahead of regulatory changes.

The cases we’ve explored show the severe consequences of non-compliance. Whether facing multi-million-dollar fines or reputational damage, the stakes are high.

By implementing a strong compliance framework and leveraging RegTech solutions, banks can meet regulatory requirements while improving operational efficiency and maintaining trust.

Take control of your institution’s compliance today.

Book a Demo with AiPrise to see how we can help you manage regulatory risk seamlessly.

FAQs

Q1: What is regulatory risk in banking?

Regulatory risk in banking refers to the chance of legal or financial loss, reputational damage, or operational disruption caused by failing to comply with laws, regulations or supervisory expectations.

This includes areas like AML/KYC, sanctions compliance, data privacy and prudential regulation.

Q2: Why is regulatory risk increasing for banks today?

Regulatory risk is rising because:

- regulations are growing more complex and global in reach;

- regulators are using bigger data sets and stronger enforcement;

- new business models (e.g., digital banking, crypto) introduce unfamiliar risks;

- public sensitivity around financial misconduct has grown, increasing reputational stakes.

Q3: What are the main consequences if a bank fails to manage regulatory risk well?

Key consequences include:

- Large fines and penalties from regulators;

- Operational restrictions (e.g., license revocation, business bans);

- Reputational damage and loss of customer trust;

- Additional cost burdens such as increased capital requirements or remediation efforts.

Q4: How do banks identify regulatory risk?

Banks identify regulatory risk through methods such as:

- Regulatory mapping across jurisdictions and business units;

- Risk assessments scoring likelihood of non‑compliance and impact;

- Key Risk Indicators (KRIs) to monitor early warning signs;

- Internal audits and self‑assessments to test control frameworks.

Q5: What tools or technologies can banks use to mitigate regulatory risk?

Banks can leverage technology such as:

- Automated AML and KYC systems for real‑time monitoring;

- AI and machine learning for risk profiling and anomaly detection;

- Automated regulatory reporting tools to reduce human error;

- Customizable workflow and case‑management platforms to support compliance functions.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately