AiPrise

12 min read

January 7, 2026

What Is 314a FinCEN? Compliance Guide for Handling Law Enforcement Requests

Key Takeaways

Financial institutions increasingly face pressure to respond accurately and quickly to law enforcement requests under FinCEN’s 314(a) compliance program. Compliance teams at banks, fintechs, and crypto platforms often struggle with fragmented record systems and rising regulatory scrutiny tied to AML obligations and operational risk. In 2025, the FinCEN 314(a) program has processed more than 8,200 law enforcement requests, including over 7,300 related to money laundering investigations across U.S. financial networks.

Understanding how a 314(a) FinCEN request flows through your compliance process helps you meet deadlines and avoid examiner findings. Many teams also lack clarity about legal requirements, internal workflows, and the data needed to comply with search and reporting expectations. Mastering these elements now helps your organization reduce risk, strengthen compliance controls, and support effective law enforcement collaboration.

At a Glance

- FinCEN 314(a) allows law enforcement to ask financial institutions to search internal records for links to suspected money laundering or terrorist financing.

- Covered institutions must review customer identities, accounts, transactions, and beneficial ownership data while maintaining strict confidentiality.

- Responses are required only when a confirmed match is found, and all searches must be documented for regulatory review.

- Clear workflows, accurate data, and audit-ready records help institutions meet deadlines and reduce compliance risk.

What Is FinCEN 314(a)?

FinCEN 314(a) is a regulatory mechanism that allows U.S. law enforcement agencies to request information from financial institutions during investigations. It was established under the USA PATRIOT Act to help identify individuals or businesses potentially involved in money laundering or terrorist financing. Through this process, financial institutions are required to search their records and report relevant matches while maintaining strict confidentiality.

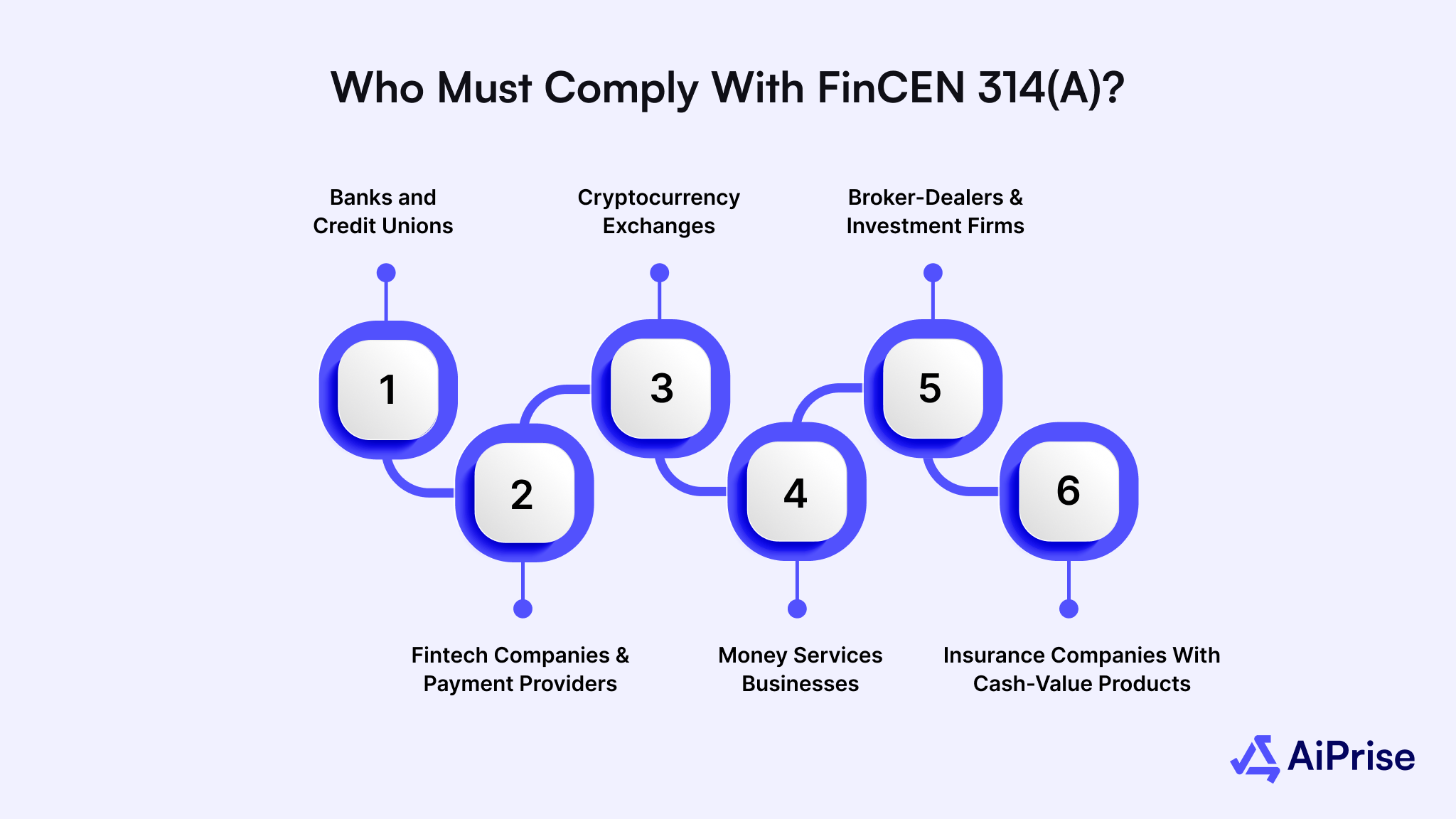

Who Must Comply With FinCEN 314(a)?

FinCEN 314(a) applies to a wide range of regulated financial entities that store customer, account, or transactional information relevant to law enforcement investigations.

Here’s how compliance responsibilities differ across institution types that fall within scope.

1. Banks and Credit Unions

Banks and credit unions are primary participants in the FinCEN 314(a) program due to their central role in holding customer deposits and processing transactions. When a 314(a) request is issued, you are required to search customer profiles, account ownership records, transaction histories, and related identifiers. Inaccurate or delayed responses often surface during AML exams and can lead to enforcement scrutiny.

2. Fintech Companies and Payment Providers

Fintech companies and payment providers are subject to FinCEN 314(a) if they operate as money services businesses or provide regulated financial products. You must assess whether customer data, digital wallets, payment flows, or stored balances match individuals or entities listed in the 314a list. Many fintechs struggle here due to fragmented systems, which increases the risk of incomplete searches.

3. Cryptocurrency Exchanges and Custodial Platforms

Cryptocurrency exchanges and custodial wallet providers are increasingly included in FinCEN 314(a) enforcement expectations. You are required to review onboarding data, KYC records, transaction histories, and blockchain-linked identifiers tied to named subjects. Regulators now expect crypto platforms to meet the same search depth and response standards as traditional banks.

4. Money Services Businesses (MSBs)

Money services businesses such as remittance providers, prepaid card issuers, and digital money transmitters fall directly under FinCEN 314(a) obligations. You must search sender and receiver data, transaction logs, and stored customer identification records when a request is received. Failure to maintain searchable records can result in compliance findings.

5. Broker-Dealers and Investment Firms

Broker-dealers and certain investment firms are covered institutions under FinCEN regulations. You are expected to search client account records, beneficial ownership details, and transaction activity tied to securities or investment products. These searches must align with your AML and recordkeeping frameworks.

6. Insurance Companies With Cash-Value Products

Insurance companies offering cash-value or investment-linked products are also subject to FinCEN 314(a). You must review policyholder records, beneficiary information, and payment histories when names appear on a request list. These obligations are often overlooked, increasing regulatory exposure.

Also read: Understanding The Basics Of A Compliance Management System

Knowing whether you fall within scope is only part of the picture; understanding the nature of the request itself is just as important.

What Is a FinCEN 314(a) Request From Law Enforcement?

A FinCEN 314(a) request is a formal mechanism that allows law enforcement agencies to seek information from financial institutions.

Here’s what you need to understand about how a 314 request works in practice.

- A 314 request is issued by federal, state, or local law enforcement through FinCEN’s secure information-sharing system.

- Each request includes a list of individuals or businesses linked to active money laundering or terrorist financing investigations.

- You receive the request on a biweekly basis, unless urgent circumstances require faster distribution.

- The request instructs you to search internal records, not proactively report unrelated suspicious activity.

- Confidentiality requirements prohibit notifying customers or third parties about the request.

- All actions taken in response to the request must be documented for regulatory review.

After understanding what a request represents, the focus shifts to how your team is expected to handle it internally.

The 314(a) Request Process: Step-by-Step

The 314(a) request process outlines how your institution must handle law enforcement information requests from receipt to record retention.

Below is a step-by-step breakdown of how compliance teams are expected to execute this process correctly.

%20Request%20Process.png)

Step 1: Receive and Acknowledge the FinCEN 314(a) Request

This step begins when your institution receives a FinCEN 314 request through FinCEN’s secure information-sharing system.

Here’s how the intake stage should be handled internally.

- You must ensure that only authorized compliance personnel access the FinCEN 314a request to maintain confidentiality.

- The request should be reviewed immediately to confirm identifiers, deadlines, and response expectations.

- Internal acknowledgment procedures help confirm that the request has been received and logged.

- Compliance leadership should assign ownership to prevent delays or miscommunication.

- All intake actions should be documented to support audit readiness.

Step 2: Review Identifiers and Define Search Scope

This step focuses on understanding exactly what information must be searched across your systems.

Here’s how you establish an accurate search scope.

- You should review all names, aliases, and identifiers listed in the FinCEN 314a request.

- Search parameters must be defined to include both individual and business records where applicable.

- You should determine which systems store relevant customer, account, and transaction data.

- Beneficial ownership and control person records must be included when entities appear on the 314a list.

- Clearly defining scope helps prevent incomplete or overbroad searches.

Step 3: Conduct Searches Across Internal Systems

This step involves executing searches in line with 314a search requirements.

Here’s how compliance teams are expected to perform the search.

- You must conduct reasonable searches across all relevant onboarding, account, and transaction monitoring systems.

- Searches should include both current and historical records retained under recordkeeping obligations.

- Identifiers used may include names, dates of birth, addresses, government-issued IDs, and business registration numbers.

- Manual systems must be reviewed alongside automated platforms if they contain relevant data.

- All search results should be captured and preserved for documentation purposes.

Step 4: Analyze Results and Determine Match Status

This step determines whether a reportable match exists. Here’s how you evaluate and validate findings.

- You must assess whether potential matches meet the threshold for reporting under FinCEN 314(a).

- False positives should be ruled out using available identifiers and contextual data.

- Legal or senior compliance review may be required for complex cases.

- Decisions should be based on documented criteria, not assumptions.

- Each determination must be recorded clearly for examiner review.

Step 5: Submit Response in Line With Reporting Rules

This step ensures your response aligns with 314a reporting requirements. Here’s how a compliant submission should occur.

- You must submit a response only if a confirmed match is identified.

- Responses should be filed through FinCEN’s secure submission channel within the specified deadline.

- You should never include unnecessary customer documents unless explicitly requested.

- Over-reporting can create privacy risks and regulatory concerns.

- Submission confirmations should be retained as part of your compliance records.

Step 6: Document Actions and Retain Records

This final step supports audit readiness and regulatory examinations. Here’s how documentation and retention should be handled.

- You must document search methodologies, systems reviewed, and identifiers used.

- Records should include match determinations and response decisions.

- Documentation must be retained according to AML and recordkeeping requirements.

- Audit trails should allow regulators to reconstruct your entire response process.

- Strong documentation reduces enforcement risk during examinations.

Also read: Top 10 Financial Compliance Challenges Businesses Face in 2026

With the full process outlined, it’s worth taking a closer look at what regulators expect during the search itself.

Understanding 314(a) Search Requirements for Compliance

314(a) search requirements define how thoroughly you must review records to identify potential matches tied to law enforcement inquiries.

Here’s what regulators expect when assessing whether your search efforts were reasonable.

- You must conduct a reasonable search across all systems that store customer identity, account ownership, and transactional data relevant to the request.

- Searches must include both active and closed accounts if records are retained under AML and recordkeeping obligations.

- Identifiers used in searches typically include full legal names, known aliases, dates of birth, addresses, government-issued identification numbers, and business registration details.

- When legal entities appear on the 314a list, beneficial ownership and control person records must also be reviewed.

- If customer data is fragmented across departments or platforms, each relevant system must be included to avoid incomplete searches.

- Regulators expect you to document the scope, systems reviewed, identifiers used, and decision logic applied during each search.

Search expectations often depend on the quality of the list you are working from, which makes understanding the list itself essential.

What Does the FinCEN 314(a) List Contain and How Is It Updated?

The FinCEN 314(a) list determines which individuals or entities you are required to search for during each request cycle.

Here’s how the list works and why the FinCen 314a list updates directly affect your compliance process.

- The 314a list contains individuals, businesses, and known aliases associated with active money laundering or terrorist financing investigations.

- Each entry may include limited identifiers such as partial names, dates of birth, geographic references, or associated entities.

- FinCEN issues FinCEN 314a list updates on a biweekly basis through its secure distribution channel.

- Updates may add new subjects, modify identifiers, or remove entities no longer under investigation.

- You are required to conduct searches only against the most current list provided by FinCEN.

- Retaining or using outdated lists increases the risk of missed matches and regulatory criticism.

Also read: Understanding Regulatory Compliance: Definition And Requirements

Beyond list mechanics, institutions also need clarity on when and how findings must be reported.

FinCEN 314(a) Reporting Requirements and Response Rules

314a reporting requirements govern when and how you must communicate findings back to FinCEN.

Here’s what compliant reporting looks like in practice.

- You are required to submit a response only when a positive match is identified during your internal search process.

- Responses must be submitted through FinCEN’s secure system within the deadline specified in the request.

- You should not submit customer documents, transaction records, or additional data unless explicitly requested.

- Over-reporting irrelevant or speculative information can create privacy risks and examiner concerns.

- If no match is identified, no response is required, but the search itself must still be completed and documented.

- All records related to searches and responses must be retained to support audits and regulatory examinations.

At this point, it also helps to distinguish 314(a) from other information-sharing provisions that often cause confusion.

Key Differences Between FinCEN 314(a) and 314(b)

FinCEN 314(a) and 314(b) serve different regulatory purposes but are frequently misunderstood.

The table below clarifies their differences.

Even with the rules clearly defined, many teams still run into avoidable issues during execution.

Common 314(a) Compliance Mistakes Financial Teams Make

Most 314(a) compliance failures occur due to execution gaps rather than misunderstanding the regulation itself.

Here are the most common mistakes you should actively work to prevent.

- Missing response deadlines due to manual workflows, unclear ownership, or poor internal coordination.

- Conducting incomplete searches that exclude archived systems, closed accounts, or legacy data sources.

- Confusing mandatory 314(a) obligations with voluntary information sharing under Section 314(b).

- Submitting excessive customer information beyond what the 314a reporting requirements actually mandate.

- Failing to document search methodologies, systems reviewed, and decision rationale.

- Relying on fragmented or outdated systems that slow response accuracy and increase operational risk.

Avoiding these pitfalls often requires better systems and clearer workflows, which is where technology plays a role.

How AiPrise Helps Manage FinCEN 314(a) Obligations

Managing FinCEN 314(a) obligations requires fast access to accurate identity data, structured review workflows, and audit-ready documentation.

Here’s how AiPrise supports compliance teams handling these requirements with purpose-built capabilities.

- AiPrise provides centralized identity and business profiles by combining KYC, KYB, and beneficial ownership data, allowing you to search relevant records efficiently when a 314 a request is received.

- The platform’s OCR-based document verification ensures government-issued IDs and business documents remain searchable and standardized, supporting accurate reviews aligned with 314a search requirements.

- Biometric verification and identity matching help you validate whether listed individuals correspond to existing customer records, reducing false positives during FinCEN 314(a) searches.

- AiPrise integrates risk scoring and fraud signals from multiple data sources, helping compliance teams assess potential relevance before determining whether reporting is required.

- Built-in case management workflows allow you to document search logic, reviewer decisions, and outcomes, supporting compliance with 314a reporting requirements during audits.

- Continuous monitoring capabilities ensure customer and business records remain up to date, even as FinCEN 314a list updates introduce new identifiers or entities.

By combining identity verification, risk intelligence, and structured compliance workflows, AiPrise helps you respond to FinCEN 314(a) requests with speed, accuracy, and examiner-ready confidence.

Wrapping Up

Handling FinCEN 314(a) requests effectively comes down to clarity, speed, and disciplined execution across your compliance operations. When you understand search expectations, reporting boundaries, and confidentiality rules, you reduce regulatory risk while supporting law enforcement confidently.

AiPrise helps by centralizing identity data, automating compliant searches, and maintaining audit-ready workflows aligned with FinCEN 314(a) requirements.

Book A Demo to see how you can respond to 314(a) requests faster, with accuracy and examiner-ready confidence.

FAQs

1. What is FinCEN 314(a) used for?

FinCEN 314(a) is used to help law enforcement agencies identify potential money laundering or terrorist financing activities. It allows investigators to request information from financial institutions about specific individuals or businesses. The goal is to trace financial networks quickly while maintaining confidentiality.

2. Is FinCEN 314(a) mandatory for financial institutions?

Yes, FinCEN 314(a) participation is mandatory for covered financial institutions under the USA PATRIOT Act. When you receive a request, you are required to conduct searches within the defined scope. Failure to comply can result in regulatory and examination issues.

3. How often does FinCEN send 314(a) requests?

FinCEN typically sends 314(a) requests on a biweekly basis through its secure information-sharing system. In certain high-priority cases, requests may be issued more frequently. Each request includes a specific response deadline you must follow.

4. What information must be searched for under a 314(a) request?

You are expected to search customer identification data, account records, transaction histories, and beneficial ownership information. This usually includes names, aliases, dates of birth, government-issued IDs, and business identifiers. Searches must align with FinCEN’s reasonable search expectations.

5. Can customers be notified about a FinCEN 314(a) search?

No, you are legally prohibited from notifying customers about a FinCEN 314(a) search. Confidentiality is a core requirement of the program. Disclosing the existence of a request can result in serious regulatory consequences.

You might want to read these...

AiPrise

11 mins read

How Compliance Copilot is Revolutionizing Risk Management and Compliance Monitoring

Discover how Compliance Copilot, an AI-powered platform, is transforming risk management and compliance monitoring. Learn how it proactively detects risks, automates tasks, and keeps businesses compliant with real-time regulatory updates across global jurisdictions

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately