AiPrise

9 min read

January 22, 2026

Visa Cross Border Payments: What Fintechs Must Get Right

Key Takeaways

Cross-border payments remain one of the toughest challenges you face when scaling card transactions globally, especially if Visa is part of your payments stack. Moving money across borders can become costly, slow, and opaque if compliance, foreign exchange management, settlement timing, and fraud risk aren’t tightly controlled.

For fintechs and payment teams, these frictions directly hit your bottom line and customer experience, often causing failed transactions, costly refunds, and disputes. According to the Federal Reserve’s payments data, U.S.-issued cards processed over 7.5 billion cross-border transactions valued at $470 billion as of the most recent reporting period, showing just how significant and rapidly growing this space remains for American businesses.

Understanding visa cross-border payments helps you pinpoint exactly where operational and compliance bottlenecks occur so you can optimize speed, cost, and security without sacrificing customer trust. Mastering these elements is essential if you want your platform to compete internationally and deliver seamless cross-border experiences.

Key Insights

- Visa cross-border payments depend on tightly coordinated compliance checks, FX handling, settlement flows, and fraud controls across multiple countries.

- At scale, fintechs face higher decline rates, hidden FX costs, and operational breakdowns when identity, risk, and payment systems are misaligned.

- Cross-border card transactions carry elevated fraud exposure, slower dispute resolution, and stricter regulatory scrutiny than domestic payments.

- Corporate cross-border card payments add further complexity through higher transaction values, complex business structures, and deeper KYB and AML requirements.

What are Visa Cross-Border Payments?

Visa cross-border payments refer to card transactions where the cardholder and merchant are located in different countries. These payments are processed through Visa’s global card network, enabling international authorization, clearing, currency conversion, and settlement across borders. For fintechs, Visa cross-border payments involve additional layers of compliance, foreign exchange handling, risk controls, and cross-jurisdictional regulations.

Why Cross-Border Card Payments Fail at Scale?

Cross-border card payments can break down for fintechs when friction points accumulate across regulatory, operational, and risk systems.

Here are the most common reasons these payments often falter at scale:

- Inconsistent global compliance frameworks hinder transaction approval efficiency because differing AML/KYC rules increase manual review rates and delays.

- Foreign exchange (FX) cost volatility can erode margins heavily, with some cross-border retail FX costs averaging above 1% of transaction value despite global reduction efforts (G20 framework reporting).

- Insufficient end-to-end identity verification increases friction and declines, especially where customer data mismatches trigger chargebacks or holds.

- Legacy processing systems and outdated interfaces struggle to handle peak volumes, leading to timeouts, retries, and drop-offs in transaction pipelines.

- Fraud detection systems that aren’t tailored to cross-border nuances elevate false positives, slowing approvals and raising operational costs.

Also read: Understanding Challenges in Cross-Border Payment Compliance

Many of these failures tie back to how currency conversion is handled, which is where margins quietly start slipping.

How FX Handling Impacts Visa Cross-Border Margins?

Effective foreign exchange (FX) management directly affects how much fintechs earn on Visa cross-border card transactions.

Here’s how FX handling can make or break payment economics for fintech operators:

.png)

- Hidden FX spreads reduce net revenues by quietly widening the gap between wholesale and customer exchange rates, often without clear disclosures.

- Volatile currency corridors increase reconciliation complexity when frequent rate swings require constant adjustment of pricing and hedging strategies.

- Delayed FX settlements create cash-flow drag as funds can sit longer than expected before being converted to the home currency.

- Opaque rate benchmarking confuses customers and partners when costs vary by corridor and lacks transparency in reconciliation reporting.

- Average retail costs on cross-border payments from North America can exceed 3 % of value, illustrating how FX and related fees significantly erode margins.

Beyond cost pressures, regulatory gaps often create delays and declines that are harder to spot but just as damaging.

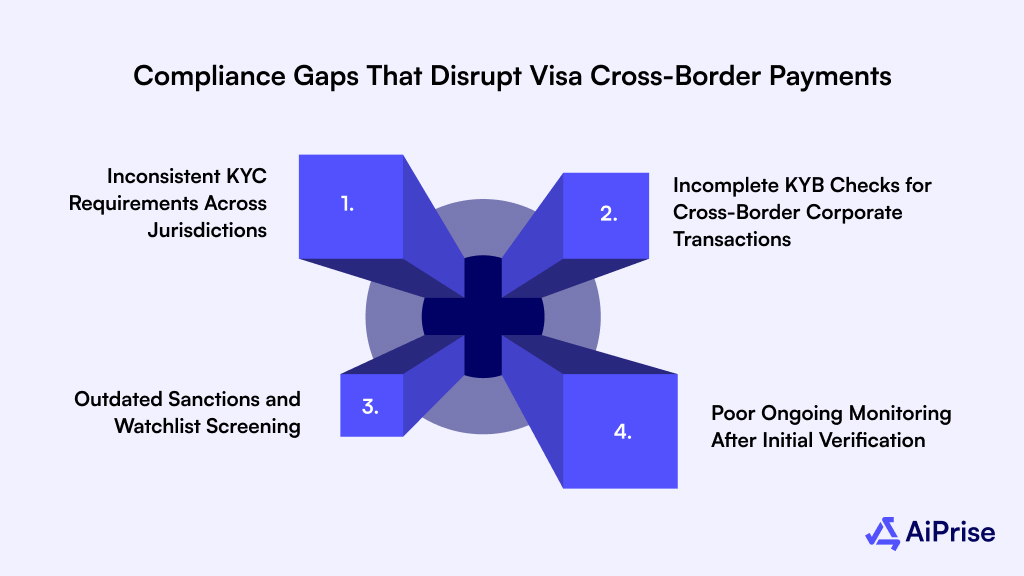

Compliance Gaps That Disrupt Visa Cross-Border Payments

Regulatory misalignment is one of the most common reasons cross-border card payments slow down or fail unexpectedly.

Below are the key compliance gaps that disrupt Visa cross-border payment flows at scale.

1. Inconsistent KYC Requirements Across Jurisdictions

KYC standards vary widely between countries, creating friction when customer data collected in one region fails validation elsewhere. This often leads to manual reviews, delayed approvals, or outright transaction declines during cross-border processing. For fintechs operating at scale, these inconsistencies compound operational costs and slow down customer onboarding.

2. Incomplete KYB Checks for Cross-Border Corporate Transactions

Corporate card payments across borders require deeper KYB checks, including ownership structures and business legitimacy verification. Gaps in KYB processes increase exposure to shell companies, sanctioned entities, or fraudulent intermediaries. This risk is especially high for fintechs serving global merchants or acting as Visa cross-border corporate payments providers.

3. Outdated Sanctions and Watchlist Screening

Sanctions lists and regulatory watchlists change frequently, especially in geopolitically sensitive regions. Relying on static or infrequently updated screening tools can result in non-compliant transactions slipping through unnoticed. This exposes fintechs to regulatory penalties, reputational damage, and forced transaction reversals.

4. Poor Ongoing Monitoring After Initial Verification

Many compliance programs focus heavily on onboarding but fail to monitor customers continuously. Changes in customer behavior, ownership, or risk profile often go undetected until a payment is flagged downstream. This reactive approach disrupts cross-border payments and increases false positives during transaction screening.

Underpinning these compliance controls, AiPrise’s KYC and KYB verification helps fintechs automate identity checks, monitor evolving risk signals, and stay aligned with changing cross-border regulations.

Fraud Risks Unique to Cross-Border Card Transactions

Cross-border card transactions expose fintechs to fraud patterns that are harder to detect, investigate, and contain at scale.

Here are the fraud risks that intensify specifically when card payments move across borders:

- Higher card-not-present fraud rates emerge because cross-border transactions rely entirely on digital signals without physical verification.

- Synthetic identity fraud scales more easily across regions, as fragmented data sources fail to connect fabricated identities early.

- Data mismatches increase false positives, since address formats, naming conventions, and identity documents vary significantly by country.

- Account takeover attacks spread faster internationally, with compromised credentials reused across multiple markets and merchants.

- Velocity-based fraud becomes harder to detect, as transactions span time zones, currencies, and merchant categories simultaneously.

- Mule networks exploit cross-border corridors, rapidly moving funds through multiple jurisdictions before controls activate.

- Device and IP-based signals lose reliability due to VPN usage, shared infrastructure, and inconsistent regional device data.

- Chargeback recovery is slower and costlier, involving multiple banks, currencies, regulatory frameworks, and dispute timelines.

- Delayed fraud visibility increases loss exposure, as cross-border settlement cycles slow investigation and response efforts.

Also read: Navigating Cross-Border Payment Regulations

Speed adds another layer of complexity, especially when settlement timelines don’t match customer or business expectations.

Speed and Settlement Challenges in Visa Card Payments

Speed and settlement inefficiencies directly affect cash flow, customer experience, and operational predictability for fintechs processing cross-border card payments.

The table below highlights where delays typically occur and why they matter at scale:

These challenges become even more pronounced when card payments involve businesses rather than individual consumers.

Why Corporate Use Cases Need Stronger Verification?

Corporate cross-border card payments introduce higher risk exposure than consumer transactions due to larger values, complex structures, and regulatory scrutiny.

Below is a detailed breakdown of why stronger verification is critical for corporate cross-border use cases:

- Corporate entities present more complex identity structures

- Businesses often operate through subsidiaries, SPVs, or holding companies across multiple jurisdictions

- Ultimate Beneficial Ownership (UBO) data may be fragmented, outdated, or intentionally obscured

- Shell companies and pass-through entities are frequently used to disguise illicit activity

- Transaction values and velocity are significantly higher

- Corporate card payments typically involve larger ticket sizes than consumer transactions

- Higher values amplify losses when fraud or compliance failures occur

- Rapid transaction velocity across borders makes post-transaction remediation harder

- KYB requirements are deeper than individual KYC

- Verification must include:

- Business registration authenticity

- Ownership and control structures

- Nature of business operations and revenue sources

- Gaps in KYB checks often go unnoticed until a transaction is flagged downstream

- Verification must include:

- Cross-border corporate payments face elevated AML scrutiny

- Regulators closely monitor corporate cross-border flows for:

- Trade-based money laundering

- Sanctions evasion

- Use of intermediaries in high-risk jurisdictions

- Regulators closely monitor corporate cross-border flows for:

- Corporate fraud patterns are harder to detect

- Fraud often blends into legitimate business activity, such as:

- Inflated invoices

- Repeated low-value transactions to avoid thresholds

- Misuse of corporate cards by authorized employees

- Traditional consumer-focused fraud tools fail to identify these patterns

- Fraud often blends into legitimate business activity, such as:

- In June 2025, U.S. banking regulators jointly issued a request for information specifically on mitigating payments fraud, reflecting heightened institutional concern across payment types, including cross-border flows.

- Regulatory expectations are higher for corporate payment providers

- Fintechs acting as visa cross-border corporate payments providers are expected to:

- Maintain auditable KYB records

- Perform continuous monitoring, not one-time verification

- Demonstrate proactive risk management to regulators

- Fintechs acting as visa cross-border corporate payments providers are expected to:

- Operational failures scale faster in corporate use cases

- One poorly verified corporate account can impact:

- Multiple merchants

- Multiple currencies

- Multiple downstream partners

- This creates cascading compliance, fraud, and settlement issues across the payment ecosystem

- One poorly verified corporate account can impact:

Also read: Making Cross-Border Payments Safer and Easier Through Compliance

To handle these pressures consistently, fintechs need internal alignment across systems, teams, and controls.

What Fintechs Must Align to Scale Visa Cross-Border Payments?

Scaling Visa cross-border payments requires tight alignment across technology, risk, compliance, and operations to avoid friction as volumes grow.

Here’s what fintechs must align to scale cross-border card payments sustainably:

.png)

- End-to-end payment orchestration that connects authorization, FX handling, clearing, settlement, and reconciliation into a single flow

- Consistent KYC and KYB standards applied across regions to reduce data mismatches and manual compliance reviews

- Real-time fraud and risk controls tuned specifically for cross-border card-not-present transaction patterns

- Transparent FX pricing and reconciliation processes to protect margins and reduce post-settlement disputes

- Scalable compliance infrastructure that adapts quickly to regulatory changes without disrupting live payment flows

- Unified data visibility across teams so product, risk, compliance, and operations work from the same transaction insights

- Automated exception handling and case management to prevent operational bottlenecks as transaction volumes increase

- Clear internal ownership models defining accountability across payments, risk, and compliance functions

This alignment is where the right technology stack starts to make a measurable difference.

How AiPrise Supports Secure Cross-Border Card Payments?

Secure scaling of Visa cross-border card payments depends on strong identity assurance, continuous risk monitoring, and automation across compliance workflows.

Here’s how AiPrise supports fintechs operating complex cross-border card environments:

- KYC verification enables fast, accurate identity checks using government verifications, proof of address, and document insights to reduce onboarding friction

- KYB verification validates business legitimacy, ownership structures, and operational authenticity for cross-border corporate card payment use cases

- Fraud and risk scoring applies AI-driven analysis to identify high-risk behaviors early in cross-border card-not-present transactions

- Compliance Co-Pilot supports ongoing regulatory alignment through watchlist screening, reverification, and continuous risk signal monitoring

- One Click KYC simplifies repeat verification flows, improving customer experience without weakening compliance controls

- Onboarding SDK integrates seamlessly into payment flows, enabling identity checks without disrupting authorization or settlement processes

- Case management and workflows centralize investigations, streamline reviews, and reduce manual intervention as transaction volumes scale

Together, these capabilities help fintechs strengthen trust, reduce fraud exposure, and maintain compliance without slowing down cross-border card payments.

Final Thoughts

Visa cross-border payments only scale smoothly when fintechs get compliance, fraud controls, FX handling, and operational alignment right from the start. As volumes grow, even small gaps in identity verification, risk monitoring, or settlement visibility can quickly turn into costly failures. By combining KYC, KYB, fraud and risk scoring, and automated compliance workflows, AiPrise helps fintechs secure cross-border card payments without adding friction or operational drag.

Ready to strengthen your Visa cross-border payment flows? Book A Demo to see how AiPrise supports secure, compliant global card payments.

FAQs

1. What are Visa cross-border payments?

Visa cross-border payments are card transactions where the cardholder and merchant are located in different countries, requiring international processing, FX conversion, and settlement.

2. Why are Visa cross-border payments more expensive?

They involve additional FX spreads, interchange fees, compliance checks, and operational overhead compared to domestic card transactions.

3. How do fintechs reduce fraud in cross-border card payments?

Fintechs reduce fraud by combining strong identity verification, real-time risk scoring, behavioral analysis, and continuous monitoring across regions.

4. What compliance checks are required for cross-border card payments?

Cross-border card payments typically require KYC or KYB verification, sanctions and watchlist screening, and ongoing AML monitoring depending on transaction risk.

5. Why do corporate cross-border card payments need extra verification?

Corporate payments involve higher values, complex ownership structures, and greater AML exposure, making deeper KYB and continuous monitoring essential.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately