AiPrise

13 mins read

August 6, 2025

How to Spot a Fake Identity: A Guide to Combating Synthetic Fraud

Key Takeaways

Synthetic identity fraud is now the fastest-growing financial crime in the world, responsible for an estimated 80% of all new account fraud. It's projected to cost at least $23 billion in losses in the U.S. alone by 2030.

This type of fraud uses a mix of real and fabricated information to create fake identities that slip past traditional security measures, costing businesses billions in lost revenue and chargebacks.

This article explores the mechanics of how these fake identities are created, the key indicators to help you spot them, and the actionable solutions to protect your business's bottom line.

Key Takeaways

- Synthetic identity fraud involves combining real and fake information to create fraudulent identities.

- Fraudsters use stolen data, like Social Security numbers, and fabricate additional details to bypass security.

- Key indicators include mismatched information, sudden high credit activity, and inconsistent digital footprints.

- Advanced tools like biometric checks, document verification, and real-time data validation can help detect fraud.

- AiPrise provides a fast, AI-driven solution to spot synthetic identities and ensure compliance.

What is Synthetic Identity Fraud?

Let's say you're a bank, and you’ve just approved a loan for a new customer. Everything seems fine until the payments stop coming in. After some digging, you find out that the borrower was using a mix of real and fake details to create a synthetic identity. They’ve vanished, and your business is left with a hefty loss.

This is synthetic identity fraud, where criminals build fake identities using real information and some fabricated details. It’s difficult to catch because the identity looks legitimate on the surface.

For businesses like yours, this means rising chargebacks, increased fraud detection costs, and a growing sense of uncertainty. As a result, businesses are facing an increasing challenge in preventing these fraudulent activities. Here’s how:

- Easier Impersonation: With advanced technology, criminals can easily gather pieces of real information (e.g., stolen Social Security numbers, email addresses, and addresses) from various sources. This makes it simple to create convincing fake identities.

- Data Breaches: Large-scale data breaches have exposed millions of personal records, including Social Security numbers and other critical details. Once leaked, this data can be used to build synthetic identities without much effort.

- Automation Tools: Fraudsters now use automated tools to generate fake identities at scale, bypassing traditional security systems and making it harder to spot fraudulent activity.

- Deep Web and Dark Web Markets: The dark web has become a growing marketplace for stolen personal data, providing criminals with easy access to information they need to create fake identities, increasing the volume of synthetic fraud cases.

- Increased Complexity of Fraud: Fraudsters can now manipulate data across multiple platforms (e.g., credit reports, loan applications, social media) to make synthetic identities appear legitimate, complicating detection efforts for businesses.

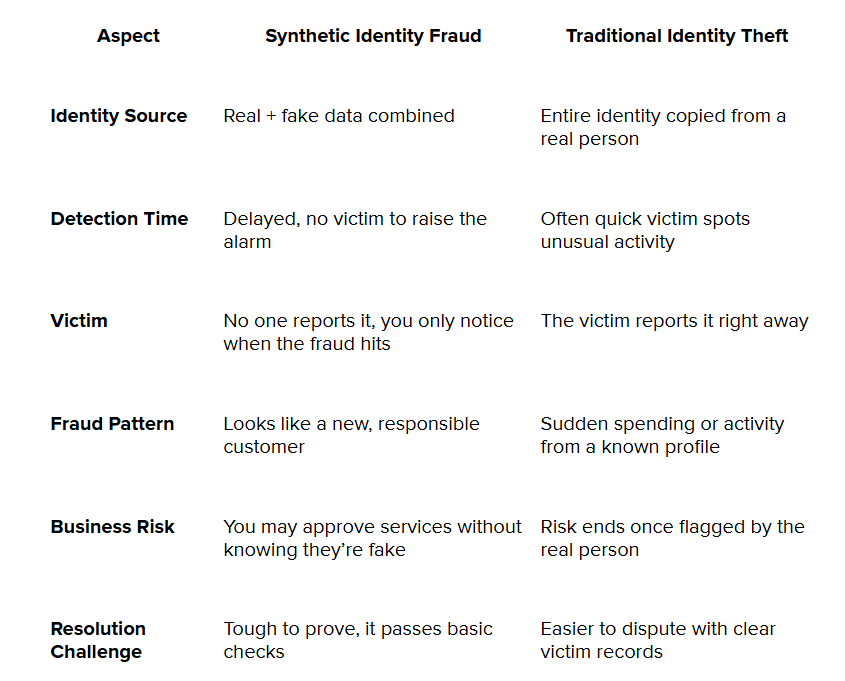

How Synthetic Identity Fraud Differs from Traditional Identity Theft

At first glance, synthetic identity fraud might look like regular identity theft, but the way it works (and how it hurts your business) is very different. Here’s how the two differ:

With that context in mind, let's explore how fraudsters build these fake identities and make them seem real.

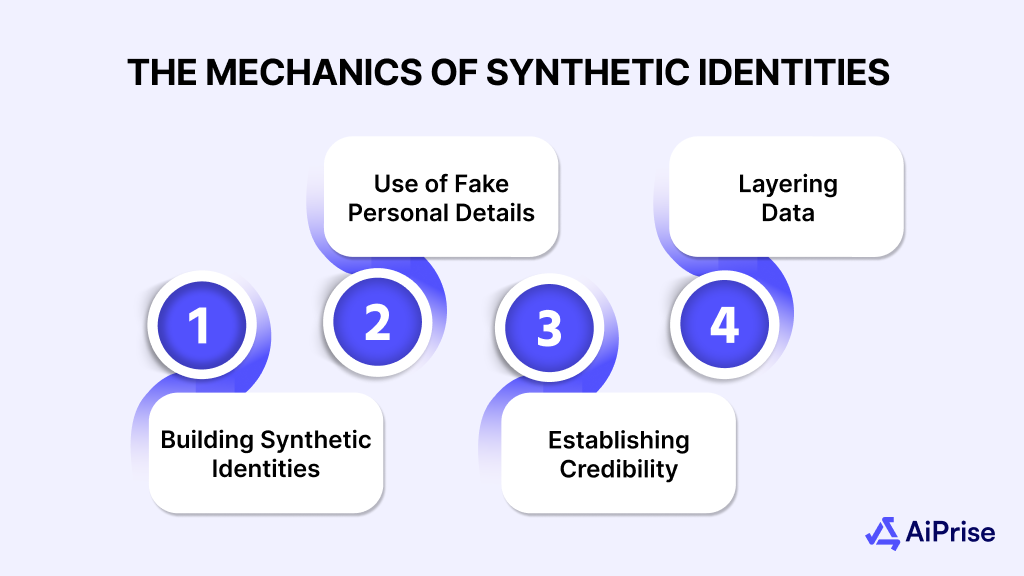

The Mechanics and Formation of Synthetic Identities

To the untrained eye, a synthetic identity can look legitimate. So, how exactly do criminals build a fraudulent identity from scratch? They use a structured process that combines real and fake data, often beginning with a key piece of information and building from there.

For businesses, the challenge lies in identifying these subtle discrepancies before they lead to financial losses.

Here’s a clearer breakdown:

- Building Synthetic Identities with Real Data:

Fraudsters often begin with real data, such as stolen Social Security numbers or birth dates, obtained from data breaches or the dark web. This real information serves as the foundation, providing an initial layer of legitimacy to the synthetic identity.

- Creation and Use of Fake Personal Details:

After establishing the real data, fake details are fabricated to complete the identity. These can include names, addresses, phone numbers, and employment history. The goal is to create a profile that appears legitimate when cross-checked against public or private databases.

- Establishing Credibility and Credit:

To strengthen the synthetic identity, fraudsters may apply for low-limit credit accounts or small loans, using the real Social Security number and fake personal details. By making on-time payments, they build a credit history that increases the perceived credibility of the identity.

This helps the fraudster gain higher credit limits and access more financial services.

- Layering Data Across Multiple Platforms:

Fraudsters often use synthetic identities across multiple platforms, including financial institutions, utility providers, and e-commerce websites. This spreads the identity’s footprint, making it harder to spot inconsistencies.

As the identity becomes more established across systems, it becomes more difficult to distinguish from a legitimate person.

Let’s look at the key indicators that can help your business spot these frauds before they cause damage.

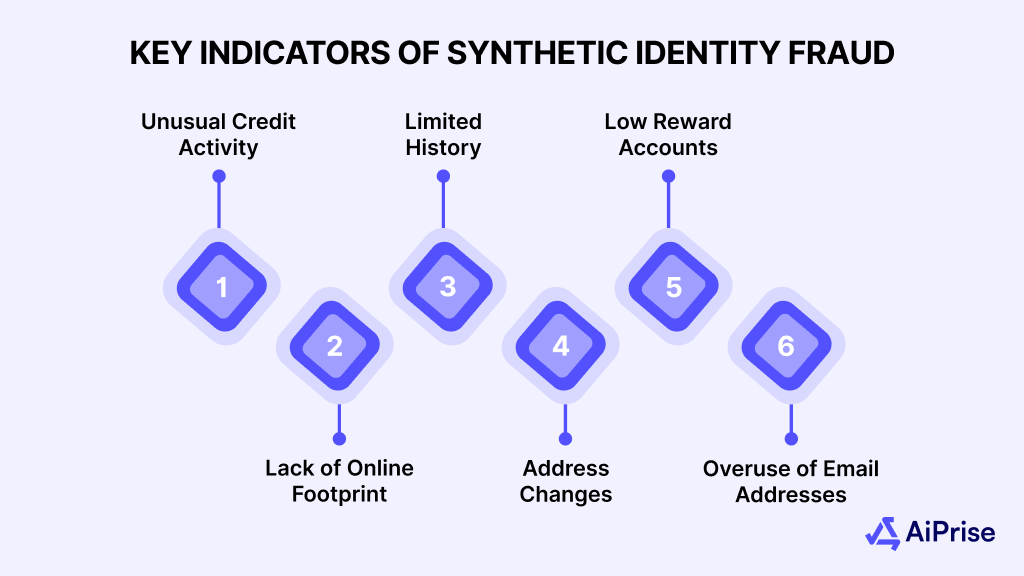

Key Indicators of Synthetic Identity Fraud

Synthetic identity fraud can be tough to spot, especially when fraudsters craft identities that appear legitimate. However, there are key indicators that can help you distinguish between real and fake identities. By recognizing these red flags early, you can minimize the risk to your business.

Below are the most common signs of synthetic identity fraud in businesses:

- Unusual Credit Activity:

A new account with a suddenly high credit limit and immediate large purchases is a red flag. For example, a person applying for a credit card might have no prior credit history but quickly max out the limit within weeks.

This could be a synthetic identity being built up quickly to exploit credit.

- Lack of Online Footprint:

A person with no digital footprint or an incomplete online history, especially when applying for loans or credit, is suspicious.

For example, someone with no prior social media activity or online presence, yet applying for high-limit credit cards, might be using a fabricated identity.

- No Credit File or Limited History:

A new identity with no significant credit history, yet qualifying for loans or other financial products, can be a sign. If someone with limited or no prior credit is approved for large loans or credit cards, it may be a synthetic identity crafted to seem credible.

- Multiple Address Changes:

Frequent or sudden address changes can signal a synthetic identity being established. Fraudsters may use different addresses across various accounts to mask their identity or establish false credibility.

- High Risk, Low Reward Accounts:

If someone opens multiple low-risk, low-reward accounts, such as store cards or utility services, and rarely uses them, they might be trying to build a credit history without raising suspicion.

These small accounts are stepping stones for creating a bigger fraudulent profile.

- Overuse of Temporary or Disposable Email Addresses:

Fraudsters often use throwaway or temporary email addresses when registering for services to avoid traceability. If you spot an unusually high number of accounts linked to temporary emails, it could be a sign of synthetic fraud in the making.

Understanding these key indicators is essential for tackling the risk of synthetic identity fraud head-on.

How to Combat Synthetic Identity Fraud?

Combating synthetic identity fraud requires a proactive approach that goes beyond just identifying fake identities. It’s about strengthening your processes, adopting advanced tools, and staying ahead of fraudsters’ tactics.

Over the years, the methods have evolved from simple paper-based checks to digital solutions, with advancements like biometrics and AI-driven technologies now playing a crucial role.

Let’s dive into the specific methods you can implement right away:

- Use Behavioral Biometrics for Continuous Authentication:

Instead of relying solely on static identification methods (like passwords or SSNs), implement behavioral biometrics. This technology tracks how users interact with your platform, such as typing speed, mouse movements, and even the way they scroll. It helps to continuously verify their identity without interrupting the user experience.

For example, a financial institution implemented this strategy and found that it significantly reduced fraudulent activities, as fraudsters couldn’t replicate natural user behavior even if they had access to real identity data.

- Integrate Cross-Industry Fraud Detection Tools:

Build partnerships with other industries to share anonymized fraud data and patterns. For example, collaborating with telecommunications companies can provide you access to data that highlights individuals who have recently moved across multiple phone carriers or address records.

Synthetic identity fraud often exploits gaps in one industry’s data, so sharing information can help you track suspicious activities across multiple touchpoints and strengthen your fraud prevention efforts.

- Use AI for Real-Time Identity Validation:

Traditional fraud detection methods rely on static rules that cannot adapt quickly to new fraud strategies. In contrast, AI uses machine learning to detect emerging patterns in real-time, making it more effective against evolving synthetic identity fraud. Instead, use machine learning algorithms that learn and adapt to new fraud patterns in real-time.

Retailers like Amazon are already implementing this with algorithms that instantly cross-check a new account’s details against historical fraudulent activities, catching potential fraud before it escalates.

- Monitor for Disjointed Social Media Footprints:

Synthetic identities may look legitimate at first, but often have incomplete or contradictory digital footprints. Invest in a social media analysis tool that checks the consistency of the identity across platforms.

For example, if the name on a credit card application matches a real person, but their social media profile only has basic or no activity, it could signal a synthetic identity.

- Implement Micro-Transactions for Validation:

A powerful strategy often overlooked by businesses is the use of micro-transactions. When a new user signs up for an account, you could initiate a small transaction, like charging them $1 for verification.

Micro-transactions act as a verification step because legitimate users usually confirm small charges, while fraudsters avoid responding to these, allowing businesses to identify and block synthetic identities early.

This method, used by some e-commerce platforms, has helped reduce fraudulent sign-ups by weeding out synthetic accounts right at the start.

- Use Geolocation for Cross-Checking Identity Movement:

Fraudsters building synthetic identities often change their locations frequently, creating an inconsistent trail. By integrating geolocation data with identity verification, you can track an applicant’s real-time location and compare it with their claimed address.

For example, if a user consistently changes locations across various states within short periods, this could indicate synthetic identity behavior.

Businesses like banks have implemented this with success, reducing the risk of synthetic identities linked to identity theft.

While the challenge is significant, the right tools and strategies can help you detect fraud early and reduce its impact.

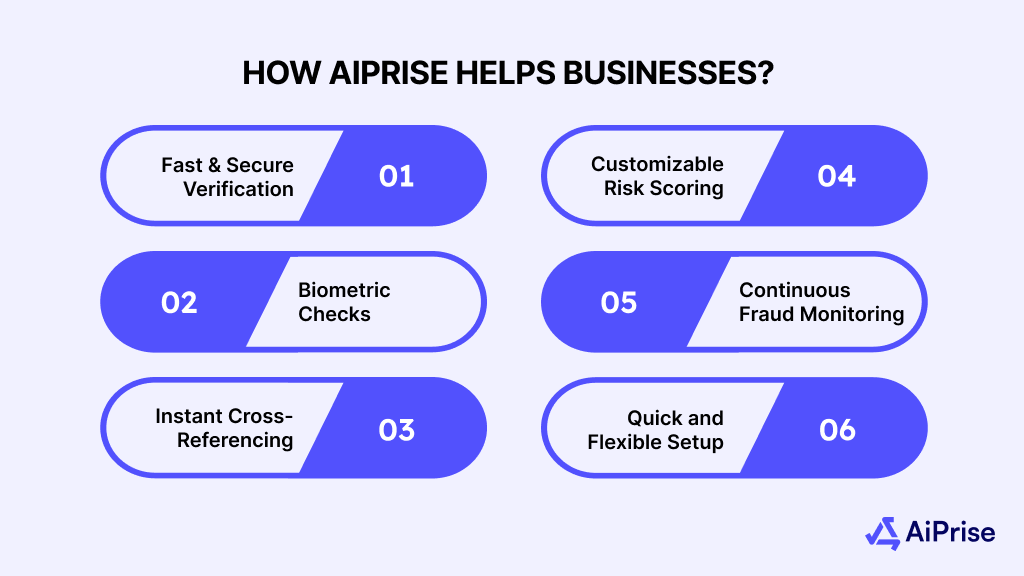

How AiPrise Helps Businesses Prevent Synthetic Identity Fraud

AiPrise offers a robust identity verification platform specifically built to help businesses detect and prevent synthetic identity fraud.

Here’s how AiPrise helps businesses combat synthetic identity fraud during digital onboarding:

- Fast and Secure Verification: Verifies IDs from 200+ countries in under 30 seconds using AI-driven OCR, barcode/MRZ scanning, and security feature checks for over 12,000 document types.

- Biometric Checks: Performs facial recognition and liveness detection to prevent spoofing, deepfakes, and synthetic identities.

- Instant Cross-Referencing: Integrates with 800+ data sources to cross-check identities against government, credit, and sanctions lists, ensuring global KYC and KYB compliance.

- Customizable Risk Scoring: Tailors onboarding flows with a customizable rule engine and automated risk scoring, reducing manual review time by up to 95%.

- Continuous Fraud Monitoring: Provides real-time alerts, adverse media scans, and ownership checks to monitor identity risk beyond the onboarding process.

- Quick and Flexible Setup: Offers a white-label UI, API, SDK support, and multi-language capability for fast deployment with minimal disruption to your operations.

AiPrise helps you verify identities, spot fraud, and stay compliant all in one place, without slowing things down.

Conclusion

Effective identity verification is key to stopping synthetic identity fraud before it begins. With the right tools in place, you can identify fake identities, meet KYC requirements, and streamline your onboarding process without delays.

It's not just about staying compliant, it’s about staying ahead of fraudsters and protecting your business from synthetic ID scams.

Want to reduce the risks of synthetic identity fraud? Book A Demo with AiPrise to see how the platform fits into your workflow and helps you stay secure and compliant.

FAQs

1. What is synthetic identity fraud?

Synthetic identity fraud involves criminals combining real and fake information to create fraudulent identities that appear legitimate. This often includes using real Social Security numbers and pairing them with fabricated names, addresses, or employment details to open accounts, obtain credit, or commit fraud.

2. How do fraudsters create synthetic identities?

Fraudsters start with real data, like stolen Social Security numbers, then add fake details such as names, addresses, and phone numbers. They build a fake profile that seems valid, and over time, use it to establish credit, rent properties, or commit financial fraud.

3. How can synthetic identities affect my business?

Synthetic identities can lead to financial losses, chargebacks, and reputational damage. Fraudsters may use these identities to open fake accounts, apply for loans or credit, and rack up debt, all under your business’s radar, making detection difficult until it's too late.

4. What are the key indicators of synthetic identity fraud?

Some red flags include mismatched information across platforms, sudden high credit activity without history, inconsistent personal details, and digital footprints that don't align with a person's claimed identity. Monitoring these signs helps prevent fraud before it escalates.

5. How can AiPrise help prevent synthetic identity fraud for my business?

AiPrise offers advanced identity verification tools like biometric checks, document verification, and real-time cross-referencing against trusted data sources. These features help you identify and block synthetic identities at the onboarding stage, reducing fraud risk and ensuring compliance.

6. Can AiPrise help with compliance and regulatory requirements?

Yes, AiPrise supports global KYC (Know Your Customer) and KYB (Know Your Business) compliance by cross-referencing identity data with government, credit, and sanctions lists, ensuring your business meets all regulatory standards while preventing synthetic identity fraud.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately