AiPrise

11 min read

December 4, 2025

KYC and AML in France: How Identity Verification Works

Key Takeaways

France’s financial sector faces a growing challenge: keeping transactions secure while meeting strict compliance obligations. Mounting fraud attempts, evolving AML expectations, and rising operational costs are stretching compliance teams thin. Businesses need efficient KYC processes that not only verify identities but also protect customer data and build regulatory trust. Data security investments in France are projected to reach US $191.73 million, highlighting how organizations are prioritizing stronger systems to prevent illegal transactions and data breaches. Recognizing how know your customer français practices fit into this context helps strengthen compliance frameworks, minimize financial risk, and safeguard both reputation and revenue.

Quick Overview

- France’s know your customer français and AML laws require strict identity checks, risk-based monitoring, and ongoing due diligence for all regulated entities.

- Acceptable IDs include passports, national IDs, residence permits, and verified address proofs, with remote KYC allowed under specific French regulations.

- Crypto platforms, payment providers, and financial institutions must register with regulators, apply enhanced checks, and report suspicious transactions to TRACFIN.

- Non-compliance can lead to heavy fines, criminal liability, and reputational damage, making accurate verification and continuous monitoring essential for every business.

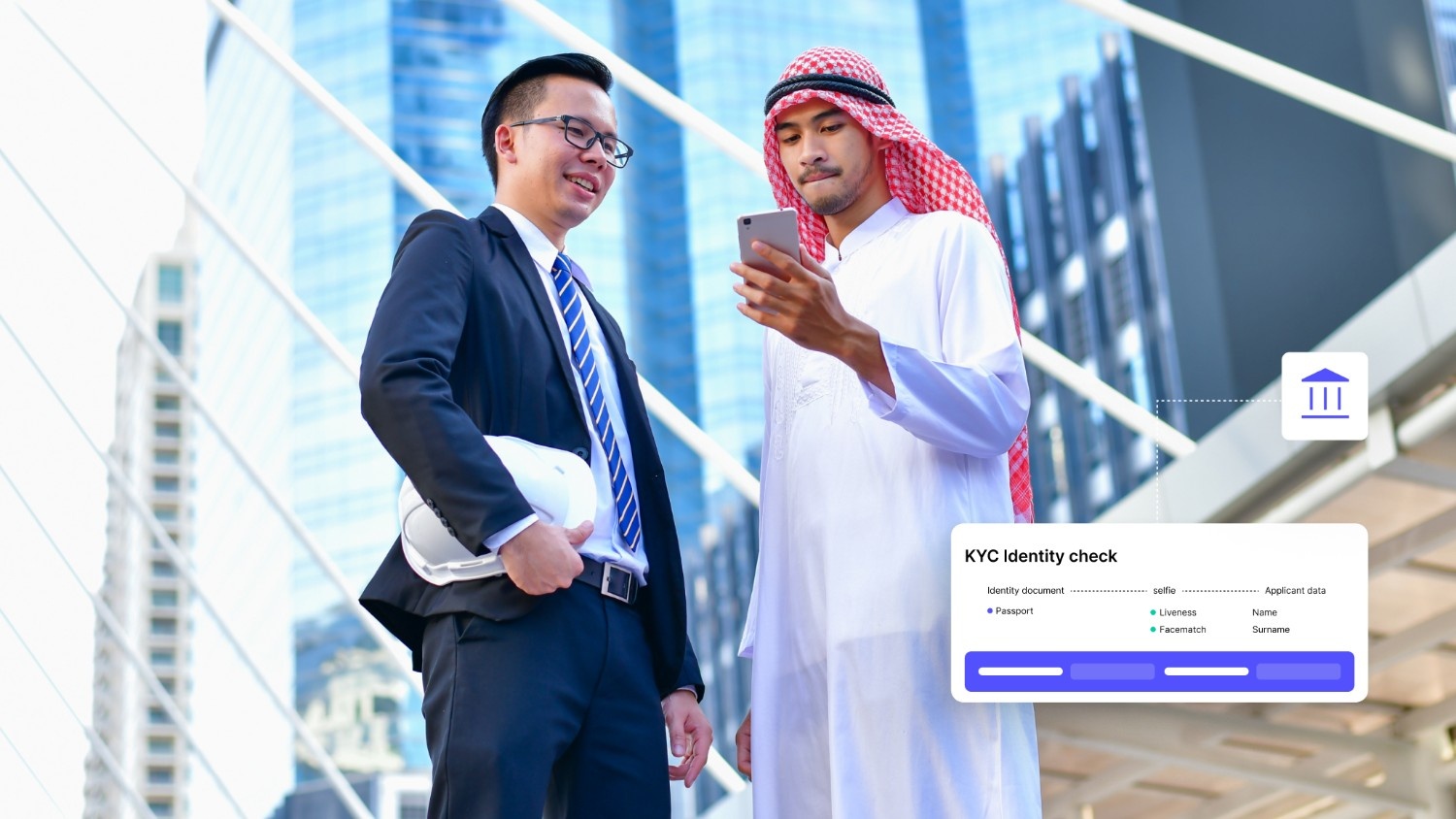

What Is KYC?

Know Your Customer (KYC) refers to the process of verifying a customer’s identity before granting access to financial products or services. In the French regulatory landscape, know your customer français is a legal requirement under the Monetary and Financial Code to prevent fraud, terrorism financing, and money laundering. Financial institutions and fintechs rely on KYC to confirm that customers are who they claim to be by collecting and validating official identification documents. This process also involves assessing customer risk profiles and ensuring compliance with data protection laws such as GDPR. By implementing strong KYC procedures, your business safeguards its reputation, builds regulatory trust, and reduces costly compliance penalties.

How KYC & AML Work in French Law?

French financial compliance rests on an advanced know your customer français framework built to prevent fraud and money laundering. Here are the essentials every business operating in France must understand:

- French AML laws stem from the EU’s 6th Anti-Money Laundering Directive (6AMLD) and are transposed into national law under the Code Monétaire et Financier.

- The ACPR (Autorité de Contrôle Prudentiel et de Résolution) and the AMF (Autorité des Marchés Financiers) enforce these regulations and oversee your institution’s compliance.

- A risk-based approach is mandatory: due diligence intensity should depend on the customer’s risk level, transaction size, and jurisdiction exposure.

- You’re expected to identify ultimate beneficial owners (UBOs) and verify their identities before onboarding or extending services.

- Continuous monitoring and reporting to TRACFIN, France’s financial intelligence unit, is a legal obligation for all regulated entities.

- Data privacy and KYC compliance now intersect, requiring GDPR-aligned record-keeping and secure storage of verification data.

Also read: KYC onboarding and AML considerations

With the basics clear, it’s time to look at how France’s legal system structures KYC and AML compliance, and what rules guide every verification process.

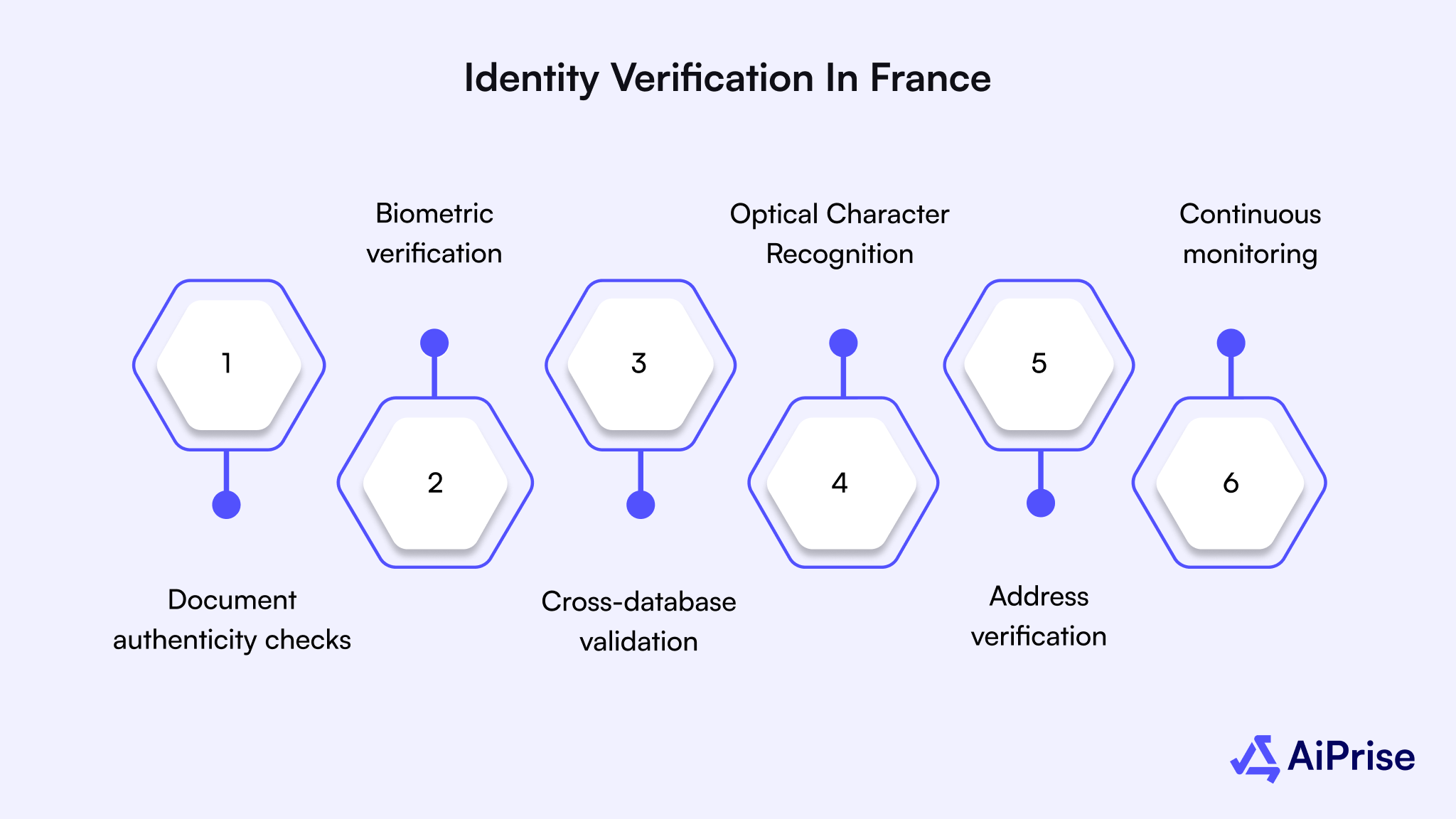

Identity Verification in France

Identity verification is the foundation of know your customer français, ensuring that individuals and businesses are genuinely who they claim to be before any transaction takes place. In France, this verification combines both legal compliance and advanced technology.

Here are the key aspects that define this process:

- Document authenticity checks confirm that passports, national IDs, or residence permits are valid, untampered, and match database records.

- Biometric verification—including facial recognition, liveness detection, and fingerprint comparison—helps confirm real-time identity during onboarding.

- Cross-database validation connects user data with government registries and sanctions lists to detect anomalies or fraudulent profiles.

- Optical Character Recognition (OCR) systems automatically extract and validate text from scanned ID documents, reducing manual errors.

- Address verification relies on trusted documents like utility bills, ensuring residency consistency with the provided identity.

- Continuous monitoring detects suspicious activity or data inconsistencies even after onboarding, fulfilling AML obligations.

Understanding the legal framework is just the beginning; the real challenge comes in applying it through everyday identity checks, particularly within France’s evolving digital onboarding landscape.

Entities That Must Comply in France

French know your customer français laws apply broadly, covering both financial and non-financial professionals.

Here’s who needs to pay attention:

- Banks and credit institutions must perform full KYC and AML checks at onboarding and throughout client relationships.

- Insurance and investment firms are legally obligated to identify policyholders and beneficiaries under Article L.561-2 CMF.

- Payment and electronic money institutions must verify senders and recipients in any transaction exceeding thresholds set by ACPR.

- Crypto-asset service providers (CASPs) and exchange platforms must register with AMF and comply with full AML/KYC due diligence.

- Lawyers, notaries, and accountants fall under “designated non-financial businesses” when handling financial transactions.

- Real-estate agents and luxury-goods merchants also fall within the scope when high-value transactions occur in cash or crypto.

Stay compliant effortlessly with AiPrise’s all-in-one verification platform.

With the key players outlined, the next step is understanding what counts as valid identification in France and which documents meet official KYC requirements.

Acceptable ID Documents in France

Compliance with the know your customer français rules means verifying authentic, valid IDs that meet French and EU standards. Here are the accepted identification options:

- Passport (French or foreign) with a clear biometric page, suitable for both face-to-face and remote onboarding.

- Carte Nationale d’Identité (CNI) or Titre de Séjour, mandatory for French residents or foreign nationals living in France.

- Driver’s licence, secondary proof accepted only when paired with proof of address (utility bill or rent receipt).

- Proof of address documents such as recent electricity, gas, or water bills are compulsory for validating residence information.

- K-bis extract and SIREN registration serve as official business identity proofs for KYB verification.

- For enhanced due diligence (EDD) cases, combine document validation with biometric verification and sanction-list screening.

Also read: Steps to Know Your Customer (KYC) Compliance and Reducing Fraud

Physical IDs aren’t the only route anymore; remote KYC has become a game-changer in how businesses verify customers while staying compliant.

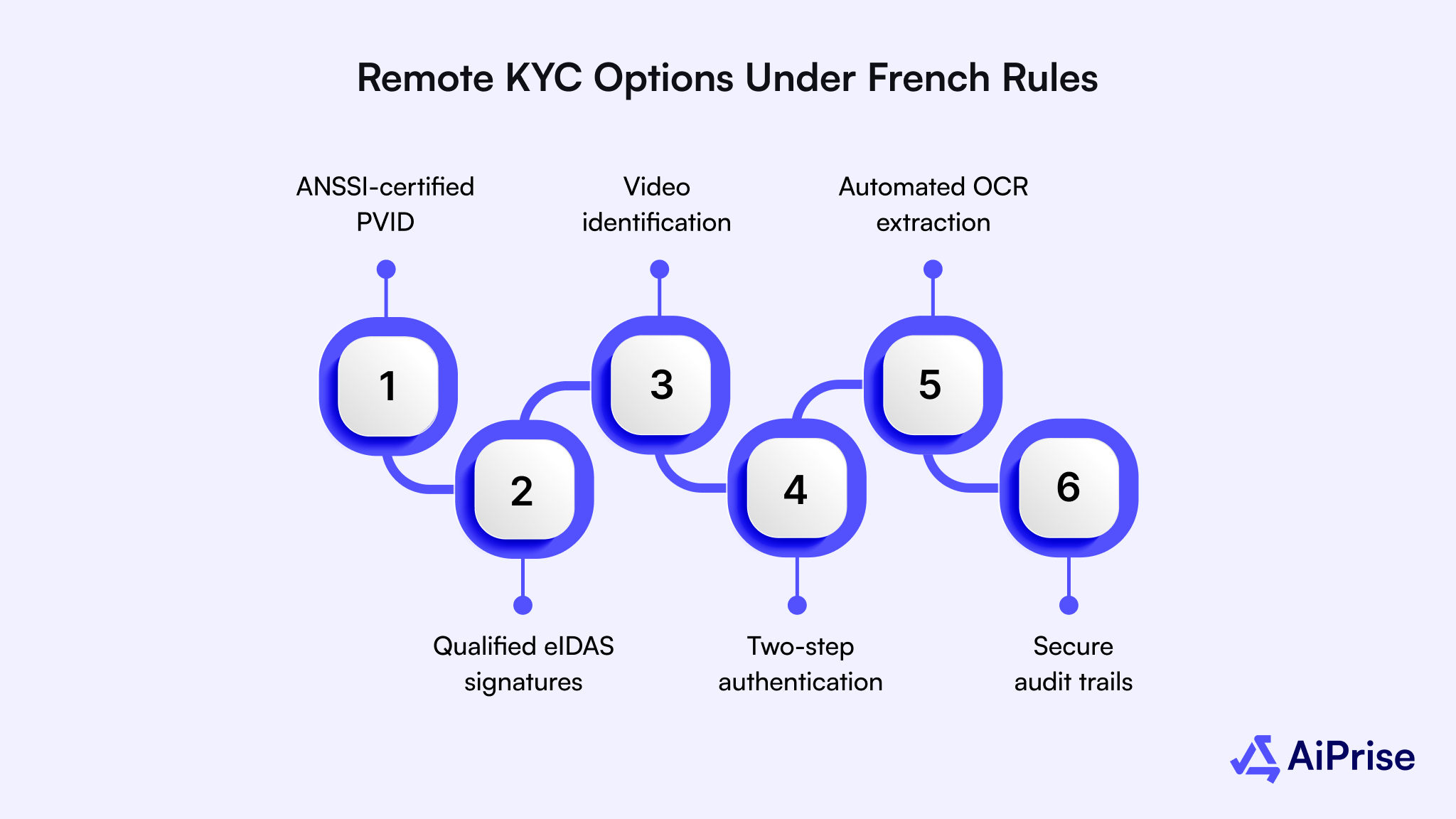

Remote KYC Options Under French Rules

Digital onboarding is central to modern know your customer français compliance, but strict rules govern how remote checks are done.

Here are the approved options and methods:

- ANSSI-certified PVID (Processus de Vérification d’Identité Dématérialisé) tools are recognized for secure remote identity verification.

- Qualified eIDAS signatures or trusted digital IDs can replace in-person verification for low-risk profiles.

- Video identification must include live presence detection and comparison between video feed and ID photo.

- Two-step authentication, document check + biometric verification, ensures compliance with Article R561-5-2 standards.

- Automated OCR extraction of ID data helps prevent human error and maintain accuracy during onboarding.

- Secure audit trails must store timestamps, IP addresses, and user interactions for regulatory inspection readiness.

While remote verification opens doors for convenience, sectors like crypto and payments face far tighter expectations, and that’s where due diligence becomes non-negotiable.

KYC for Crypto Platforms & Payments

In France, crypto and payment ecosystems face tighter know your customer français expectations to combat fraud and anonymity abuse.

Here are the compliance practices to follow:

- Crypto-asset service providers (CASPs) must obtain AMF approval before operating and apply full AML controls.

- Payment processors and fintechs must conduct customer and merchant due diligence, even for micro-transactions, to avoid cumulative risk.

- Enhanced verification applies to customers engaging in high-volume crypto trades or cross-border remittances.

- Transaction-pattern analysis tools should flag anomalies such as frequent small deposits or mixing-service usage.

- Wallet-ownership validation (linking user data with wallet IDs) is recommended for blockchain-based payments.

- Continuous re-screening against global sanctions and PEP lists ensures compliance with evolving AML directives.

These evolving standards highlight how essential it has become for digital payment and crypto businesses to integrate AiPrise’s real-time verification tools into their compliance framework. Even with best practices in place, businesses that slip up on compliance face more than financial losses; the penalties can reshape their entire operation.

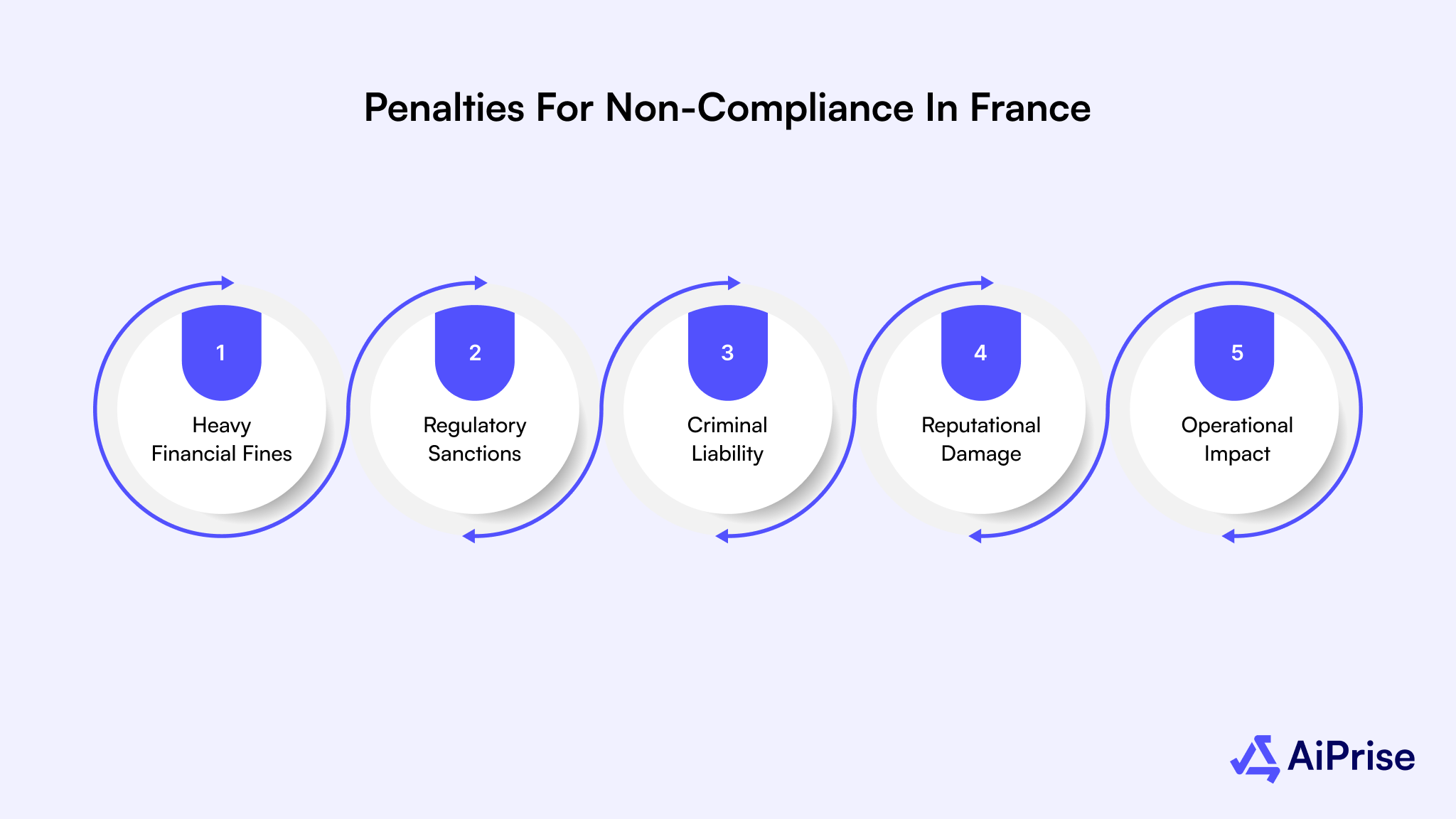

Penalties for Non-Compliance in France

Failing to comply with the know your customer français and AML regulations in France can lead to significant financial, legal, and reputational consequences. French authorities enforce strict penalties to ensure that institutions maintain robust verification and reporting standards.

Here are the main repercussions to be aware of:

- Heavy Financial Fines: Non-compliance can result in fines ranging from €5 million to 10% of annual turnover, depending on the severity and duration of the violation, as outlined in the Code Monétaire et Financier.

- Regulatory Sanctions: The ACPR and AMF may impose sanctions, including operational restrictions, suspension of licenses, or public reprimands that damage credibility and investor trust.

- Criminal Liability: In cases of willful negligence or facilitation of money laundering, executives and compliance officers may face personal liability, including imprisonment of up to five years and individual fines.

- Reputational Damage: Publicized enforcement actions can lead to loss of clients, reduced investor confidence, and long-term harm to brand integrity within the French and EU markets.

- Operational Impact: Failure to meet ongoing monitoring and reporting obligations may result in heightened regulatory scrutiny, delays in business expansion, or complete revocation of operating authorization.

Also read: Importance of KYC and AML for Crypto Exchanges

Avoiding penalties isn’t just about ticking boxes; it requires continuous monitoring and quick action when suspicious activity arises.

AML Monitoring & Suspicious-Activity Reporting

Strong AML monitoring keeps your know your customer français program legally compliant and risk-resilient.

Here’s how to structure this process effectively:

1. Implementing Ongoing Monitoring

An advanced monitoring setup analyzes customer transactions in real time, spotting deviations from normal behavior. Alerts should trigger when thresholds, geographies, or counterparties fall into high-risk categories. The ACPR recommends using AI-enhanced systems to streamline these reviews while maintaining accuracy.

2. Submitting Suspicious Activity Reports (SARs)

When unusual activity persists or cannot be justified, a SAR must be filed with TRACFIN immediately. The report can be submitted electronically through Télé-DS, accompanied by supporting documentation. Keeping internal escalation paths short ensures faster, compliant filing.

3. Maintaining Audit Trails

All verifications, risk scores, and decision logs must be archived securely for at least five years after the relationship ends. These audit trails support inspections from regulators like ACPR or AMF. Comprehensive documentation demonstrates a proactive compliance culture, reducing enforcement exposure.

4. Staff Training & Awareness

Regular internal training ensures every team member recognizes red flags in customer behavior. Refresher sessions keep compliance staff updated on new French AML rules. Embedding this awareness culture minimizes reporting errors and improves overall AML readiness.

5. Utilize Technology & Automation

Adopting automated case-management tools enhances oversight across onboarding and monitoring workflows. AI-driven analytics help you prioritize genuine alerts over false positives. Integrating these tools reduces operational strain and increases compliance efficiency.

6. Internal Review & Continuous Improvement

Periodic audits and internal reviews validate the strength of your monitoring system. These evaluations identify weak points before regulators do. Regular updates to algorithms and risk matrices maintain alignment with France’s evolving AML framework.

To manage these obligations efficiently, having the right tools and local integrations can make compliance far less complicated, and that’s where tailored solutions come in.

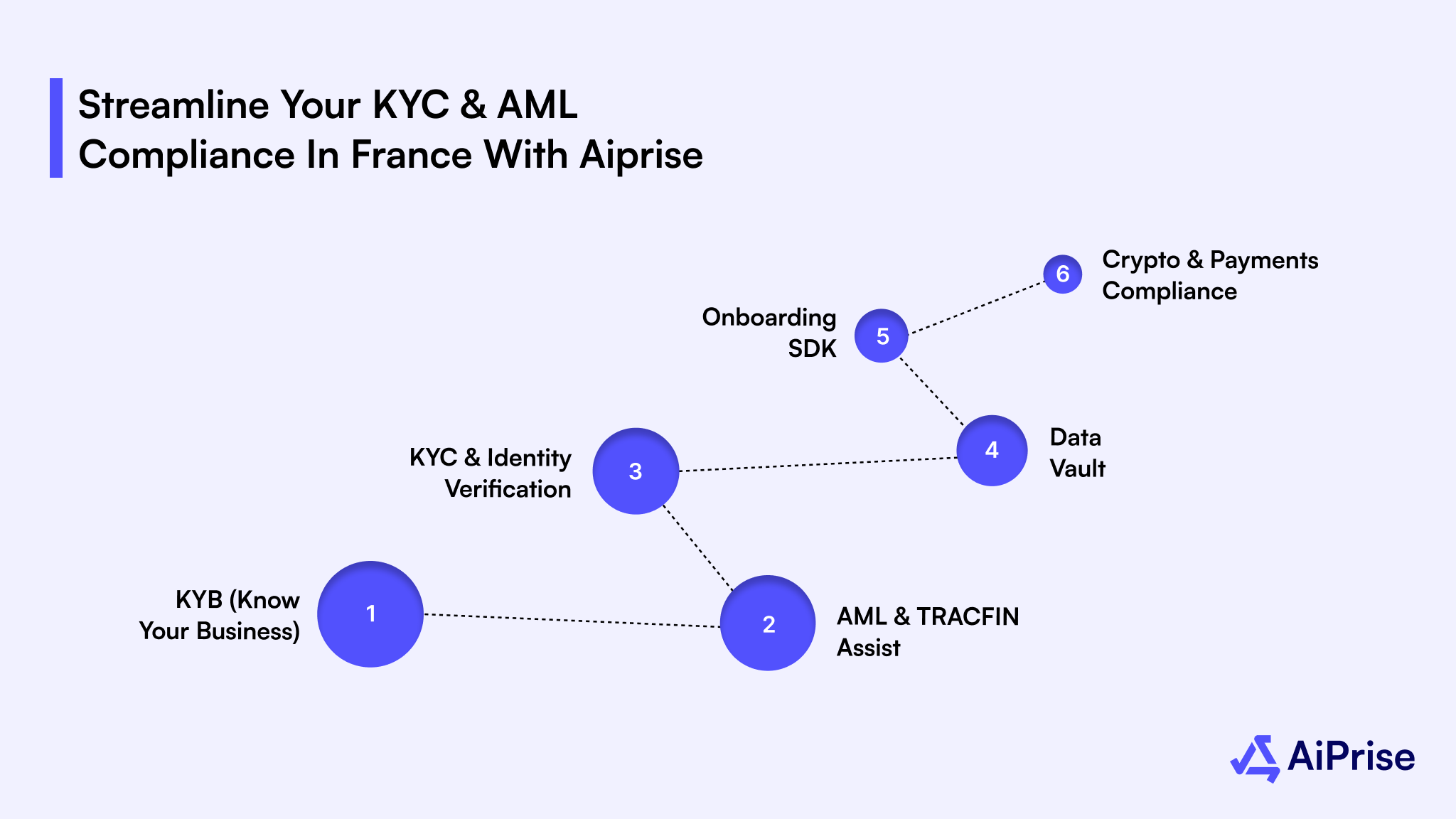

Streamline Your KYC & AML Compliance in France With Aiprise

Tailored for the French market, this offering maps know your customer français workflows to local law, language, and data sources.

Here are the France-specific capabilities to help keep onboarding fast and regulator-ready:

- KYB (Know Your Business): instantly validates K-bis extracts, SIREN/SIRET records, and corporate filings through official registries, ensuring accurate French business verification and faster decisioning.

- AML & TRACFIN Assist: automates suspicious-activity data collection, prepares TRACFIN-ready SARs, and aligns reports with French evidence and metadata standards.

- KYC & Identity Verification: supports Carte Nationale d’Identité, titre de séjour, and passport checks with ANSSI-certified PVID workflows and eIDAS-compliant remote onboarding.

- Data Vault: enforces GDPR-aligned data-residency controls, retention policies, and access logs to simplify privacy audits and secure customer information.

- Onboarding SDK: offers a fully localized French interface with address validation, telecom data checks, and branded flow customization to reduce friction and abandonment.

- Crypto & Payments Compliance: delivers CASP-grade enhanced due diligence, wallet verification, and transaction-pattern analytics to meet France’s AML and crypto-asset standards.

Wrapping Up

Navigating know your customer français and AML compliance in France demands more than just meeting regulations; it requires precision, agility, and trust. By understanding how identity verification works within the French legal and operational landscape, your business can reduce risk, stay compliant, and deliver a secure onboarding experience that builds lasting credibility.

AiPrise brings all these elements together with AI-driven tools that simplify KYC, KYB, and AML processes while ensuring local compliance with French and EU regulations. From document verification to ongoing monitoring, AiPrise helps you stay ahead of fraud and compliance challenges effortlessly.

Book A Demo today to future-proof your verification workflows and scale compliance with confidence.

Frequently Asked Questions (FAQ)

1. What documents are required for KYC in France?

For KYC in France, acceptable documents include a valid passport, Carte Nationale d’Identité (CNI), or Titre de Séjour for foreign residents. Proof of address, such as a recent utility bill, rent receipt, or tax statement, is also required to confirm residency details.

2. Can KYC be completed remotely in France?

Yes, remote KYC is legally permitted in France under Article R561-5-2 of the Code Monétaire et Financier. Businesses can use certified PVID (Processus de Vérification d’Identité Dématérialisé) solutions, video identification, or eIDAS-qualified signatures for compliant digital onboarding.

3. Who regulates KYC and AML compliance in France?

KYC and AML compliance are supervised by two main authorities — ACPR (Autorité de Contrôle Prudentiel et de Résolution) for financial institutions and AMF (Autorité des Marchés Financiers) for investment and market entities. Reporting of suspicious transactions is handled by TRACFIN, France’s financial intelligence unit.

4. How long must KYC and AML records be kept in France?

Under French AML law, all KYC-related documents and transaction records must be retained for at least five years after the end of the customer relationship. This retention supports future audits, regulatory reviews, and law enforcement investigations.

5. What are the penalties for non-compliance with KYC and AML regulations in France?

Non-compliance can lead to severe administrative and criminal penalties, including hefty fines, license suspension, or reputational damage. The ACPR and AMF regularly issue sanctions against institutions that fail to implement effective customer due diligence and monitoring controls.

You might want to read these...

.jpeg)

.jpg)

.jpeg)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately