AiPrise

14 min read

January 23, 2026

Requirements for AML AI in Banking: The Ultimate Guide You Cannot Miss

Key Takeaways

Ever feel like your bank’s AML systems are struggling to keep up with modern financial crime? As transaction volumes rise and laundering methods grow more complex, traditional rule-based controls start generating more alerts, reviews, and risk. The impact often goes beyond inefficiency and can lead to real exposure to regulatory fines, delayed investigations, and reputational damage.

That's where AI comes into the picture. Understanding the requirements for AML AI in banking is now essential to improve detection accuracy and reduce compliance costs. In this blog, you’ll learn how AML regulations shape the use of AI in banking. You’ll also see how AI fits into real AML workflows and what it takes to apply it at scale.

Key Takeaways

- Static rules and manual reviews cannot keep pace with changing laundering tactics, leading to high false positives, rising costs, and missed risk.

- AI shifts AML from rules to behavior. It detects patterns across time, accounts, and entities, enabling earlier risk detection, dynamic scoring, and fewer unnecessary alerts.

- From KYC and transaction monitoring to SAR filing and sanctions screening, AI improves accuracy, speed, and consistency across the AML lifecycle.

- Successful AI adoption requires preparation. Data quality, explainability, system integration, and regulatory readiness are critical to moving from pilots to production-scale AML AI.

- AiPrise enables scalable, compliant AML AI solutions. With real-time risk scoring, automated screening, UBO transparency, and continuous monitoring, it helps you apply AI without adding complexity.

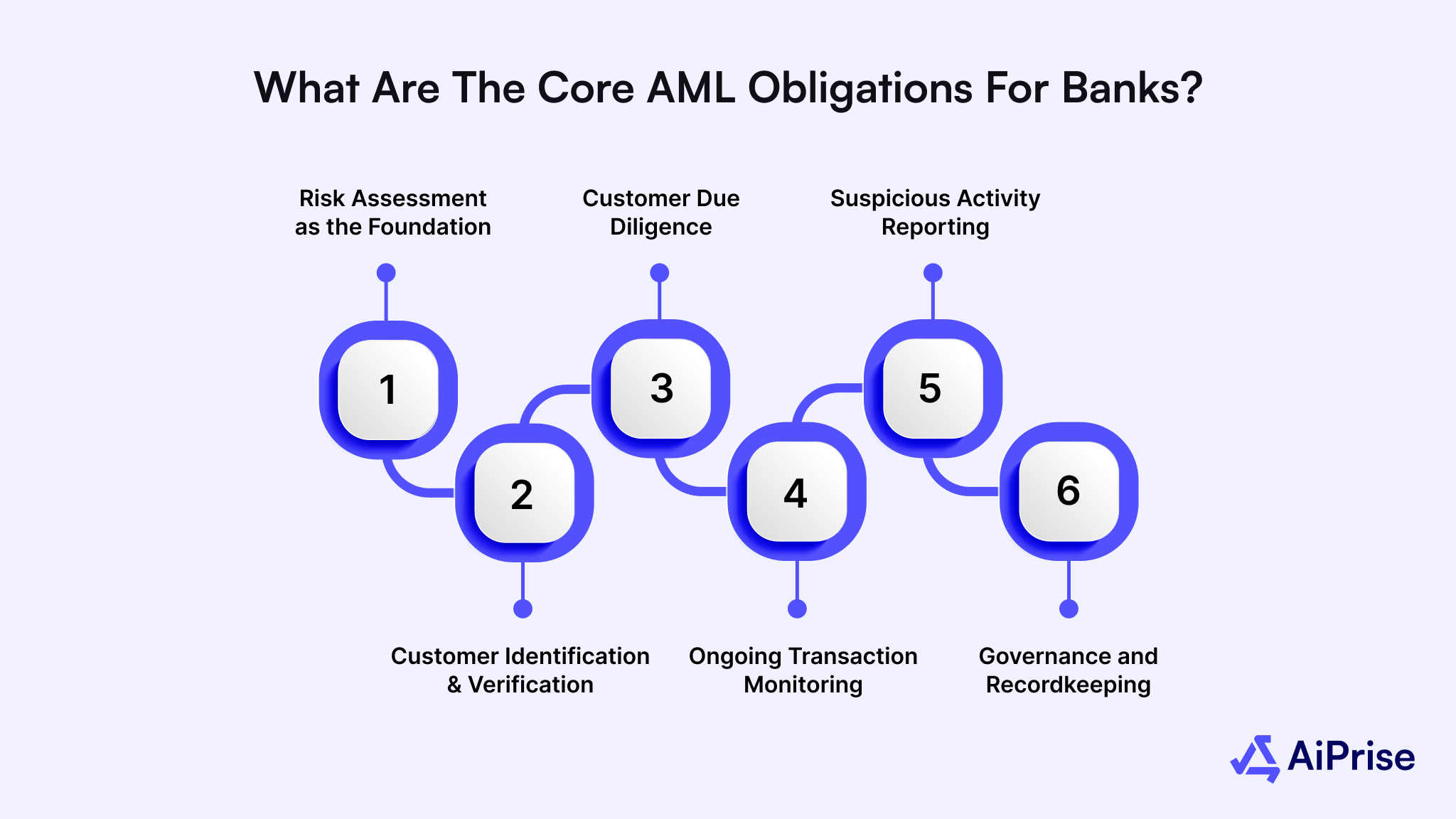

What are the Core AML Obligations for Banks?

As a bank, you are legally required to comply with strict AML regulations set by national regulators, such as the Bank Secrecy Act, and with global standards established by FATF. They define how you assess risk, onboard customers, monitor activity, and report suspicious behavior.

Below is a consolidated, structured view of the core AML requirements banks must meet today.

Risk Assessment as the Foundation

- You must identify and assess money laundering and terrorist financing risks across customers, products, geographies, and channels.

- It must be documented, reviewed regularly, and updated as your risk profile changes.

Customer Identification and Verification (KYC)

- You are required to identify and verify every customer before establishing a relationship.

- This includes verifying the customer and beneficial owner, and confirming the purpose of the account.

- Identity checks typically involve:

- Government-issued ID verification

- Face verification

- Proof of address, such as utility bills or bank statements

Customer Due Diligence (CDD)

- After KYC, you must assess the customer’s risk level.

- Customer data is screened against:

- Sanctions lists

- Politically Exposed Persons (PEP) databases

- Watchlists and government records

- Factors such as nationality, business activity, and transaction behavior influence risk ratings.

- Higher-risk customers require enhanced due diligence and closer monitoring.

Ongoing Transaction Monitoring

- You must continuously monitor customer transactions, not just at onboarding.

- Monitoring should reflect the customer’s risk profile and expected behavior.

- This includes transactions involving customers of other banks.

- You are required to:

- Detect unusual patterns or changes in behavior.

- Verify the source of large or unusual funds.

- Monitor cash transactions, including those exceeding $10,000.

Suspicious Activity Reporting (SAR)

- Any transaction suspected to involve criminal proceeds or terrorist financing must be reported to the national Financial Intelligence Unit (FIU).

- Reports must be complete, timely, accurate, and supported by clear audit trails.

Governance and Recordkeeping

- You must appoint a senior AML compliance officer with sufficient authority, resources, and expertise.

- Records related to KYC, CDD, transactions, and internal controls must be retained for the legally required period.

Practical Example: A customer opens a personal account and initially shows low-risk behavior. Over time, you notice frequent high-value international transfers that do not match their stated income. Further customer screening flags one recipient as recently sanctioned. You are required to pause the transaction, investigate the activity, and submit a suspicious activity report.

However, despite strong AML frameworks, laundering activity often passes through banks without triggering immediate red flags.

How Money Laundering Hides in Plain Sight

Money laundering is designed to blend into regular banking activity. Criminals place funds into the financial system, then layer them through multiple transactions, accounts, and institutions, and finally integrate them so the money appears legitimate. Banks sit at the center of this flow, which makes traditional controls increasingly fragile.

Criminals use combinations of tactics that individually look harmless. These include:

- Depositing cash in small amounts to stay below reporting thresholds

- Moving funds rapidly between accounts or across borders

- Using shell companies or cash-heavy businesses to blur ownership

- Routing money through countries with weaker AML oversight

- Mixing illicit funds with legitimate customer activity

Over time, these transactions make 'dirty money' appear clean. Once integrated, funds can be withdrawn or reused to support crimes such as fraud, trafficking, or terrorism.

Also Read: A Complete Guide to Money Laundering Scams in 2026

This layered activity is precisely where traditional AML controls begin to fail.

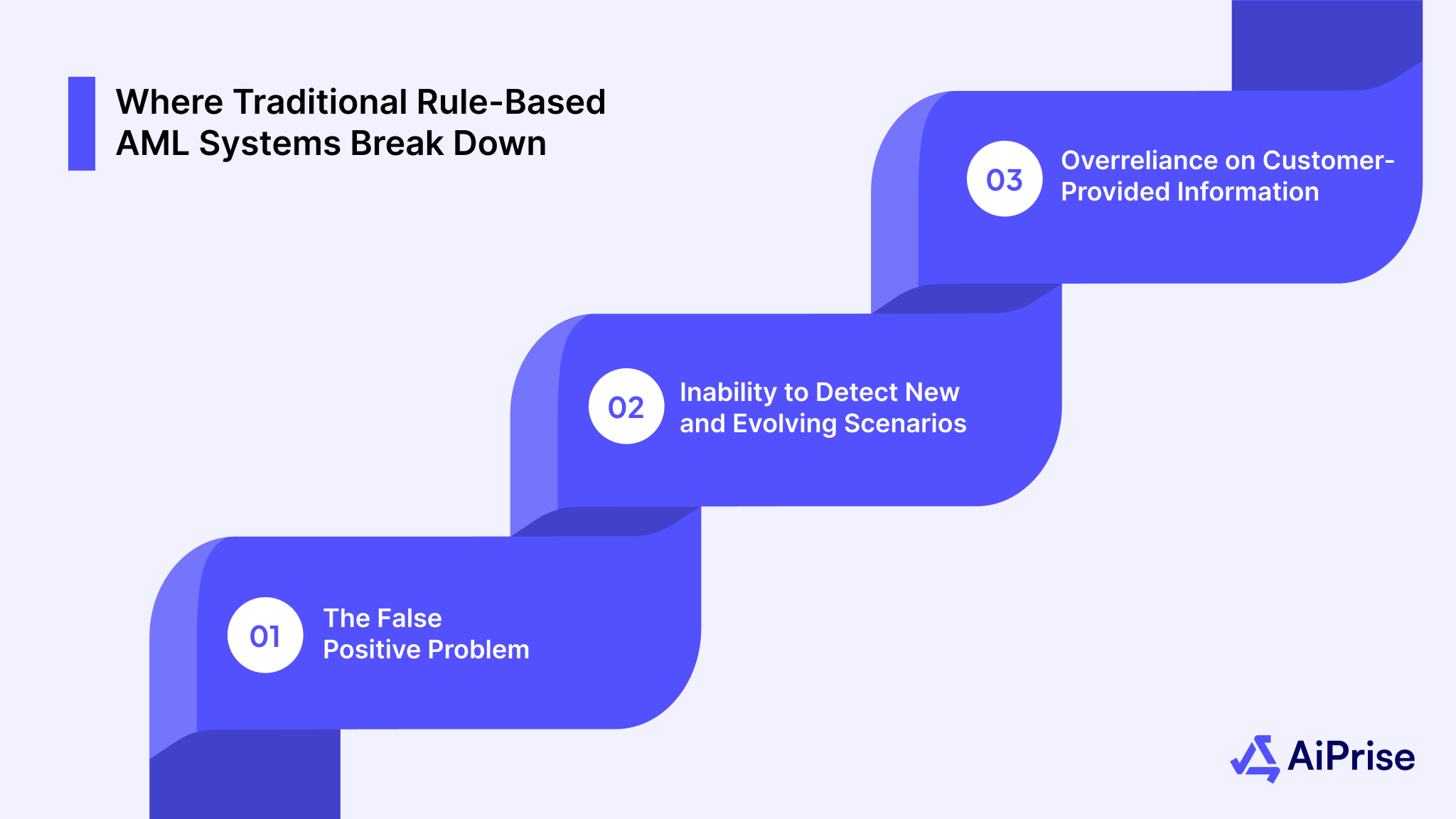

Where Traditional Rule-Based AML Systems Break Down

Most legacy AML systems rely on predefined rules and static red flags. These rules worked when transaction volumes were lower and laundering patterns were predictable. That is no longer the case.

That's because traditional systems typically focus on:

- Threshold breaches, such as deposits just under reporting limits

- Repeated transfers of similar amounts

- Rapid movement of funds between accounts

- Matches against sanctions and watchlists

Criminals now design their activity specifically to avoid these patterns.

Moreover, there are specific problems with traditional AML systems. These include:

The False Positive Problem

One of the biggest operational failures of traditional AML controls is the quality of alerts. In the event of false positives, each alert requires manual review to avoid regulatory errors. As a result, review teams grow, but risk coverage does not keep pace.

Why it matters

- High costs from staffing and investigations

- Slower response times to real threats

- Analyst fatigue, which increases the chance of missing genuine risk

Inability to Detect New and Evolving Scenarios

Criminal behavior does not stand still. Traditional AML systems struggle because:

- New laundering methods must be manually identified and coded into rules.

- Scenario updates lag behind real-world criminal tactics.

- Detection relies heavily on past patterns rather than emerging behavior.

Key insight: By the time a new scenario is added to rules, criminals may already have devised newer plans and approaches.

Overreliance on Customer-Provided Information

Traditional AML controls often assume customers act as stated during onboarding. In reality:

- Customers may misrepresent income, activity, or intent.

- Legitimate profiles can change over time.

- Deviations are hard to spot without behavioral analysis.

That's why you need AI-based AML systems that focus less on fixed rules and more on behavior over time, across channels, and within relationships. Let's now find out how AI strengthens your ability to meet AML obligations consistently and at scale.

How AI Strengthens AML Compliance in Banking

AI changes AML from a static, rules-driven process into a continuously learning system that adapts to how financial crime actually behaves. Instead of reviewing transactions in isolation, AI analyzes behavior, relationships, timing, and deviations from expected activity across customers and networks. This allows you to detect laundering techniques that are intentionally designed to bypass traditional controls.

What AI Does That Traditional AML Cannot

Traditional AML systems rely on fixed thresholds and predefined scenarios. AI focuses on patterns over time and connections across entities.

With AI, you can:

- Detect transaction patterns that only become risky when viewed collectively.

- Compare customer behavior against their own historical activity and peer benchmarks.

- Adjust customer risk scores dynamically using live transaction data and KYC inputs.

- Identify previously unknown relationships between people, accounts, and businesses.

- Automatically close or deprioritize alerts that show no meaningful risk.

Key insight: AI shifts AML from “Did this transaction break a rule?” to “Does this behavior pattern make sense?”

Core AI Techniques Used in Banking AML

Let's now examine the specific AML use cases where AI plays an important role.

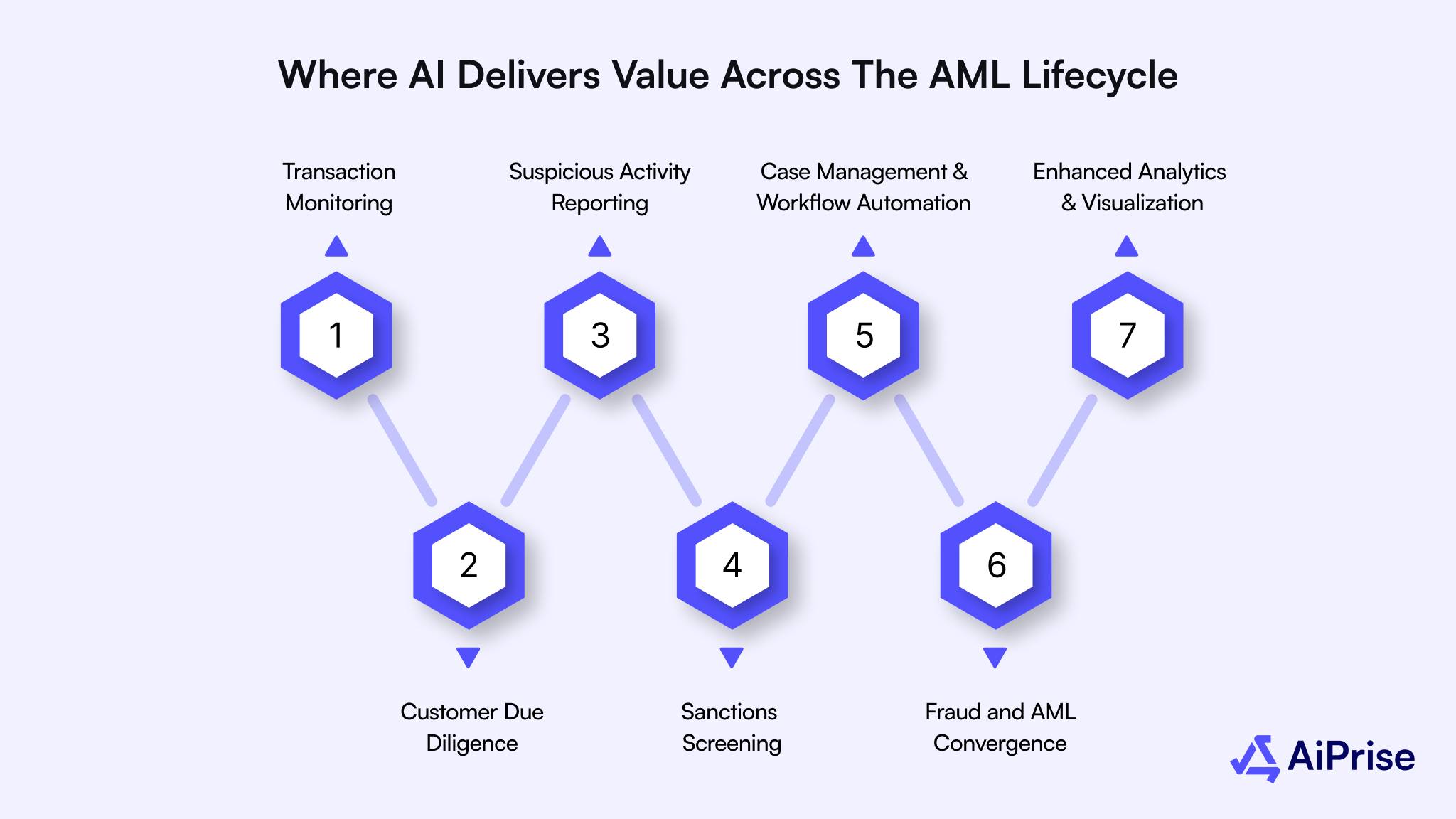

Where AI Delivers Value Across the AML Lifecycle

AI supports AML at every stage of the banking lifecycle, from onboarding and transaction monitoring to investigations and regulatory reporting. These capabilities connect data, behavior, and outcomes to help you detect risk earlier, reduce manual effort, and maintain consistent compliance.

Transaction Monitoring

AI improves transaction monitoring by moving beyond static rules.

How it works

- Learns normal transaction behavior for each customer

- Flags deviations in volume, velocity, frequency, and counterparties

- Detects structured transactions designed to avoid thresholds

- Identifies circular fund movements and rapid layering activity

Why this matters: Real threats surface earlier, with fewer false positives.

Also Read: How Continuous Payment Transaction Monitoring Prevents AML Risks

Customer Due Diligence (CDD) and KYC

AI strengthens both onboarding and ongoing risk assessment. Typical applications include:

- Automated ID document verification and face matching

- Authenticity checks for identity documents

- Continuous reassessment of customer risk as behavior changes

- Screening against sanctions, PEPs, and adverse media

If KYC reviews are becoming harder to scale, AI-driven identity verification can help. Platforms like AiPrise’s KYC solutions offer faster ID checks, continuous risk assessment, and sanctions screening without slowing onboarding.

Suspicious Activity Reporting (SAR)

AI improves SAR quality and speed. Here's how it helps:

- Auto-generates structured SAR narratives using transaction context

- Highlights missing data or inconsistencies

- Suggests follow-up actions for analysts

Sanctions Screening

AI improves sanctions accuracy in complex name-matching environments.

Capabilities

- Matches names across spelling variations and languages

- Extracts risk indicators and insights from unstructured documents

- Differentiates between similar but unrelated entities

- Adapts quickly to frequent sanctions updates

Why it matters: AI reduces unnecessary reviews while maintaining coverage.

Case Management and Workflow Automation

AI reduces the operational burden of AML compliance.

What it automates

- Alert prioritization and triage

- Low-risk alert closure

- Evidence collection for investigations

- Audit trail generation

Fraud and AML Convergence

Fraud and money laundering often overlap. AI enables a unified view of financial crime risk by connecting investigations across AML, fraud, and sanctions.

It also follows adaptive learning, which results in the following:

- Confirmed cases improve future detection.

- Edge cases near detection thresholds are identified earlier.

- Models improve without constant manual tuning.

Also Read: Fraud and Money Laundering: Key Differences and Connections

Enhanced Analytics and Visualization

AI-powered analytics and visualization tools help you turn complex AML data into insights that are easy to act on. Instead of reviewing raw alerts or spreadsheets, you can see risk patterns visually across customers, entities, and geographies.

How it helps in practice

- Geographic maps highlight where suspicious activity is concentrated.

- Dashboards track key AML metrics such as:

- Transactions monitored

- Alerts generated and resolved

- SARs filed

- Investigations opened and closed

Why it matters

- Nontechnical teams can understand risk without deep data expertise.

- Decisions are faster and better informed, especially during regulatory reviews.

While these capabilities deliver clear benefits, they also introduce new operational, data, and governance considerations. Let's explore them next.

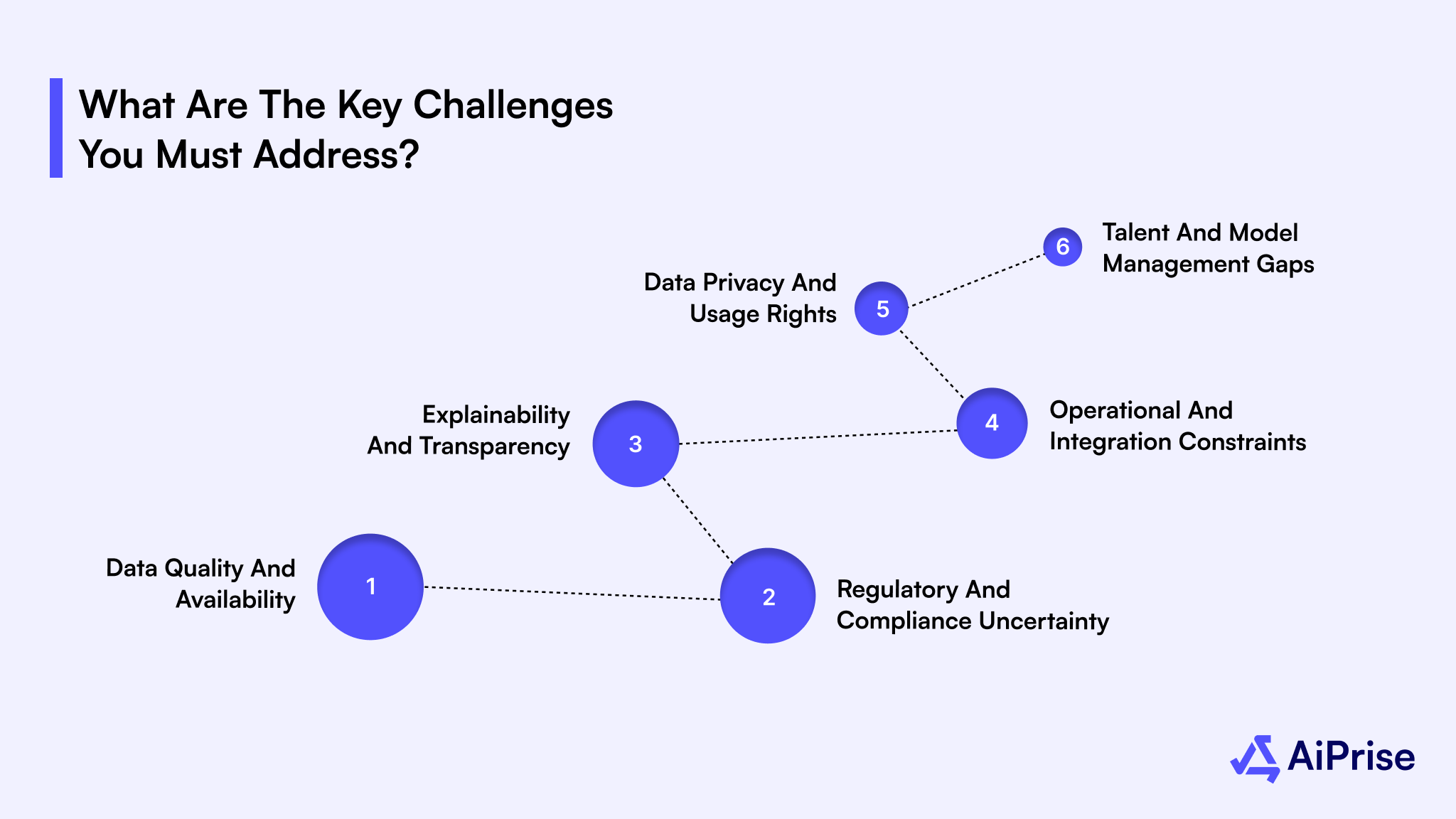

What are the Key Challenges You Must Address?

AI can significantly strengthen AML policies, but it is not a plug-and-play solution. AI systems can create new risks rather than reduce existing ones if the following challenges are not addressed.

- Data Quality and Availability: AI models rely on large volumes of accurate, well-labeled training data. Incomplete records, inconsistent formats, or limited examples of confirmed money laundering activity can reduce model accuracy and weaken detection outcomes.

- Regulatory and Compliance Uncertainty: AML regulations continue to change and are often open to interpretation. Guidance from bodies like FATF allows flexibility, which makes it harder to align AI models with supervisory expectations without early regulator engagement.

- Explainability and Transparency: Some AI models operate as “black boxes,” making it difficult to explain why a transaction or customer was flagged. Limited explainability can slow investigations and create challenges during audits and regulatory reviews.

- Operational and Integration Constraints: Many banks store customer and transaction data across legacy systems not designed for AI processing. Integrating these systems and standardizing historical data remain major technical hurdles.

- Data Privacy and Usage Rights: AI-driven AML systems process sensitive personal and transactional data. You must ensure data usage complies with privacy laws and internal governance frameworks to avoid regulatory and reputational risk.

- Talent and Model Management Gaps: Building, tuning, and maintaining AI models requires specialized skills. Limited access to experienced data science and compliance talent can slow deployment and reduce long-term effectiveness.

Addressing these challenges upfront is essential before moving from experimentation to production-scale AI in AML.

How to Incorporate AI into AML in Banking: A Step-By-Step Checklist

Adopting AI for AML is a structured transformation, not a single deployment. You need a clear plan that aligns technology choices with operational goals, regulatory expectations, and existing systems to deliver measurable results. The following steps outline a practical approach to introducing AI into existing AML programs.

Executing these steps successfully requires technology that can support AI across AML workflows without adding complexity. That's what AiPrise offers.

How AiPrise Enables AI-Driven AML Compliance at Scale

AI-powered AML only works when it strengthens risk detection without slowing down banking operations or creating compliance blind spots. For you, that means assessing risk instantly, adapting controls as behavior changes, and maintaining clear visibility into customers, ownership, and transactions. AiPrise is built to support this balance by combining intelligent automation with continuous risk oversight across AML workflows. Here's how:

- Dynamic Risk Scoring and Instant Risk Assessment: AiPrise delivers real-time risk assessments using your custom-built rules and regulatory requirements. Instead of static scoring, risk levels update continuously as new data emerges, helping you respond faster to new threats.

- Intelligent Risk-Based Actions: Based on dynamic risk scores, AiPrise automatically triggers enhanced due diligence or deeper investigations only when required. This ensures higher-risk cases receive attention without overburdening teams with unnecessary reviews.

- IP and Device Intelligence for Stronger Signal Detection: It provides accurate location intelligence to identify where users are onboarding from. Advanced device analysis helps detect and block bot activity, ensuring interactions come from genuine users and reducing entry points for fraud.

- Fraudulent Website Detection: The platform analyzes registrar details, traffic patterns, geographic signals, and visual indicators such as Google Street View data to identify suspicious or deceptive websites.

- Automated Sanctions and Watchlist Screening: Customers and related entities are screened in real time against global sanctions lists and watchlists. AI-driven matching improves accuracy while reducing false positives.

- Comprehensive UBO Verification: AiPrise delivers complete transparency into ownership structures by identifying ultimate beneficial owners and uncovering complex or hidden connections across entities.

Together, these capabilities help you apply AI across AML risk assessment, screening, and investigation workflows.

Wrapping Up

As banks adopt AI to strengthen AML compliance, success depends on more than deploying advanced models. Risk shifts continuously, transaction patterns change, and regulatory expectations grow more demanding over time. Relying on static rules or fragmented tools makes it harder to detect real threats while controlling costs and maintaining consistency.

AiPrise helps you move beyond these limits by bringing AI-driven risk assessment, verification, and continuous monitoring into a unified AML framework. With dynamic risk scoring, automated screening, and clearer visibility, you can improve detection accuracy, reduce false positives, and stay aligned with regulatory requirements.

Ready to strengthen your AML program with AI that scales with your bank operations? Book A Demo to see how AiPrise supports AML risk management, compliance, and operational efficiency across the full lifecycle.

FAQs

1. Which banks are using AI for AML?

Leading global banks such as JPMorgan Chase, Citigroup, and Wells Fargo actively use AI for AML to improve transaction monitoring, reduce false positives, and strengthen compliance.

2. What is the future of AI in AML for U.S. banks?

In the U.S., AI will become central to AML as the Financial Crimes Enforcement Network (FinCEN) expands Bank Secrecy Act oversight and scrutiny increases. Banks will rely more on explainable AI, real-time monitoring, graph analytics, and automation to meet rising regulatory and cost pressures.

3. Can AI-driven AML decisions be challenged or overridden by human analysts?

Yes. In practice, you must retain human oversight. AI flags, scores, and prioritizes risk, but analysts are expected to review findings, apply judgment, document decisions, and override AI outputs for regulatory defensibility.

4. How do we validate AI AML models before putting them into production?

Validation typically includes historical backtesting, parallel runs against existing systems, stress testing edge cases, and independent model reviews. These ensure accuracy, stability, and regulatory alignment before full deployment.

5. How does AI handle cross-border AML risks differently from traditional systems?

AI analyzes behavior across jurisdictions simultaneously, linking transactions, entities, and timing. This allows you to detect cross-border layering and routing through weaker AML regions that static, country-specific rules often miss.

You might want to read these...

.jpg)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately