AiPrise

8 min read

March 4, 2026

Low-Friction KYC Onboarding for Fintech Growth

Key Takeaways

Low-friction KYC onboarding ensures strong compliance while preventing customer drop-offs that can cost your business growth and revenue momentum. Your current onboarding may feel slow and clunky, discouraging users and letting competitors capture conversions you deserve. Tight regulatory requirements like AML and KYC often make you fear losing compliance or increasing risk.

At the same time, inefficient onboarding processes can frustrate users and drive abandonment before verification finishes. Seamless verification accelerates onboarding conversion, enhances trust, and protects your business from escalating fraud threats. Prioritizing a frictionless flow without compromising identity assurance helps you scale faster with confidence and regulatory alignment.

In 2025, the FBI’s IC3 reported that U.S. internet crime losses exceeded $16 billion, increasing 33 % and underscoring rising fraud pressures against businesses and financial platforms. Knowing how to streamline KYC onboarding helps you balance risk, increase conversions, and protect your fintech operations from evolving fraud tactics.

Quick Look

- Low-friction KYC onboarding reduces drop-offs by combining automated identity checks, biometric verification, and embedded AML screening within a fast, user-friendly flow.

- Progressive data capture and risk-based routing allow low-risk users instant approval while triggering enhanced KYC due diligence only when necessary.

- Real-time sanctions screening, fraud intelligence, and adaptive risk scoring protect fintech platforms against account takeovers and financial crime exposure.

- Automated workflows, mobile-first design, and continuous monitoring transform compliance from a bottleneck into a scalable growth driver.

What is Low-Friction KYC Onboarding?

Low-friction KYC onboarding is a streamlined client onboarding process in KYC that verifies identities quickly while maintaining strict AML compliance and regulatory controls. It combines automated document verification, biometric checks, real-time AML KYC onboarding, low-friction workflows, and adaptive risk scoring to reduce manual intervention. By integrating end-to-end KYC, KYC due diligence, and intelligent AML client onboarding processes, you shorten verification time without compromising security or audit readiness.

The Benefits Of A Frictionless And Secure KYC Process

A frictionless and secure KYC process strengthens compliance, improves onboarding conversions, and reduces operational risk without slowing customer acquisition.

Here are the key benefits you unlock when your verification strategy balances speed with regulatory precision:

- Higher onboarding completion rates because users move through verification steps without unnecessary delays or repetitive data entry.

- Reduced customer acquisition costs as fewer prospects abandon the client onboarding process in KYC midway through identity checks.

- Faster revenue realization since verified users can transact sooner within your end-to-end KYC environment.

- Lower manual review workload through automated AML client onboarding processes that reduce dependency on compliance teams.

- Stronger fraud prevention powered by real-time AML KYC onboarding, low-friction screening, and adaptive risk scoring mechanisms.

- Improved audit readiness with built-in KYC due diligence logs, ensuring documentation remains structured and regulator-friendly.

- Enhanced customer trust because secure, biometric-backed identity verification signals professionalism and data protection maturity.

- Scalable growth capacity, as automated KYC best practices allow you to expand across regions without rebuilding compliance workflows.

Also read: What is KYC? A Simple Guide for Beginners

Benefits sound promising, yet they only materialize when the onboarding structure itself is built correctly.

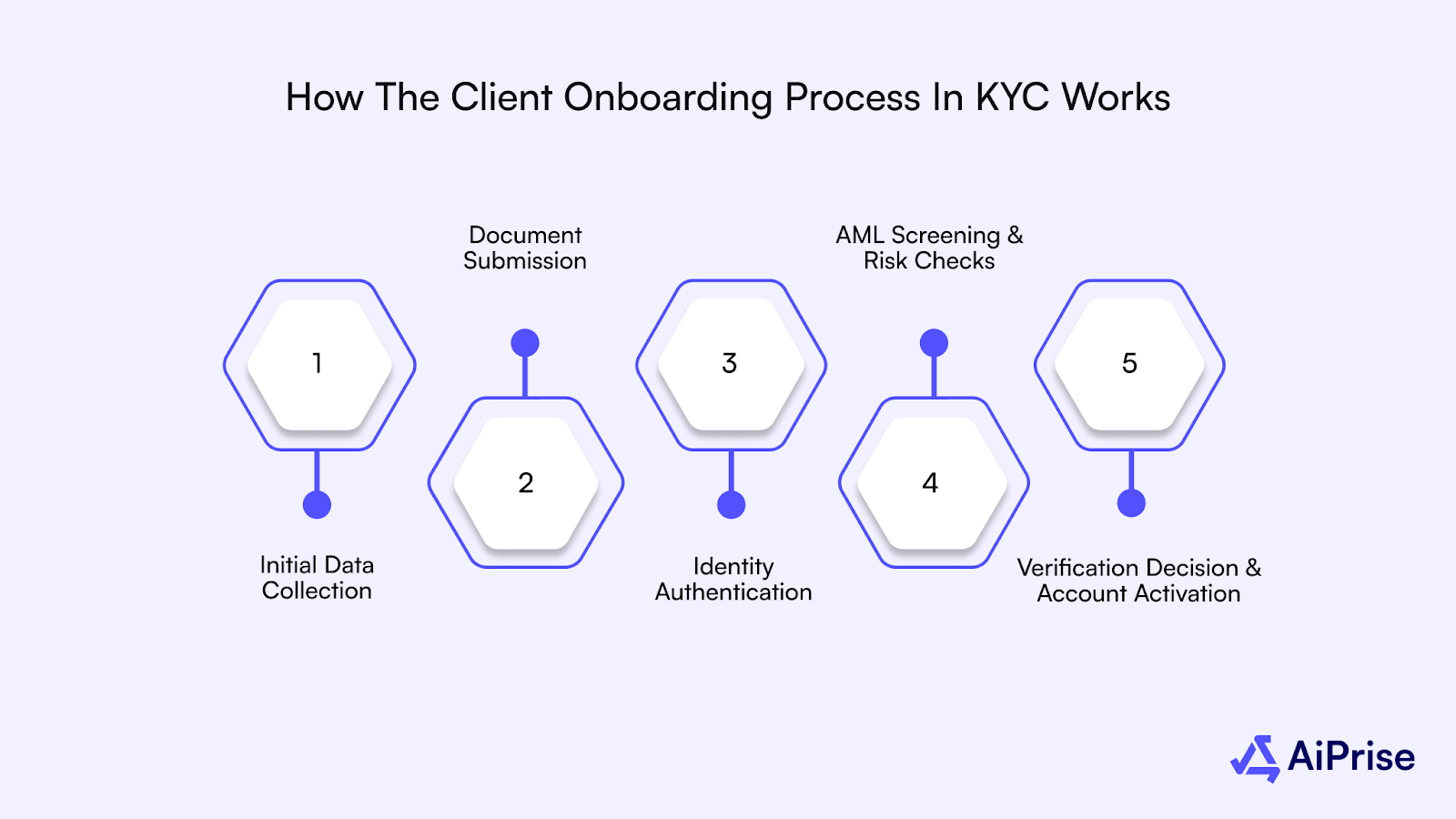

How The Client Onboarding Process In KYC Works

Understanding how the client onboarding process in KYC operates helps you identify where friction forms and where optimization drives measurable conversion gains.

Below is a structured breakdown of how an AML client onboarding process typically unfolds within an end-to-end KYC framework:

- Initial Data Collection:

- Capture full legal name, date of birth, residential address, and contact information.

- For business accounts, collect the company name, registration number, and principal place of business.

- Document Submission:

- Require government-issued identification such as a passport, driver’s license, or national ID card.

- For KYB verification, request incorporation certificates, tax identification numbers, and ownership documentation.

- Identity Authentication:

- Perform biometric verification through facial recognition and liveness detection.

- Match extracted document data against user-submitted information for consistency validation.

- AML Screening And Risk Checks:

- Screen individuals and entities against sanctions lists, PEP databases, and adverse media records.

- Apply risk scoring models to determine whether standard or enhanced KYC due diligence is required.

- Verification Decision And Account Activation:

- Approve low-risk applicants through straight-through processing for faster onboarding completion.

- Escalate higher-risk profiles to compliance teams for additional review before activation.

Once you see how onboarding traditionally unfolds, it becomes easier to pinpoint exactly where friction begins.

Core Elements Of A Low-Friction KYC Process

A low-friction KYC process is engineered to remove conversion blockers while preserving full regulatory defensibility across your AML and compliance stack.

Here are the tactical building blocks that make your client onboarding process in KYC faster, safer, and commercially scalable:

- Progressive Capture: Only essential customer data is collected upfront, while additional KYC due diligence information is triggered dynamically based on risk signals.

- Instant ID Validation: Government-issued IDs such as passports, driver’s licenses, and national identity cards are authenticated in seconds using automated forensic checks.

- Liveness Proofing: Selfie-based biometric verification confirms the applicant is physically present, reducing synthetic identity and impersonation fraud exposure.

- Embedded AML Screening

Sanctions, PEP, and adverse media checks run simultaneously during submission, preventing delays in the AML client onboarding process. - Risk-Based Routing: Low-risk profiles move through straight-through processing, while higher-risk entities enter enhanced KYC due diligence workflows automatically.

- Business Verification: For KYB cases, incorporation documents, UBO details, and registry data are validated instantly to support end-to-end KYC controls.

- Decision Automation: Rule engines and machine learning models generate approval or escalation outcomes instantly, reducing manual review bottlenecks.

- Lifecycle Monitoring: Post-onboarding surveillance ensures AML KYC onboarding low-friction standards remain intact as customer risk profiles evolve.

Also read: Understanding Identity Management in KYC Processes

Understanding the mechanics is important, but recognizing why customers abandon the journey is where growth decisions get sharper. To reduce drop-offs, you first need to confront what is pushing users away in the first place.

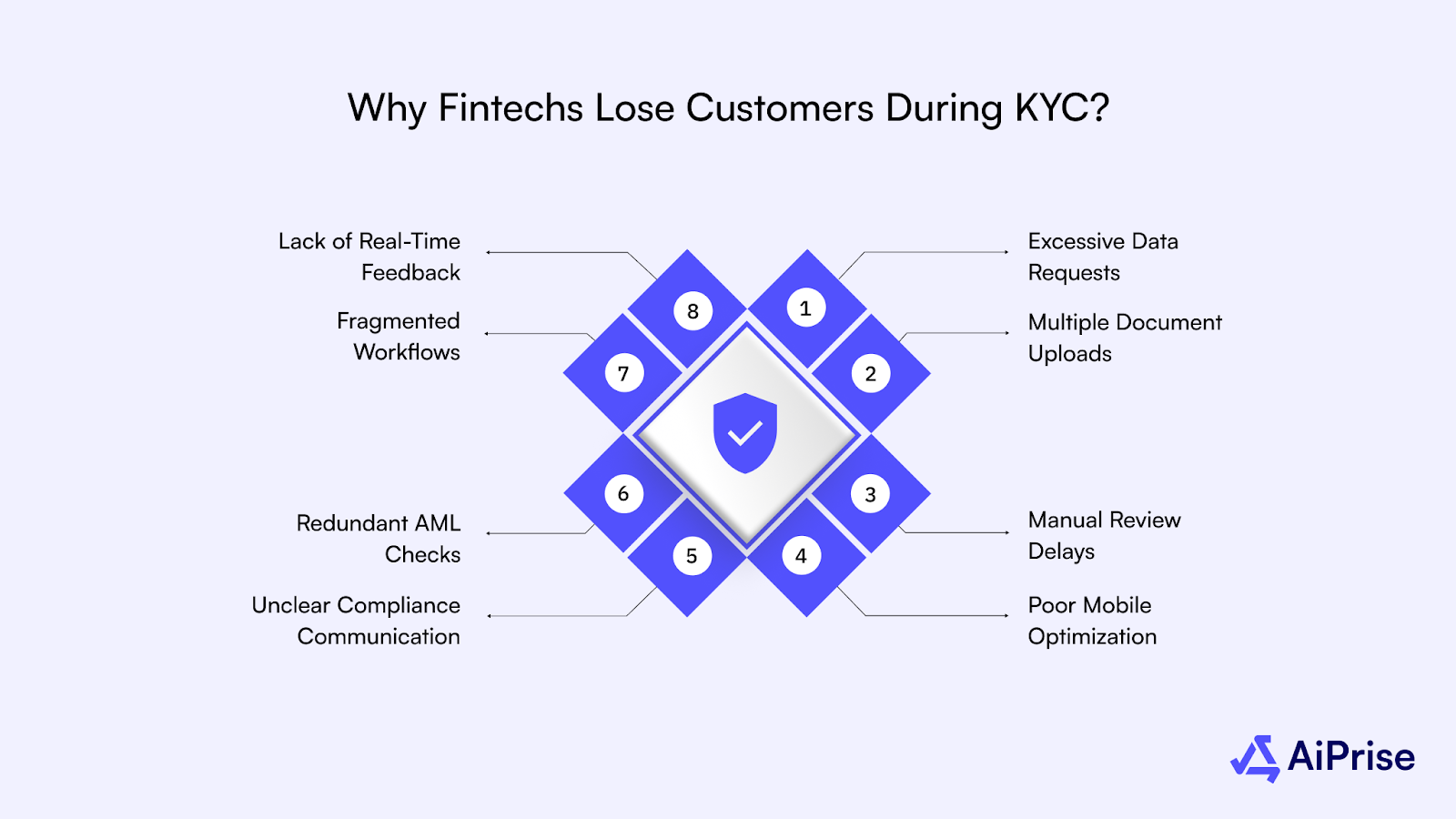

Why Fintechs Lose Customers During KYC?

Customer drop-offs during verification rarely happen because of compliance itself, but because the experience feels slow, unclear, or unnecessarily intrusive.

Here are the most common friction points that weaken your client onboarding process in KYC and directly impact conversion rates:

- Excessive Data Requests: Long forms asking for non-essential information upfront overwhelm users before trust is established.

- Multiple Document Uploads: Requiring repeated submissions of passports, driver’s licenses, or proof of address increases frustration and abandonment.

- Manual Review Delays: Slow approval queues within the AML client onboarding process create uncertainty and reduce onboarding momentum.

- Poor Mobile Optimization: Verification flows that fail on mobile devices disrupt completion rates in an increasingly mobile-first fintech environment.

- Unclear Compliance Communication: When users do not understand why KYC due diligence checks are required, skepticism replaces cooperation.

- Redundant AML Checks: Repetitive screening steps within AML KYC onboarding low-friction frameworks signal inefficiency rather than security.

- Fragmented Workflows: Disconnected tools and systems break your end-to-end KYC journey, forcing customers to restart or re-upload documents.

- Lack of Real-Time Feedback: Absence of instant status updates leaves applicants confused about next steps and expected verification timelines.

Customer frustration does not happen in isolation; it reflects broader shifts in fraud patterns and compliance expectations.

The Latest Trends In KYC Verification

KYC verification is no longer a static compliance checkbox because fraud sophistication and regulatory scrutiny are reshaping how financial platforms design onboarding systems.

Here are the major trends redefining how your AML client onboarding process and end-to-end KYC strategy must evolve:

- Account Takeover–Driven Identity Reinforcement: In 2025, the FBI’s IC3 reported over 5,100 account takeover complaints, causing $262 million in losses, pushing fintechs to strengthen biometric authentication and real-time identity verification controls during onboarding.

- Financial Crime Escalation Triggering Advanced Due Diligence: IRS Criminal Investigation identified $10.59 billion in financial crimes in 2025, signaling that stronger KYC due diligence and adaptive AML KYC onboarding low-friction workflows are becoming mandatory rather than optional.

- Embedded AML During Onboarding: AML screening is increasingly integrated directly into the client onboarding process in KYC instead of running as a post-verification check.

- Risk-Based Verification Depth: End-to-end KYC systems now dynamically escalate verification layers based on transaction risk, geography, and behavioral signals.

- Synthetic Identity Detection Models: AI-driven identity analytics are replacing static document checks to combat deepfake and fabricated identity fraud.

- Continuous Identity Monitoring: Verification is shifting from one-time onboarding checks to lifecycle-based monitoring aligned with modern KYC best practices.

Also read: End to End KYC Process: A Complete Guide for Compliance and Fraud Prevention

Trends show where the industry is heading, but practical execution depends on disciplined implementation.

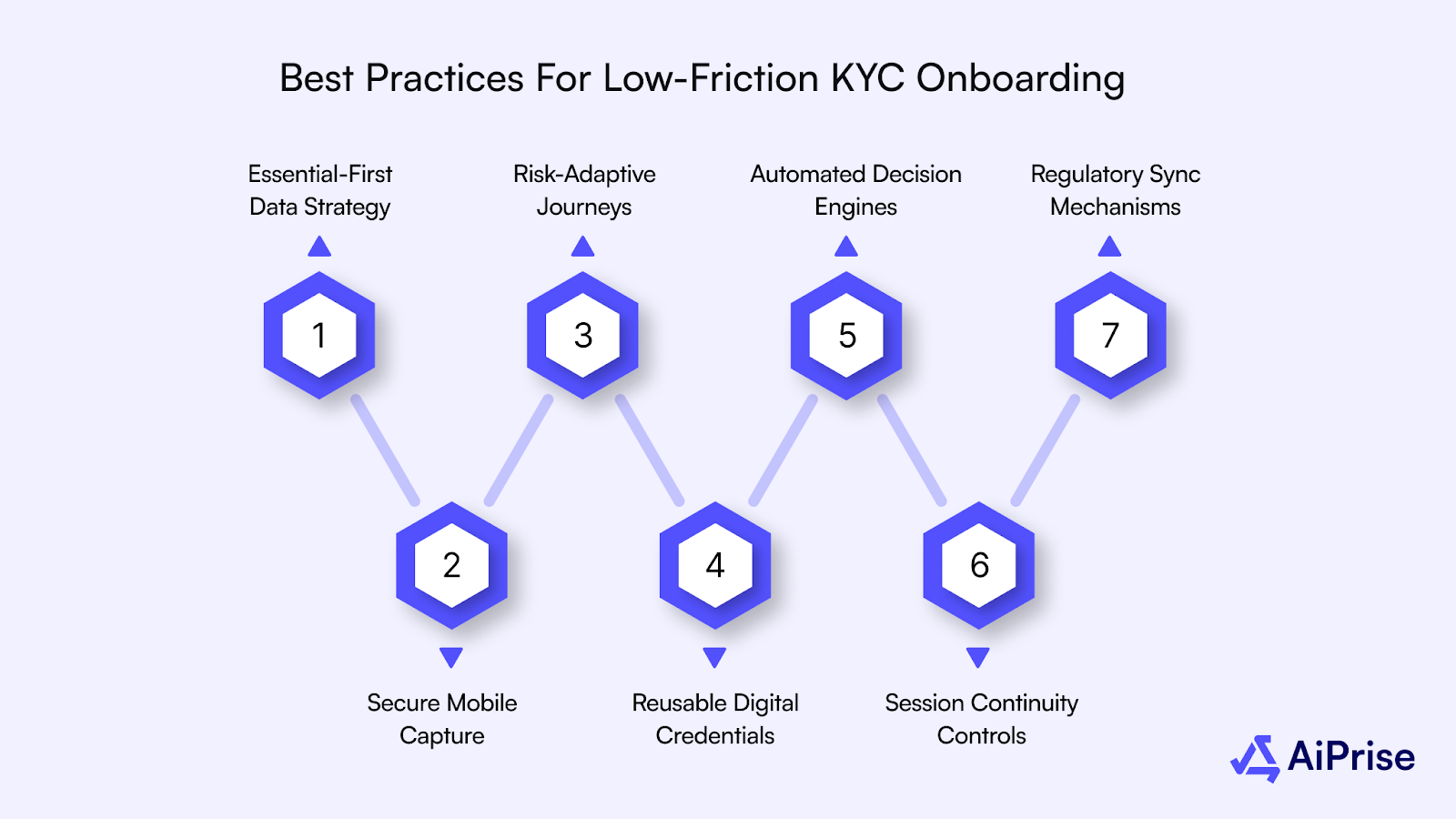

Best Practices For Low-Friction KYC Onboarding

Executing low-friction KYC onboarding requires precision design choices that improve conversion while preserving full compliance defensibility.

Here are tactical best practices that strengthen your AML client onboarding process without recreating friction points already discussed:

- Essential-First Data Strategy: Request only legally required information at entry, then expand KYC due diligence layers only when triggered by measurable risk indicators.

- Secure Mobile Capture: Deploy encrypted, camera-native ID capture with automatic glare detection and edge recognition to reduce upload failures on mobile devices.

- Risk-Adaptive Journeys: Route customers dynamically using behavioral signals, geolocation risk, and transaction intent instead of static onboarding templates.

- Reusable Digital Credentials: Enable tokenized identity reuse or verified digital ID frameworks to prevent repeated document submissions across sessions.

- Automated Decision Engines: Use rule-based and machine-learning models to generate instant approval, rejection, or escalation outcomes within your end-to-end KYC flow.

- Session Continuity Controls: Allow applicants to pause and resume onboarding securely, preventing drop-offs caused by interruptions or incomplete documentation.

- Regulatory Sync Mechanisms: Update verification workflows proactively when AML or KYC best practices evolve, ensuring compliance alignment without system overhauls.

Even with best practices in place, comparing older models with modern approaches reveals the operational gap clearly.

Traditional Vs Low Friction KYC Onboarding

Evaluating structural differences between legacy verification systems and modern low-friction models helps you identify where operational drag impacts growth.

The table below highlights the key distinctions shaping onboarding speed, compliance strength, and user experience outcomes:

Also read: 6 Types of Sanctions in KYC You Must Know to Avoid Penalties

Seeing the contrast makes one thing clear: technology determines whether compliance slows you down or supports your growth.

How AiPrise Helps With Low-Friction KYC Onboarding

Translating strategy into execution requires infrastructure that connects identity verification, AML controls, and risk intelligence into one scalable environment.

Here is how AiPrise enables you to operationalize low-friction KYC onboarding without sacrificing compliance strength or global reach:

- Unified KYC And KYB Infrastructure: Verify individuals and businesses within a single platform, eliminating fragmented tools across your end-to-end KYC workflow.

- One Click KYC Capability: Authenticate users using an ID number and selfie, reducing document friction while maintaining regulatory-grade identity assurance.

- Global Document Coverage: Verify over 12,000 document types across 220+ countries, supporting expansion without rebuilding your client onboarding process in KYC.

- UBO and Stakeholder Verification: Validate beneficial owners and key officers to strengthen KYC due diligence beyond surface-level entity checks.

- Integrated AML and Watchlist Screening: Screen against global sanctions, PEPs, and adverse media in real time during the AML client onboarding process.

- Dynamic Risk Scoring Engine: Configure custom rules and weightage models aligned to your risk appetite, enabling adaptive AML KYC onboarding low friction decisions.

- Fraud Intelligence Beyond Identity: Assess email, phone, device, IP, website signals, and judicial records to detect fraud patterns early.

- Ongoing Monitoring Controls: Automate periodic checks and risk-based monitoring frequency to maintain continuous compliance coverage.

- Customizable Onboarding Workflows: Design branded, drag-and-drop onboarding journeys that align with your regulatory requirements and growth objectives.

- Case Management and Audit Trail: Manage escalations, log review decisions, and export compliance reports for regulators or banking partners.

When verification, fraud intelligence, and compliance automation operate within one ecosystem, scaling globally becomes operationally efficient instead of operationally complex.

Wrapping Up

Low-friction KYC onboarding is no longer just a UX upgrade, because it directly determines how efficiently you scale while staying regulator-ready. Designing your client onboarding process in KYC with automation, embedded AML controls, and adaptive risk scoring transforms compliance from a bottleneck into a growth engine.

AiPrise enables you to operationalize this strategy through AI-driven verification, dynamic risk-based decisioning, and globally scalable end-to-end KYC infrastructure.

Book A Demo to see how you can accelerate onboarding, reduce fraud exposure, and strengthen compliance without slowing growth.

Frequently Asked Questions

1. What Is Low-Friction KYC Onboarding?

Low-friction KYC onboarding refers to a streamlined identity verification process that minimizes user effort while maintaining full regulatory compliance. It integrates automated document checks, biometric authentication, and real-time AML screening within a seamless digital workflow.

2. How Long Should A KYC Onboarding Process Take?

A modern low-friction KYC process should complete identity verification within seconds to a few minutes for low-risk users. Delays typically occur only when enhanced KYC due diligence or manual review is required.

3. What Documents Are Required For KYC Onboarding?

Government-issued identification, such as passports, driver’s licenses, or national ID cards, is typically required. For business verification, incorporation certificates, tax IDs, and Ultimate Beneficial Owner documentation are also necessary.

4. Does AML Increase Onboarding Friction?

AML requirements can increase friction if implemented manually or as separate steps. Embedded AML client onboarding processes with automated screening reduce delays while maintaining compliance standards.

5. What Is The Difference Between KYC And KYB?

KYC verifies the identity of individual customers, while KYB validates the legitimacy and ownership structure of businesses. Both processes form part of an end-to-end KYC framework designed to mitigate fraud and financial crime risks.

You might want to read these...

.jpeg)

.jpg)

.jpeg)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately