AiPrise

10 min read

November 24, 2025

What Is KYC Compliance in Banking? Essential Guide 2025

Key Takeaways

Do you know, the LexisNexis study reveals North American institutions collectively spend massive resources on customer verification, with some banks exceeding $50 million annually on compliance technology alone.

The investment yields questionable returns as 70% of fraud occurs after initial KYC completion, highlighting limitations of point-in-time verification.

Businesses face the challenge of balancing strict regulatory demands with frictionless customer experiences, complicated further by fragmented data and evolving identity risks.

The solution is adopting smart, risk-based, and automated KYC processes that speed onboarding while ensuring ongoing monitoring accuracy.

This blog explores these challenges and provides practical steps to help you master KYC compliance, protect your business, and build stronger customer trust.

Key Takeaways:

- KYC compliance in banking is essential to prevent financial crimes, ensure regulatory adherence, and protect reputations amid increasing AML fines.

- A risk-based approach combined with AI-driven identity verification and continuous customer monitoring optimizes resource use and accelerates onboarding while maintaining rigorous compliance.

- Core KYC components include customer identification supported by advanced biometric and document authentication technologies.

- Major challenges like regulatory complexity and data privacy can be overcome with automation, centralized data management, and customer-centric KYC workflows.

- AiPrise’s user verification platform, featuring One Click KYC, onboarding SDK, and proof of address verification, empowers banks to streamline compliance, reduce costs, and enhance customer experience efficiently.

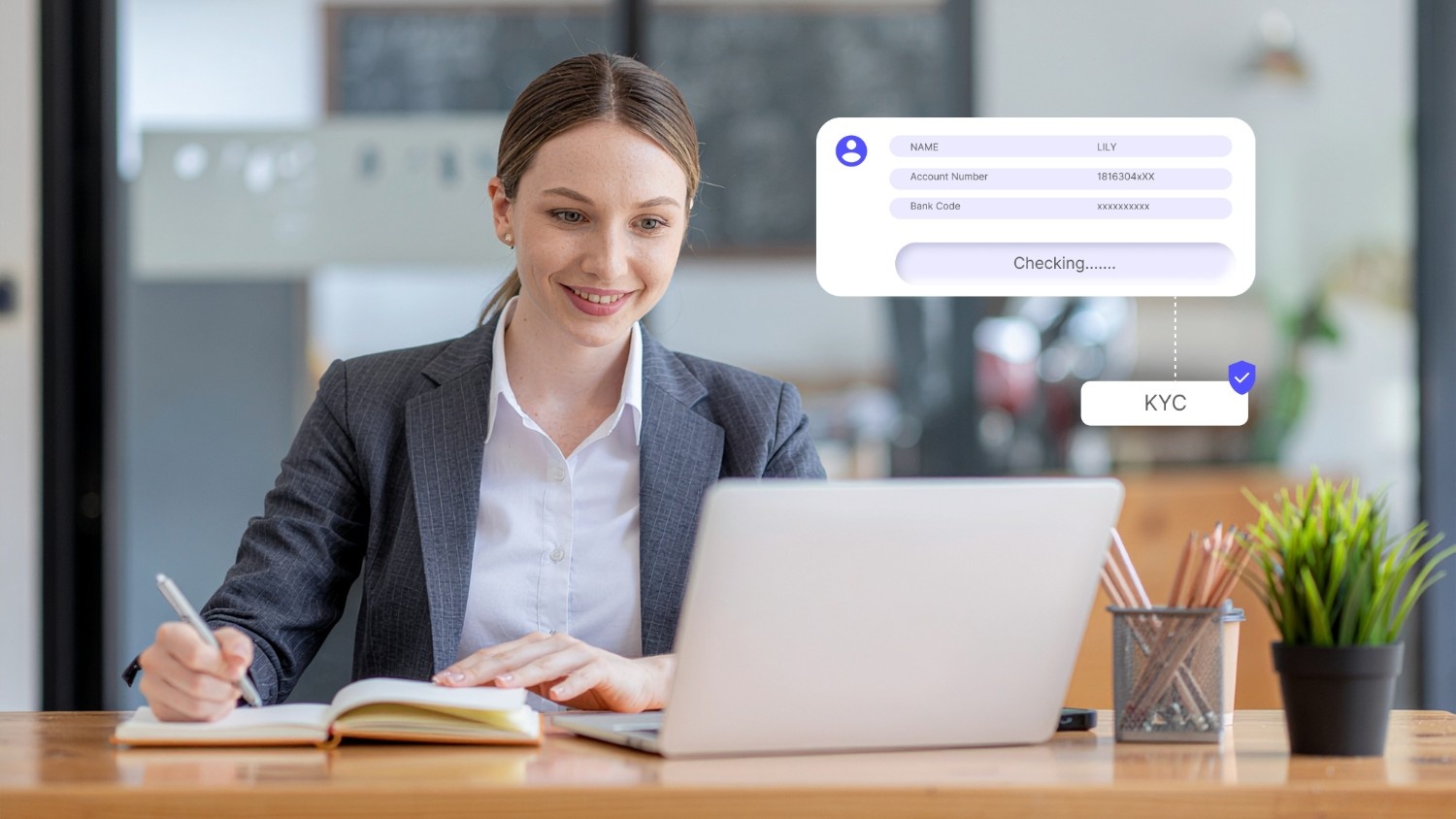

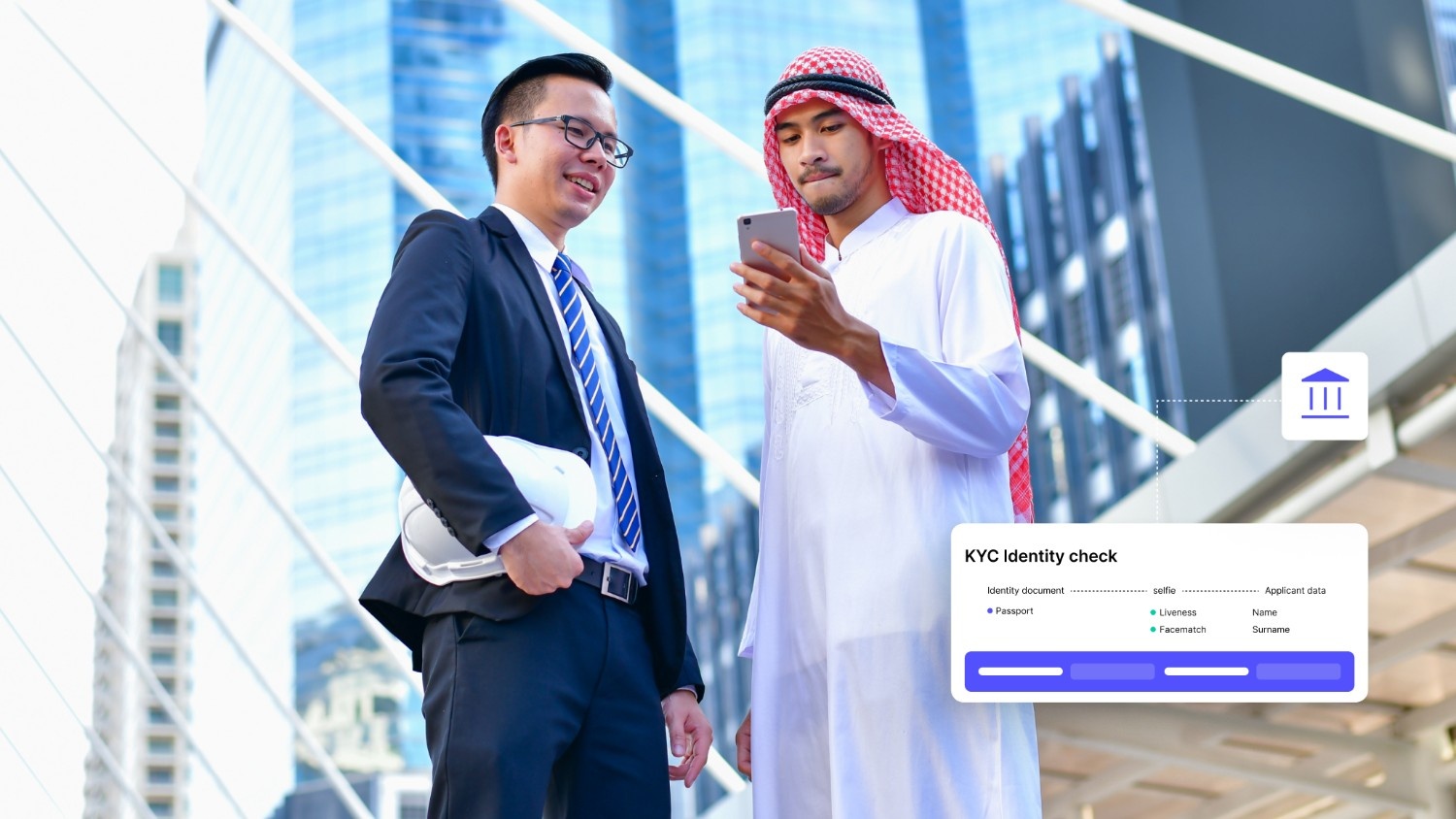

What is KYC Compliance in Banking?

KYC compliance is a mandatory process where banks and regulated entities collect and verify detailed information about their customers’ identity, address, financial status, and nature of business.

This is done to ensure the bank knows exactly who it is dealing with and to prevent its services from being used for illicit purposes such as money laundering, terrorist financing, or proliferation financing.

Banks must conduct KYC:

- When opening any account-based relationship.

- On occasional transactions exceeding ₹50,000 (single or aggregated).

- For international money transfers.

- Whenever there is suspicion about the authenticity or adequacy of customer information.

To understand why KYC is so crucial in banking, it’s important to understand exactly who must follow these processes to maintain compliance and secure the financial ecosystem.

Who Needs to Have KYC Processes?

KYC processes are legally and operationally required for a variety of parties involved in financial transactions. This requirement extends well beyond banks themselves, ensuring comprehensive fraud prevention and regulatory compliance.

Primarily, the following parties must comply:

- Banks and Financial Institutions: These include commercial banks, credit unions, investment firms, insurance providers, and brokerage houses. Every institution that handles money or financial assets must implement KYC to verify clients’ identities and assess risks.

- Individual Customers: Anyone opening or maintaining personal or business accounts must undergo KYC. This includes individuals engaging in significant transactions or digital banking services.

- Corporate and Business Clients: Entities such as corporations, partnerships, trusts, and non-profits need KYC to identify beneficial owners (those owning 25% or more equity) and verify the legitimacy of business activities.

- Politically Exposed Persons (PEPs) and High-Risk Clients: Special attention is given to individuals with political exposure or higher risk profiles due to geography, occupation, or transaction patterns. Enhanced due diligence requirements apply to these customers.

- Non-Financial Businesses and Professions: Depending on jurisdiction, professions like real estate brokers, dealers in precious metals, legal and accounting firms engaged in financial activities must comply with KYC standards.

Also Read: How KYC Is Done In Banks: A Step-by-Step Guide

Building on the fundamental understanding of KYC compliance, it’s essential to explore the core components that form its framework and ensure thorough risk management.

Components of KYC Compliance

KYC compliance in banking rests on three pivotal components that collectively ensure robust customer identification, risk assessment, and ongoing surveillance. Each element plays a critical role in preventing financial crimes and maintaining regulatory alignment.

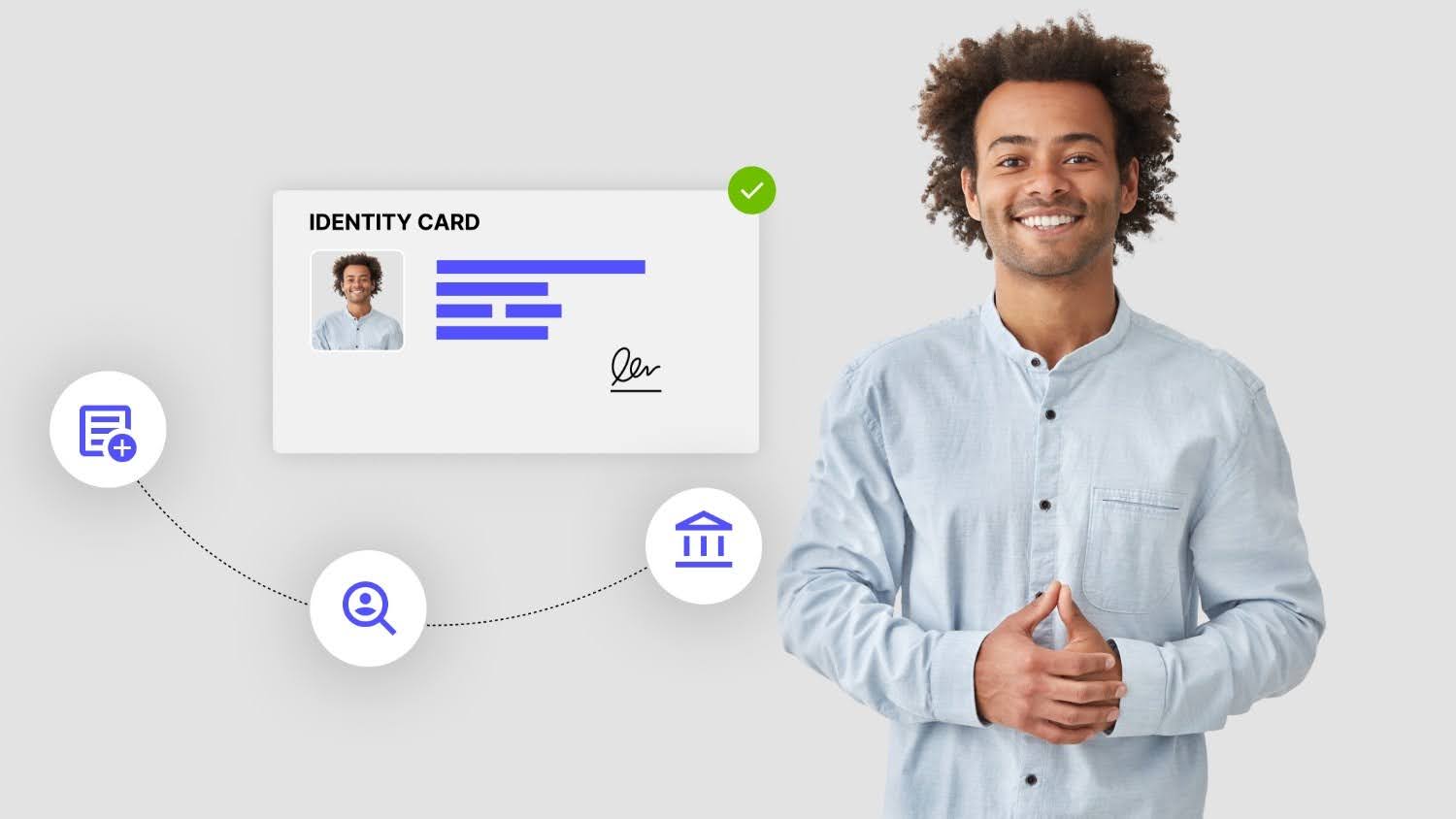

1. Customer Identification Program (CIP)

This initial step confirms the authenticity of a customer’s identity using official documents and biometric technologies. Key activities include:

- Document Verification: Scrutinizing government-issued IDs, passports, or driver’s licenses against authentic databases to confirm validity.

- Face and Liveness Verification: Utilizing facial recognition and liveness detection technologies to match the customer’s live presence against ID photos and prevent spoofing.

- Address Verification: Validating proof of residence documents like utility bills or bank statements to corroborate the customer’s address.

2. Customer Due Diligence (CDD)

CDD involves assessing the customer’s risk profile to determine the appropriate level of scrutiny during onboarding and beyond. This process focuses on:

- Risk Profiling: Evaluating factors such as geographic location, occupation, transaction behavior, and source of funds.

- Purpose and Expected Activity: Understanding the customer’s intended use of banking services to identify anomalous or suspicious behaviors.

- Enhanced Due Diligence (EDD): For high-risk customers or complex transactions, deeper investigation, including background checks and monitoring politically exposed persons (PEPs), is conducted.

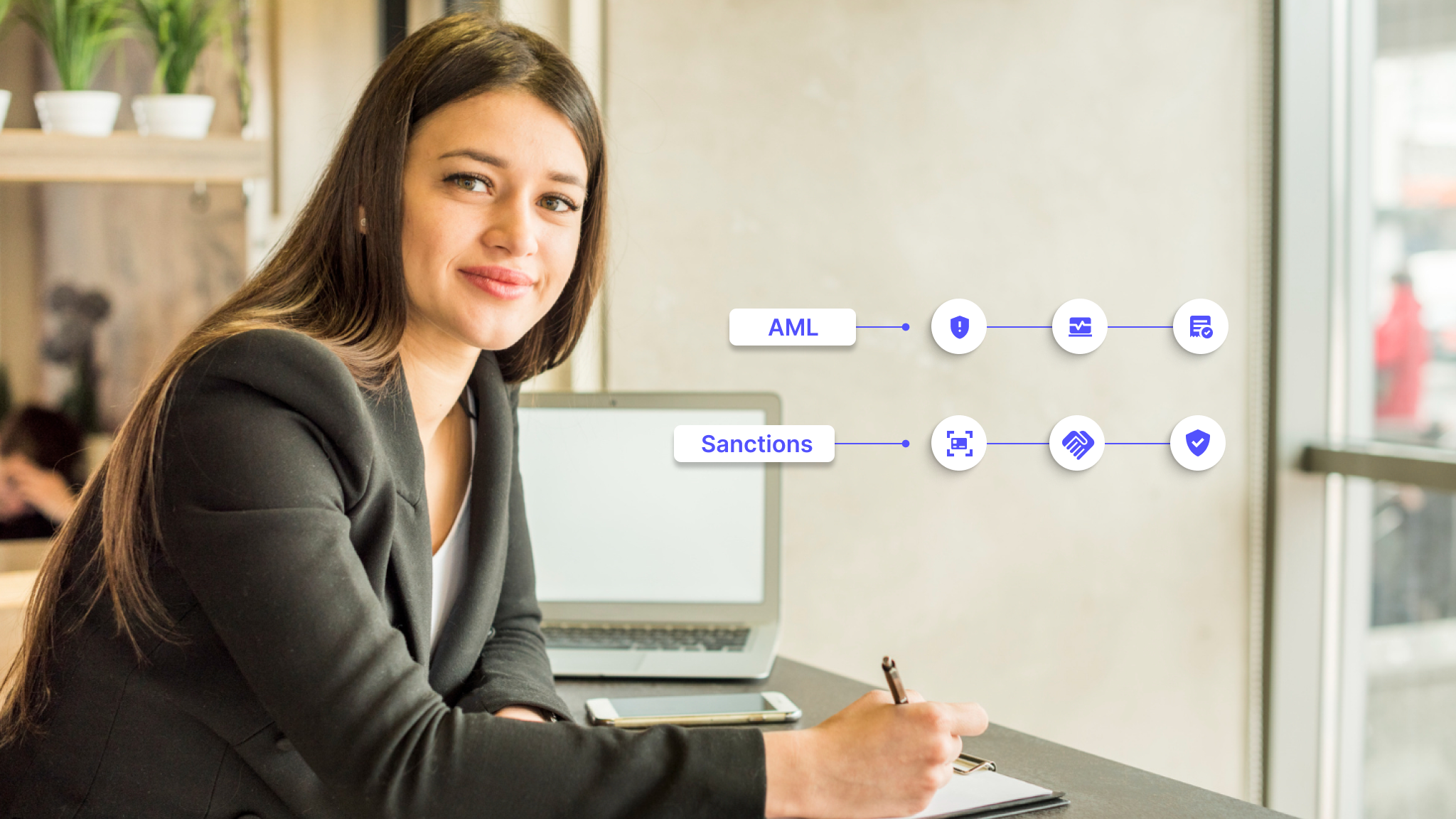

3. Ongoing Monitoring

KYC is not a one-time process but requires continuous assessment throughout the customer relationship. Key tasks involve:

- Transaction Monitoring: Automated systems analyze ongoing transactions to flag unusual patterns or compliance breaches.

- Periodic Reviews: Scheduled updates of customer information to capture any significant changes in behavior or profile.

- Sanctions and Watchlist Screening: Regularly cross-checking customers against global sanctions lists, PEPs databases, and adverse media sources.

Also Read: 3 Essential Components of KYC

Understanding the foundational requirements of KYC leads naturally to recognizing why its implementation is important within the banking sector.

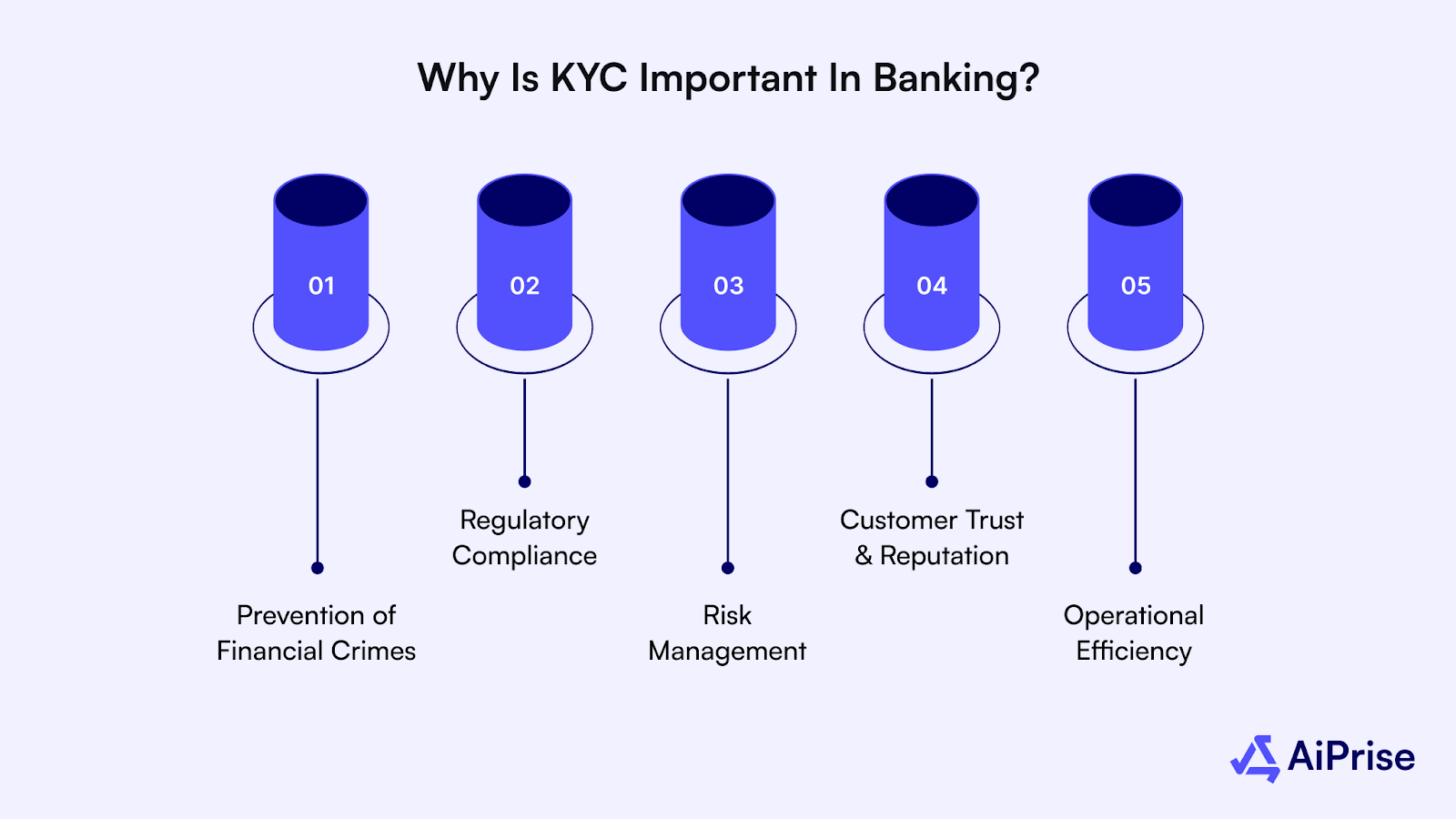

Why Is KYC Important in Banking?

KYC (Know Your Customer) holds critical importance in banking for legal, financial, and operational reasons that protect both the institution and its customers:

1. Prevention of Financial Crimes

- Money Laundering Mitigation: Banks use KYC to verify the identity of customers, disrupting channels used for laundering illicit funds.

- Fraud Detection: Accurate identity verification reduces risks of account takeovers, synthetic identity fraud, and unauthorized access.

2. Regulatory Compliance

- Banks comply with international and local regulations such as FATF recommendations, AMLD in Europe, FinCEN in the U.S., and RBI guidelines in India.

- Failure to comply can result in substantial fines.

3. Risk Management

- KYC allows banks to assign risk scores based on customer profiles and transactions, enabling tailored monitoring and controls.

- High-risk customers get subject to Enhanced Due Diligence (EDD) to mitigate exposure to fraud or financing of terrorism.

4. Customer Trust and Reputation

- By securing financial dealings, banks uphold a trustworthy reputation and foster stronger customer relationships.

5. Operational Efficiency

- Effective KYC reduces onboarding delays and costly manual reviews by leveraging automated identity verification and monitoring tools.

Also Read: Common Types of Business and Financial Fraud

Let’s now understand the real-world obstacles these institutions face and explore practical ways to overcome them.

Overcoming Major KYC Compliance Challenges: Practical Solutions for Financial Institutions

KYC compliance is essential but fraught with challenges that can strain resources, delay onboarding, and jeopardize regulatory adherence. Addressing these requires both strategic insight and technological innovation.

Here are some key challenges that organizations face and their solutions:

1. Complex and Constantly Evolving Regulations

Financial institutions struggle to keep pace with frequent regulatory changes across multiple jurisdictions.

Implement dynamic compliance management systems that automatically update rules and integrate with global regulatory databases for real-time adjustments.

2. High Costs and Inefficiency in Onboarding

Manual processes inflate costs, sometimes exceeding $3,000 per corporate client review, while also increasing onboarding time and lowering customer conversion.

Use identity verification and automation to expedite onboarding, reduce manual errors, and lower expenses

Need a faster account opening and onboarding flow? AiPrise offers identity verification that combines document authentication and real-time AML screening.

3. Balancing Regulatory Compliance with Customer Experience

Having strict KYC protocols can cause friction, resulting in customer drop-off. Employ seamless digital KYC platforms that minimize required customer input, use biometric verification, and offer transparent communication about data usage.

Try AiPrise One Click KYC for instant, accurate identity verification that keeps your customers engaged. Book a Demo today.

4. Data Privacy and Sharing Concerns

Banks must share customer data for AML, yet comply with privacy laws like GDPR. Adopt privacy-by-design frameworks that ensure data encryption, consent management, and controlled data access to maintain compliance without sacrificing AML efficiency.

5. Fragmented Customer Data and Record-Keeping

Disparate systems lead to inconsistent records, complicating KYC reviews. Centralize data in cloud-based platforms with strong audit trails and update mechanisms for consistency and regulatory readiness.

Now that we know the challenges, let’s also have a look at some proven strategies to effectively implement KYC programs that meet regulatory demands.

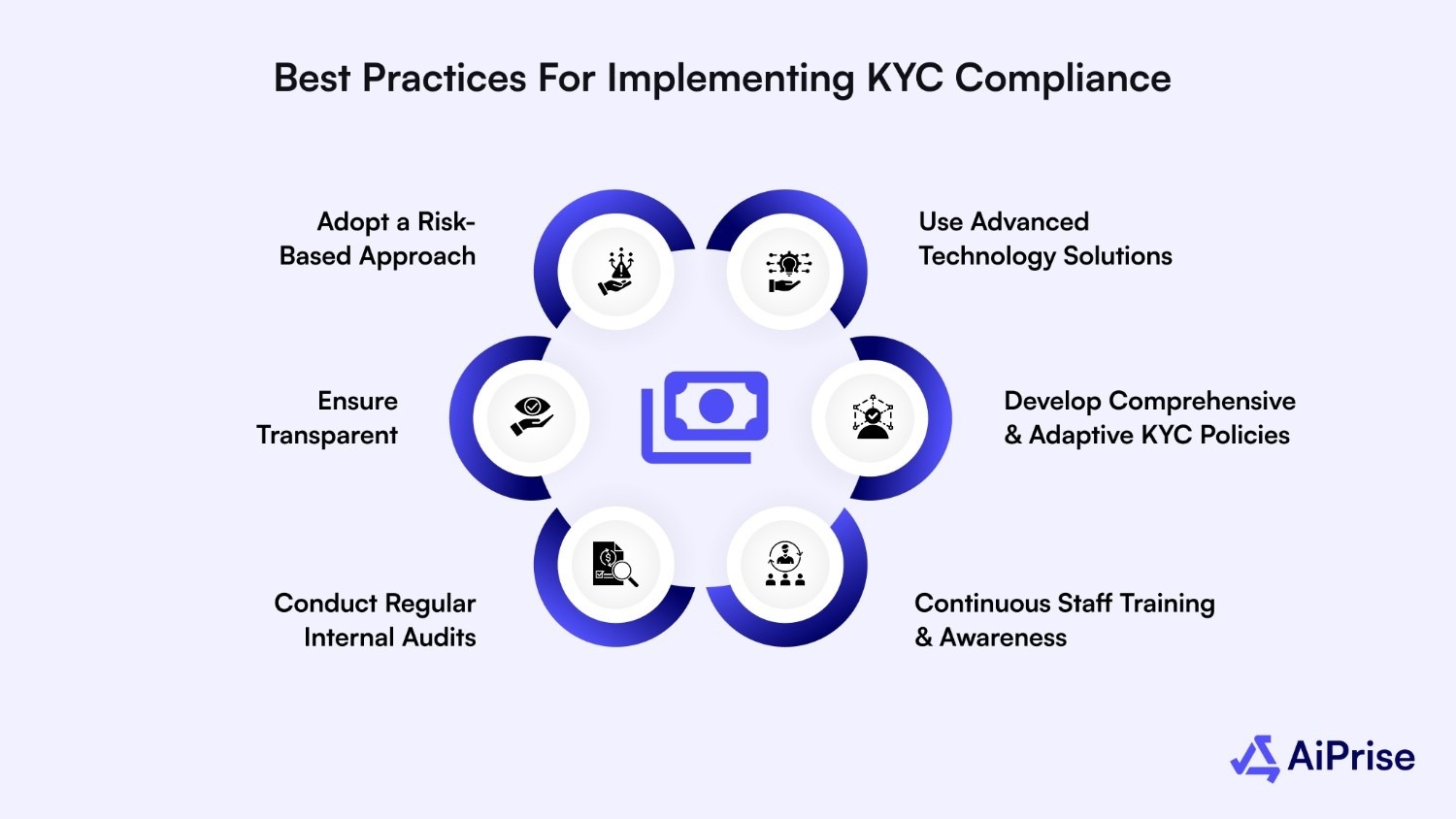

Best Practices for Implementing KYC Compliance in 2025

Implementing KYC compliance successfully requires up-to-date practices customized to changing regulations and customer expectations.

Here are best practices financial institutions should adopt to stay compliant and competitive in 2025:

1. Adopt a Risk-Based Approach (RBA)

- Continuously assess customer and transaction risks.

- Prioritize enhanced due diligence (EDD) for higher-risk entities such as politically exposed persons (PEPs) and customers from high-risk geographies.

- Adjust verification intensity and monitoring frequency based on risk profiles, improving resource allocation and reducing unnecessary customer friction.

2. Use Advanced Technology Solutions

- Utilize AI and machine learning to automate identity verification, transaction monitoring, and fraud detection.

- Deploy biometric tools (facial recognition, liveness detection) and OCR-enhanced document validation to reduce human error and accelerate onboarding.

- Integrate centralized customer data platforms for seamless data access and regulatory reporting.

3. Develop Comprehensive and Adaptive KYC Policies

- Regularly update policies to reflect new regulations like FATF recommendations, FinCEN updates, and regional AML directives.

- Maintain detailed customer identification programs (CIP), due diligence processes, and ongoing monitoring frameworks.

4. Continuous Staff Training and Awareness

- Provide ongoing training focusing on regulatory changes, fraud typologies, and technology tools.

- Use risk culture where all employees understand their role in compliance.

5. Conduct Regular Internal Audits and Independent Reviews

- Schedule periodic audits to verify the effectiveness of KYC controls and uncover vulnerabilities.

- Use audit findings to refine processes, enhance risk frameworks, and ensure regulatory readiness.

6. Ensure Transparent and Customer-Centric Experience

- Communicate clearly with customers about data use, privacy safeguards, and the importance of KYC.

- Streamline onboarding flows to reduce drop-offs by minimizing documentation steps and using digital KYC features.

Let's focus on how AiPrise’s advanced solutions can streamline your verification process while ensuring full regulatory adherence.

How AiPrise Accelerates and Simplifies KYC Compliance

AiPrise offers a powerful user verification solution designed to help financial institutions maintain strict KYC compliance efficiently and effectively. Its feature-rich platform addresses the challenges of identity verification and onboarding with automation, accuracy, and user convenience.

Core feature’s of AiPrise’s KYC solution:

- One Click KYC: Enables instant identity verification by securely retrieving customer data from government databases using only an ID number and a selfie, minimizing customer effort and onboarding time.

- Onboarding SDK: A customizable, developer-friendly software development kit that integrates seamlessly into your app or website, providing smooth identity capture, document scanning, and biometric verification without disrupting user experience.

- Proof of Address Verification: Verifies residential addresses using official documents such as utility bills or bank statements, ensuring compliance with regulatory requirements.

- Document Authentication: Uses AI-powered Optical Character Recognition (OCR) and advanced fraud detection algorithms to validate documents swiftly and accurately.

- Biometric Verification: Includes liveness detection and facial recognition to prevent spoofing and ensure that the customer is physically present.

- Ongoing Monitoring Support: Facilitates reverification and continuous compliance by maintaining updated customer profiles and monitoring for changes or suspicious activities.

Simplify your KYC process. Visit the AiPrise website today to experience seamless, secure user verification designed for modern banking.

Wrapping Up

Mastering KYC compliance is essential for financial institutions to safeguard against fraud, ensure regulatory adherence, and build lasting customer trust.

By adopting a risk-based approach, using advanced technologies, centralizing data management, and creating a culture of ongoing training and transparency, businesses can turn compliance challenges into operational strengths.

Embracing these strategies not only reduces risks and costs but also enhances customer experience in today’schanging financial market.

For businesses ready to simplify their KYC process with automation and accuracy, AIPrise offers a comprehensive solution customized to meet 2025 compliance standards.

Book A Demo today to transform your KYC compliance and onboarding efficiency with AiPrise.

FAQs

1. Can KYC be completed remotely, or must it be face-to-face?

KYC can now be completed remotely using video KYC, electronic verification (e-KYC), or mobile biometric authentication, especially with updated regulations allowing non-face-to-face verification to enhance convenience without compromising compliance.

2. What documents qualify as proof of address for KYC?

Acceptable proof of address documents include utility bills (electricity, water, gas), bank statements, rental agreements, or government-issued letters that are recent and clearly show the customer’s residence.

3. How often should KYC information be updated?

KYC updates depend on customer risk: high-risk customers require updates every 1-2 years, medium risk every 3-5 years, and low risk every 8-10 years, ensuring ongoing accuracy and compliance with regulatory requirements.

4. Is biometric verification mandatory for all KYC processes?

While biometric verification enhances security and reduces fraud risk, it is not universally mandatory but increasingly recommended and adopted by regulators and financial institutions for higher assurance levels.

5. How does KYC compliance impact customer onboarding times?

Traditional KYC can delay onboarding significantly, but digital and AI-driven verification methods reduce times from days to minutes, improving customer experience while maintaining thorough compliance.

You might want to read these...

.jpeg)

.jpg)

.jpeg)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately