AiPrise

9 min read

March 3, 2026

Address Verification for Fintech: Best Practices to Prevent Fraud

Key Takeaways

Address verification has become one of the toughest challenges you face when onboarding new customers in fintech, because fraudsters increasingly slip through weak identity checks and exploit gaps in verification systems. In 2025, official data from the Government revealed that about $65 million in rental scams were reported over a 12-month period ending in June 2025. With half of those victims saying the scam began with a fake address listing or related misrepresentation, a reminder that verifying where a person says they live still matters in the digital age.

Because fintech companies must balance fast onboarding with compliance requirements under KYC and AML rules, failing to validate addresses rigorously can expose you to synthetic identities, mule accounts, and costly fraud losses. By gaining a deeper understanding of how address verification fits into your broader risk and compliance strategy, you can reduce fraud exposure and build trust with regulators and customers alike.

Incorporating advanced checks early in your customer lifecycle also strengthens fraud risk management and operational efficiency. In an environment where scammers adapt quickly, mastering address verification isn’t optional; it’s essential to protecting your bottom line and safeguarding user experience.

Key Takeaways

- Address verification for fintech confirms whether a customer’s stated residential address is real, deliverable, and genuinely linked to their identity during KYC onboarding.

- Basic AVS checks only validate billing address matches, while full proof-of-address verification detects synthetic identities, mule accounts, and altered documents.

- Weak address controls contribute to account takeover, loan stacking, payment fraud, and AML exposure, especially in fully digital onboarding environments.

- Combining multi-source data checks, AI document authentication, dynamic risk scoring, and continuous monitoring reduces fraud losses and strengthens regulatory compliance.

What is Address Verification in Fintech?

Address verification for fintech is the process of confirming that a customer’s residential address is real, deliverable, and legitimately linked to their identity. It combines tools like an Address Verification System (AVS), document checks, and online address verification for fintech platforms to reduce onboarding fraud risk. A strong address verification service check also validates proof-of-address documents and flags inconsistencies before they trigger AML exposure or compliance penalties.

Why Address Verification Is a High-Risk Blind Spot in Fintech?

Address verification often becomes a high-risk blind spot in fintech because speed-driven onboarding models unintentionally weaken location-based identity controls.

Here are the key risk factors that make address verification for fintech more vulnerable than most compliance teams anticipate.

- Rapid digital onboarding compresses verification timelines, increasing reliance on automated checks without layered validation controls.

- Basic Address Verification System AVS responses only confirm numeric matches, not whether the address truly belongs to the applicant.

- Synthetic identity fraud blends real and fabricated data, allowing fraudsters to pass superficial online address verification for fintech platforms.

- Remote account opening removes physical branch scrutiny, reducing behavioral cues that previously supported fraud detection efforts.

- Cross-border applicants introduce jurisdictional data inconsistencies, complicating address verification service check processes and compliance assessments.

- Free address verification for fintech tools validates formatting accuracy but fails to assess ownership, occupancy, or fraud exposure.

- Fraud rings frequently reuse compromised residential addresses, creating mule networks that evade static rule-based monitoring systems.

- Weak proof-of-address review processes allow manipulated utility bills or digitally altered documents to bypass onboarding controls.

Also read: How to Get and Verify Proof of Address

When these gaps go unnoticed, they often translate into measurable fraud losses rather than theoretical compliance risks.

Common Fraud Patterns Linked to Weak Address Verification

Weak address verification creates an opening for sophisticated fraud schemes that cost fintechs money and damage trust.

Here are notable fraud patterns tied to weak or incomplete address verification:

- Fraudsters use stolen or synthetic identities with fake or mismatched addresses to open accounts that evade basic checks.

- Since January 2025, the FBI Internet Crime Complaint Center received over 5,100 account takeover complaints, with reported losses exceeding $262 million, highlighting how weak address verification controls enable credential misuse and financial drain.

- Mule accounts flourish when verification fails to flag invalid or unverified addresses, enabling money laundering and transaction routing.

- Imposter scams often use plausible but fabricated addresses to make fraudulent accounts appear legitimate to human or automated reviews.

- Organized fraud rings exploit weak proof-of-address controls to establish multiple linked accounts from the same invalid address cluster.

- Loan stacking and credit product misuse occur when multiple applications pass superficial address checks but hide risk signals.

- High-risk payment fraud arises when automated systems accept free address verification checks that validate format but not credibility.

- Cross-border and remote applicant profiles with unverifiable physical addresses bypass simplified AVS checks, increasing AML audit exposures.

Recognizing the fraud patterns is useful, but prevention depends on choosing the right verification approach from the start.

Manual vs Automated Address Verification

Manual and automated address verification approaches produce very different fraud, compliance, and operational outcomes in fintech environments.

Here is a side-by-side comparison to help you evaluate risk exposure, scalability, and control depth.

If you are moving beyond manual reviews or basic AVS checks, AiPrise strengthens automated proof-of-address verification using AI-driven document authentication and real-time multi-source validation.

Best Practices for Online Address Verification for Fintech

Strong online address verification for fintech reduces onboarding fraud, strengthens KYC compliance, and limits downstream AML exposure.

Here are the best practices that help you build a resilient and scalable address verification framework.

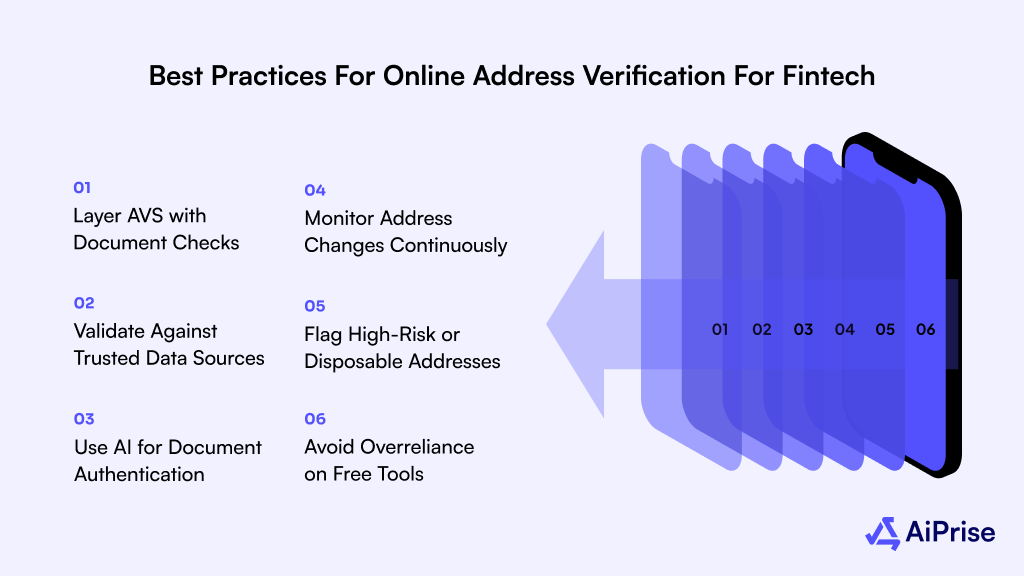

1. Layer AVS with Document Checks

Relying only on an Address Verification System AVS creates validation gaps that sophisticated fraudsters easily exploit. Combining AVS responses with proof-of-address documents such as utility bills or bank statements improves ownership validation accuracy.

This layered approach strengthens online address verification for fintech while reducing synthetic identity onboarding risks.

2. Validate Against Trusted Data Sources

Address verification service check processes should cross-reference government databases, credit bureaus, and utility records whenever possible. Multi-source validation detects mismatches between declared addresses and established financial or residential history patterns.

This strengthens compliance alignment and reduces false approvals that increase fraud and AML exposure.

3. Use AI for Document Authentication

Manual document inspection cannot reliably detect digitally altered proof-of-address submissions or hidden metadata manipulation risks. AI-based OCR, tamper detection, and pattern recognition significantly improve fraud detection across uploaded address documents.

Platforms such as AiPrise embed these capabilities into automated workflows, helping you identify AI proof of address generator misuse through intelligent anomaly scoring and multi-source validation.

4. Monitor Address Changes Continuously

Fraud risk does not end after onboarding, especially in high-velocity fintech transaction environments. Continuous monitoring flags unusual address updates, duplicate address clusters, and high-risk geographic patterns in real time.

Ongoing online address verification for fintech platforms reduces mule account creation and layered laundering activity.

5. Flag High-Risk or Disposable Addresses

Certain residential clusters, mail-forwarding services, and temporary addresses frequently appear in fraud investigations. Risk-based scoring helps you detect reused, synthetic, or high-frequency addresses across multiple accounts.

Proactively blocking suspicious address patterns prevents future compliance escalations and operational losses.

6. Avoid Overreliance on Free Tools

Free address verification for fintech tools often confirms formatting accuracy but fails to validate true occupancy or ownership legitimacy. Generate proof of address online; free solutions can be manipulated without strong backend verification controls.

Enterprise-grade automation ensures stronger regulatory defensibility and lower long-term fraud costs.

Also read: Understanding ID And Verification Of Residence Proof

Even with best practices in place, tool selection can determine whether your controls hold up under real transaction pressure.

Free Address Verification Tools vs Enterprise-Grade Systems

Choosing between free tools and enterprise systems directly impacts fraud exposure, compliance readiness, and operational scalability in fintech environments.

Here is how free address verification for fintech compares with enterprise-grade address verification systems in real-world risk scenarios.

Free tools may help you confirm whether an address exists, but they do not validate whether the applicant actually resides there. Enterprise-grade online address verification for fintech platforms connects address data with identity intelligence, transaction monitoring, and compliance controls.

How AiPrise Helps Strengthen Address Verification in Fintech?

Modern fintech verification demands more than surface-level checks; it requires integrated, intelligent, and scalable address validation.

Here is how AiPrise strengthens address verification for fintech while improving compliance efficiency and fraud resilience.

- Proof of Address: Automatically extracts address data, validates ownership, and performs tamper detection against official document templates.

- Multi-Source Government & Database Checks: Cross-verifies submitted address details against 100+ government databases, registries, and trusted data partners.

- Document Insights Engine: Detects metadata edits, overwritten text, font inconsistencies, and document manipulation in real time.

- Dynamic Risk Scoring: Assigns real-time address risk scores using custom rules tailored to your risk tolerance and compliance model.

- Geo-Optimized KYC/KYB Workflows: Routes verification through localized data vendors to improve match rates and reduce false positives globally.

- Ongoing Monitoring & Reverification: Flags suspicious address updates, high-risk logins, and account changes before they escalate into AML exposure.

- Compliance Co-Pilot: Reduces manual document review time by up to 95 percent while generating audit-ready reports for regulatory scrutiny.

- Case Management Dashboard: Centralizes address verification outcomes, escalations, audit trails, and reporting within a unified compliance view.

By consolidating proof-of-address validation, fraud detection, and compliance automation into a single API-driven platform, AiPrise enables you to reduce onboarding friction while maintaining stronger regulatory defensibility.

Wrapping Up

Address verification for fintech is no longer a supporting control; it is a frontline defense against onboarding fraud, synthetic identities, and regulatory exposure. Strong online address verification for fintech platforms directly reduces fraud losses, protects customer trust, and strengthens your KYC and AML compliance posture.

AiPrise helps you unify proof-of-address validation, AI-driven risk scoring, and continuous monitoring into a single automated workflow built for regulated fintech growth.

If you are serious about reducing fraud while maintaining seamless onboarding, Book A Demo and see how stronger address verification transforms your compliance strategy.

FAQs

1. What is address verification in fintech?

Address verification in fintech is the process of confirming that a customer’s residential address is valid, deliverable, and legitimately linked to their identity during KYC onboarding. It typically involves an Address Verification System AVS, proof-of-address document validation, and database cross-checks to reduce fraud risk.

2. How does an Address Verification System (AVS) work?

An Address Verification System AVS compares the billing address submitted by a customer with the address on file at the card issuer. It returns a match or mismatch response but does not confirm ownership or residency, which is why additional verification layers are often required.

3. Is AVS enough for KYC compliance?

AVS alone is not sufficient for full KYC compliance because it only validates billing address components. Regulated fintech platforms typically require proof-of-address documents, database verification, and risk-based monitoring to meet AML and CIP obligations.

4. What documents are accepted as proof of address?

Common proof-of-address documents include recent utility bills, bank statements, lease agreements, and government-issued correspondence showing the customer’s name and residential address. Most financial institutions require documents dated within the last three months.

5. Can proof of address be generated online for free?

While some tools claim to generate proof of address online for free, these documents often fail authenticity checks and increase compliance risk. Financial institutions use automated tamper detection and multi-source address verification service checks to detect fabricated submissions.

You might want to read these...

.png)

.png)

.png)

.png)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately