AiPrise

12 min read

January 19, 2026

How Fintechs Automate KYB Checks To Cut Verification Time And Risk 2026

.jpg)

Key Takeaways

You can launch new fintech products quickly, but business onboarding often slows you down. Every new merchant, platform partner, or corporate customer you onboard requires KYB checks to confirm legitimacy, identify ownership, and assess financial risk. When these checks depend on manual reviews and scattered data sources, approvals drag on, your team spends hours on follow-ups, and potential customers drop off.

The impact goes beyond inefficiency. Weak KYB controls expose you to shell companies that exist primarily on paper and are used to hide ownership or move suspicious funds. Risk signals are already common. Registered companies in the United States have the most flags for financial anomalies, with over 1.25 million flagged activities. These include revenues, profits, or capital flows that do not match industry averages.

That’s why automation matters now. In this blog, you’ll learn how fintechs automate KYB checks to verify businesses faster, reduce manual effort, and keep compliance strong as you scale.

At a Glance

- Human-led reviews create delays, raise costs, and leave gaps in ownership visibility, making it harder to spot shell companies and stay compliant at scale.

- Automated systems collect data, verify businesses, assess ownership, and flag only high-risk cases, reducing manual effort while improving speed and accuracy.

- Scalable KYB relies on three connected components: strong verification sources, intelligent risk decisioning, and workflow automation. These work together to approve low-risk businesses quickly and handle exceptions.

- Implementation success depends on data quality and adaptability. Clear goals, reliable data sources, configurable risk rules, and phased rollouts help you automate KYB without disrupting onboarding or compliance.

- By combining KYB, UBO verification, sanctions screening, risk scoring, and continuous monitoring, AiPrise helps fintechs scale KYB with confidence and control.

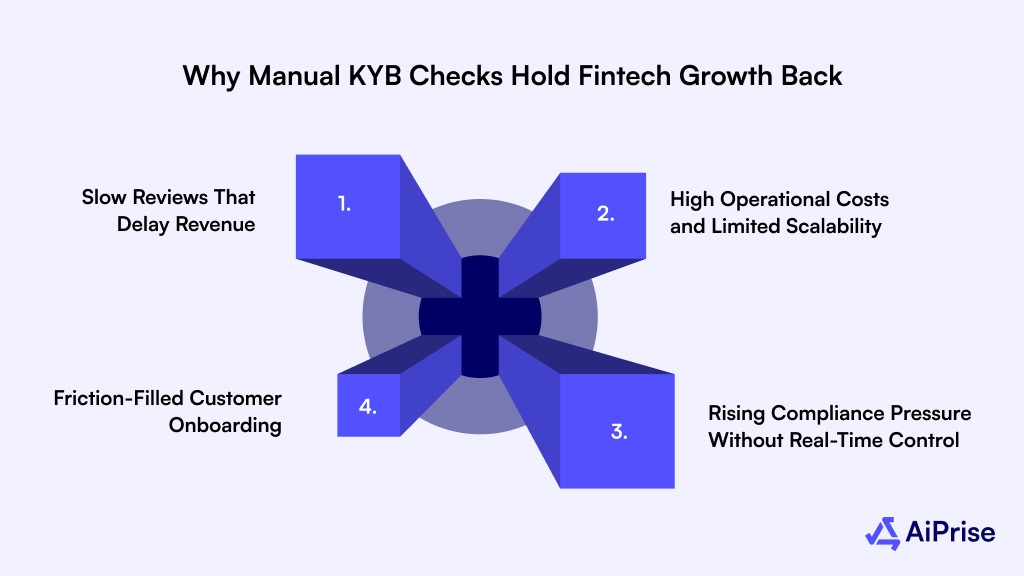

Why Manual KYB Checks Hold Fintech Growth Back

Manual KYB processes were built for a time when onboarding volumes were lower and regulatory expectations were simpler. Today, they slow you down, increase risk, and create friction for both your teams and your customers. If KYB is still largely manual, these are the core issues you’re likely facing.

Slow Reviews That Delay Revenue

Manual KYB requires your compliance team to gather, enter, and validate business data across multiple registries, sanctions lists, tax records, and other documents. Each additional entity, shareholder, or jurisdiction adds more review time. This leads to:

- Long onboarding cycles that stretch from hours to several days

- Backlogs during high-volume onboarding periods

- Delayed activation for legitimate businesses

High Operational Costs and Limited Scalability

Manual KYB does not scale well. As your onboarding volume increases, so does your reliance on larger compliance teams. This raises operational costs and introduces human error, making it harder to maintain consistent risk standards across regions. You’re left managing:

- Rising compliance headcount

- Inconsistent decision-making

- Difficulty scaling into new markets

Rising Compliance Pressure Without Real-Time Control

KYB requirements continue to change across regions, especially around beneficial ownership, AML, and ongoing monitoring. When checks are handled manually, staying aligned becomes difficult.

Without real-time updates or standardized KYB workflows, you risk these common challenges:

- Applying outdated regulatory rules

- Inconsistent reviews across teams or regions

- Limited visibility into ongoing compliance risks

Friction-Filled Customer Onboarding

From the customer’s perspective, manual KYB feels repetitive. Multiple document requests and long wait times damage trust early in the relationship. This often results in:

- Higher onboarding drop-off rates

- Lost deals to faster-moving competitors

- A poor first impression of your platform

These limitations explain why fintechs are shifting away from manual KYB and toward automated verification.

What KYB Automation Means and Why It Matters

KYB automation is the use of technology to handle core business verification tasks, such as collecting company data, validating records, identifying beneficial owners, and assessing risk. It involves minimal manual effort. Instead of relying on spreadsheets and human reviews at every step, automated systems pull data from trusted sources. Then they run real-time checks and flag only high-risk cases for deeper review.

This matters because KYB is not optional. Compliance with Anti-Money Laundering (AML), Combating Financing of Terrorism (CFT), and Counter-Proliferation Financing (CPF) rules is essential for protecting trust across the financial system. Regulators expect accuracy, consistency, and ongoing oversight, even as onboarding volumes grow.

At the same time, KYB is resource-heavy. It consumes significant staff time, high operational costs, and compliance resources that could be used to support growth and product development.

Key Insight: By automating KYB, you reduce human error, speed up onboarding, and free your teams to focus on risk decisions that truly need expertise.

Also Read: Streamlining Business Onboarding with KYB: Ensuring Compliance and Efficiency

To make automation effective, you need a structured approach that connects data, decisioning, and review.

What are The Three Core Components of Building Scalable KYB Automation?

Effective automation works as a structured system, where each component plays a distinct role in reducing risk, speeding up onboarding, and limiting unnecessary manual reviews. Understanding this setup helps you design a KYB process that scales without weakening compliance.

Component 1: Verification Sources

This foundational component focuses on answering a critical question: Is this business real, active, and who controls it? Verification sources connect directly to trusted registries and databases to validate enterprises and their owners during onboarding.

What this component typically checks

- Legal business registration and operational status

- Beneficial owners, directors, and controlling parties

- IDs such as EINs or TINs

- Sanctions lists, watchlists, and PEP exposure

- Address, phone, and email risk indicators

Example: You operate a U.S.-based payments platform that onboards small businesses. This component confirms that each merchant is registered, active, and not linked to any sanctioned individuals before processing transactions.

Pro Tip: Choose verification sources that support global coverage and continuous updates.

If address validation is part of your KYB flow, automated proof-of-address verification can further strengthen this foundation. AiPrise helps confirm whether a business actually operates from its declared location, reducing exposure to shell entities and misrepresented addresses.

Component 2: Risk Orchestration and Decisioning

Once business data is collected, orchestration systems determine how to act on it. This component aggregates all verification results and applies risk logic to determine whether a business should be approved, flagged, or declined.

Modern decisioning platforms combine configurable rules with machine learning to evaluate risk across hundreds of signals.

What happens here

- Automated risk scoring based on ownership, geography, and financial signals

- Instant approvals for low-risk businesses

- Automatic escalation of higher-risk cases

- Ongoing tuning of rules and thresholds

Why it matters: Without orchestration, every case requires human review. With it, most legitimate businesses move through automatically, while your compliance team focuses on the exceptions that genuinely matter.

Component 3: Workflow Automation for Exception Handling

No KYB system can eliminate human judgment. When data is incomplete or risk indicators appear, cases move into manual review. Workflow automation ensures these reviews stay fast, consistent, and auditable.

Common triggers for manual review

- Newly formed businesses that are not yet visible in registries

- Complex or layered ownership structures

- Sanctions, adverse media, or PEP matches

- Data inconsistencies or document quality issues

How workflow automation helps

- Routes cases to the right analyst automatically

- Pre-populates review screens with relevant data

- Tracks actions and decisions for audit trails

- Reduces review time and operational errors

How These Components Are Held Together in Practice

KYB automation relies on multiple techniques working in parallel, not in isolation.

Why this structure works: Rules provide consistency, data analysis detects anomalies, and AI improves over time. Together, they reduce manual effort while strengthening compliance outcomes.

Also Read: Understanding KYB Risk Factors and Assessment

Once you understand how fintechs automate KYB checks, the next step is execution. Here's how you need to proceed.

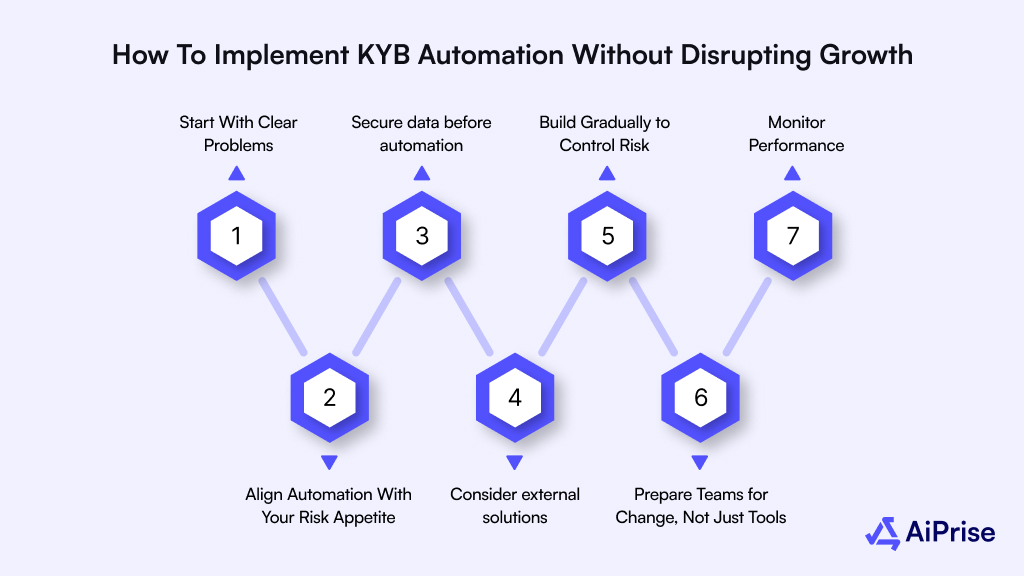

How to Implement KYB Automation Without Disrupting Growth

A strong implementation plan helps you reduce risk, protect conversion rates, and avoid costly compliance mistakes. Below are practical, field-tested principles to guide a successful KYB automation rollout.

Step 1: Start With Clear Problems and Measurable Goals

Before selecting any solution, be clear about what you’re trying to fix. KYB automation should solve specific pain points, not just modernize your stack. Ask yourself:

- Are legitimate businesses being rejected too often?

- Is manual review slowing merchant activation?

- Are compliance costs growing faster than onboarding volume?

- Do regulatory reviews require more substantial proof of business legitimacy?

Why it matters: Clear goals help you choose automation that aligns with your risk tolerance and regulatory obligations instead of over- or under-screening businesses.

Step 2: Align Automation With Your Risk Appetite

Not every fintech faces the same level of risk. Your KYB automation should reflect the industries you serve, transaction volumes and values, geographic exposure, and regulatory scrutiny.

What flexibility looks like

- Adjustable risk thresholds

- Configurable approval and escalation rules

- The ability to adapt as regulations or business models change

Step 3: Secure Reliable Data Before Automating Decisions

Automation is only as good as the data behind it. Using unreliable or outdated sources can lead to serious errors. Focus on data that is:

- Authoritative and frequently updated

- Consistent across regions where you operate

- Able to support beneficial ownership and risk screening

Step 4: Consider External Solutions Before Building In-House

Building KYB automation from scratch is expensive and time-consuming. For most fintechs, using established platforms delivers faster results with lower risk. External solutions often provide:

- Pre-trained risk models

- Regulatory updates built in

- Faster deployment and scalability

Struggling to scale KYB checks without adding manual reviews or slowing business onboarding? AiPrise automates KYB verification with global data coverage, dynamic risk scoring, and ongoing monitoring so that you can focus on growth.

Step 5: Build Gradually to Control Risk

Rolling out too many changes at once makes it hard to spot problems. If you're building in-house, a phased approach makes more sense, as it reduces disruption. Best practices include:

- Adding automation components one at a time

- A/B testing changes on limited volumes

- Reviewing impact before full rollout

Did you know? Many fintechs test automation logic against historical onboarding data to estimate its impact before going live.

Step 6: Prepare Teams for Change, Not Just Tools

Automation works best when your compliance team understands why it’s being implemented. Practical training should explain:

- How automation reduces repetitive work

- Which cases still require human judgment

- How risk decisions are made

Step 7: Monitor Performance and Refine Regularly

KYB automation is not a “set it and forget it” system. Ongoing evaluation ensures it delivers real value. Track metrics such as:

- Manual review rates

- Business activation speed

- False rejections and approvals

- Compliance exceptions and audit outcomes

If performance drops, adjust rules, data inputs, or workflows quickly.

Also Read: KYB Due Diligence: Proven Ways to Cut Compliance Risk

To put all of this into perspective, even the most well-planned KYB automation strategies can face real-world constraints once they go live. Understanding these risks up front helps you design safeguards before they become operational or compliance issues.

What are the Common Challenges Fintechs Face With KYB Automation?

Even with the right intent and tools, automating KYB is not always straightforward. Most challenges come from data gaps, technical limits, and real-world onboarding behavior. Below are the most common obstacles fintechs run into when moving from manual to automated KYB.

- No single source of verified business data: There is no universal or fully authoritative database for business verification. You often need to pull information from multiple registries, tax authorities, sanctions lists, and commercial data providers. As a result, automation is left to work with fragmented inputs, which increases complexity.This becomes even more difficult when different databases show different versions of the same business, such as old addresses, inactive directors, or outdated ownership details. When automation relies on conflicting data, it can lead to:

- Incorrect risk scores

- False rejections of legitimate businesses

- Missed red flags

- Friction during document and ID collection: Automation depends on cooperation from business representatives. This resistance can reduce completion rates and delay approvals. Some hesitate to submit information digitally due to:

- Privacy concerns

- Lack of understanding of automated verification

- Preference for traditional, manual processes

- Difficulty standardizing risk rules across regions: KYB requirements vary by country. Applying the same automation logic globally can create compliance gaps if local regulations are not reflected accurately in workflows.

- Limits in document recognition and processing: Automated KYB tools can efficiently process standard documents, such as certificates of incorporation or tax filings. But challenges arise with:

- Unstructured or free-form documents

- Region-specific formats that the system hasn’t seen before

- Files that are missing required details due to user error

A good example of overcoming these hurdles is this real-world case study: "A Fast-Growing AR Platform Streamlines Global KYB With AiPrise."

While these challenges are common, they’re not permanent barriers. You need a platform built specifically to handle fragmented data, regional complexity, and scale without adding manual overhead.

How AiPrise Enables Scalable KYB Automation for Fintechs

KYB automation only works when it removes friction without weakening risk controls. For you, that means verifying businesses quickly, identifying real ownership, and staying compliant as volumes and regulations grow. AiPrise is built to do exactly that. It brings speed, accuracy, and continuous oversight into one KYB framework.

Below is how AiPrise supports effective KYB automation in practice:

- Custom-Branded, Low-Friction Business Onboarding: It enables you to design KYB onboarding flows that fit your product. Using flexible, branded forms, you can collect required business information without overwhelming applicants. Also, it allows them to save progress and return, reducing abandonment and improving activation rates.

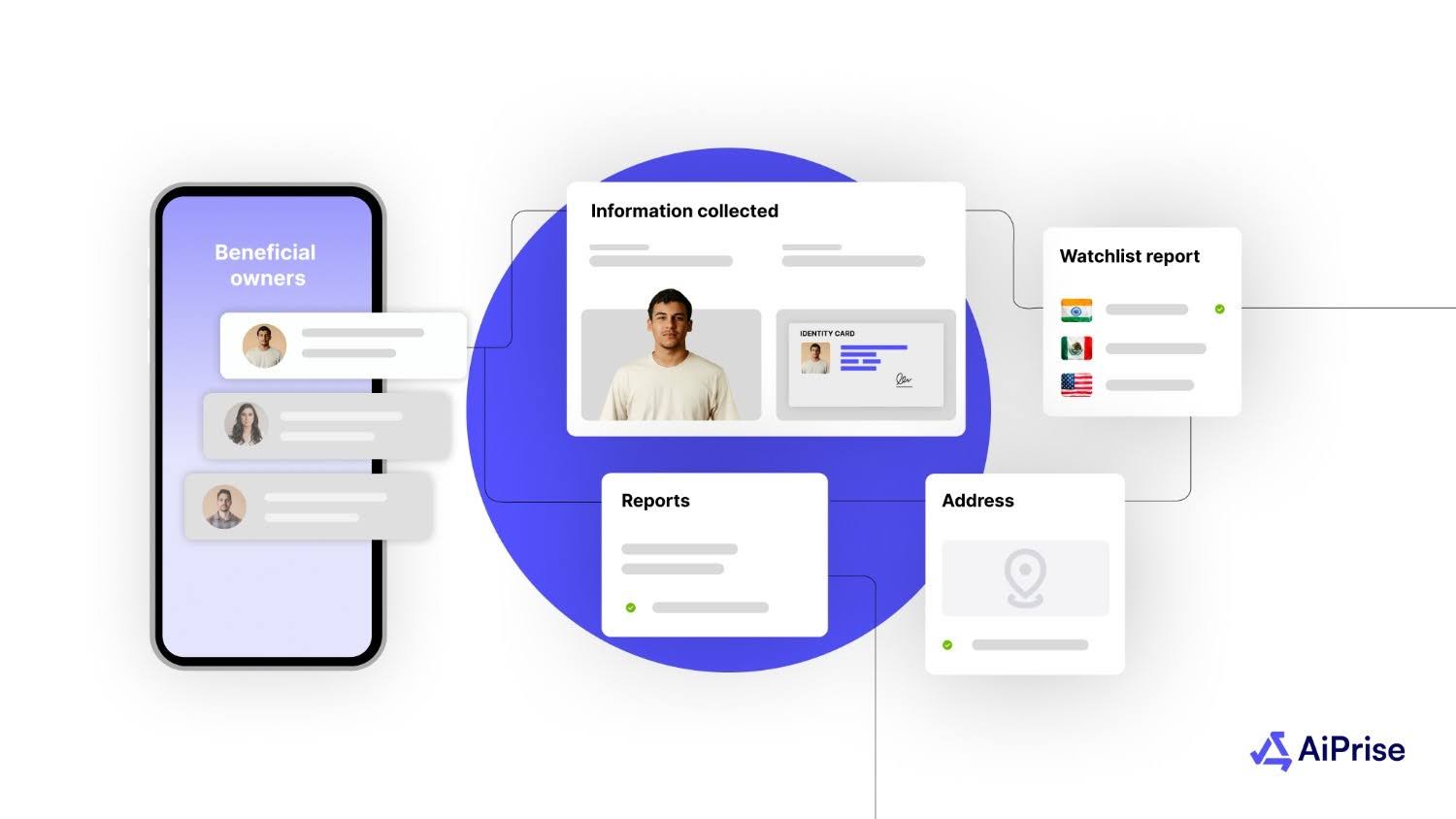

- Deep and Fast Ultimate Beneficial Owner (UBO) Verification: AiPrise provides clear visibility into ownership structures by mapping beneficial owners and finding complex or hidden relationships.

- Dynamic, Risk-Based Decisioning: It applies real-time risk scoring based on your internal rules and regulatory needs. Instead of static thresholds, risk scores adapt with new data. This allows you to apply enhanced due diligence only when needed.

- Online Presence and Business Activity Analysis: The solution goes beyond registry data to identify industry classifications, review social presence, and detect suspicious websites or inconsistencies that may indicate fraud or misrepresentation. This added context strengthens KYB decisions.

- Automated Sanctions and Watchlist Screening: Businesses, owners, and related entities are screened against sanctions lists and watchlists in real time.

- Continuous KYB Monitoring After Onboarding: It continuously monitors changes in ownership, registration status, and risk signals. Alerts are triggered when meaningful changes occur, allowing you to act early and reduce downstream exposure.

Together, these capabilities allow you to automate KYB checks without sacrificing visibility or control.

Conclusion

As fintechs expand, KYB cannot be treated as a one-time onboarding task. Business risk and ownership changes, with regulatory scrutiny increasing over time. Relying on manual reviews or disconnected tools makes it harder to keep up, often at the cost of speed, consistency, or confidence in your decisions.

AiPrise helps you move beyond these limits by bringing automation, verification, and ongoing oversight into a single KYB framework. With clearer ownership insight, adaptive risk scoring, and continuous monitoring, you can approve legitimate businesses faster while staying aligned with global compliance expectations.

Ready to implement KYB automation that supports growth instead of slowing it down? Book A Demo to see how AiPrise fits into your verification, onboarding, and risk workflows.

FAQs

1. Is KYB automation suitable for cross-border or global onboarding?

It is often essential for cross-border onboarding. Automation helps standardize checks across jurisdictions while adapting to local data availability and regulatory requirements, reducing inconsistencies that usually arise with manual, country-by-country KYB processes.

2. Can KYB automation differentiate between legitimate complex structures and shell companies?

Yes, when automation evaluates ownership depth, control paths, and economic activity together. Legitimate holding structures usually show operational consistency, while shell entities often reveal weak business presence, circular ownership, or unexplained financial anomalies.

3. What operational metrics improve most after deploying KYB automation?

You'll see faster business activation, lower manual review volume, improved approval consistency, and reduced rework during compliance reviews, especially for repeat onboarding patterns.

4. How do fintechs test KYB automation before rolling it out fully?

Most teams backtest automation logic against historical onboarding data to measure shifts in approval and risk exposure. Controlled rollouts or parallel runs help isolate the impact before automation replaces existing workflows.

5. Does KYB automation reduce false positives or increase them?

When configured correctly, KYB automation reduces false positives by using multiple data signals instead of single-source checks. Poor configuration or weak data quality, however, can increase false alerts, making tuning and review critical to long-term accuracy.

You might want to read these...

AiPrise

KYB Compliance: 2026 Regulations You Should Know About

As organizations expand globally and face tighter regulations, adherence to Know Your Business (KYB) standards has become one of the most critical compliance layers for fintech, online marketplaces, and other companies that need to verify business customers before letting them perform financial transactions.

%20Can%20Improve%20Your%20Compliance%20Strategy.png)

%20Verification%20in%20the%20US.png)

AiPrise

5 min read

How KYB Verification Works in the US: The Ultimate Guide for Navigating Know Your Business

You can approve a new business customer in minutes. Or you can lose them while your team searches through registries, ownership records, and sanctions lists, trying to piece everything together.

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately