AiPrise

11 min read

June 16, 2026

How to Build a KYB and KYC Workflow for Compliance

Key Takeaways

Every new customer your compliance team onboards manually is time lost to spreadsheets and follow-up emails. And the cost of getting it wrong keeps climbing.

In 2025 alone, US AML and KYC failure penalties topped $1.1 billion, with crypto exchanges, money transmitters, securities firms, and casinos all fined for weak or missing programs. Meanwhile, fraud losses reached over $12.5 billion in 2024, according to the FTC, a 25% jump year-over-year.

In short, the pressure isn't easing. For fintechs, neobanks, and payment platforms scaling across borders, a disjointed verification process creates bottlenecks at the worst possible moment: onboarding. Your prospective customers are ready to convert, but your compliance process is what's slowing them down. A solid KYC and KYB workflow can fix this problem.

We’ll explain what KYB and KYC workflows actually look like and how you can implement one in your organization.

Key Takeaways

- A structured KYC workflow follows four stages: customer identification (CIP), customer due diligence (CDD), enhanced due diligence (EDD) for high-risk cases, and ongoing monitoring. Skipping or weakening any stage creates gaps that regulators and bad actors will find.

- Manual KYC and KYB won’t scale. Automation is the primary lever for reducing costs without weakening your compliance standards.

- The industry is shifting from periodic batch reviews to continuous KYC and KYB, where risk profiles are updated in real time based on live data. Automated, event-driven monitoring closes the gaps left by calendar-based reviews.

What Are KYC and KYB Workflows?

KYB workflows verify business entities and their ownership structures, while KYC workflows verify individual customers. You need both for comprehensive compliance.

What Are KYC Workflows?

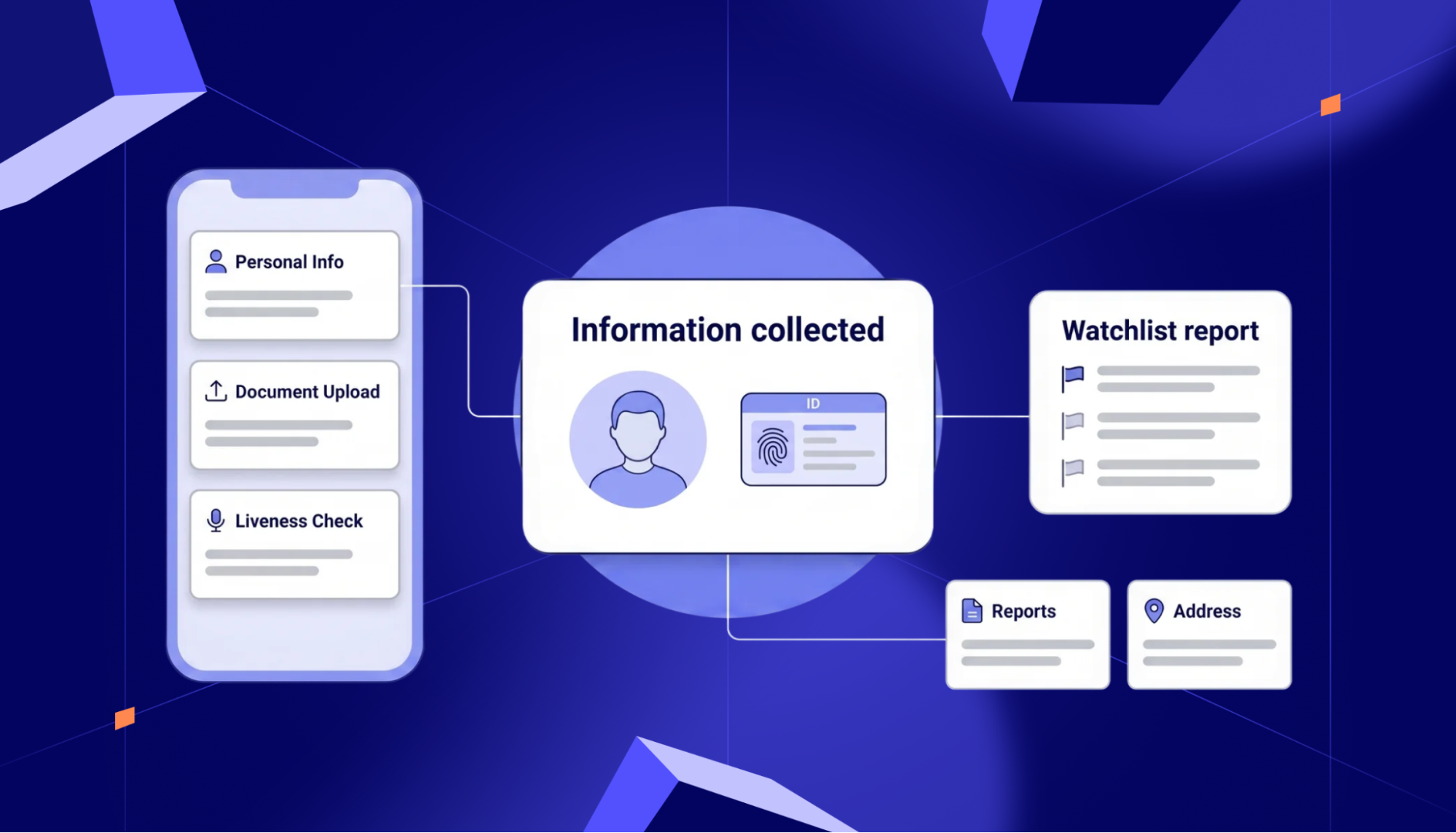

KYC (Know Your Customer) is a regulatory requirement for financial institutions and other regulated businesses to verify customers' identities and assess risk before establishing a business relationship. It’s a sequence of steps that takes a customer from initial data collection through identity verification, risk assessment, due diligence, and ongoing monitoring.

If you don’t have an automated KYC workflow, verification remains an ad hoc process. This happens because human reviewers have to gather information and complete checks manually, so they apply the standards inconsistently and can’t keep up with high volumes of KYC checks in time.

Automated workflows use AI-powered verification, real-time screening, region-specific screening, and rule-based routing to handle the same steps faster and more consistently.

What Are KYB Workflows?

KYB workflows are systematic processes that businesses use to verify the identity, legitimacy, and risk profile of other businesses before establishing relationships. These workflows combine document collection, data verification, screening procedures, and ongoing monitoring to ensure compliance with anti-money laundering (AML) regulations and other legal requirements.

Unlike KYC processes that focus on individual verification, KYB workflows must navigate additional layers of complexity. They need to verify corporate structures, identify ultimate beneficial owners (UBOs), assess business legitimacy, and monitor for changes in ownership or risk status over time.

What Are The Differences Between KYC and KYB Workflows?

Here’s an overview of how a KYC workflow compares to KYB:

Why Do You Need to Build Strong KYC and KYB Workflows?

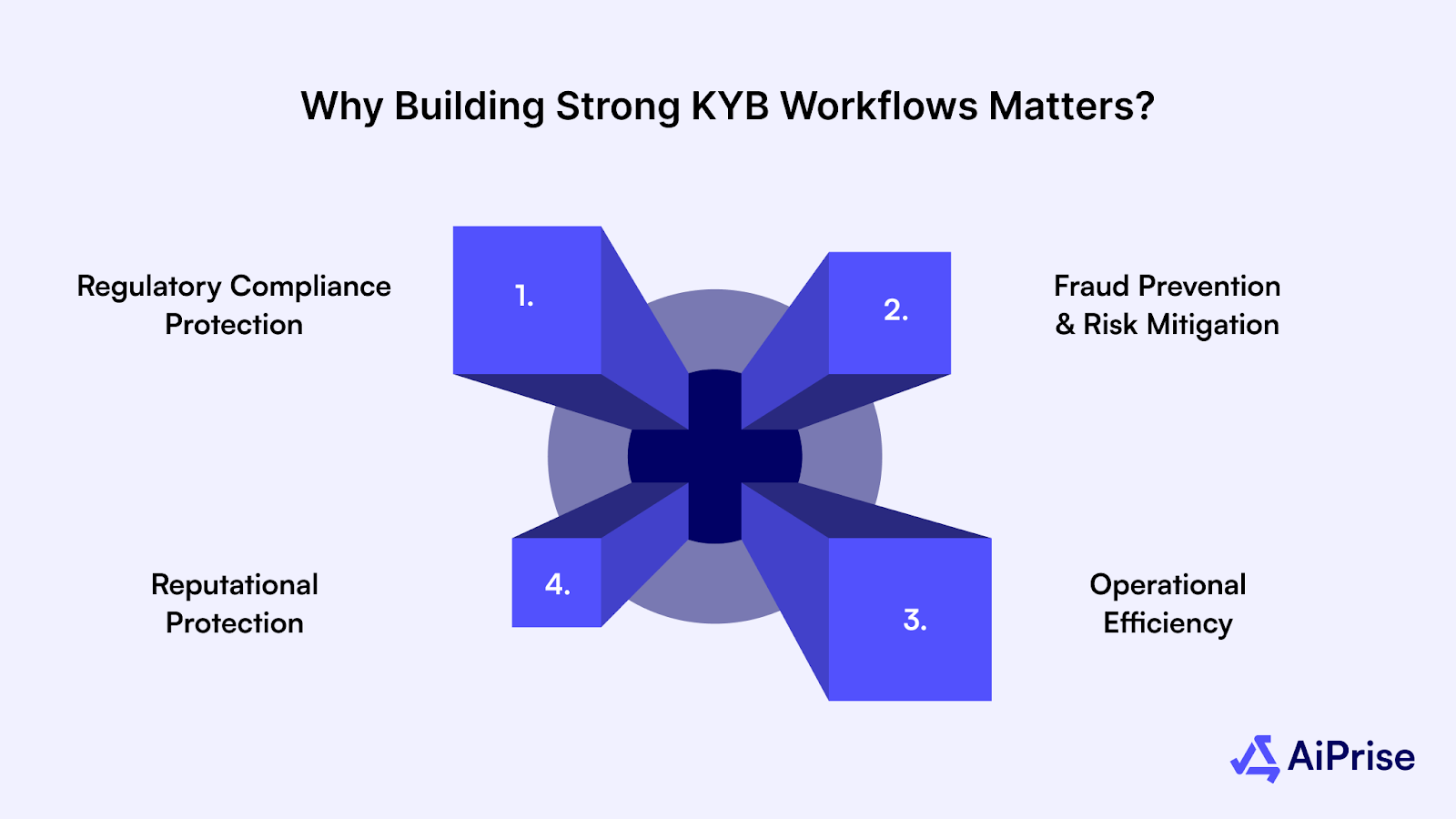

Strong KYC and KYB workflows are essential because they serve as your primary defense against major risks like regulatory fines, fraud, and reputational harm. These workflows don't just help you comply with rules; they also create strategic advantages, as mentioned below:

Regulatory Compliance Protection

Regulatory bodies worldwide have intensified their focus on business verification. The Financial Crimes Enforcement Network (FinCEN) in the United States requires financial institutions to identify and verify the beneficial owners of legal-entity customers. The FCA, MAS, and FATF member states all require documented, auditable KYC processes.

The EU's 5th and 6th Anti-Money Laundering Directives impose similar requirements with substantial penalties for non-compliance.

According to recent data, GDPR violations alone resulted in fines totaling €1.2 billion in 2024, bringing the total to €5.88 billion since 2018. Inadequate KYB processes expose organizations to similar regulatory risks across multiple jurisdictions.

A defined verification workflow ensures that every customer goes through the same checks, making it easier to demonstrate compliance during audits. That matters when you consider the cost of getting it wrong.

In the US and Canada alone, the annual cost of financial crime is estimated at $61 billion. And it’s mostly applicable to mid- and large-sized financial institutions. You need to get the workflow right as it’s a cost lever.

Fraud Prevention and Risk Mitigation

Effective KYB workflows serve as a critical defense against various forms of business fraud. Shell companies, fraudulent documentation, and concealed beneficial owners are common tactics used by bad actors to infiltrate legitimate business networks.

With fraud losses continuing to rise—including $789 million from government imposter scams alone in 2024—robust verification workflows are no longer optional. They provide the first line of defense in identifying suspicious entities before they can cause harm.

But fraud isn't limited to the business side. Reported consumer fraud losses jumped to over $10 billion in 2023 and $12.5 billion in 2024, with 2.6 million fraud reports and rising per-victim losses. That points to more successful high-value account takeovers and scams targeting individuals.

If you use strong Know Your Customer workflows with ongoing due diligence, you can directly target the root cause and help reduce fraud.

Operational Efficiency

Well-designed KYB workflows strike a balance between thoroughness and efficiency. Manual verification processes can take days or weeks, creating friction in business relationships and potentially leading to the loss of valuable clients to competitors with faster onboarding.

The numbers back this up. Seventy percent of financial institutions lost customers in the past year due to inefficient onboarding. The issue is that slow verification frustrates customers, but more importantly, it increases your exposure to financial crimes.

If you create a concrete KYC or KYB workflow, it can remove unnecessary friction for low-risk customers while giving you time to review high-risk cases as they come.

Automated workflows reduce verification time from days to hours or even minutes, improving customer experience while maintaining compliance standards. This efficiency directly translates into competitive advantage in fast-moving industries like fintech and cryptocurrency.

Reputational Protection

Association with fraudulent or sanctioned entities can devastate a company's reputation. News of businesses unknowingly facilitating money laundering or terrorist financing can result in lost customer trust, damaged partnerships, and long-term brand harm. This damage far exceeds any immediate financial penalties.

To achieve these essential benefits, a KYB workflow must be built on a reliable foundation.

Scalable Compliance

As your customer base grows, especially across borders, manual processes break down. A workflow designed for 500 customers a month won't hold at 5,000 or 50,000. Every new market adds different document types or regulatory thresholds, which means you’re also held to different verification standards depending on the type of verification.

A standardized KYC workflow ensures your compliance standards hold regardless of volume. For instance, platforms like Aiprise let you do the following:

- Configure country-specific or region-specific verification rules

- Route cases to human reviewers based on risk tiers

- Scale onboarding volume without increasing your headcount or verification time

When you automate KYC using an AI-powered platform, compliance becomes a routine process in your organization.

Core Components of Effective KYC Process Workflows

The components of a KYC workflow depend on the documents and data you need to verify an individual’s identity and understand their risk profile. It usually includes the following phases:

- Customer Identification (CIP): You’ll need to collect the minimum identifying information required by regulation. Then, you would verify this identifying information against authoritative sources.

- Customer Due Diligence (CDD): Once identity is confirmed, CDD assesses risk. You’ll screen the customer’s profile against global sanctions lists, PEP databases, and adverse media, then assign a risk score based on the results.

- Enhanced Due Diligence (EDD): This step gets triggered if a customer is flagged as high-risk during CDD. It involves conducting a deeper investigation by verifying the source of funds and obtaining approval from senior management.

- Ongoing Monitoring: KYC doesn't end at onboarding. You need to continuously screen customers after onboarding to catch changes in their sanctions status or if they engage in unusual transaction behavior.

Step-by-Step Guide to Build KYC Workflows

Let’s say you’re a fintech launching a payments product and you need to verify a customer’s KYC information before activating their account. Here’s an example of the KYC workflow you might use:

Step 1: Customer Identification Program (CIP)

In this step, you collect the minimum identifying information required by regulations before establishing a business relationship. For instance, if you’re a US financial institution operating under the USA PATRIOT Act, CIP requires:

- Full legal name

- Date of birth

- Government-issued ID number (SSN, passport, or national ID)

- Residential address

Documents are verified against government databases or through authentication methods such as OCR, NFC chip reads, and tamper detection. The goal is to confirm the person exists and is who they say they are.

At this stage, automation makes the biggest difference in speed. Manual data entry and document review are where onboarding delays typically start. Automated document capture and verification compress this step from hours to seconds without compromising verification quality.

Step 2: Customer Due Diligence (CDD)

Once you've confirmed the customer’s identity, CDD takes the process a step further. In this step, you're verifying the customer's background and assessing the risk of doing business with them.

This step covers several checks, such as:

- Sanctions screening: Checking the customer against OFAC, EU, UN, and other global sanctions lists.

- PEP screening: Identifying politically exposed persons who face a higher corruption and bribery risk.

- Adverse media checks: Scanning for negative news coverage related to financial crime, fraud, or regulatory action.

- Risk scoring: Assigning a risk level (low, medium, or high) based on geography, transaction patterns, screening results, and other signals.

You’ll be able to apply a risk tier that determines what happens next. While low-risk customers move forward, medium-risk cases require a second look, and high-risk cases trigger an Enhanced Due Diligence (EDD) process.

Note: Platforms like AiPrise combine identity verification, sanctions screening, and risk scoring in a single automated step. Instead of your analysts cross-referencing three or four tools, the entire CDD process runs in a single pass, producing consistent, auditable output.

Step 3: Enhanced Due Diligence (EDD)

When CDD identifies a high-risk case, you need to start looking at the following:

- PEPs and their close associates

- Customers from high-risk jurisdictions (FATF grey or blacklist countries)

- Unusual transaction patterns or an inconsistent stated purpose of the account

- Complex ownership structures that obscure the source of funds

- Source-of-Wealth documentation

Only after you’ve done a thorough analysis should you pass it on to senior management for approval. This ensures compliance by giving you more than one pair of eyes on the documents and having final approval come from an experienced analyst.

Step 4: Ongoing Monitoring and Perpetual KYC

You need ongoing monitoring because risks don’t stay the same. For example, a customer who was clean at onboarding could appear on a sanctions list six months later, changing their risk profile.

Ongoing monitoring covers four areas: transaction monitoring, sanction list updates, periodic reviews, and perpetual KYC (pKYC).

While the first three areas follow the same process outlined above, pKYC requires you to move from calendar-based review to continuous, event-driven monitoring. This is where automation matters most, as KYC platforms can automatically scan thousands of databases and re-verify KYC in real time.

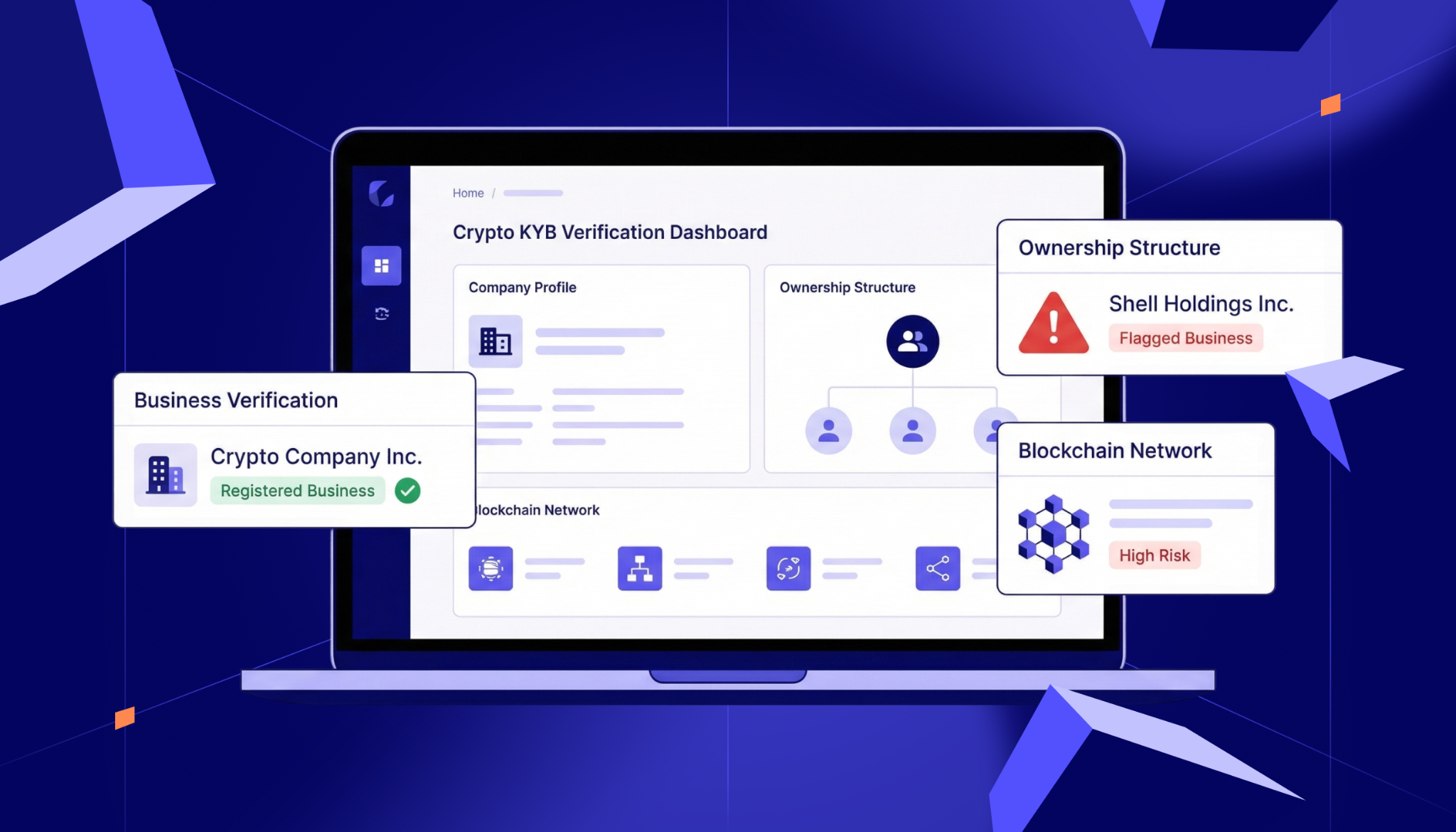

Core Components of Effective KYB Workflows

The core components of an effective Know Your Business (KYB) workflow are the steps necessary to verify a business entity's identity, ownership structure, and risk profile for compliance and fraud prevention.

The key elements can be categorized into four main phases:

- Business Verification: Confirming the company's legal identity and legitimacy by checking official registration documents and public registries.

- UBO Identification: Tracing the corporate structure to identify and verify the identities of all Ultimate Beneficial Owners (UBOs).

- Risk Screening: Checking the business and its owners against sanctions lists, PEPs (Politically Exposed Persons), and adverse media to assess risk.

- Ongoing Monitoring: Continuously screening the entity to quickly detect any changes in ownership, status, or risk profile.

To operationalize these four phases effectively, organizations should follow a structured approach. Below is the step-by-step process for developing seamless KYB workflows.

Step-by-Step Guide to Build KYB Workflows

Building an effective KYB workflow is a crucial part of Anti-Money Laundering and Counter-Financing of Terrorism (CFT) compliance. It is a structured process for verifying a corporate customer's identity, legitimacy, and risk.

Here is a step-by-step guide to building an effective KYB workflow:

Step 1: Define Your Compliance Requirements

Before designing workflows, thoroughly understand applicable regulations in your operating jurisdictions. Requirements vary significantly between industries and regions.

Key Regulatory Frameworks

- Bank Secrecy Act (BSA) and Customer Due Diligence (CDD) Final Rule in the United States.

- European Union's 5th and 6th Anti-Money Laundering Directives (AMLD5, AMLD6).

- Financial Action Task Force (FATF) recommendations.

- Industry-specific regulations (payment services, cryptocurrency, securities).

Document your compliance obligations clearly.

Step 2: Establish Document Collection Protocols

Standardization is crucial for consistent, defensible verification. Create clear documentation requirements for different business types.

Step 3: Automate Identity and Registration Verification

This step involves using technology to quickly and accurately confirm the business's legal existence and the legitimacy of its documentation.

- Registry Checks: Integrate with official government registries and commercial data sources globally (e.g., U.S. Secretary of State filings, UK Companies House) via API. This allows you to verify details in real-time.

- Document Verification: Implement AI-powered document analysis to automatically check the authenticity of submitted files (e.g., Certificates of Incorporation).

- Cross-Referencing: Ensure the business data provided by the customer aligns with the data found in public registries. Discrepancies are a major red flag and should trigger an automatic manual review (escalation).

Step 4: Execute UBO and Control Person Identification (UBO/CP)

The most critical part of KYB is piercing the corporate veil to find the actual individuals who own or control the company.

- Beneficial Ownership Tracing: Systematically trace the ownership structure through multiple layers of corporate entities (subsidiaries, holding companies) until the ultimate individuals who own a set percentage (e.g., 25% or more) or exert control (e.g., senior management, directors) are identified.

- Source of Data: Use corporate filings, shareholder registers, and official regulatory filings to trace.

- Individual KYC: Once identified, run a full Know Your Customer (KYC) check on every UBO and Control Person, including identity verification (biometric or liveness checks if remote) and proof of address.

Step 5: Implement Comprehensive Risk Screening

Screening assesses the financial crime risk associated with the business and its associated individuals.

- Sanctions Screening: Screen the business, all UBOs, directors, and senior management against global Sanctions Lists.

- Watchlist and PEP Screening: Check all relevant individuals against Politically Exposed Persons (PEPs) lists and other government or law enforcement watchlists.

- Adverse Media Screening: Use structured data and NLP to search global news and web sources for negative information (adverse media) related to financial crime, fraud, bankruptcy, or regulatory action.

Step 6: Finalize Risk Assessment and Decisioning

This step consolidates all previous checks into a final, auditable business decision.

- Risk Scoring Model: Implement a dynamic scoring model that aggregates risk factors (e.g., high-risk jurisdiction, complex structure, adverse media hits) into a single, tiered risk score (Low, Medium, High).

- Decision Logic: Based on the final risk score and your defined risk appetite:

- Low/Medium Risk: Automatic Approval (or review by a junior analyst).

- High Risk: Mandatory Enhanced Due Diligence (EDD) and escalation to a senior compliance officer for final approval.

- Prohibitive Risk: Immediate Rejection.

- Documentation: Record the final risk score, the reasoning for the decision, and the date.

Step 7: Establish Ongoing Monitoring and Auditing

KYB is a continuous, not one-time, process to maintain compliance and detect emerging risks.

- Event-Based Monitoring: Configure triggers to run a full re-verification when key events occur (e.g., a change in sanctions lists, a company files a significant ownership change with a registry, a key executive is flagged in adverse media).

- Periodic Reviews: Schedule automatic internal alerts to conduct full, periodic re-reviews of client files based on their risk level.

- Audit Trail Maintenance: Ensure your KYB system generates a time-stamped, unalterable log of every action, check, and decision taken.

By building trust with partners and accelerating the onboarding of legitimate businesses, effective KYB systems protect your organization from costly incidents while ensuring both security and operational excellence.

Common Mistakes to Avoid in Building KYC and KYB Workflows

While building an effective KYC or KYB workflow is critical for compliance, there are several common mistakes that businesses should avoid to ensure the process is efficient and effective:

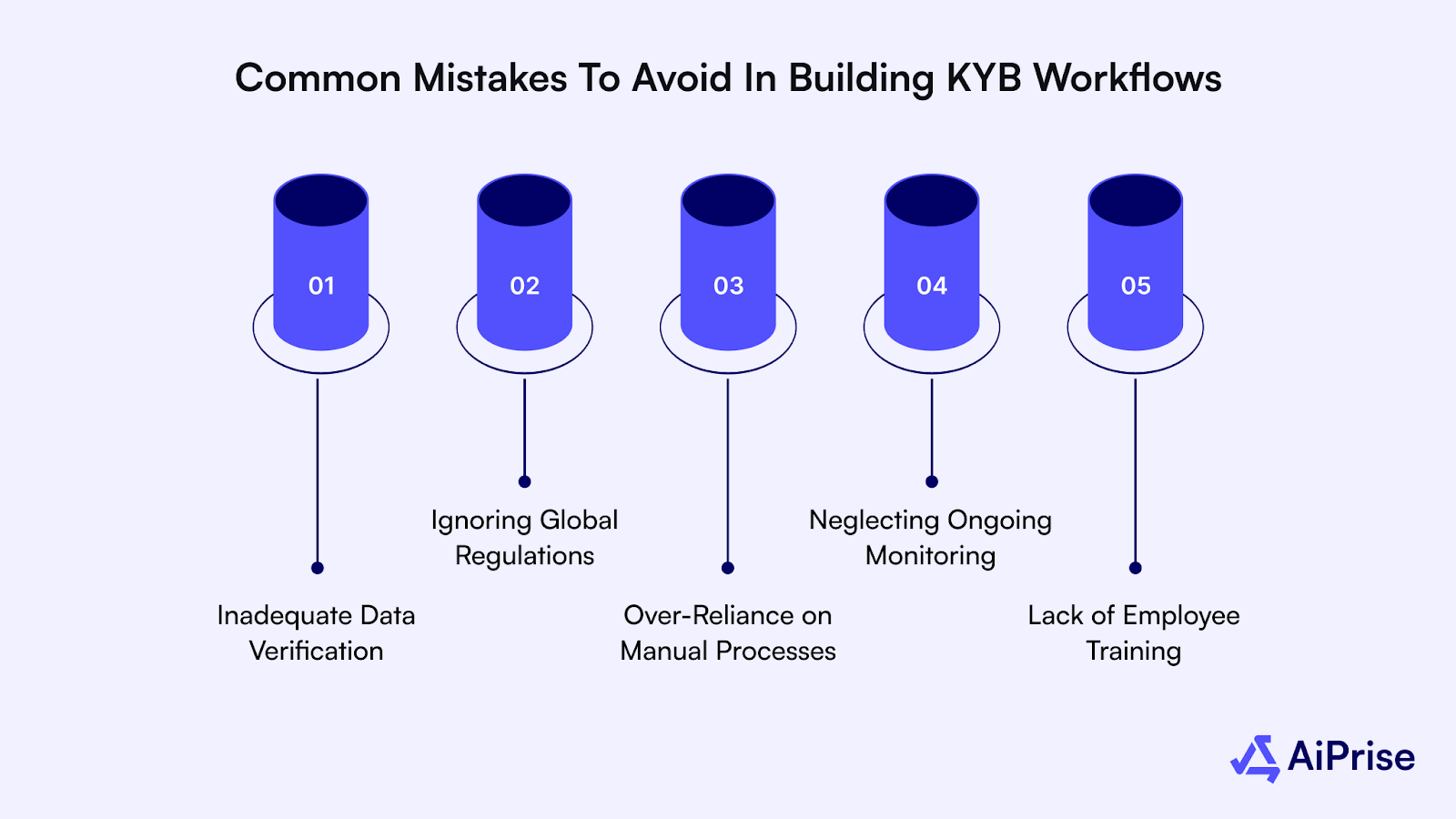

1. False Positives

Sanctions and PEP screening generate a high volume of false matches. For instance, a name that partially matches a watchlist entry triggers an alert, even when there's no actual connection. And this triggers a manual review.

If you’re reviewing hundreds of documents each day, it becomes unsustainable. Consider using an AI-powered verification platform to match records more accurately and configure the thresholds as needed.

2. Data Overload

KYB and KYC workflows pull data from multiple sources, including government registries, document verification providers, sanctions databases, credit bureaus, and adverse media feeds. When these sources aren't integrated into a single workflow, your analysts end up switching between tools and manually reconciling mismatches.

Over time, this just leads to more data overload and results in inconsistent decisions. A centralized workflow aggregates data before it reaches the reviewer.

3. High Compliance Costs

The average KYC review for a commercial or corporate client costs about $2,397 per review. This high cost is driven by manual data collection and periodic refresh cycles. In fact, asset management firms allocate almost 30% of their budgets to KYC workflows alone.

If you’re a mid-market fintech or a growing payment platform, compliance costs can consume a disproportionate share of your operational budget. The financial burden is just one part of the equation. The real cost is the direct impact on time-to-revenue for every new customer you onboard.

4. Ignoring Global Regulations

The biggest problem with KYC compliance is that you need to account for requirements across different jurisdictions. Here are a few examples of compliance regulations:

- FinCEN CDD Rule in the US

- AMLD5 and AMLD6 in the EU

- MAS Notice 626 in Singapore

- FATF recommendations (global)

They all have overlapping but non-identical requirements around customer identification, due diligence thresholds, and monitoring obligations. So you need to build a modular workflow with a configurable design that accounts for risks within each jurisdiction and regulation.

5. Lack of Employee Training

Irrespective of how sophisticated your KYC or KYB workflow is, it comes down to who’s operating it. Your analysts might be able to handle standard cases, but can they handle the edge cases effectively? Let’s say you have a medium risk with an unusual occupation. It doesn’t mean you can’t onboard them, but it takes expertise to categorize that profile correctly.

So train your employees on the workflow itself, as well as the regulatory context behind it.

Best Practices for Building Seamless KYC and KYB Workflows

Building an efficient and scalable KYC and KYB workflow requires careful planning and implementation. To ensure it is both effective and adaptable, consider the following best practices:

Move to Automated Customer and Business Verification Workflows

Automation doesn't mean removing human judgment from the process. It means reserving it for the cases that actually need it.

You can start by automating the repeatable, high-volume steps like:

- Document verification

- Sanctions screening

- Risk scoring

- Watchlist monitoring

If you use AI-powered verification, it can reduce false positives and apply the same checks consistently without relying on simple string matching.

Implement Risk-Based Verification

Every customer doesn’t need the same level of scrutiny. It doesn’t make sense to apply the same checks to a low-risk customer and a PEP from a high-risk jurisdiction. You’ll waste resources and even miss any underlying nuance during the assessment.

Keep Workflows Audit-Ready

Every step in your workflow should generate a time-stamped, unalterable record: who was checked, what was found, what decision was made, and why. Regulators need the whole picture to decide if you’re actually staying compliant with the requirements. If your team is manually logging decisions after the fact, you're creating gaps that are hard to defend during an audit.

Note: Platforms with built-in case management, like AiPrise, generate this trail automatically as checks are completed.

Maintain Transparency in Every Workflow

When a compliance analyst picks up a flagged case, they need full context in one place. Some of that includes screening results, document verification status, prior review history, and any notes from previous analysts.

If that context lives across five different tools, your analyst wastes time reconstructing a picture that should already be assembled. Design your KYC and KYB workflow so that each step passes the output to the next, making it easy to hand things off.

Why Are Businesses Relying on AI-Powered KYB and KYC Workflows?

Business verification used to be straightforward. In the early days of B2B/B2C relationships, companies relied primarily on manual document review and reference checks. This process was time-consuming, inconsistent, and vulnerable to fraudulent documentation.

The introduction of digital business registries in the 1990s and early 2000s marked the first major shift toward more efficient verification. Companies could now cross-reference business claims against official government databases, though this still required significant manual effort.

The EU rolled out stricter Anti-Money Laundering Directives while the FATF tightened its recommendations. The 2008 financial crisis accelerated global regulatory requirements. The United States strengthened its Bank Secrecy Act (BSA) enforcement, while the European Union implemented stricter Anti-Money Laundering Directives. These regulations mandated more thorough due diligence on business clients, particularly regarding beneficial ownership transparency.

Now, regulators demand continuous monitoring and real-time screening, which manual processes were never built to deliver at scale.

At the same time, fraud has become more sophisticated. Bad actors aren't submitting obviously fake IDs anymore. They're using AI-generated documents and synthetic identities designed to pass the kinds of checks that a human reviewer would perform manually. The tools used to commit fraud have advanced faster than the manual processes used to detect it. And with high document volumes, it’s virtually impossible to keep up with the scale.

That’s the problem AI-powered KYC and KYB workflows solve. They handle the repeatable, high-volume checks in real time while reserving human judgment for more complex cases.

How AiPrise Streamlines KYB and KYC Workflows

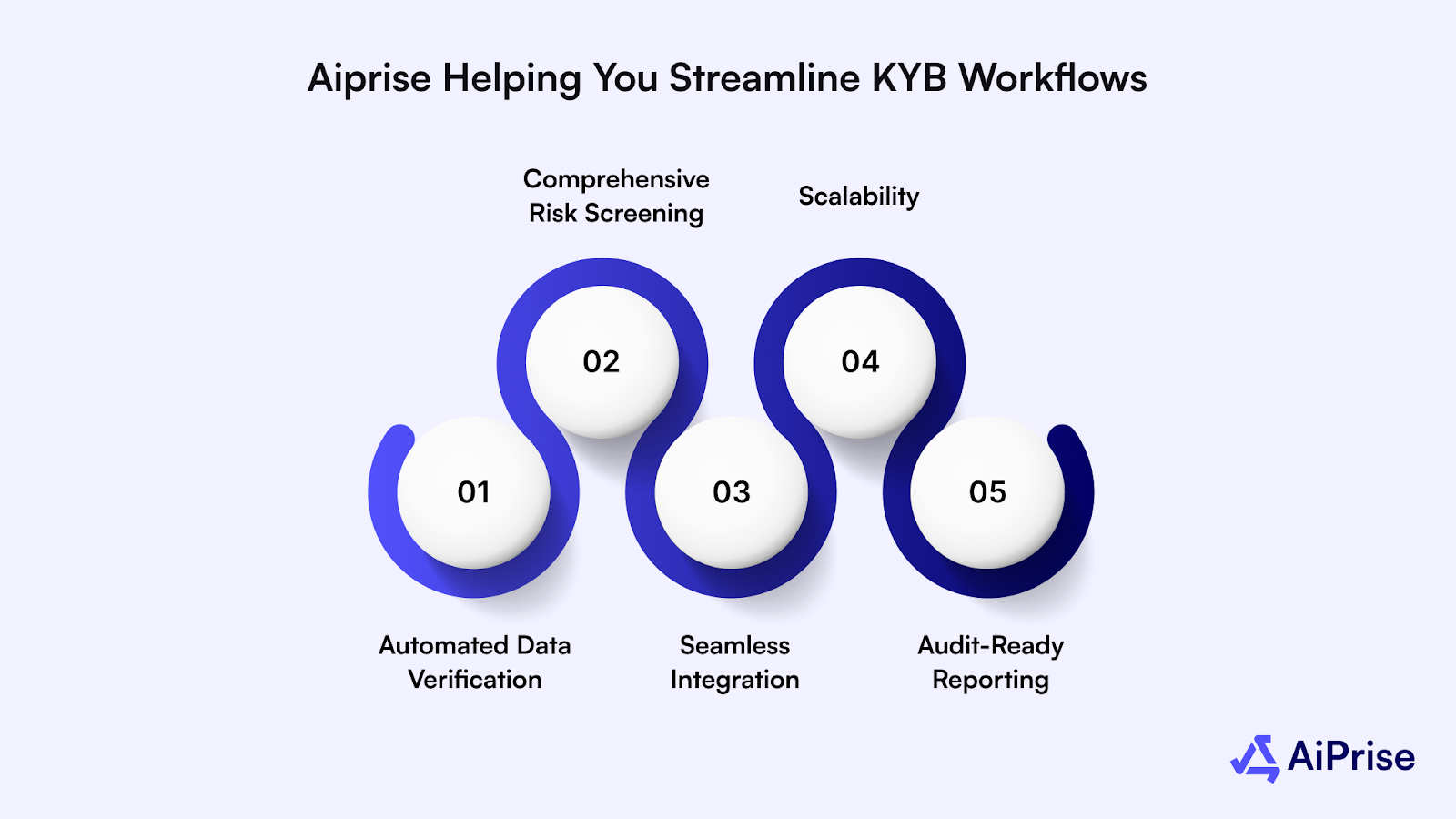

Aiprise is a powerful platform designed to optimize and automate the KYC and KYB process, making it easier for businesses to stay compliant and efficiently verify their business partners. Here’s how Aiprise can enhance your KYC and KYB workflows:

.png)

- Automated Data Verification: Aiprise leverages AI to automatically verify business credentials, reducing the risk of human error and ensuring fast, accurate results.

- Comprehensive Risk Screening: The platform integrates with global risk databases, including sanctions lists, PEPs, and adverse media, to assess businesses' risk profiles in real time.

- Seamless Integration: Aiprise can be easily integrated with your existing systems, ensuring a smooth transition and minimal disruption to your workflow.

- Scalability: Whether you're a startup or a large enterprise, Aiprise scales with your business needs, providing tailored solutions that grow with your company.

- Audit-Ready Reporting: Aiprise automatically generates transparent and auditable reports, helping businesses stay prepared for regulatory audits and internal reviews.

Using Aiprise, businesses can automate their KYB processes, enhance compliance, and improve operational efficiency, all while minimizing the risk of fraud or legal issues.

The Future of KYB and KYC Workflows Is Automated and Continuous

It’s a fact that every customer your compliance team onboards manually results in heavy time and staff costs. But what’s worse is that if you get the verification process wrong, the real cost is measured in millions, if not billions of dollars.

This is where KYC and KYB workflows come in. They turn a patchwork of manual checks into a streamlined, auditable, and scalable process. But the real gains come from automating it so your team can work on complex, high-risk cases with ease.

If you’re interested in automating KYB and KYC workflows, consider using a platform like Aiprise. It brings identity verification, screening, risk scoring, and monitoring into a single platform. As a result, your team can stop managing the workflow and start managing outcomes.

Ready to see how Aiprise can manage your KYC and KYB? Book a demo with us today.

Frequently Asked Questions

What is KYB, and why is it important?

KYB (Know Your Business) is the process of verifying a business's identity and legitimacy. It’s essential for preventing fraud and money laundering and for ensuring compliance with regulations.

What is KYC, and how does it fit in with KYB workflows?

KYC (Know Your Customer) is the process of verifying individual customer identities and assessing their risk level. It fits directly into KYB workflows because every beneficial owner identified during business verification must undergo individual KYC checks.

What are the 5 stages of KYC?

The five stages of KYC are:

- Customer identification, where you collect and verify basic identity data

- Customer due diligence, where you screen against sanctions lists and assess risk

- Enhanced due diligence for high-risk customers

- Risk-based decision-making, where you approve, escalate, or reject based on findings

- Ongoing monitoring to catch changes in risk after onboarding

How does Aiprise help with KYB workflows?

Aiprise automates KYB, ensuring fast, accurate verification and seamless integration with existing systems, reducing errors and improving efficiency.

How can automation improve my KYB process?

Automation speeds up verification, reduces human error, and ensures compliance checks are completed accurately and on time, improving efficiency.

You might want to read these...

AiPrise

KYB Compliance: 2026 Regulations You Should Know About

As organizations expand globally and face tighter regulations, adherence to Know Your Business (KYB) standards has become one of the most critical compliance layers for fintech, online marketplaces, and other companies that need to verify business customers before letting them perform financial transactions.

%20Verification%20in%20the%20US.png)

AiPrise

5 min read

How KYB Verification Works in the US: The Ultimate Guide for Navigating Know Your Business

You can approve a new business customer in minutes. Or you can lose them while your team searches through registries, ownership records, and sanctions lists, trying to piece everything together.

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately