AiPrise

8 min read

March 3, 2026

What Is AML? Verification, Monitoring, and Compliance Needs

Key Takeaways

AML verification becomes frustrating when your team follows the rules, yet onboarding is still slow, reviews are still manual, and regulators still want more evidence. Anti-Money Laundering (AML) verification is more than just a compliance obligation; it’s a critical safeguard that helps you protect your business from financial crime and regulatory scrutiny.

When your team struggles with slow onboarding, gaps in identity verification, and weak transaction monitoring, it often means that AML systems aren’t keeping pace with evolving regulatory expectations under the Bank Secrecy Act (BSA) and related U.S. laws. In the United States in 2025, FinCEN’s financial trend analyzes recorded over 500 suspicious activity reports referencing complex money-laundering networks that amounted to more than $7.1 billion in suspected illicit transactions, underscoring how pervasive money-laundering threats remain when AML checks aren’t robust.

Understanding how AML verification works, from identity and address checks to ongoing monitoring, helps you close operational gaps and reduce the risk of costly fines or enforcement actions. It also gives you a framework for choosing verification systems that streamline compliance, improve risk detection, and strengthen trust with regulators and clients. With the right approach, AML verification becomes a business enabler that helps you balance risk management with growth, rather than a burden.

Key Takeaways

- AML verification confirms customer and business identities, applies risk checks, and supports compliance throughout onboarding and ongoing activity.

- Identity verification establishes trust at entry, while monitoring tracks behavior and transactions to detect emerging money-laundering risk.

- Businesses must meet risk-based verification requirements, apply enhanced due diligence when risk increases, and maintain audit-ready records.

- Weak AML verification leads to regulatory violations, enforcement actions, higher fraud exposure, and increased operational and compliance costs.

What Is AML Verification?

AML verification is the process of confirming identities, validating risk signals, and ensuring customers or businesses are not linked to illicit financial activity. It combines identity checks, sanctions screening, and risk-based assessment to determine whether onboarding or ongoing relationships pose regulatory exposure. Effective AML verification helps compliance teams detect inconsistencies early, reduce manual reviews, and demonstrate defensible compliance during audits or investigations.

AML Identity Verification vs AML Monitoring

AML identity verification and AML monitoring serve distinct but connected purposes within a broader compliance framework, each addressing different stages of risk management.

Here’s how both functions differ in scope, timing, and operational responsibility.

AML Identity Verification

- Confirms an individual’s or business’s identity during onboarding using AML identity checks and AML ID verification methods

- Validates government-issued IDs, business documents, and address information to meet AML verification requirements

- Establishes an initial risk profile before allowing account access or transactional activity

- Reduces exposure to impersonation, synthetic identities, and onboarding-stage fraud

AML Monitoring

- Continuously tracks customer behavior and transactions after onboarding to detect suspicious patterns

- Flags unusual activity that deviates from expected risk profiles or transactional behavior

- Supports ongoing compliance obligations under AML regulations and audit expectations

- Helps compliance teams respond quickly to emerging risks without re-verifying identity data repeatedly

While AML identity verification and AML monitoring serve different compliance purposes, the distinction often becomes unclear in day-to-day operations.

The comparison table below highlights where responsibilities, costs, and risks diverge, helping you quickly identify which function requires process or technology improvement.

Also read: Identity Verification Protocols in 2026

Seeing the differences side by side raises an important question: What exactly happens during identity checks, and which documents regulators expect you to verify?

AML Identity Checks and AML ID Verification Explained

AML identity checks and AML ID verification focus on confirming whether customers and businesses are genuine before financial relationships are established.

The points below clarify what each check involves, which IDs are required, and where compliance teams commonly face friction.

- AML identity checks validate personal or business information against trusted and authoritative data sources

- AML ID verification confirms the authenticity of government-issued identification documents submitted during onboarding

- Accepted IDs typically include passports, driver’s licenses, national identity cards, and business incorporation documents

- Proof of address documents, such as utility bills or bank statements, support AML address verification requirements

- These checks help prevent impersonation, synthetic identities, and misuse of stolen credentials

- Gaps or mismatches in ID data often lead to manual reviews, onboarding delays, and increased compliance risk

Identity checks alone don’t satisfy regulators, which is why it’s important to understand the broader verification requirements businesses are held accountable for.

AML Verification Requirements Businesses Must Meet

AML verification requirements define what regulators expect businesses to demonstrate when identifying customers, assessing risk, and maintaining compliant records.

The following points outline compliance expectations without repeating earlier verification or identity-check details.

- Businesses must apply a documented, risk-based approach aligned with their customer profiles and exposure levels

- Customer identity information must be collected, validated, and retained in accordance with regulatory timelines

- Higher-risk customers and entities require enhanced due diligence and deeper verification controls

- Ongoing reviews must ensure customer information remains accurate and up to date

- Suspicious activity must be identified, investigated, and reported within mandated timeframes

- Verification processes must be auditable, consistent, and defensible during regulatory examinations

Also read: Comprehensive Guide to AML Compliance in FinTech

Meeting these requirements consistently becomes difficult without the right systems in place, especially as customer volume and regulatory scrutiny increase.

What Systems Support AML Checks?

AML checks rely on interconnected systems that automate verification, reduce manual effort, and help teams respond to risk efficiently.

The bullets below highlight the core systems businesses use to support AML checks at scale and where technology closes common compliance gaps.

- Identity verification systems that validate customer and business data against authoritative and government-backed sources

- Sanctions and watchlist screening tools that continuously scan customers against global and domestic lists

- Transaction monitoring platforms that analyze behavioral patterns and flag suspicious activity in real time

- Case management systems that centralize alerts, investigations, and audit-ready documentation

- Risk scoring engines that dynamically adjust customer risk profiles based on activity and exposure

- AI-driven platforms like AiPrise, which automate AML verification using machine learning, multi-source data checks, and continuous monitoring to reduce false positives and manual reviews

Even with automated systems, certain customers and activities demand closer attention, which is where enhanced due diligence comes into play.

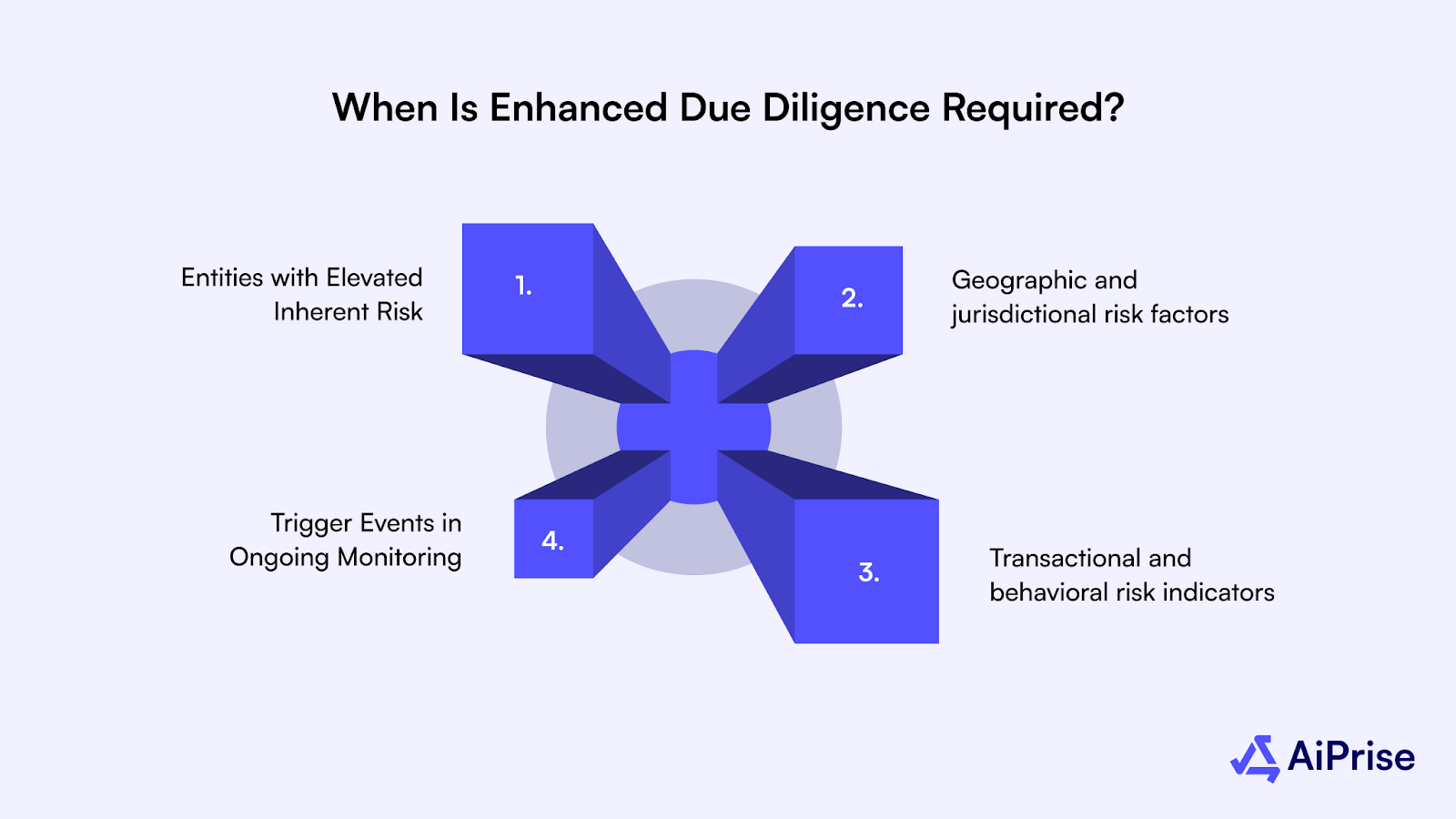

When Is Enhanced Due Diligence Required?

Enhanced Due Diligence is required when standard AML verification measures cannot adequately assess heightened financial crime risk.

The nested bullets below explain when deeper scrutiny is expected and why additional controls become necessary.

- Customers or entities presenting elevated inherent risk

- Politically exposed persons and their close associates require deeper verification due to potential exposure to corruption or abuse of power

- Businesses with complex ownership structures often need additional checks to identify beneficial owners accurately

- Geographic and jurisdictional risk factors

- Customers linked to high-risk or sanctioned jurisdictions require enhanced screening to address regulatory and reputational risk

- Transactions involving countries with weak AML frameworks increase exposure to illicit fund flows

- Transactional and behavioral risk indicators

- Unusual transaction volumes or patterns that conflict with declared business activities warrant closer examination

- Rapid movement of funds across multiple accounts or jurisdictions signals potential layering activity

- Trigger events identified during ongoing monitoring

- Sudden changes in customer behavior or risk profile require reassessment beyond standard controls

- Adverse media findings, sanctions updates, or regulatory alerts necessitate immediate enhanced review

Platforms like AiPrise support Enhanced Due Diligence by automating deeper risk assessments, continuous monitoring, and multi-source verification for high-risk customers.

Also read: Effective AML Compliance for Small Businesses

Failing to apply enhanced checks when risk escalates often leads to consequences that extend beyond compliance findings and into business continuity.

Consequences of Weak AML Verification

Weak AML verification creates direct regulatory, financial, and operational exposure under established U.S. AML laws and enforcement standards.

The bullets below reflect consequences tied to actual regulatory expectations, not generic risk statements.

- Violations of the Bank Secrecy Act (BSA) when customer identities are inadequately verified, or risk profiles are poorly documented

- Enforcement actions from regulators such as FinCEN, OCC, FDIC, or the Federal Reserve due to ineffective AML controls

- Civil monetary penalties resulting from failure to apply risk-based AML verification and ongoing monitoring

- Mandatory remediation programs imposed by regulators, increasing compliance workload and operational disruption

- Heightened audit scrutiny when verification records cannot demonstrate consistent and defensible AML practices

- Loss of banking relationships or partner trust due to perceived compliance weaknesses

- Increased fraud exposure when weak identity verification allows high-risk actors to access financial systems

Avoiding these outcomes depends on how effectively your AML framework is executed, which is where the right verification platform makes a measurable difference.

How AiPrise Helps Strengthen AML Verification?

AiPrise strengthens AML verification by bringing identity verification, risk assessment, and ongoing monitoring into a single, scalable platform built for real regulatory pressure.

It enables you to reduce manual effort, apply risk-based controls consistently, and maintain defensible compliance as your customer base and geographic reach expand.

Key Capabilities That Support Strong AML Verification:

- Verifies individuals and businesses using a risk-based approach that aligns onboarding checks with customer profile, geography, and exposure level

- Connects to 100+ global data sources to validate identities, businesses, and beneficial owners with higher accuracy and lower dependency on manual reviews

- Applies dynamic risk scoring using customizable rules, allowing you to adapt AML verification requirements as risk changes

- Supports Enhanced Due Diligence by automating deeper checks, document analysis, and AI-generated EDD reports for high-risk entities

- Enables continuous monitoring to detect behavioral changes, adverse signals, or regulatory triggers without re-running full verification cycles

- Centralizes case management and audit trails, making AML verification decisions easier to review, justify, and report during examinations

Bringing these elements together shows how AML verification can function as a controlled, defensible process rather than a recurring operational headache.

Wrapping Up

Strong AML verification is no longer just about meeting regulatory expectations; it’s about protecting your business from hidden risk, operational drag, and avoidable compliance failures.

By understanding how identity verification, monitoring, and risk-based controls work together, you’re better equipped to build AML programs that scale without slowing growth.

With AiPrise, you can strengthen AML verification through automation, smarter risk decisions, and audit-ready compliance built for real-world pressure.

Book A Demo to see how a unified AML verification platform can reduce risk, speed onboarding, and simplify compliance without adding operational complexity.

Frequently Asked Questions

1. What is AML verification?

AML verification is the process of confirming identities, assessing risk, and ensuring customers or businesses are not linked to money laundering or financial crime.

2. Is AML verification part of KYC?

AML verification works alongside KYC by adding risk assessment, sanctions screening, and monitoring beyond basic identity confirmation.

3. What documents are required for AML verification?

Common documents include government-issued photo IDs, business registration records, proof of address, and beneficial ownership information.

4. How often should AML checks be performed?

AML checks are required at onboarding and should continue on an ongoing basis through monitoring and periodic reviews.

5. Who needs to comply with AML verification requirements?

Banks, fintechs, payment providers, crypto platforms, lenders, and other regulated entities must comply with AML verification obligations.

You might want to read these...

.png)

.png)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately