AiPrise

8 min read

March 4, 2026

AI Risk Scoring System: A Practical Guide for AML

Key Takeaways

A routine transaction alert at 2 a.m. can quickly escalate into a full-scale compliance crisis.

Mounting false positives, limited analyst bandwidth, and evolving typologies leave your AML team stretched thin.

An AI Risk Scoring System changes that equation by detecting patterns that traditional rules simply fail to capture. In 2025, FinCEN reported that suspicious activity filings identified nearly $7.1 billion in suspected laundering transactions nationwide.

Such numbers reflect growing regulatory pressure, higher investigation costs, and increased expectations for real-time risk visibility. Understanding AI-driven risk scoring equips your institution to reduce false positives, strengthen compliance, and allocate resources strategically.

Key Takeaways

- An AI Risk Scoring System assigns dynamic risk scores using behavioral patterns, sanctions data, geographic exposure, and transaction history.

- Unlike static rule engines, AI models detect hidden structuring patterns, reduce false positives, and prioritize high-risk alerts.

- Effective AML scoring depends on quality data ingestion, machine learning validation, explainable model logic, and continuous feedback loops.

- Strong governance, threshold calibration, and ongoing monitoring ensure risk models remain accurate, defensible, and aligned with evolving fraud typologies.

What Is AML Risk Scoring?

AML risk scoring is a structured compliance methodology that assigns quantified risk levels to customers, transactions, and counterparties. An AI Risk Scoring System strengthens AML programs by evaluating transaction behavior, geographic exposure, sanctions data, and historical suspicious activity indicators. Under U.S. regulations enforced by FinCEN and the Bank Secrecy Act, risk scoring enables financial institutions to prioritize high-risk alerts and maintain defensible compliance controls.

How Does AI Improve Risk Scoring Over Legacy Approaches?

AI improves AML risk scoring by shifting from static, manually weighted rules to data-driven models that evaluate behavioral, transactional, and geographic risk signals simultaneously. Here are the specific ways AI-driven systems outperform legacy AML risk frameworks:

- Identifies layered structuring patterns across multiple accounts, even when individual transactions remain below reporting thresholds.

- Applies behavioral baselining to detect deviations in transaction velocity, counterparties, and cross-border fund flows.

- Dynamically adjusts customer risk ratings when exposure to high-risk jurisdictions or sanctioned entities changes.

- Correlates internal transaction data with external risk indicators, including sanctions lists and adverse media signals.

- Reduces alert fatigue by assigning probability-based risk scores instead of triggering binary rule breaches.

- Enhances model accuracy through supervised learning using previously filed Suspicious Activity Report outcomes.

- Supports regulator-ready explainability by documenting feature weighting, model logic, and decision rationales.

- Improves case prioritization by ranking alerts based on composite risk exposure rather than transaction size alone.

Also read: AI Powered Enhanced Due Diligence for Risk Management

Understanding the improvements is only part of the picture; the underlying architecture determines whether those improvements hold up in real-world environments.

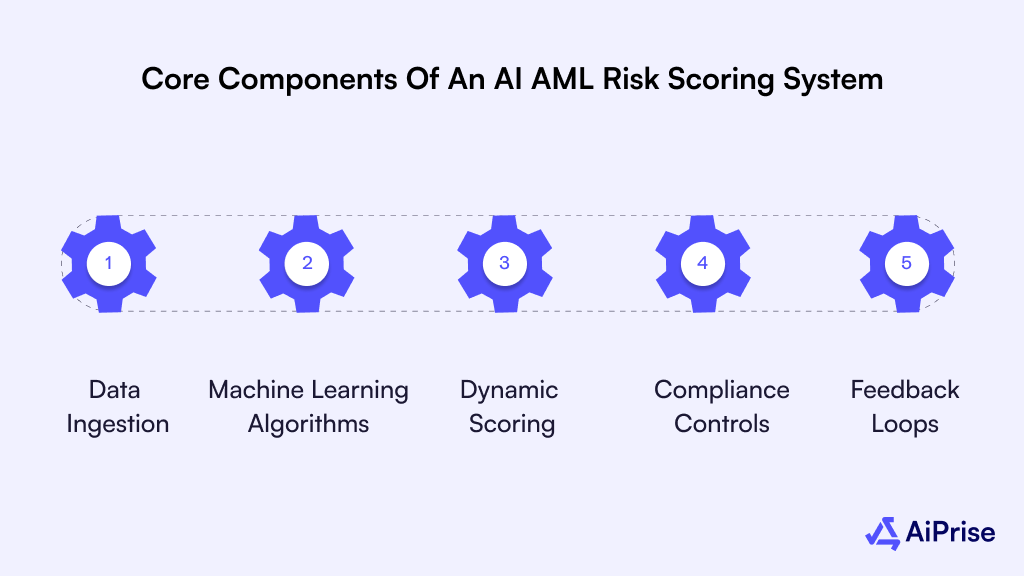

Core Components of an AI AML Risk Scoring System

An AI AML risk scoring system operates through interconnected technical layers that transform raw financial data into actionable compliance intelligence. The following elements define a robust and regulator-ready AI risk scoring architecture.

1. Data Ingestion & Feature Engineering

Data ingestion consolidates structured and unstructured inputs, including transaction histories, customer identification records, device fingerprints, and geographic indicators. Feature engineering then transforms this raw data into measurable risk variables such as transaction velocity, cross-border exposure frequency, and counterparty risk concentration.

Within U.S. AML programs, high-quality feature construction directly determines alert precision and investigative efficiency.

2. Model Training & Machine Learning Algorithms

Machine learning models are trained using historical transaction data, Suspicious Activity Report outcomes, and confirmed fraud cases to identify high-risk behavioral patterns. Supervised learning detects known typologies, while unsupervised models uncover anomalies that traditional rule engines miss.

Proper model validation ensures statistical reliability and regulatory defensibility under Bank Secrecy Act compliance standards.

3. Dynamic Scoring & Prioritization

Dynamic scoring assigns weighted risk values in real time based on evolving behavioral and geographic indicators. Threshold calibration determines whether an alert requires escalation, enhanced due diligence, or continued monitoring.

This structured prioritization reduces investigative backlogs and ensures high-risk cases receive immediate analyst attention.

4. Explainability & Compliance Controls

Explainability frameworks document how specific variables influence individual risk scores and escalation outcomes. Transparent scoring logic enables compliance teams to justify decisions during internal audits and regulatory examinations.

Strong governance controls also include model documentation, audit trails, and performance monitoring aligned with FinCEN expectations.

5. Feedback Loops & Continuous Model Refinement

Feedback mechanisms incorporate investigator decisions, SAR filings, and false positive outcomes into ongoing model retraining cycles. Continuous refinement improves detection accuracy as criminal typologies and geographic risk exposures evolve.

Platforms such as AiPrise integrate automated monitoring and adaptive model updates to maintain consistent risk scoring performance across onboarding and transaction workflows.

Knowing the building blocks is important, but effectiveness depends on how those components operate at scale under daily transaction pressure.

Technical Elements That Make AI Risk Scoring Effective

An AI Risk Scoring System becomes effective when its infrastructure supports speed, contextual intelligence, and scalable investigation workflows. The following technical elements directly determine whether your AI-driven AML framework delivers measurable risk reduction.

- Real-Time Data Processing Architecture

- Processes transactions instantly during onboarding or live payment authorization events.

- Flags suspicious fund transfers before settlement, preventing irreversible financial exposure.

- For example, detects rapid micro-deposits across linked accounts within seconds.

- Behavioral Baselining and Anomaly Detection

- Establishes normal transaction patterns based on historical customer activity profiles.

- Identifies deviations such as sudden high-value cross-border transfers from low-risk accounts.

- For instance, flags a dormant account initiating large crypto withdrawals overnight.

- Multi-Source Risk Correlation Engines

- Combines internal transaction data with sanctions lists and adverse media databases.

- Strengthens entity risk visibility across counterparties, geographies, and ownership structures.

- For example, link a business account to a newly sanctioned beneficial owner.

- Adaptive Machine Learning Infrastructure

- Retrains models using confirmed suspicious activity and cleared false positive outcomes.

- Adjusts feature weighting when fraud typologies shift across industries.

- For example, recalibrates risk thresholds after detecting mule account networks.

- Explainable AI and Governance Controls

- Documents how each variable contributes to the generated risk scores.

- Provides defensible reasoning during internal audits and regulatory examinations.

- For instance, shows transaction velocity carried a higher risk weighting than geography.

- Integrated Case Prioritization Systems

- Ranks alerts using composite probability scores instead of chronological queues.

- Directs analysts toward high-impact investigations first, improving productivity.

- For example, escalates structured layering activity above isolated threshold breaches.

Also read: Defining Marketplace Risk And How To Prevent It

Even the most advanced technical setup can fail without disciplined execution, which is why implementation strategy deserves equal attention.

Best Practices in Implementing AI Risk Scoring for AML

Successful AI risk scoring implementation requires disciplined governance, quality data inputs, and measurable performance benchmarks from the beginning. The following best practices help ensure your AI-driven AML framework delivers consistent, defensible results:

- Define clear risk objectives aligned with fraud typologies, transaction exposure, and institutional risk appetite.

- Conduct structured data audits to eliminate incomplete customer records and inconsistent transaction tagging.

- Establish measurable performance indicators, including precision rate, recall rate, and false positive reduction targets.

- Validate models using historical Suspicious Activity Report outcomes before full production deployment.

- Calibrate scoring thresholds to balance regulatory scrutiny with customer onboarding experience efficiency.

- Implement independent model validation and stress testing under simulated high-risk transaction scenarios.

- Maintain detailed documentation covering feature selection, weighting logic, and model governance procedures.

- Design structured feedback loops incorporating investigator decisions and confirmed case resolutions.

- Monitor model drift continuously to detect declining accuracy caused by emerging fraud typologies.

- Train compliance analysts to interpret probability-based risk scores rather than relying on binary alerts.

As your AI risk scoring framework matures, platforms like AiPrise support automated model governance, adaptive monitoring, and integrated AML risk workflows designed to strengthen detection accuracy without increasing operational burden.

Common Challenges and How to Mitigate Them

AI risk scoring implementation often exposes operational, data, and governance gaps that slow adoption and reduce effectiveness. Addressing these challenges early prevents model instability, regulatory friction, and unnecessary investigation costs. The following obstacles frequently impact AML teams, along with practical mitigation strategies:

- Poor data quality reduces model accuracy, so conduct structured data cleansing before deployment.

- Inconsistent customer risk categorization creates scoring bias, so standardize the risk taxonomy across departments.

- High false positive volumes overwhelm analysts, so recalibrate thresholds using historical case outcomes.

- Limited explainability creates audit concerns, so deploy transparent feature attribution and model documentation controls.

- Model drift weakens detection over time, so schedule periodic retraining using updated transaction datasets.

- Overfitting during training reduces real-world performance, so validate models on independent testing datasets.

- Resistance from compliance teams slows adoption, so provide structured training on probability-based scoring interpretation.

- Integration gaps with core banking systems disrupt workflows, so ensure API compatibility before production rollout.

- Evolving fraud typologies reduce detection effectiveness, so continuously monitor emerging risk indicators across industries.

- Regulatory scrutiny increases governance pressure, so maintain detailed audit trails and version-controlled model updates.

Also read: Understanding Risk Profiles in Know Your Customer (KYC) Processes

Implementation rarely happens without friction, and recognizing common obstacles early can prevent expensive setbacks later.

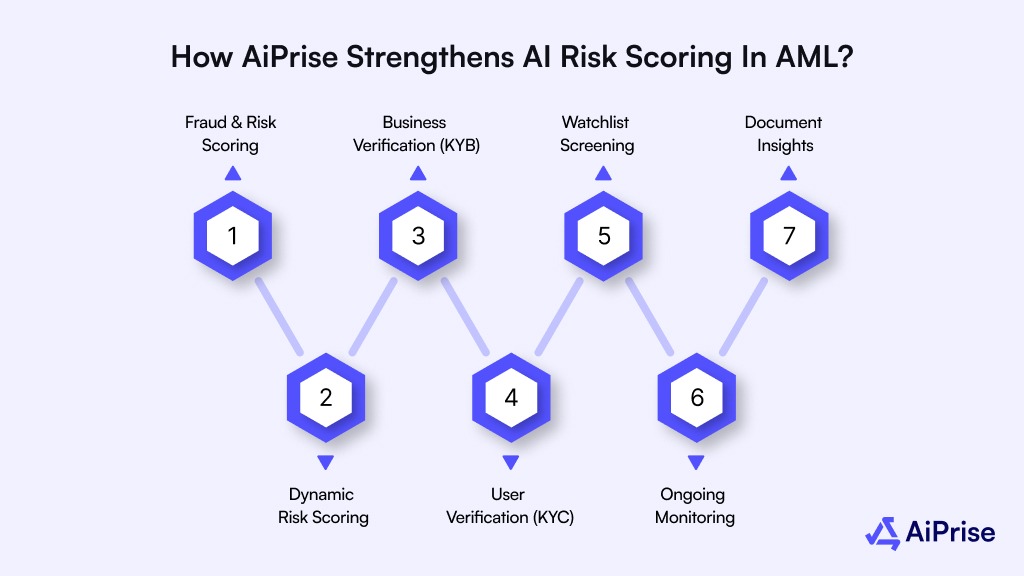

How AiPrise Strengthens AI Risk Scoring in AML?

An AI Risk Scoring System performs effectively when verified identity data, weighted risk logic, and automated review workflows operate together. AiPrise strengthens this process by feeding validated data into scoring models and automating high-risk escalation decisions.

- Fraud & Risk Scoring provides a customizable rule engine that assigns weighted risk scores based on defined fraud indicators and tolerance levels.

- Dynamic Risk Scoring delivers real-time risk assessments and allows backtesting to optimize scoring thresholds.

- Business Verification (KYB) improves enterprise risk scoring by validating registry data and verifying UBO structures before assigning business risk ratings.

- User Verification (KYC) ensures scoring models rely on verified identities through document validation and liveness checks.

- Watchlist Screening directly influences risk weighting by screening entities against sanctions and PEP databases.

- Ongoing Monitoring enables continuous reassessment of risk profiles after onboarding.

- Document Insights extracts structured data, performs template matching, and detects document tampering to improve scoring accuracy.

This focused integration allows your AI Risk Scoring System to operate with validated inputs, dynamic recalibration, and faster investigation turnaround without increasing analyst workload.

Wrapping Up

AI Risk Scoring Systems are no longer experimental tools; they are becoming foundational to modern AML effectiveness and operational resilience. When risk models rely on verified data, adaptive scoring logic, and automated review workflows, your compliance program moves from reactive alert handling to proactive risk intelligence.

AiPrise strengthens this shift by combining dynamic risk scoring, verified identity data, and AI-powered Compliance Co-Pilot capabilities into one unified AML infrastructure.

If reducing false positives, accelerating investigations, and strengthening AML controls are priorities, it may be time to Book A Demo and see how AI-driven risk scoring can transform your compliance operations.

FAQs

1. What is an AI risk scoring system in AML?

An AI risk scoring system in AML uses machine learning models and weighted rules to assign dynamic risk levels to customers, businesses, and transactions based on behavioral, identity, and sanctions-related data signals.

2. How does AI reduce false positives in AML monitoring?

AI reduces false positives by analyzing contextual behavior patterns and historical outcomes instead of triggering alerts solely based on static transaction thresholds.

3. What data is used in AML risk scoring models?

AML risk scoring models typically use identity verification data, transaction history, geographic exposure, sanctions screening results, device intelligence, and behavioral activity indicators.

4. Is AI-based AML risk scoring compliant with regulations?

AI-based AML risk scoring can meet regulatory expectations when supported by explainability frameworks, audit trails, documented governance controls, and validated model performance testing.

5. What is the difference between rule-based and AI-based AML risk scoring?

Rule-based AML scoring relies on fixed thresholds and predefined triggers, while AI-based scoring adapts to evolving risk patterns using historical data and predictive modeling techniques.

You might want to read these...

.png)

.png)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately