AiPrise

17 mins read

August 6, 2025

7 Biggest Fraud Cases and Scams in History

Key Takeaways

Fraud has always been a part of human history, but it has evolved dramatically over the years. From simple street hustles in ancient civilizations to highly sophisticated cyber schemes today, the scale and scope of scams have only grown.

Some of the most notorious frauds have caused billions of dollars in losses and left a trail of destruction for businesses, governments, and individuals alike.

As we continue to advance into the digital age, the need for robust fraud prevention systems becomes increasingly critical. What was once a con artist’s quick trick is now a multi-billion-dollar scam that can wreak havoc across industries, especially in sectors like finance, crypto, and e-commerce.

In this blog, we'll explain the seven most significant fraud cases and scams in history. We’ll also offer insights into how these events shook industries and societies, and what businesses can learn from them to safeguard against future threats.

Key Takeaways

- From ancient coin forgery to modern-day Ponzi schemes, scams have evolved, but the core principle of exploiting trust for personal gain remains unchanged.

- Major fraud cases like Enron, Bernie Madoff, and FTX have caused billions in losses, highlighting the need for businesses to adopt stronger fraud prevention systems and maintain transparency.

- Scandals like Enron and Theranos demonstrate the importance of ethical leadership, transparent financial reporting, and strict oversight in preventing fraudulent activities.

- With the rise of cryptocurrency and online transactions, scams like the Mt. Gox hack and online fraud have exposed vulnerabilities in digital platforms. Businesses must invest in cybersecurity and compliance measures to safeguard against digital threats.

- Scandals have driven regulatory reforms, such as the Sarbanes-Oxley Act, highlighting the need for robust corporate governance and accountability in the fight against fraud.

- Businesses must continuously assess risks, implement proactive fraud detection technologies, and educate employees to safeguard against the growing complexity of modern fraud tactics.

Historical Context: The Evolution of Fraud

Fraud has been part of human history since the beginning of commerce and trade. In ancient times, simple acts like coin forgery were common. Rulers and merchants would shave precious metals off coins, passing them off as full-value currency to pocket the difference. This was just the beginning of a long history of deceit.

In the 15th century, we saw a more elaborate scam with Perkin Warbeck, who falsely claimed to be Richard, Duke of York. Warbeck’s deception shook the English court and led many to support his fraudulent claim to the throne.

Fast forward to the 18th century, and the “South Sea Bubble” duped investors in Britain with promises of wealth through a speculative scheme. At its peak, even Isaac Newton, the famous scientist, was caught in the trap and lost as much as £40 million of today’s money in the process.

By the 20th century, fraud had become even more sophisticated. The Ponzi scheme, named after Charles Ponzi in the 1920s, became a symbol of financial deception. In more recent history, corporate frauds like Enron’s accounting scandal and Bernie Madoff’s multi-billion-dollar Ponzi scheme showed how massive the stakes could be in the modern world.

Today, we see a new generation of fraud, often involving digital tools and cryptocurrency scams, with cybercriminals using advanced technology to perpetrate fraud at scale. The tactics may have shifted from physical manipulation to virtual schemes, but the core principle remains the same—exploiting trust for personal gain.

The evolution of fraud has made one thing clear: as systems grow more complex, so do the ways fraudsters exploit them. Understanding the history of fraud is vital for businesses today as they confront more sophisticated threats.

7 Biggest Fraud Cases and Scams in History

Fraud and scams have grown increasingly sophisticated over time. From street-level hustles to complex cybercrime schemes, scammers have always adapted to the tools of the era.

Let's explore the seven most infamous fraud cases in history—each one leaving a lasting impact on industries, economies, and public trust.

1. The Enron Scandal: A Corporate Collapse

Enron, once a leading energy company, became infamous for one of the largest corporate frauds in history. Founded in 1985, the company grew rapidly by trading natural gas derivatives and expanding into broadband. However, behind this success, Enron used deceptive accounting practices like "mark-to-market" accounting, inflating profits, and hiding debts through special purpose entities (SPEs), with the complicity of its auditors, Arthur Andersen.

In 2001, the truth came out when Enron’s financial discrepancies were exposed, causing its stock price to crash from $90 to under $1 per share. The company filed for bankruptcy in December, wiping out billions in shareholder value, and leaving thousands of employees without jobs or retirement savings.

The scandal led to criminal charges for Enron’s executives, the dissolution of Arthur Andersen, and a wave of regulatory reforms, including the Sarbanes-Oxley Act of 2002, aimed at preventing such corporate frauds in the future.

Key Business Takeaway:

The Enron scandal highlights the dangers of corporate complacency, where executives exploit weak oversight and regulatory loopholes. Companies must ensure transparency, use accurate financial reporting practices, and maintain strong governance frameworks. Regular audits, external oversight, and a commitment to integrity are essential to avoid similar risks.

2. Bernie Madoff Ponzi Scheme: A Deceptive Scheme That Shattered Trust

Arguably the largest Ponzi scheme in history, Bernie Madoff’s fraud tricked thousands of investors out of $50 billion. Madoff, a well-respected financier, promised consistent high returns, even during times of market volatility, which attracted numerous wealthy clients. Instead of investing the funds as promised, Madoff used new investors' money to pay returns to earlier investors.

The scandal, which unraveled in 2008, exposed the severe lack of due diligence and oversight by both investors and regulatory bodies. Madoff's firm was able to operate for decades due to the trust he had built, and the SEC failed to investigate his operations despite multiple red flags.

The impact of Madoff’s scheme was profound—thousands of people lost their life savings, including charities, individuals, and institutional investors. The scandal also led to regulatory changes, with an increased focus on protecting retail investors and tightening oversight on financial institutions.

Key Business Takeaway:

Madoff’s scheme underscores the importance of vigilant due diligence and trust in financial professionals. Businesses must regularly vet their financial partners, implement comprehensive risk management systems, and be proactive in reporting suspicious activities to prevent fraud.

3. Volkswagen Emissions Scandal: Deception on a Global Scale

In 2015, Volkswagen was caught cheating on emissions tests, a scandal that affected over 11 million cars worldwide. The company had installed software in their diesel vehicles that detected when the car was being tested and altered emissions to meet regulatory standards. Outside of tests, the vehicles emitted far higher levels of pollutants.

Volkswagen’s actions were not only a violation of environmental laws but also a deliberate attempt to deceive regulators and customers. The company faced hefty fines, with some estimates putting the total cost of the scandal at over $30 billion, including vehicle buybacks, regulatory fines, and lawsuits.

The impact was felt across the automotive industry, as it damaged consumer trust in Volkswagen and other manufacturers. It also prompted stricter emissions regulations globally and renewed efforts to hold companies accountable for deceptive environmental practices.

Key Business Takeaway:

The Volkswagen scandal serves as a warning about the dangers of ethical lapses and misleading consumers. Companies must invest in building a culture of transparency, ensuring that their product claims align with actual performance and that they adhere to regulatory standards.

4. Theranos: Silicon Valley's Biggest Fraud

Elizabeth Holmes, the founder of Theranos, promised to revolutionize the blood testing industry with a device that could conduct hundreds of medical tests using just a drop of blood. The company raised over $700 million, achieving a valuation of $10 billion at its peak. However, the technology never worked. Holmes and her team misled investors, patients, and doctors about the efficacy of their product.

The impact of the fraud was widespread—investors lost millions, and patients were subjected to false test results, which could have led to misdiagnoses and unnecessary treatments. The case raised serious questions about Silicon Valley's culture of promoting unverified, high-risk ideas without proper oversight.

Key Business Takeaway:

Theranos’ story highlights the importance of honesty in innovation. Businesses must prioritize transparency, verify the functionality of their products through independent testing, and avoid overstating capabilities to attract investments. Ethics and accountability are key in building a lasting reputation.

5. Mt. Gox: The Cryptocurrency Exchange Heist

In 2014, Mt. Gox, one of the largest Bitcoin exchanges in the world, filed for bankruptcy after revealing that 850,000 Bitcoins—worth over $450 million at the time—had been stolen. The company initially blamed a hacking attack, but later admitted that poor internal controls and mismanagement played a key role in the massive theft.

The impact of the hack was devastating to the emerging cryptocurrency industry. Mt. Gox handled 70% of global Bitcoin transactions at its peak, and its collapse severely undermined trust in cryptocurrency exchanges. While some of the stolen Bitcoins were later recovered, many users lost their investments, leading to legal actions against the company’s executives.

Key Business Takeaway:

The Mt. Gox scandal emphasizes the need for robust cybersecurity in digital financial platforms. Businesses in fintech and crypto must prioritize secure operations, implement strict access controls, and regularly audit their systems to protect customer assets.

6. The South Sea Bubble: A Historical Investment Fraud

In the early 1700s, the South Sea Company, granted a monopoly on trade with South America, promised enormous profits to investors. The stock price surged dramatically from £128.5 to £1,000 per share in 1720, fueled by speculation. However, the company’s business was largely fictional, and its profits were based on deceit. When the bubble burst, the stock value plummeted, causing financial ruin for many investors, including members of the British elite.

The crash led to widespread economic panic and the creation of new laws to regulate stock trading, setting the stage for modern market manipulation laws.

Key Business Takeaway: The South Sea Bubble serves as a stark reminder of the dangers of market manipulation and speculation. Businesses must ensure transparency, avoid unrealistic promises, and uphold the integrity of their financial dealings.

7. FTX Collapse: A Crypto Giant's Fall

FTX, a once-thriving cryptocurrency exchange, collapsed in spectacular fashion in 2022, shocking the digital asset industry. Founded by Sam Bankman-Fried in 2019, FTX rapidly grew to a $32 billion valuation, drawing in major investors and clients.

However, behind the scenes, FTX’s financial foundation was fragile. The company had substantial exposure to internally created tokens like FTT and Serum, which were largely unregulated and lacked real-world value. These tokens played a significant role in the company's asset base, contributing to an unsustainable imbalance between assets and liabilities.

On November 2, 2022, news broke that Alameda Research, a trading firm closely linked to FTX, held a massive $14.6 billion in FTT tokens. The revelation sparked panic, as FTT was primarily used as a self-created, permissionless token, giving it little to no intrinsic value. The value of FTT fell dramatically in the days following Binance's announcement.

The collapse accelerated as FTX’s customers began a massive withdrawal, seeking to pull their funds out. With FTX unable to cover these withdrawals, the exchange filed for bankruptcy on November 11, 2022, leaving customers, investors, and the broader cryptocurrency market reeling.

Key Business Takeaway: The FTX crash underscores the importance of proper risk management, transparency, and governance in any industry, especially one as volatile as cryptocurrency. As digital assets continue to grow, so must the regulatory framework to prevent similar frauds.

As fraud continues to evolve, businesses must stay vigilant and implement strategies to protect themselves against emerging threats. Let’s explore how companies can safeguard their operations with modern fraud prevention methods.

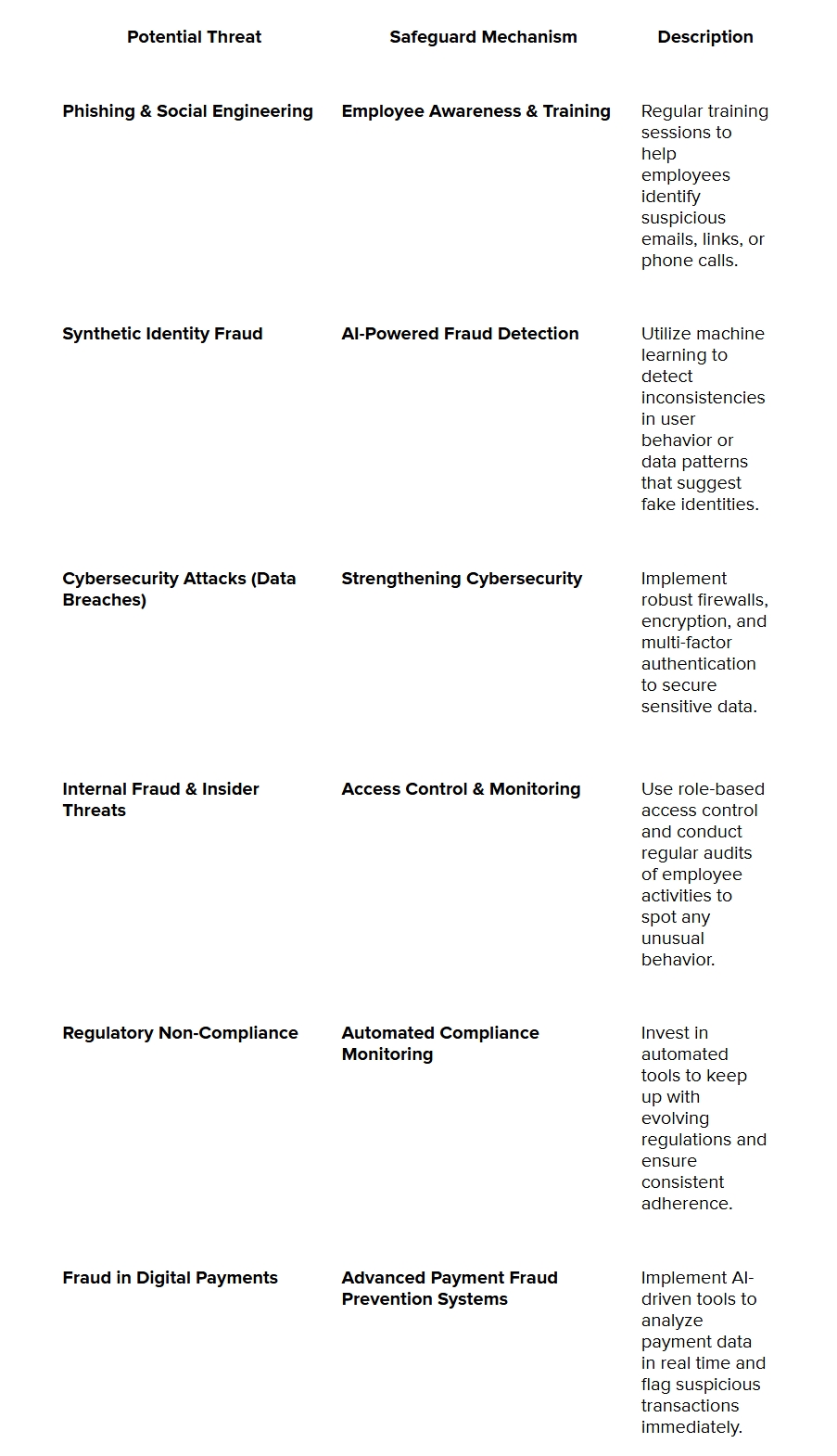

Safeguarding Against Emerging Threats

As fraud tactics continue to evolve, businesses need to implement proactive measures to mitigate these risks. Whether it's through the rise of cybercrime, social engineering, or new forms of digital fraud, understanding potential threats is key to creating a resilient fraud prevention strategy.

The following table outlines some of the most common fraud threats businesses face today, along with recommended safeguard mechanisms to prevent them.

As we’ve explored, fraud is a constant challenge, and staying ahead of emerging threats requires more than just awareness—it requires actionable solutions. In today’s fast-evolving digital world, businesses need to equip themselves with innovative tools that not only prevent fraud but also ensure compliance across various jurisdictions.

This is where AiPrise steps in. With a robust, AI-powered platform designed to address the most pressing fraud challenges, AiPrise helps businesses with the tools they need to safeguard their operations and protect customer trust.

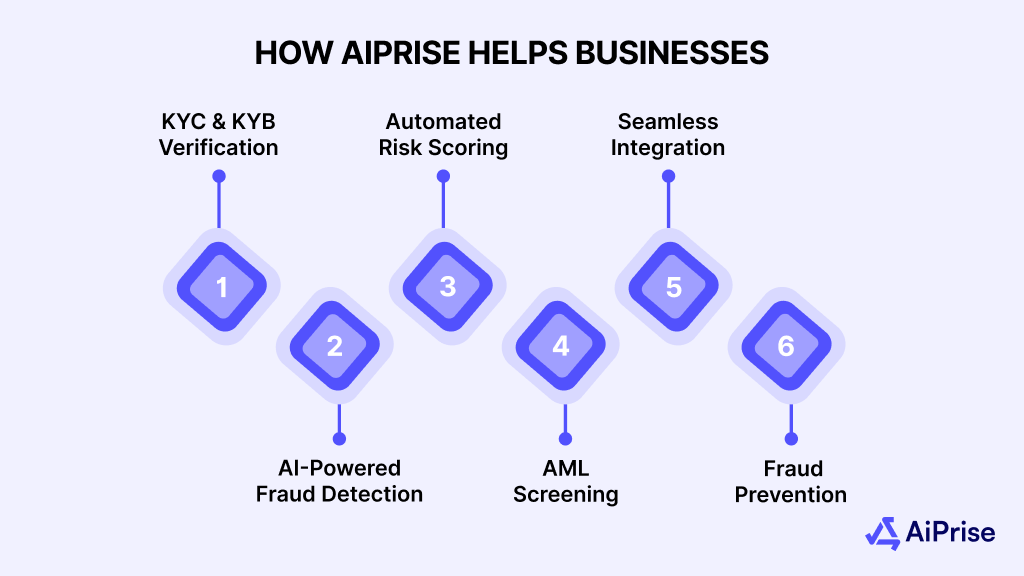

How AiPrise Helps Businesses Safeguard Against Fraud

AiPrise offers a comprehensive, AI-driven solution that helps businesses tackle the growing challenges of fraud prevention, risk management, and regulatory compliance. With its cutting-edge technology, AiPrise empowers businesses to stay ahead of fraudsters while maintaining trust and transparency with their customers.

Here’s how AiPrise supports businesses in safeguarding against fraud and compliance risks:

1. Comprehensive KYC & KYB Verification

AiPrise provides seamless Know Your Customer (KYC) and Know Your Business (KYB) verification processes. By verifying the identities of both individuals and companies globally, AiPrise ensures businesses comply with anti-money laundering (AML) regulations and prevent identity fraud before it occurs. This is especially critical as businesses expand into new markets.

- KYC: Ensures the verification of customers' identities with real-time document authentication, facial recognition, and multi-source data verification.

- KYB: Validates businesses and their owners by checking company registration documents, beneficial ownership, and risk assessments.

2. AI-Powered Fraud Detection & Prevention

AiPrise utilizes machine learning and AI algorithms to detect suspicious activities and potential fraud in real-time. The platform analyzes vast amounts of data, identifies patterns, and flags any inconsistencies, such as unusual transaction activities or mismatched information, to minimize risk.

- AI Algorithms: The system constantly learns from past fraud patterns to improve detection accuracy.

- Behavioral Analytics: Monitors user behavior, including login patterns and transaction activities, to identify anomalies.

3. Automated Risk Scoring and Real-Time Monitoring

With AiPrise’s automated risk scoring, businesses can classify customers and transactions based on their risk profile, allowing for targeted due diligence. AiPrise also provides continuous monitoring to track changes in risk over time, ensuring businesses stay compliant with ever-evolving regulations.

- Dynamic Risk Scoring: Customizable risk rules to score customers based on their activities, location, and behavior.

- Continuous Monitoring: AiPrise’s platform provides 24/7 monitoring of all transactions and behaviors, ensuring you never miss a red flag.

4. AML Screening and Global Compliance

AiPrise helps businesses comply with global AML regulations by screening transactions against the most up-to-date global sanctions and politically exposed persons (PEP) lists. This ensures that businesses don’t engage in transactions that could lead to legal or reputational risks.

- Sanctions & PEP Screening: Cross-checks all customers and transactions against international watchlists.

- Regulatory Updates: Ensures businesses are always compliant with the latest global regulations.

5. Seamless Integration with Existing Systems

AiPrise’s solutions are designed to integrate seamlessly with your existing business systems and workflows. Whether you're in the financial services, fintech, e-commerce, or gaming industries, AiPrise’s flexible platform adapts to your specific needs.

- API Integrations: AiPrise offers robust APIs that integrate directly with your CRM, payment processing, and other backend systems for a smooth experience.

- Customizable Workflows: Tailor the platform to your business model and compliance requirements.

6. Fraud Prevention in Real Time

AiPrise’s fraud detection tools provide real-time alerts for suspicious activities, such as account takeovers or unauthorized access attempts. The system’s ability to act instantly ensures that fraudsters are stopped before they can cause significant harm.

- Instant Alerts: AiPrise’s platform triggers real-time alerts for suspicious activity, enabling businesses to take immediate action.

- Advanced Analytics: Detects patterns in fraud behavior across various industries, enhancing prevention capabilities.

As fraud risks and regulatory challenges continue to grow, AiPrise stands as a trusted partner for businesses, offering the tools and solutions necessary to overcome these complexities.

Conclusion

Fraud prevention and compliance are non-negotiable in today’s business world, especially as industries continue to digitize and expand globally. AiPrise’s innovative solutions help businesses manage the complex challenges of fraud, risk, and compliance while enhancing customer experience.

By adopting AiPrise’s cutting-edge technology, businesses can protect themselves from the rising tide of fraud, reduce the risk of regulatory penalties, and maintain customer trust in an increasingly challenging environment.

If you're looking to safeguard your business and stay ahead of emerging threats, AiPrise is here to help. Book a Demo to explore how AiPrise can future-proof your business against fraud and compliance risks.

Frequently Asked Questions (FAQs)

What are the biggest fraud scams in history?

Some of the biggest fraud scams in history include the Enron scandal, Bernie Madoff’s Ponzi scheme, the South Sea Bubble, Volkswagen's emissions scandal, the Theranos fraud, the Mt. Gox hack, and the recent FTX collapse. Each of these frauds left a significant impact on industries and economies worldwide.

What was the biggest corporate accounting fraud case in history?

The Enron scandal remains one of the biggest corporate accounting frauds in history. Enron’s executives used deceptive accounting practices, including off-balance-sheet entities and mark-to-market accounting, to inflate the company’s profits and hide its massive debt. This led to the company's bankruptcy in 2001.

Are scams a modern invention?

No, scams have existed for centuries. In ancient times, fraud was often seen in the form of coin forgery, and in the 15th century, Perkin Warbeck’s identity theft case was one of the earliest examples of a major fraud. Over time, fraud schemes have evolved, with modern scams now leveraging technology to deceive people on a much larger scale.

What are the most common online scams?

Common online scams include phishing, identity theft, online shopping fraud, romance scams, and investment frauds. Scammers often use fake websites, emails, or social media to trick people into providing personal information or making payments for goods or services that do not exist.

What is the biggest corporate fraud penalty in the 21st century?

The biggest corporate fraud penalty in the 21st century was likely imposed on BP following the Deepwater Horizon oil spill, which resulted in the company paying over $60 billion in fines, lawsuits, and cleanup costs. However, the Enron scandal and Bernie Madoff's Ponzi scheme also generated enormous penalties and losses in the financial world.

Why is fraud prevention so important?

Fraud prevention is critical for businesses to maintain trust, ensure financial stability, and avoid significant legal and financial repercussions. By implementing robust fraud detection systems and monitoring practices, businesses can protect themselves from financial losses, safeguard customer data, and maintain a positive reputation.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately