AiPrise

12 min read

March 3, 2026

AML Compliance in Zimbabwe Made Simple for Businesses

Key Takeaways

Zimbabwe sits at the crossroads of cash-driven commerce, regional trade, and a growing digital payments sector. While this creates opportunities, it also brings AML compliance into sharp focus.

Between 2019 and 2024, Zimbabwe lost around US $6.15 billion to money laundering, roughly US $1.23 billion per year, showing the real risks businesses face.

Cash-heavy transactions, informal business structures, and cross-border flows make it harder to spot risks early, while regulators expect faster reporting and stronger controls.

In this blog, you’ll explore Zimbabwe’s AML framework, key obligations, potential penalties, and practical ways to manage risk without slowing down your operations.

Key Takeaways:

- AML compliance in Zimbabwe is built on local laws, FIU oversight, and risk-based controls, not generic global checklists.

- Cash-heavy activity, informal business structures, and cross-border flows are the biggest drivers of AML risk.

- Strong programs focus on continuous due diligence, timely goAML reporting, and audit-ready records.

- Penalties extend beyond fines to license restrictions, personal liability, and long-term reputational damage.

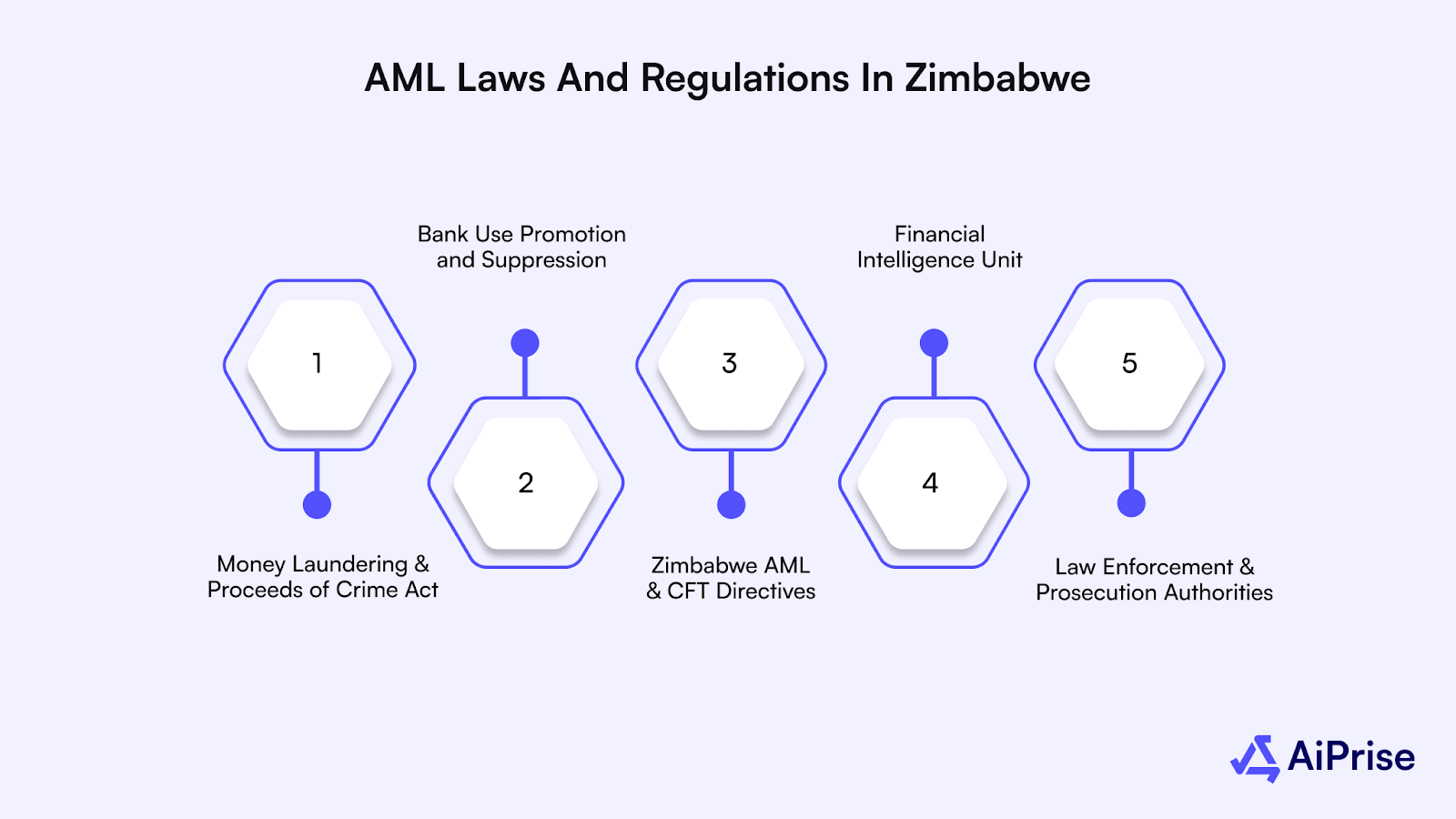

AML Laws and Regulations in Zimbabwe

Zimbabwe tackles financial crime through a clear set of laws, regulators, and enforcement bodies that guide institutions in spotting, managing, and reporting suspicious activity.

If your business operates in Zimbabwe or deals with Zimbabwe-based customers, knowing this framework helps you stay compliant and avoid regulatory trouble.

Below is a simple breakdown to make things easier to follow:

Money Laundering and Proceeds of Crime Act

This is the main law that governs anti-money laundering and counter-terrorist financing in Zimbabwe. It clearly explains what counts as money laundering and what institutions must do to prevent and report it.

Key requirements include:

- Verifying customer and business identities before onboarding

- Monitoring transactions to spot unusual or suspicious behavior

- Reporting suspicious transactions to the Financial Intelligence Unit

- Keeping records that support audits and regulatory checks

- Applying penalties to individuals or institutions involved in laundering activities

Bank Use Promotion and Suppression of Money Laundering Act

This law strengthens the AML framework by encouraging transparent financial activity and limiting misuse of the banking system.

Key requirements include:

- Using formal banking channels for large or significant transactions

- Cutting down the use of anonymous or cash-heavy transactions

- Making it easier to trace funds across the financial system

Reserve Bank of Zimbabwe AML and CFT Directives

Under the Reserve Bank of Zimbabwe Act, the RBZ is empowered to issue AML and CFT directives and supervise regulated institutions. The Reserve Bank of Zimbabwe issues AML and counter-terrorist financing directives for banks and other regulated financial institutions.

Key requirements include:

- Using a risk-based approach when onboarding customers

- Carrying out customer due diligence on an ongoing basis

- Monitoring transactions throughout the customer relationship

- Maintaining strong internal controls, policies, and compliance records

Financial Intelligence Unit

The Financial Intelligence Unit, which operates under the Reserve Bank of Zimbabwe, serves as the central authority for AML reporting.

Key responsibilities include:

- Receiving and reviewing suspicious transaction reports

- Issuing guidance and setting reporting standards

- Sharing intelligence with local and international partners

- Supporting investigations into complex financial crime cases

Law Enforcement and Prosecution Authorities

Zimbabwe’s law enforcement agencies work closely with the FIU to investigate and prosecute financial crime.

Key responsibilities include:

- Investigating money laundering and terrorist financing cases

- Enforcing penalties for AML violations

- Working with regional and international authorities on cross-border cases

Knowing Zimbabwe’s AML laws and regulations makes it easier to understand the key compliance requirements that follow.

Suggested Read: Understanding Anti-Money Laundering Policies and Their Importance

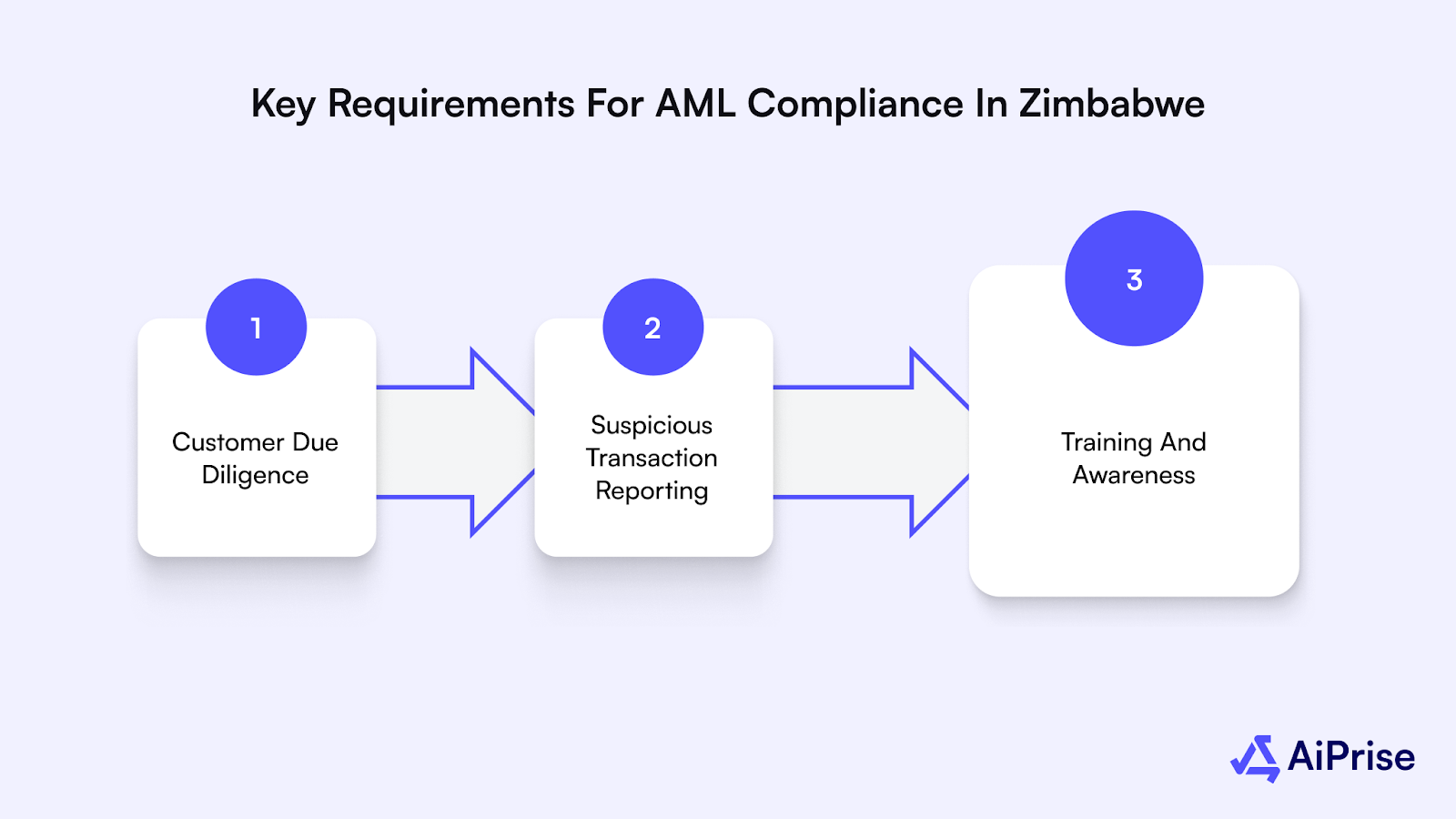

Key Requirements for AML Compliance in Zimbabwe

AML compliance in Zimbabwe focuses on practical controls that help you spot, assess, and report financial crime risks early. The framework is about meeting Zimbabwe-specific requirements set by local laws and regulators, while keeping your operations efficient and workable. Below are the core elements regulators expect you to get right.

Customer Due Diligence

CDD applies at onboarding and continues throughout the customer relationship. It helps you understand who your customer is, how they operate, and how closely you should monitor their activity.

CDD usually includes:

- Verifying individual or business identities using reliable documents and trusted data sources

- Understanding the purpose and nature of the account or business relationship

- Assigning a risk profile based on customer type, industry, location, and expected activity

- Applying enhanced due diligence for politically exposed persons and other higher-risk customers

For higher-risk customers, regulators expect deeper checks. This often includes reviewing the source of funds and understanding ownership or control structures.

Suspicious Transaction Reporting

When you notice activity that appears unusual or lacks a clear lawful purpose, you must review it promptly and report it if concerns persist.

In Zimbabwe:

- You submit suspicious transaction reports to the Financial Intelligence Unit

- You must file reports as soon as possible, and no later than three working days after forming a suspicion

- Reporting happens through the goAML system used by regulated institutions

Common indicators include:

- Transactions that do not match a customer’s known profile

- Sudden changes in transaction behavior without a clear explanation

- Repeated cash or cross-border activity with no obvious economic reason

Training and Awareness

AML controls only work when your teams understand how to apply them in real situations. Regulators expect regular training across all relevant roles.

Training programs should include:

- Practical examples linked to your products and customer base

- Clear internal escalation and reporting steps

- Updates that reflect regulatory changes or emerging risks

- Role-specific red flags for frontline, operations, and compliance teams

Once you understand the key AML compliance requirements in Zimbabwe, it’s important to be aware of the penalties for non-compliance.

Penalties for AML Non-Compliance in Zimbabwe

AML non-compliance in Zimbabwe brings consequences that go far beyond paying fines. Regulators expect strong controls, timely reporting, and clear ownership of AML responsibilities.

When those expectations are not met, enforcement actions can escalate quickly and directly affect your ability to keep operating.

Financial and Criminal Penalties

Zimbabwe’s AML laws allow regulators and courts to impose financial penalties when institutions fail to meet due diligence, monitoring, or reporting requirements.

Key implications include:

- Heavy fines for failing to report suspicious transactions or maintain required controls

- Penalties that grow with repeated issues or widespread control failures

- Criminal liability for individuals involved in deliberate or negligent money laundering, including the risk of imprisonment

These consequences do not apply only to institutions. Directors, senior management, and compliance officers can also be held accountable when responsibility is established.

Regulatory Enforcement and License Impact

When AML weaknesses continue, supervisory authorities can step in with corrective measures.

Possible actions include:

- Orders to fix control gaps within set timelines

- Limits on certain business activities until compliance issues are resolved

- Suspension or cancellation of operating licenses in serious cases

- Closer regulatory oversight and more frequent inspections

For regulated entities, license-related action can stall growth plans and disrupt daily operations.

Reputational and Operational Consequences

AML violations often become visible beyond regulators, especially when enforcement actions are made public.

Common impacts include:

- Loss of trust among customers, business partners, and correspondent banks

- Tougher onboarding and review processes due to increased scrutiny

- Termination of relationships with international financial institutions

- Slower entry into new markets because of higher perceived risk

Once trust is damaged, rebuilding it usually takes time and significant effort.

Knowing the penalties for AML non-compliance underscores the importance of addressing the common compliance challenges in Zimbabwe.

Also Read: 6th Anti Money Laundering Directive: Key Changes and Compliance

Common Challenges with AML Compliance in Zimbabwe

Even with a clear legal framework in place, AML compliance in Zimbabwe comes with real, day-to-day challenges. These issues often sit where regulation, infrastructure, and market realities overlap, and they can slow operations while increasing risk.

Below are some of the challenges institutions commonly deal with.

- Cash-Heavy Economic Activity: Large parts of the economy still depend on cash. This makes it harder to track transactions, build reliable audit trails, and spot suspicious behavior early.

- Limited Availability of Reliable Identity Data: Access to accurate and up-to-date identity and business records is not always consistent. When data gaps exist, customer verification takes longer, and teams rely more on manual checks.

- Cross-Border Transaction Exposure: Zimbabwe’s financial system is closely connected to regional and international markets. Cross-border transactions add complexity and increase exposure to higher-risk jurisdictions.

- Operational Strain on Compliance Teams: Compliance teams often handle large workloads with limited automation. Manual reviews slow down onboarding and raise the chances of inconsistent decisions.

- Changing Regulatory Expectations: Regulatory guidance and enforcement priorities continue to change. Keeping policies, procedures, and staff training aligned with these updates requires ongoing effort.

- Technology Gaps Across Institutions: Not all institutions have access to advanced monitoring or risk detection tools. This leads to uneven AML maturity across the market and increases overall system risk.

Finding it hard to keep up with Zimbabwe’s complex AML requirements and a growing number of false positives? AiPrise lets you spot real risks faster, simplify KYC/KYB checks, and stay compliant, all without slowing down your operations.

Recognizing the common AML compliance challenges in Zimbabwe makes it easier to adopt best practices that keep businesses compliant and secure.

AML Best Practices for Businesses in Zimbabwe

To manage AML risk in Zimbabwe, your controls need to match local realities. Cash-heavy operations, informal business setups, and cross-border exposure all call for a practical, flexible approach. These best practices help you stay compliant without slowing down your operations.

Build an AML Program Grounded in Local Risk

A strong AML program starts with understanding how your customers actually transact and where risk builds up in your business. Generic frameworks often miss risks associated with informal trade and regional capital flows.

Best practices include:

- Assess customer types, industries, and transaction corridors that are specific to Zimbabwe

- Clearly document why customers fall into low, medium, or high-risk categories

- Review and update your AML framework when products, volumes, or geographies change

Tip: Pay close attention to how cash usage, informal business activity, and unclear ownership affect your risk.

Strengthen Verification for Businesses and Ownership Structures

Unclear or layered ownership is a common challenge. When you cannot see who controls a business, AML controls weaken fast.

Best practices include:

- Apply deeper checks when ownership or control is unclear

- Confirm beneficial ownership using more than one source where possible

- Revisit ownership details when a business’s activity changes in a meaningful way

Tip: Treat unclear ownership as a risk signal that calls for closer monitoring, not as a reason to delay decisions.

Use Risk-Based Monitoring to Manage Transaction Complexity

Cross-border transfers and changing transaction patterns add pressure to AML teams. Monitoring everything the same way spreads your resources too thin.

Best practices include:

- Focus monitoring on higher-risk corridors and transaction types

- Adjust thresholds based on customer risk levels and expected behavior

- Review alert quality regularly to cut down noise and missed risks

Tip: Set monitoring rules based on real transaction patterns seen in Zimbabwe, not assumptions borrowed from other markets.

Invest in Continuous Staff Awareness

AML controls depend on people as much as systems. Frontline teams often notice warning signs before automated tools do.

Best practices include:

- Train staff on local red flags tied to cash use, informal trade, and cross-border activity

- Keep reporting steps simple and easy to follow

- Update training regularly as risks and regulatory expectations change

Tip: Short, scenario-based sessions tend to work better than long, policy-heavy training.

Maintain Audit-Ready Records at All Times

Record-keeping is a constant focus for regulators. Delays or missing information during inspections increase the risk of enforcement.

Best practices include:

- Keep verification, monitoring, and reporting records in one place

- Make sure records are easy to retrieve when requested

- Clearly document decisions, especially when judgment plays a role

Tip: If you cannot explain a decision clearly during an inspection, regulators are likely to question it.

Once businesses understand AML best practices in Zimbabwe, a clear compliance checklist can help financial institutions implement them effectively.

AML Compliance Checklist for Financial Institutions in Zimbabwe

You can use this table to step back and review how well your AML controls line up with Zimbabwe’s regulatory requirements and real-world operating conditions.

It gives you a quick way to spot weaknesses early and address them before they create larger compliance issues.

Must Read: Anti Money Laundering and Procurement Risk in Insurance Sector

How AiPrise Simplifies AML Compliance in Zimbabwe?

Strong AML compliance in Zimbabwe goes beyond ticking regulatory boxes. You need clear, timely visibility into customer and business activity, consistent risk assessments, and processes that are always ready for audit review.

AiPrise brings these pieces together into a single platform, helping you meet AML requirements while keeping day-to-day operations running smoothly.

Core features that support AML compliance in Zimbabwe:

- Global KYC and KYB Coverage: Verify individuals and businesses across multiple jurisdictions, supporting various document types and ownership structures. This helps lower onboarding risk while meeting both local and cross-border AML expectations.

- Government Verifications: Confirm identity and business details using reliable government and registry sources. Keep clear verification records that support audits and regulatory inspections.

- Risk-Based Decisioning: Apply configurable risk rules and scoring models that account for Zimbabwe-specific risks, including cash-intensive activities and cross-border transactions. This helps you focus monitoring efforts where risk is highest.

- Watchlist Screening: Screen customers and businesses against global and regional watchlists to flag higher-risk relationships early. This helps teams focus on alerts that matter and reduces time spent on low-risk matches.

- Fraud and Transaction Risk Insights: Strengthen AML controls with behavioral, device, and transaction signals that help surface unusual activity earlier in the customer lifecycle.

- Compliance Co-Pilot: Use AI-assisted tools to support enhanced due diligence, document reviews, and faster case handling. Improve consistency in compliance decisions while reducing manual effort.

With AiPrise, managing AML compliance in Zimbabwe becomes simpler and more consistent across teams. You gain stronger controls, better visibility, and the confidence to grow your operations without increasing compliance risk.

Final Thoughts

AML compliance in Zimbabwe is a measure of the resilience and trustworthiness of your operations. Institutions that treat AML as a dynamic system, one that adapts to customer behavior, changing transactions, and regional risks, are better equipped to handle regulatory scrutiny and market fluctuations.

What’s often overlooked is the long-term benefit. Clear risk ownership, consistent decision-making, and centralized oversight help reduce friction between compliance, operations, and growth teams.

AiPrise helps you achieve this by combining verification, risk assessment, monitoring, and audit-ready processes into a single, connected workflow. Instead of managing AML as a reactive task, you get a clearer, more controlled way to handle risk throughout the entire customer lifecycle.

Book A demo to see how AiPrise can help build a more resilient and scalable AML program for your Zimbabwe operations.

FAQs

Q1. Does AML compliance apply to non-financial businesses in Zimbabwe?

A1. Yes, some non-financial businesses also fall under AML rules, especially if they deal with large transactions or operate in higher-risk sectors. This includes areas like real estate, precious metals, and high-value goods, where the risk of money laundering is higher.

Q2. Can AML obligations differ based on transaction size in Zimbabwe?

A2. Yes, transaction size often determines the level of scrutiny required. Larger or unusual transactions usually trigger closer monitoring and may need extra review or reporting, depending on the risk involved.

Q3. Is AML compliance required for one-time transactions with Zimbabwe-based customers?

A3. In certain situations, yes, AML compliance is needed for one-time transactions with Zimbabwe-based customers. Even one-off or occasional transactions can require identity checks and monitoring if they cross risk thresholds or show suspicious signs.

Q4. How often should AML policies be reviewed in Zimbabwe?

A4. You should review AML policies regularly and update them when regulations change, new products are introduced, or customer risk profiles shift. Waiting until an audit to make updates can increase your compliance risk.

Q5. What happens if suspicious activity turns out to be legitimate after review?

A5. If a proper review shows the activity is legitimate, keeping clear documentation of that decision is usually enough. Regulators care more about whether you followed the right review and reporting steps than whether every alert leads to enforcement action.

You might want to read these...

.png)

.png)

.png)

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately