AiPrise

12 min read

December 15, 2025

AML Insights: Key Trends Shaping Financial Crime Risk in 2026

Key Takeaways

Anti-money laundering (AML) compliance remains one of the most closely examined areas in financial services, especially as regulators increase scrutiny across banks, fintechs, and payment platforms.

With the UNODC estimating that 2-5% of global GDP is laundered each year, the scale of financial crime continues to grow faster than many institutions can respond. Recent enforcement actions show how reactive AML programs expose firms to regulatory penalties, customer-onboarding restrictions, and reputational damage that can take years to repair.

This blog breaks down the key AML insights shaping financial crime risk in 2026, including emerging typologies, technology shifts, regulatory expectations, and how banks and fintechs can strengthen detection, monitoring, and overall AML resilience.

Key Takeaways

- AML programs must evolve in 2026 to address AI fraud, crypto risks, and cyber-enabled laundering effectively.

- Proactive, risk-based AML strategies reduce regulatory fines, reputational damage, and operational disruptions.

- FinCEN and DOJ prioritize outcome-focused compliance, requiring measurable effectiveness over checklist adherence.

- Real-time monitoring, behavioral analytics, and AI-powered risk scoring help detect emerging threats faster.

- AiPrise enables institutions to operationalize AML insights with unified risk scoring, behavioral analytics, and real-time monitoring.

Why Financial Institutions Need Proactive AML in 2026

Responding only after regulators intervene is often far more expensive than maintaining strong controls from the start. When an investigation uncovers gaps in customer due diligence, monitoring, or escalation processes, financial institutions are required to implement corrective action, sometimes under strict timelines.

This may include exiting high-risk relationships, rewriting AML policies, upgrading monitoring systems, or retraining staff across multiple business units. A reactive posture also exposes institutions to significant financial and reputational damage.

In recent years, several global banks have paid hundreds of millions of dollars in penalties for AML deficiencies. Beyond fines, enforcement actions frequently lead to years of remediation work and intrusive regulatory oversight.

In severe cases, regulators have temporarily restricted banks from onboarding new customers in specific segments or regions, directly impacting growth.

Key consequences of a reactive AML approach include:

- Costly remediation programs: Re-reviewing accounts, enhancing monitoring rules, and deploying new technology can consume substantial budget and internal resources.

- Lost revenue opportunities: Restrictions on onboarding or servicing customers hinder market expansion and long-term competitiveness.

- Reputational erosion: Public enforcement actions damage trust with customers, investors, and partner institutions.

- Operational strain: Large-scale process fixes and staff retraining can disrupt daily operations and divert teams from strategic initiatives.

In short, reactive AML is never cheaper, it simply delays the cost until the risk has already materialized.

Suggested Read: How to Spot a Fake Identity: A Guide to Combating Synthetic Fraud

Strengthen your AML program with the adaptive Fraud and Risk Scoring solution. Detect emerging financial crime risks faster, reduce false positives, and gain real-time insights to stay ahead in 2026.

Top AML Insights Shaping Financial Crime Risk in 2026

AML risks are shifting rapidly as criminals combine classic laundering techniques with AI-driven fraud, cyberattacks, crypto obfuscation tools, and high-velocity digital transactions.

For U.S. banks, fintechs, broker-dealers, and payment platforms, understanding these trends is essential to strengthening risk assessments, upgrading controls, and meeting the heightened expectations regulators are setting this year.

Below are the key AML insights shaping financial crime risk in 2026:

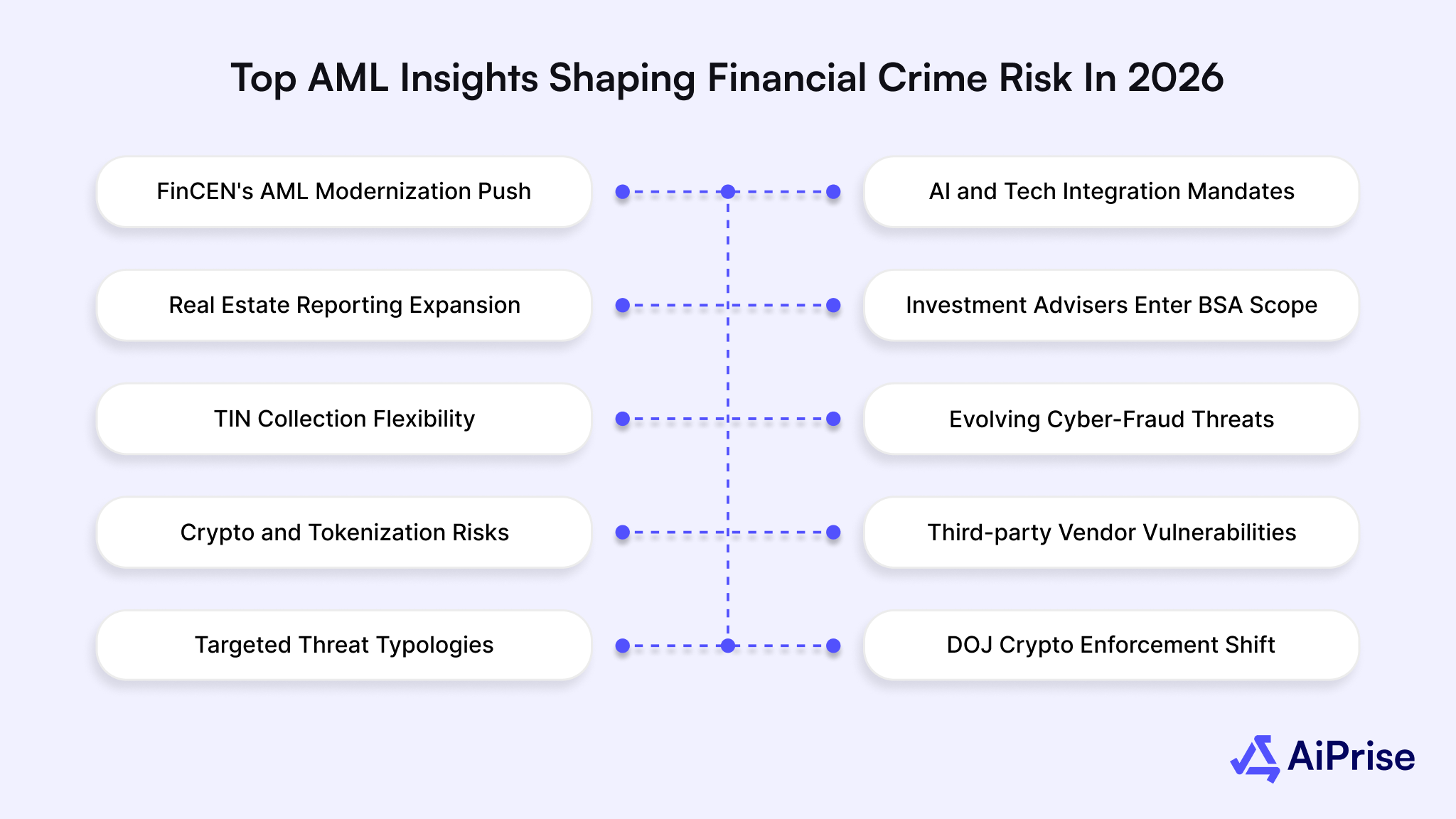

FinCEN's AML Modernization Push

The US Financial Crimes Enforcement Network (FinCEN) continues shifting AML programs away from procedural checklists toward demonstrable risk mitigation.

Under the Anti-Money Laundering Act (AMLA), institutions must design programs that directly support national AML/CFT priorities while producing “highly useful” reporting that assists law enforcement, not just comply with static rulebooks.

What’s New in 2026:

- Outcome-based exams: Examiners now assess whether SARs and controls materially help identify illicit finance, rather than focusing on policy completeness.

- Priority-aligned testing: Institutions must map risks to national priorities such as fentanyl trafficking, kleptocracy, and cybercrime, proving alignment during exams.

- Data-quality expectations: Regulators emphasize accuracy and relevance in AML reporting, pushing banks to improve the usefulness of SAR narratives and transaction monitoring data.

Takeaway: Institutions must shift from “paper programs” to measurable effectiveness. Firms that modernize analytics, restructure risk assessments, and document how data supports investigations will be best positioned for 2026 exams.

AI and Tech Integration Mandates

AI continues evolving from a competitive advantage into an expected component of effective AML monitoring. But regulators stress that AI must be explainable, well-validated, and supervised by humans, not deployed as a black box.

What’s New in 2026:

- Explainability standards: Models must provide transparent reasoning for alerts, allowing investigators and auditors to understand decision drivers.

- Model risk governance: AI used in AML now falls under stricter validation and bias-testing frameworks, including vendor accountability reviews.

- Human accountability: Regulators reiterate that final decisions cannot be fully automated. Staff must remain responsible for escalations and SAR filings.

Takeaway: Firms adopting AI need to balance innovation with governance. The winners in 2026 will pair advanced analytics with disciplined oversight and clear documentation that stands up to supervisory scrutiny.

Real Estate Reporting Expansion

FinCEN’s new rule requires title agents to report all-cash residential purchases by legal entities nationwide, closing a long-abused laundering loophole. This broadens visibility into opaque property transactions, which banks must now incorporate into their due diligence frameworks.

What’s New in 2026:

- Universal geographic coverage: Unlike previous Geographic Targeting Orders, reporting is now nationwide and permanent.

- Entity-focused scrutiny: Any legal entity purchasing residential real estate with cash must report the beneficial owners, raising expectations for banks handling their accounts.

- Risk assessment updates: Banks must reevaluate their exposure to shell companies engaged in property purchases and adjust onboarding questions accordingly.

Takeaway: Financial institutions need refreshed customer-risk models and monitoring rules for clients dealing in real estate, especially high-value cash transactions and entity-based purchases.

Investment Advisers Enter BSA Scope

The Treasury’s proposed rule brings SEC-registered investment advisers and exempt reporting advisers under full AML/BSA requirements.

Although the compliance deadline has been delayed to 2028, the industry must begin building controls now, especially where banks rely on advisers for due diligence.

What’s New in 2026:

- Future KYC alignment: Banks must map where advisers currently perform identity checks and where gaps will emerge under the new rule.

- Transaction-monitoring prep: Advisers must evaluate how they will monitor flows into private funds, hedge funds, or managed portfolios.

- Shared oversight expectations: Regulators expect clear delineation between banks and advisers on who performs which AML functions.

Takeaway: Preparing early prevents compliance gaps. Banks with advisory partners should formalize responsibility matrices and begin integrating shared-risk data before the rule takes effect.

TIN Collection Flexibility

FinCEN’s updated guidance allows banks to verify taxpayer identification numbers using reliable third-party sources before full onboarding. This supports digital account opening while maintaining accuracy standards for identity verification.

What’s New in 2026:

- Pre-onboarding checks: Banks can authenticate TINs earlier in the workflow using approved vendors.

- Remote identity assurance: The rule supports digital banking growth, enabling smoother remote onboarding.

- Risk-based confirmation: Institutions must still validate discrepancies and apply enhanced reviews for high-risk profiles.

Takeaway: The flexibility accelerates digital onboarding but raises expectations for vendor due diligence and ongoing data-quality checks. Banks must strengthen controls around third-party verification workflows.

Evolving Cyber-Fraud Threats

Cyber-enabled financial crime is rising sharply, with criminals using deepfakes, AI-generated identities, and large-scale account-takeover (ATO) operations to bypass traditional controls. Regulators highlight these threats as top AML/CFT risks in 2026.

What’s New in 2026:

- Deepfake-driven fraud: Synthetic voice and video are increasingly used to bypass authentication and conduct social-engineering scams.

- ATO escalation: FINRA notes growing attacks on customer brokerage accounts using credential-stuffing and malware-based harvesting.

- Imposter platforms: Fraudsters mimic legitimate financial brands to lure victims into transferring funds.

Takeaway: Institutions must adapt monitoring models to detect session anomalies, behavioral deviations, and device-based threats, not just transactional red flags.

Crypto and Tokenization Risks

Crypto adoption accelerates, but so do risks around privacy-enhancing technologies, decentralized platforms, and tokenized assets. Regulators expect proactive oversight, accurate disclosures, and timely reporting of suspicious customer activity.

What’s New in 2026:

- Regulator notifications: Firms must notify authorities before launching crypto-related products or changes in custody models.

- Rep activity monitoring: FINRA warns of undisclosed broker participation in crypto projects, which may hide fraud or conflicts.

- Scam-prevention focus: Rising fraud schemes—including pig-butchering, giveaway scams, and unauthorized token launches—drive heightened surveillance expectations.

Takeaway: Banks and fintechs must expand monitoring models to include blockchain behavior, wallet-risk heuristics, mixer-usage indicators, and tokenization flows.

Third-party Vendor Vulnerabilities

Vendor ecosystems have become a major source of AML and cybersecurity risk. Institutions increasingly depend on external providers for KYC, data enrichment, analytics, and technology operations, creating exposure to breaches and control failures.

What’s New in 2026:

- Fourth-party risk focus: Regulators now expect visibility into vendors’ vendors, especially where data is transmitted or stored.

- Stress-testing data flows: Institutions must test how vendor failures would affect AML monitoring continuity.

- Threat-intelligence sharing: FINRA expands alerts that notify firms about vendor-linked cyber incidents.

Takeaway: Vendor oversight must be continuous, not annual. Banks should adopt real-time performance monitoring, breach-notification rules, and redundancy plans for critical AML functions.

Targeted Threat Typologies

Illicit-finance typologies tied to sanctions evasion, drug trafficking, and terrorist financing remain priority areas for regulators. Recent advisories outline specific patterns that institutions must incorporate into monitoring.

What’s New in 2026:

- Fentanyl flows: $1.4B in fentanyl-related proceeds move through funnel accounts, money mules, and China-linked payment channels.

- Kleptocracy networks: Iranian oil networks rely on layered intermediaries, shadow banking entities, and front companies.

- Terrorist financing: ISIS and other groups increasingly exploit charities and informal value-transfer networks.

Takeaway: Institutions need targeted rules and typology-based analytics, not generic monitoring, to detect specialized laundering patterns more effectively.

DOJ Crypto Enforcement Shift

The Department of Justice is shifting attention from platforms to user-level crimes, increasing pressure on banks and fintechs to detect suspicious crypto activity occurring through customer accounts.

What’s New in 2026:

- Focus on sanctions evasion: Banks must identify customer transfers involving mixers, privacy tokens, or high-risk exchanges.

- Scam tracing: DOJ emphasizes tracing victim funds moving through U.S. banks before entering crypto ecosystems.

- Platform transparency: Institutions handling fiat-to-crypto flows must document controls and report gaps promptly.

Takeaway: Banks must enhance blockchain-integrated monitoring and strengthen SAR narratives involving crypto, as regulators increasingly expect detection of user-driven illicit activity, not just platform-level failures.

Also Read: How AI is Transforming AML Compliance

With a clear understanding of the latest AML insights, let’s look at how financial institutions can incorporate them into their AML strategies.

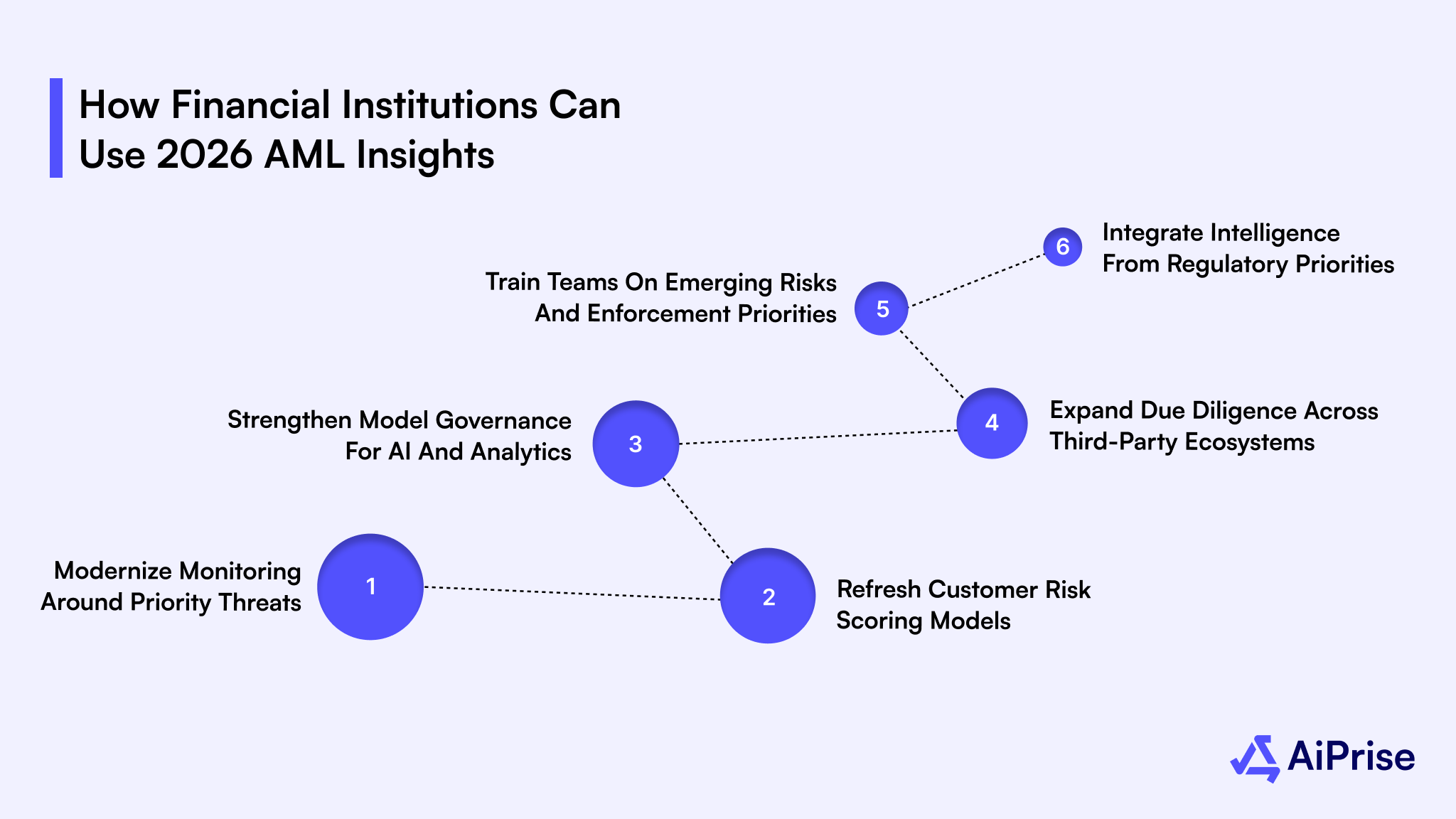

How Financial Institutions Can Use 2026 AML Insights

Identifying emerging AML trends is useful, but the real value comes from turning those insights into practical, measurable improvements across a financial institution’s risk and compliance program.

As threats evolve in 2026, banks, fintechs, lenders, and payment platforms must translate these insights into smarter controls, sharper detection, and more adaptive oversight.

Ways Institutions Can Apply 2026 AML Insights:

- Modernize monitoring around priority threats: Use the year’s top risks, including AI-enabled fraud, sanctions evasion tactics, crypto-linked schemes, and high-velocity transactions, to recalibrate monitoring scenarios. Adjust thresholds, add new typology-aligned rules, and fine-tune alert logic to reflect today’s behaviors rather than legacy patterns.

- Refresh customer risk scoring models: Update KYC/CDD frameworks to incorporate 2026 risk drivers such as deepfake-enabled onboarding, cross-border instant payments, and new high-risk sectors flagged by regulators. Institutions should reevaluate how they classify risk and ensure scoring engines capture new behavioral and device-level signals.

- Strengthen model governance for AI and analytics: With regulators emphasizing explainability and accountability, banks should implement documented governance around AI-driven AML systems. This includes testing for bias, validating model outputs, documenting decision frameworks, and ensuring humans remain accountable for final decisions.

- Expand due diligence across third-party ecosystems: 2026 insights highlight the rise in cyber incidents and compliance gaps originating from vendors, processors, and embedded-finance partners. Institutions should enhance onboarding, monitoring, and contractual oversight for all third parties touching customer data or transactions.

- Train teams on emerging risks and enforcement priorities: Compliance officers, investigators, and frontline staff need updated training on evolving typologies, including fentanyl flows, corporate structuring schemes, crypto obfuscation, new real-estate reporting, and sanctions evasion methods. Awareness improves escalation quality and reduces operational blind spots.

- Integrate intelligence from regulatory priorities: Use insights from FinCEN priorities, OFAC advisories, FINRA reports, and DOJ enforcement trends to guide updates to policies, risk assessments, and investigative playbooks. Institutions that map their controls directly to regulatory priorities demonstrate stronger alignment during exams.

Financial institutions that adapt their AML programs around 2026’s insights, rather than reacting after enforcement actions, gain a major advantage.

By combining modern monitoring tools, sharper risk scoring, stronger third-party oversight, and intelligence-driven decision-making, they can spot illicit behavior earlier, reduce false positives, and meet rising regulatory expectations with confidence.

Also Read: How Banks Utilize Machine Learning For Fraud Detection

Financial institutions, fintechs, and payment platforms need smarter systems that can identify emerging red flags, track high-risk behavior as it develops, and respond to evolving typology patterns in real time.

How AiPrise Strengthens AML Risk Management

Understanding 2026’s evolving AML landscape is only useful if institutions can operationalize those insights. Banks, fintechs, and payment platforms need systems that translate regulatory priorities, emerging typologies, and behavioral red flags into timely, actionable decisions.

AiPrise provides that foundation by unifying identity intelligence, behavioral analytics, and real-time risk scoring across the customer lifecycle.

How AiPrise supports modern AML programs:

- Fraud & Risk Scoring: AiPrise analyzes 100+ risk signals, from transactional behavior and device fingerprints to identity inconsistencies and adverse media, to surface elevated-risk profiles earlier in the customer journey.

- Real-Time Behavioral & Flow Analysis: Continuous monitoring helps institutions identify unusual patterns linked to current typologies, including rapid-movement funds, multi-hop transactions, mule indicators, and cross-channel anomalies.

- Device, Network & Session Intelligence: AiPrise flags suspicious access behavior such as VPN/proxy routing, emulator activity, device switching, or session hijacking, signals that often precede fraud or laundering attempts.

- Configurable Rule Engine & Automated Workflows: Compliance teams can align rules with 2026 AML priorities like national risk themes, sanctions advisories, and typology alerts, while preserving smooth onboarding and legitimate user activity.

By pairing AML insights with dynamic scoring and real-time analytics, AiPrise enables financial institutions to detect threats faster, reduce false positives, and build AML programs that keep pace with emerging risks in 2026.

Book A Demo to see how AiPrise turns AML insights into proactive, high-impact compliance decisions.

Wrapping Up

As financial crime evolves, institutions face increasing pressure to detect suspicious activity, adapt to new regulations, and manage complex risks. Staying ahead requires proactive AML strategies that combine data-driven insights, real-time monitoring, and adaptive risk management.

AiPrise helps institutions harness actionable AML intelligence by integrating behavioral analytics, transaction monitoring, and risk scoring in one platform. By providing early visibility into emerging threats, it enables teams to respond quickly, reduce regulatory exposure, and maintain operational resilience.

Talk to Us Today to see how AiPrise can strengthen your AML insights and support confident, compliant decision-making in 2026.

FAQs

1. What are the key AML trends financial institutions should monitor in 2026?

In 2026, banks must focus on AI-driven fraud detection, crypto transaction monitoring, cyber-enabled laundering, third-party risk exposure, and compliance with updated FinCEN and FATF guidance. Staying ahead of these trends enables proactive risk management.

2. How is AI transforming AML monitoring and reporting in 2026?

AI and machine learning help detect complex patterns, reduce false positives, and provide actionable alerts in real time. Explainable AI models, combined with human oversight, are increasingly expected by regulators for compliance effectiveness.

3. What emerging risks are associated with cryptocurrency transactions?

Crypto-related AML risks include privacy coins, mixer usage, tokenization scams, and cross-border transfers that evade traditional banking controls. Continuous monitoring and blockchain analytics are critical to mitigate these threats.

4. Why is a risk-based AML approach becoming more important?

Regulators now emphasize effectiveness over checklists. Institutions must allocate resources based on customer, product, and geographic risk profiles, focusing on high-risk transactions to prevent money laundering efficiently.

5. How can AML insights help prevent operational and reputational losses?

By analyzing trends, typologies, and transaction anomalies, AML insights enable early detection of suspicious activity, reducing regulatory fines, fraud losses, and reputational damage while ensuring ongoing compliance readiness.

You might want to read these...

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately