AiPrise

July 10, 2026

KYB vs. KYC: Key Differences & How to Stay Compliant

Key Takeaways

There is a lot of compliance jargon to contend with in the financial sector, and acronyms like KYB and KYC can cause confusion. Many teams misunderstand where one process ends and the other begins, resulting in operational overlaps and compliance gaps.

Factors like beneficial ownership and when onboarding requires address verification all factor into how compliance and onboarding procedures develop for neobanks, crypto exchanges, and other regulated companies. While non-compliance can result in fines, the real financial risk lies in the inefficiency of managing these processes in house.

But Know Your Business (KYB) and Know Your Customer (KYC) become easier to understand when you view them through their core purpose. Here is how to know the real differences between the two, and what it means for compliance processes.

Key Takeaways

- KYB and KYC are complementary controls that help organizations assess both customer and business risk.

- KYB typically requires more extensive due diligence than KYC, particularly around ownership and control.

- Compliance teams often struggle with manual reviews, documentation gaps, and complex ownership structures.

- Risk-based workflows, automation, and trusted data sources can improve both compliance and onboarding efficiency.

KYC vs. KYB: Key Differences

The distinction matters because the data sources, verification requirements, risk indicators, and operational challenges differ significantly.

Verification Subject

The primary difference between KYC and KYB is the entity that’s being verified.

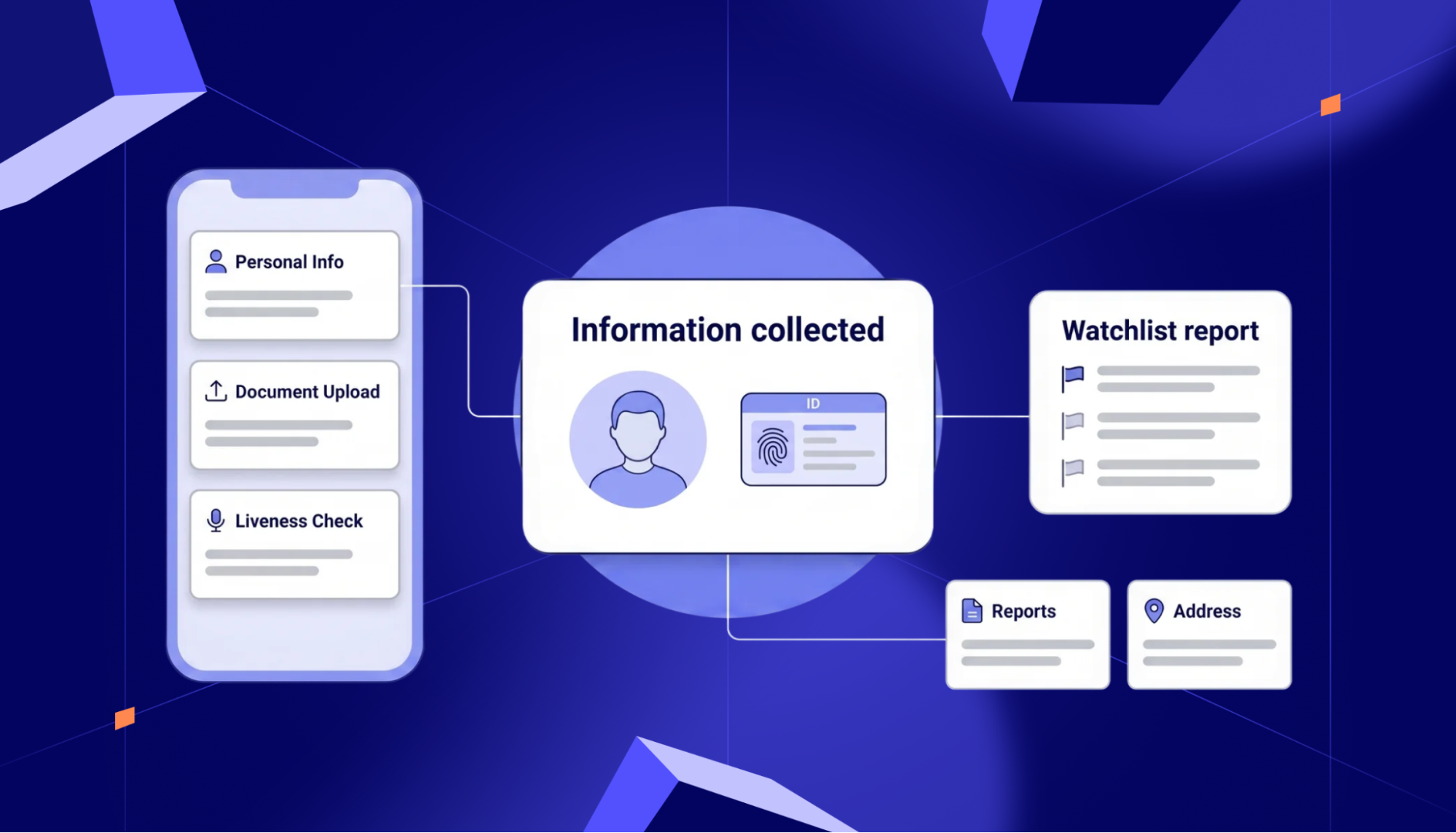

The KYC process focuses on validating the identity of an individual, including customers, account holders, and users. The objective is to assess whether the individual is free from a financial crime or compliance risk.

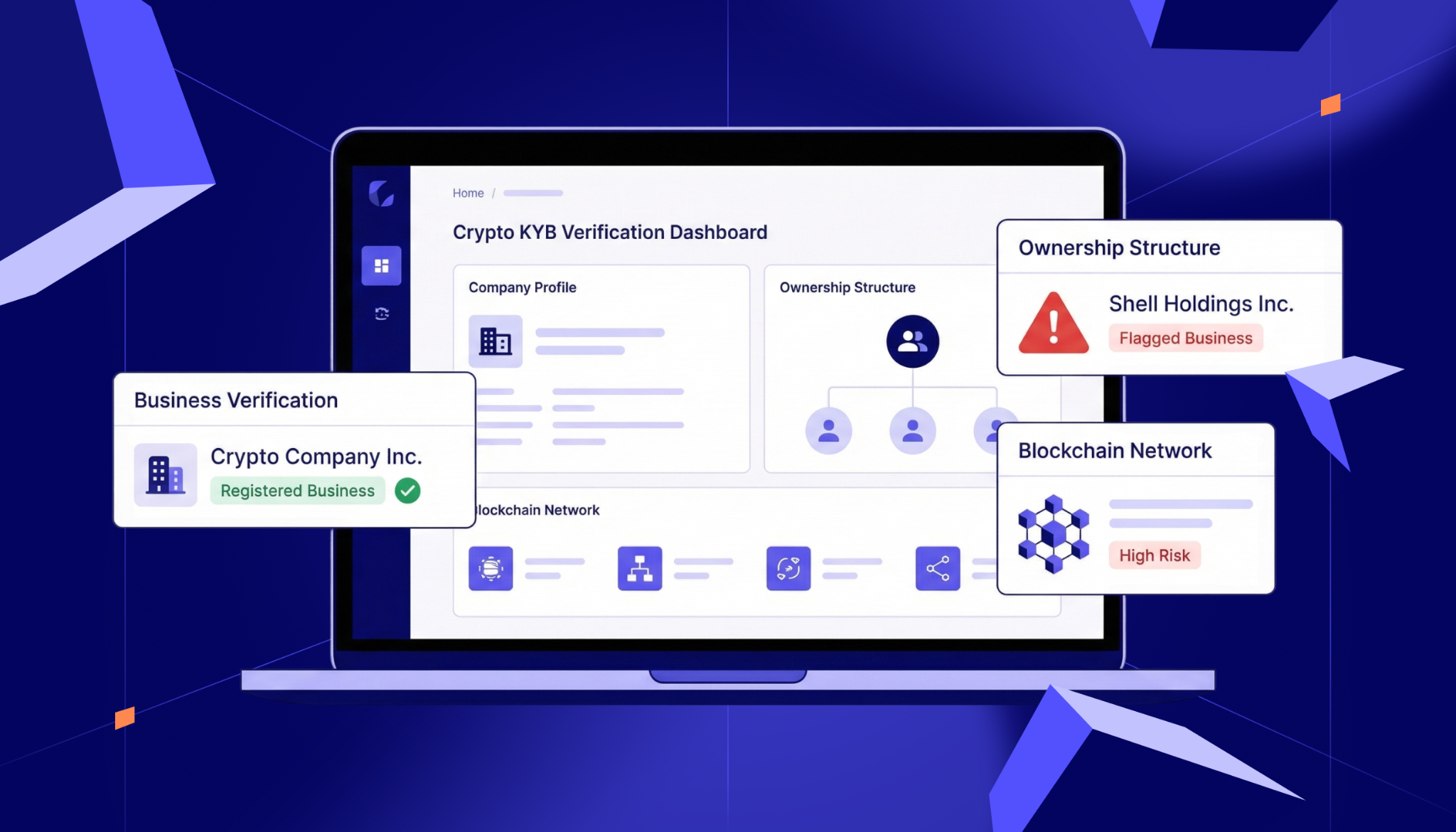

KYB verifies legal entities like corporations, partnerships, and other business structures. In addition to this, it also identifies the people behind these, including directors and business owners.

Information Collected

The type and amount of information required for both are also different.

KYC Information Requirements

For KYC, you need personal information like:

- Full name

- Date of birth

- Residential address

- Government-issued ID

- Contact information

- Nationality or citizenship details

KYB Information Requirements

KYB requires a broader set of data points to establish business legitimacy and ownership.

Common requirements include:

- Legal business name

- Company registration number

- Date of incorporation

- Registered business address

- Tax identification details

- Business activities

- Directors and key executives

- Shareholders

- Ultimate Beneficial Owners (UBOs)

For multinational organizations or complex ownership structures, this process can be significantly more challenging.

Verification Checks

The checks performed during onboarding are another major differentiator.

Typical KYC checks include:

- Identity verification: Confirms the customer is who they claim to be.

- Document verification: Validates government-issued identity documents.

- Address verification: Confirms residential address information.

- Sanctions screening: Checks against global sanctions lists.

- PEP screening: Identifies politically exposed persons.

- Adverse media checks: Reviews negative news and public records.

- Customer risk assessment: Assigns a risk profile based on customer characteristics.

KYB incorporates many of the same compliance controls but applies them at the business level.

Typical KYB checks include:

- Business registration verification: Confirms the company is legally registered and authorized to operate.

- Corporate registry checks: Validates company information against official business registries.

- Company status verification: Confirms the entity is active, compliant, and not dissolved or suspended.

- Director verification: Verifies the identity and legitimacy of company directors and officers.

- UBO identification: Identifies the individuals who ultimately own or control the business.

- Ownership structure analysis: Maps ownership chains and control relationships across entities.

- Sanctions and watchlist screening: Checks the business and associated individuals against sanctions and watchlists.

- Adverse media checks: Identifies negative news, allegations, or reputational concerns linked to the entity.

- Enhanced due diligence reviews: Investigates higher-risk businesses through additional verification and risk assessment procedures.

Unlike KYC, KYB goes beyond verifying a single party and identifies who owns, controls, and influences the organization.

Risk Assessment Factors

Both KYC and KYB support risk-based compliance programs, but the factors are different.

KYC Risk Factors

Organizations typically evaluate:

- Customer location

- Occupation or source of income

- Transaction behavior

- Sanctions exposure

- PEP status

- Source of funds

KYB Risk Factors

KYB assessments generally consider:

- Industry risk

- Geographic exposure

- Business activities

- Ownership complexity

- Beneficial owner risk

- Regulatory history

- Transaction patterns

- Corporate transparency

Common KYB and KYC Challenges

According to the European Banking Authority, 48% of European supervisory authorities identified weaknesses in Customer Due Diligence (CDD) processes in 2024, up from 34% the previous year, while 69% reported high or increasing money laundering risks.

As organizations work to strengthen compliance programs, they often encounter the same set of KYB and KYC challenges throughout the onboarding process.

Manual Documentation Reviews

Many onboarding processes still rely heavily on manual reviews. Compliance teams often need to examine identity documents, business registrations, ownership records, and supporting evidence one file at a time. This can quickly become overwhelming as customer volumes grow.

For example, a payment provider onboarding hundreds of merchants each week may need analysts to review incorporation certificates, shareholder records, and proof of business activities manually. The process is time-consuming and increases the risk of human error.

Incomplete Documentation from Customers

Verification is rarely delayed because of a lack of effort from compliance teams. More often, customers submit incomplete, outdated, or inconsistent information.

A business might upload an expired registration document. Similarly, an individual customer may submit incomplete address information.

Each missing document creates additional follow-up requests, slowing onboarding and increasing operational costs.

Complex Ownership Structures

KYB becomes significantly more challenging when businesses have layered ownership structures. A company may be owned by multiple holding companies, trusts, or entities registered in different jurisdictions.

Identifying the UBOs can require reviewing multiple records and tracing ownership across several entities before the true controllers of the business become clear.

Keeping Up with Regulatory Changes

Compliance requirements rarely stay the same for long. Regulations evolve, new guidance is introduced, and reporting obligations continue to change across jurisdictions.

For organizations operating internationally, this creates an ongoing challenge. A neobank serving customers in multiple markets may need to adapt its verification requirements whenever local regulations change.

Balancing Verification with Customer Experience

Customers expect fast and seamless onboarding. Regulators expect thorough due diligence. Meeting both expectations at the same time is often difficult.

Lengthy verification processes, repeated document requests, and onboarding delays can frustrate legitimate customers. Yet reducing verification steps may increase compliance risks.

Best Practices for Efficient Verification Processes

With 88% of banks prioritizing investment in regulatory compliance and risk management, many organizations are re-evaluating their verification workflows. Here are some best practices that can help strengthen KYB and KYC processes.

Use a Risk-Based Approach

Organizations should focus compliance resources where risk is highest. A locally registered software company with transparent ownership may require standard due diligence, while a crypto business operating across multiple jurisdictions may warrant enhanced review.

Risk-scoring models can help identify higher-risk applicants early by analyzing behavioral signals, business characteristics, ownership structures, and other risk indicators.

AiPrise supports risk-based onboarding through automated fraud and risk scoring, allowing teams to prioritize investigations where they are most needed.

Automate Document Collection and Validation

Manual document reviews can quickly become a bottleneck, particularly for organizations onboarding large numbers of customers or businesses. Automating document collection and validation helps reduce review times, minimize errors, and improve consistency.

Automated KYC/KYB providers can verify information in near real time by extracting data from submitted documents, validating authenticity, and applying predefined compliance rules.

AiPrise supports this process through automated identity verification capabilities that combine document analysis, biometric matching, and liveness checks.

Only Use Trusted Data Sources

Organizations should validate customer and business information against trusted registries, sanctions databases, and watchlists rather than relying solely on self-reported information.

AiPrise combines identity verification, KYB verification, and AML screening capabilities to help organizations verify information against authoritative sources throughout the onboarding process. For example, it connects to over 100 global data sources, including government records, credit bureaus, telecom databases, voter registries, and private datasets.

Ensure Full Audit Trails

Audit trails help organizations demonstrate compliance during regulatory reviews by documenting verification results, risk assessments, screening outcomes, and escalation decisions.

Automated workflows can maintain these records consistently without creating additional administrative burdens.

Create Clear Escalation Path

Potential sanctions matches, adverse media findings, ownership discrepancies, or unusual behavioral patterns often require further investigation.

Establishing clear escalation routes helps ensure higher-risk cases receive appropriate scrutiny while lower-risk applicants continue through onboarding without unnecessary delays.

AiPrise case management simplifies case reviews by routing escalations, assigning reviewers, and tracking decisions.

Regulations That Govern KYB and KYC Compliance

Regulators are actively pulling corporate licenses for weak compliance, with the UK's FCA alone canceling 1,456 firm authorizations in a single year. To keep your operations secure, you need to know exactly which rules dictate your verification processes.

Here are the essential regulations governing global KYC and KYB compliance.

USA

BSA

The Bank Secrecy Act (BSA) is the foundational framework for US anti-money laundering enforcement. Passed in 1970, it requires financial institutions to keep records of cash purchases, file reports on daily cash transactions exceeding $10,000, and flag suspicious activity that might signal money laundering or tax evasion.

FinCEN

Financial Crimes Enforcement Network (FinCEN) is a bureau of the U.S. Department of the Treasury that enforces the BSA. FinCEN reviews transactional data to trace illicit wealth and block criminal access to the financial system.

It also sets the specific regulatory benchmarks that force financial institutions, broker-dealers, and cryptocurrency platforms to run rigorous identity checks and uncover the actual human owners hiding behind complex corporate entities.

EU

AML Directives

The EU has traditionally updated its framework through progressive Anti-Money Laundering Directives (AMLD). Over the years, these directives shifted the focus from simple identity verification to mandatory risk-based assessments.

- 4AMLD & 5AMLD: Introduced and expanded the requirement for member states to launch public beneficial ownership registers, specifically bringing cryptocurrency exchanges into the scope of KYC requirements.

- 6AMLD: Toughened criminal penalties, expanding corporate liability so that companies can be held criminally liable for the compliance failures of their employees.

MiCA

The Markets in Crypto-Assets (MiCA) regulation is the EU's comprehensive framework for digital assets. It forces Crypto-Asset Service Providers (CASPs) to adhere to the same strict KYC and CDD standards as traditional banks.

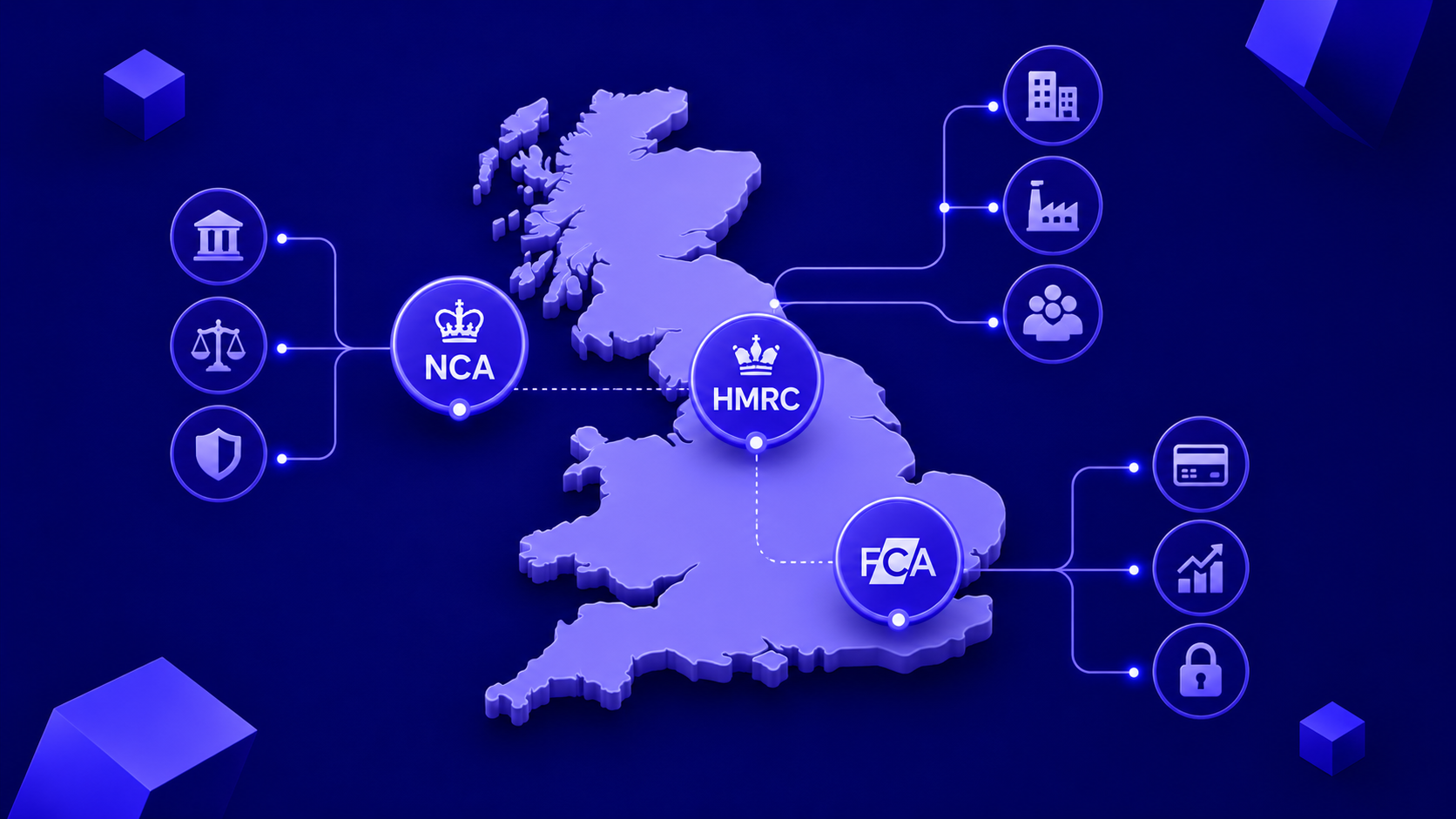

UK

FCA

The Financial Conduct Authority (FCA) is the regulatory body responsible for overseeing the conduct of financial firms in the UK. It supervises businesses to ensure they maintain robust, risk-based KYC and money-laundering controls, holding senior executives personally accountable for systemic compliance failures.

Money Laundering Regulations (MLRs)

The Money Laundering, Terrorist Financing and Transfer of Funds Regulations govern day-to-day KYC and KYB compliance in the UK.

These regulations outline exactly when a business must perform CDD, how to identify UBOs, and when to apply Enhanced Due Diligence (EDD) for high-risk clients or PEPs.

APAC

AUSTRAC

The Australian Transaction Reports and Analysis Centre (AUSTRAC) is Australia's financial intelligence agency and anti-money laundering regulator. It is known for issuing heavy civil penalties to financial institutions that fail to maintain adequate transaction monitoring systems.

MAS

The Monetary Authority of Singapore (MAS) is the central bank and integrated financial regulator of Singapore.

It enforces stringent AML and counter-terrorist financing guidelines, requiring financial firms to use reliable, independent source data, like Singapore's national digital identity system, to conduct digital KYC and thoroughly map corporate ownership networks.

Stay compliant with KYB and KYC

Organizations rarely choose between KYB and KYC. They often need both to build a complete picture of risk. While one focuses on the business relationship and the other on the people connected to it, together they help create stronger onboarding and compliance programs.

For fintechs, payment providers, and crypto exchanges, the challenge is no longer simply meeting regulatory requirements. It is doing so efficiently, consistently, and at scale without creating unnecessary bottlenecks for legitimate customers.

To learn more about modern verification strategies, schedule a demo to see how AiPrise’s automated KYB and KYC workflows can support your onboarding goals.

FAQs

Are KYB and KYC the same?

No. KYC focuses on individual customers, while KYB focuses on businesses and the people who own or control them. Organizations onboarding corporate customers often perform both checks as part of the same compliance process.

Is there a difference between KYC and AML?

Yes. KYC is one part of AML. While KYC helps organizations understand who they are doing business with, AML includes broader controls such as sanctions screening, transaction monitoring, and suspicious activity reporting.

How long does KYB verification typically take?

KYB timelines vary depending on the complexity of the business. A company with a simple ownership structure may be reviewed within a few days, while businesses with multiple entities or cross-border ownership can take several weeks to verify. Also, manual vs automated matters too. Manual checks can take anywhere from 5 to 7 days, but automated checks can take minutes.

How do KYC and KYB apply to crypto exchanges?

Crypto exchanges typically use KYC for individual users and KYB for corporate accounts. Together, these checks help exchanges meet AML obligations and reduce exposure to fraud, sanctions risks, and other financial crimes.

What happens if a customer fails KYC or KYB verification?

A failed verification doesn't mean that the customer isn't trustworthy. It may simply mean that there are missing documents or they require further review. Depending on the case, the organization can request additional information, conduct enhanced due diligence, or delay the onboarding.

You might want to read these...

AiPrise

KYB Compliance: 2026 Regulations You Should Know About

As organizations expand globally and face tighter regulations, adherence to Know Your Business (KYB) standards has become one of the most critical compliance layers for fintech, online marketplaces, and other companies that need to verify business customers before letting them perform financial transactions.

.jpg)

%20Verification%20in%20the%20US.png)

AiPrise

5 min read

How KYB Verification Works in the US: The Ultimate Guide for Navigating Know Your Business

You can approve a new business customer in minutes. Or you can lose them while your team searches through registries, ownership records, and sanctions lists, trying to piece everything together.

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately