AiPrise

5 min read

March 25, 2026

How KYB Verification Works in the US: The Ultimate Guide for Navigating Know Your Business

%20Verification%20in%20the%20US.png)

Key Takeaways

You can approve a new business customer in minutes. Or you can lose them while your team searches through registries, ownership records, and sanctions lists, trying to piece everything together.

In the United States, Know Your Business (KYB) sits at the intersection of growth and compliance. Every new merchant, platform partner, or corporate client requires you to verify legal existence, identify Ultimate Beneficial Owners (UBOs), screen against Office of Foreign Assets Control (OFAC) sanctions, and assess Anti-Money Laundering (AML) risk.

When those checks rely on manual reviews and disconnected data sources, onboarding stretches from minutes to days. Analysts get buried in repetitive work, and qualified customers abandon the process.

How much legitimate business have you lost simply because verification took too long?

That’s why getting KYB right matters now. You need robust verification that doesn’t sacrifice a low-friction onboarding experience for customers. In this blog, you’ll learn how to execute KYB in the US and how to streamline the process with the right technology. This way, you reduce onboarding friction, strengthen AML controls, and scale with confidence.

Key Takeaways

- US KYB verification is fragmented: no centralized registry exists, requiring verification across 50+ state systems.

- Federal AML rules, including FinCEN’s Corporate Transparency Act, heighten scrutiny on ownership transparency and UBO identification.

- Critical data gaps persist: there’s limited public ownership disclosure, restricted BOI access, no real-time EIN verification, and minimal private company financial visibility.

- Effective KYB programs combine multi-source verification, risk-based due diligence, automated screening, and continuous monitoring to stay compliant and scalable.

Why KYB Checks in the United States Matter

In the United States, KYB is your frontline defense against financial crime. Is your current process built for how financial crime actually operates today?

The risk of fraud and money laundering isn’t theoretical. The United States Sentencing Commission reports 1,095 federal money-laundering convictions in 2024, with a median loss of approximately $526,000 per case. Layered LLCs and opaque ownership structures make misuse harder to detect.

If you’re a financial institution or fintech platform, you’re responsible for clearly identifying who you do business with and who ultimately controls those businesses.

KYB verification acts as the layer protecting your business from bad actors. Here’s why a thorough check is so critical:

1. Verifying Business Legitimacy

KYB confirms that an entity legally exists and is authorized to operate by validating registration status, incorporation records, tax identifiers, and active standing in state registries. Without that verification, shell entities and dissolved companies can move through onboarding undetected, creating both regulatory exposure and downstream operational delays.

2. Identifying UBOs and Exposing Hidden Risk

Fraud and money laundering often rely on layered ownership structures designed to obscure control. Effective KYB requires identifying Ultimate Beneficial Owners (UBOs), screening them against OFAC sanctions lists, and flagging potential Politically Exposed Persons (PEPs). When ownership transparency breaks down, risk visibility disappears. This is why US regulators have tightened beneficial ownership requirements in recent years.

3. Strengthening Trust With Regulators and Partners

A robust KYB program signals operational maturity. Regulators expect documented controls and defensible audit trails. Business partners expect protection from exposure to sanctioned or fraudulent entities. Strong KYB frameworks support both.

Now let’s examine the regulatory frameworks shaping KYB expectations in the United States and what compliance teams must verify today.

KYB Regulations in the US

What are regulators expecting today? In the United States, Know Your Business (KYB) processes must align with federal AML and sanctions frameworks.

Regulators Overseeing KYB

KYB obligations are primarily enforced by:

- Financial Crimes Enforcement Network (FinCEN): Administers AML regulations, beneficial ownership rules, and reporting requirements.

- Office of Foreign Assets Control (OFAC): Enforces US sanctions programs and maintains the Specially Designated Nationals (SDN) list.

Regulators expect institutions to verify the legitimacy of entities, identify beneficial owners, and maintain ongoing sanctions screening controls.

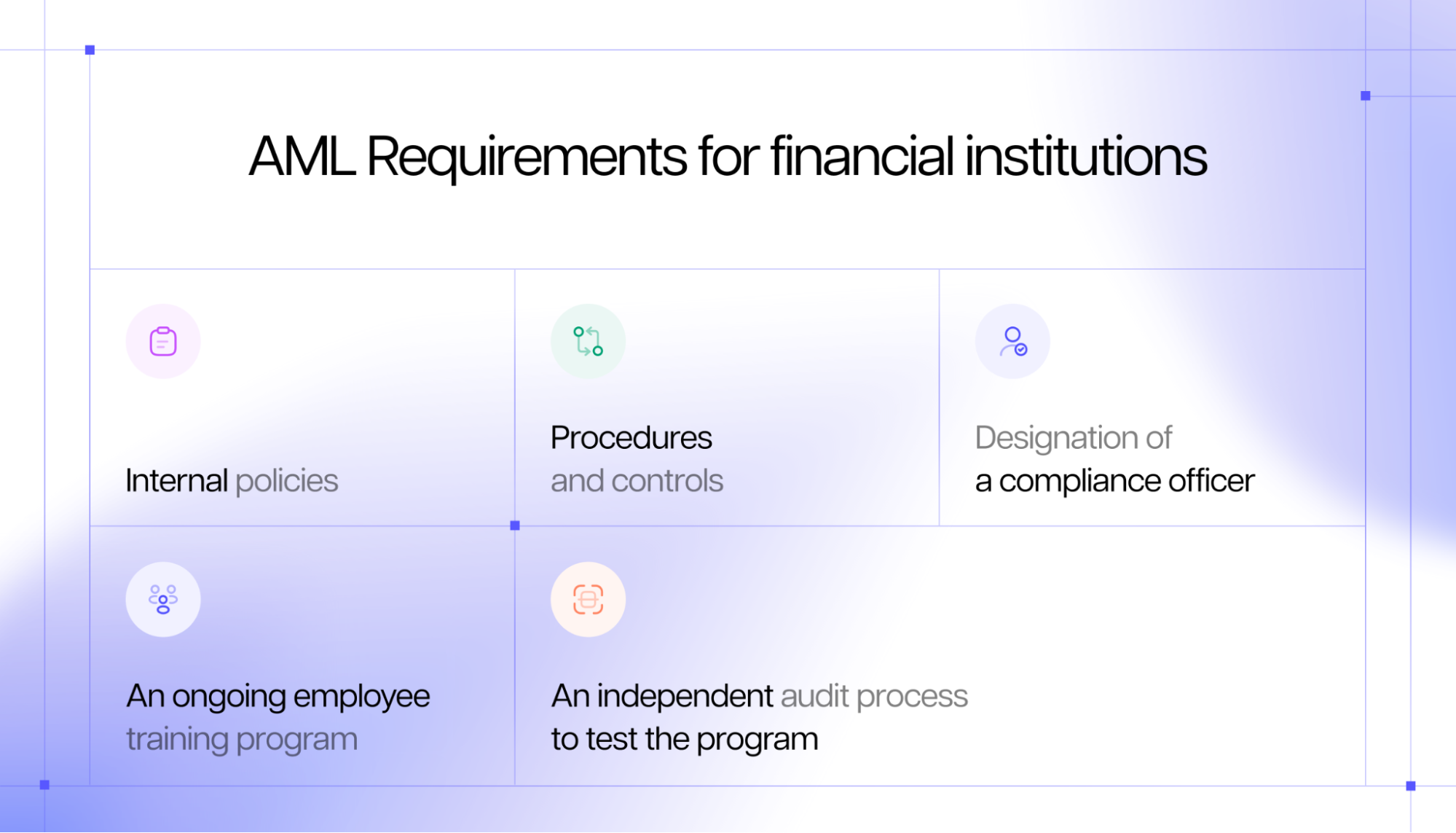

Foundational AML Laws, the Corporate Transparency Act, and Beneficial Ownership Reporting

The modern AML framework is grounded in:

- Bank Secrecy Act (BSA): Requires recordkeeping and suspicious activity reporting.

- USA PATRIOT Act: Expanded customer identification and AML requirements.

The Corporate Transparency Act (CTA) established a federal Beneficial Ownership Information (BOI) database requiring many US entities to report true ownership to FinCEN.

For compliance teams, this elevates expectations around:

- Accurate ultimate beneficial owner (UBO) identification

- Alignment with BOI reporting structures

- Verification of complex control arrangements

Access to the BOI database is restricted, meaning you cannot rely on it as a substitute for direct customer verification. Think of the BOI database as a VIP-only library: the books are there, but you need special permission to access them. So, you still need direct verification from the source.

Staying Ahead of Evolving Risks with Comprehensive KYB Verification

The 2024 National Money Laundering and Terrorist Financing Risk Assessments released by the Department of the Treasury, the biggest money laundering risks today are:

- The misuse of legal entities

- Lack of transportation in real estate transactions

- Lack of AML coverage in some financial sectors

- Complicit merchants and business professionals

- Pockets of weakness in compliance or supervision at some regulated financial institutions in the US

A rigorous KYB verification process can help prevent bad actors from taking advantage of your business, whether it’s a crypto, stablecoin, or payments platform, a marketplace, a neobank, or another financial institution.

On the other hand, non-compliance can lead to serious issues.

Inadequate KYB programs can result in:

- Civil monetary penalties

- Regulatory investigations

- Remediation requirements

- Operational restrictions

- Reputational damage

In many cases, enforcement actions cite not the absence of a program, but the failure to operationalize it consistently.

The US Business Data Landscape: Structural Limits That Impact KYB

KYB in the United States is complex because there is no centralized company registry. Instead, more than 50 separate Secretary of State systems maintain business records, each with its own search tools, disclosure standards, and data formats.

Manual business verification is a lot like trying to find a single puzzle piece across 50 different boxes, each labeled differently and with missing pieces, forcing compliance teams to hunt through multiple sources just to confirm basic entity information. Some provide structured filing histories; others offer minimal visibility. Status labels like “Active” or “Good Standing” aren’t standardized, and API access varies widely, complicating automation.

Ownership transparency is equally limited. Many states do not publicly disclose beneficial owners. Delaware, for example, does not list ownership information in its registry, and several states require only a registered agent for LLC filings, not managers or equity holders.

Even where officers or owners are listed, you won’t necessarily find verification details such as date of birth, ownership percentage, or government ID numbers. As a result, confirming control requires customer disclosures, supporting documentation, and layered screening.

The Corporate Transparency Act’s BOI database strengthens regulatory oversight, but the data isn’t public and cannot serve as a standalone verification tool for private-sector onboarding. EIN verification presents a similar gap: no public database allows real-time confirmation. Unlike the EU or UK, private US companies generally do not publish financial statements, limiting financial transparency during KYB.

These structural realities mean effective KYB verification in the US must operate within fragmented state data, limited ownership disclosure, and restricted financial visibility. If the data itself is incomplete, how do you build a process that’s both fast and defensible?

How the KYB Process Works in the United States: A Step-by-Step Breakdown

Conducting KYB verification in the United States requires more than collecting documents. Unlike some jurisdictions with centralized company registries, the US operates across federal, state, and industry-specific frameworks. That fragmentation creates verification gaps and compliance risk if your process isn’t structured correctly.

Here’s what to include in your Know Your Business process to stay compliant.

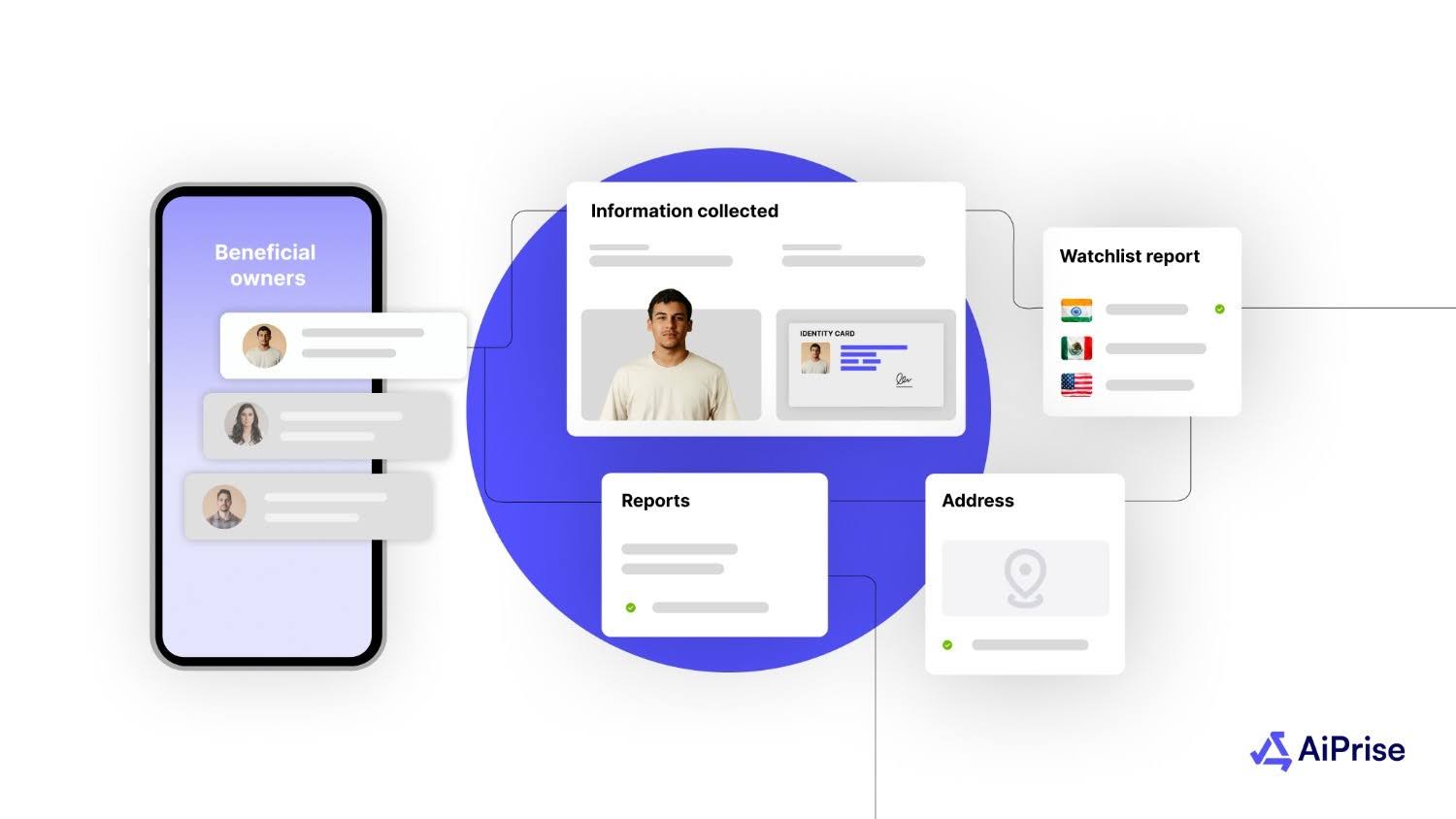

Step 1: Collect Business Information

Start by gathering core entity details, including legal names and “Doing Business As” (DBAs), registered address and state of incorporation, business registration number, EIN, the nature of operations, and ownership structure.

Because US states maintain separate business records with varying conventions and access, standardize data fields in your onboarding flow, validate formatting in real time, and normalize entity names before registry lookups to reduce mismatches. Collect ownership details upfront to avoid re-contacting customers and prevent delays in downstream verification.

Step 2: Verify Business Registration

Once you collect the required information, confirm that the company legally exists and remains in good standing. Check active registration status, review incorporation records, validate filing history where available, and ensure the entity is authorized to operate.

Because the US lacks a centralized company database and each Secretary of State maintains different registries with varying formats and access, cross-reference multiple state sources rather than relying solely on self-submitted documents. Confirm “active” or “good standing” status, flag any discrepancies between declared incorporation and registry records, and document your verification process for audit readiness.

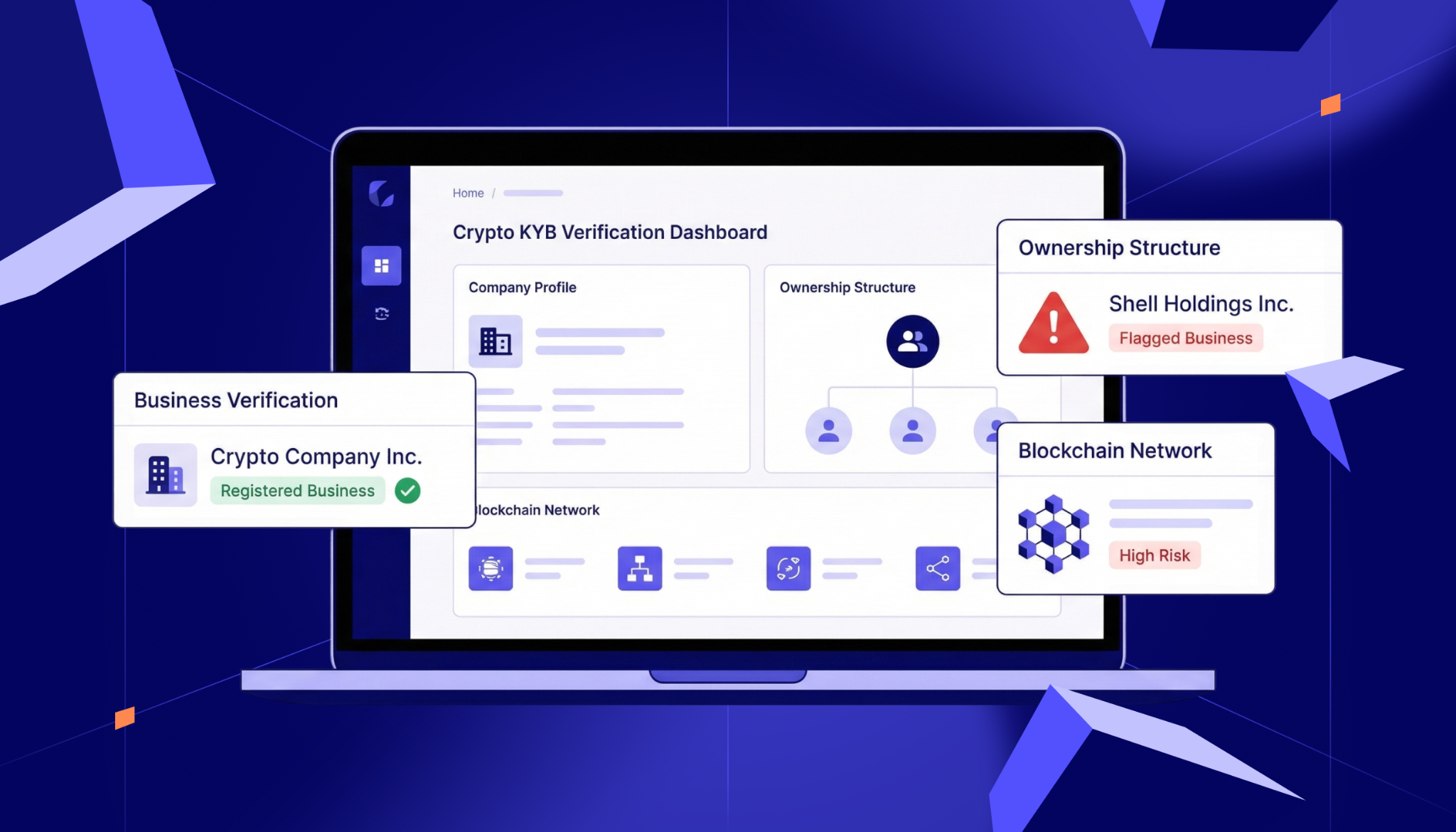

Step 3: Verify Ownership and Control

To comply with KYB, identify Ultimate Beneficial Owners (UBOs) who hold 25% or more ownership or have significant control. In the US, ownership structures are sometimes layered. An LLC registered in Delaware might be owned by another LLC in Nevada, which is in turn held by a trust with multiple beneficiaries. Mapping both direct and indirect ownership in these cases requires collecting supporting documents, attesting to ownership, and understanding the legal entities behind each layer.

Screen the entity and all UBOs against OFAC and PEP lists, and use available Beneficial Ownership Information (BOI) to confirm ownership. For complex or multi-jurisdictional structures, apply enhanced due diligence and document your verification process for audit readiness.

Step 4: Validate EIN and Tax Information

Verify the business’s Employer Identification Number (EIN) to confirm federal tax registration and detect synthetic or misrepresented entities. Check that the EIN format is consistent, cross-check details against submitted tax documents, and look for mismatches between the EIN issuance and entity registration date.

Whenever possible, confirm the business’s EIN using IRS resources, such as the TIN Matching Program for authorized payers, or by reviewing IRS documents the company provides. Use layered verification methods rather than relying on the EIN alone, documenting your approach to strengthen audit defensibility.

Step 5: Check Licensing and Operational Permissions

Confirm that your business customer holds all required state or federal licenses, that they are active, and that their operations match their declared purpose, especially if they operate in regulated industries like healthcare, cannabis, transportation, or money services businesses (MSBs).

Because licensing rules vary by state and some regulators lack searchable databases, verify licenses directly with issuing authorities. Use industry-based risk scoring to prioritize checks and maintain updated regulatory mappings for multi-jurisdiction operations.

Step 6: Ongoing Monitoring and Periodic Rescreening

Continue monitoring after onboarding, including rescreening against updated OFAC sanctions lists, tracking ownership changes, checking state registry status, and recalibrating risk scores as new threats emerge. Ongoing KYB works like a security system: locking the door once is not enough; you need continuous vigilance to detect new risks as they arise.

Because sanctions and registry information can change frequently and ownership transfers may not appear immediately, use automated alerts, schedule periodic checks for high-risk entities, trigger event-based reviews when adverse signals appear, and document all monitoring actions for audit readiness.

Automating US KYB Compliance with AiPrise

Manual KYB in the US breaks down quickly. Fragmented state registries, non-public beneficial ownership data, inconsistent officer disclosures, and the absence of centralized EIN validation create bottlenecks your team has to close manually.

AiPrise supports US (and global) KYB by bringing entity verification, UBO identification, sanctions screening, EIN validation, explainable risk scoring, and continuous monitoring into a single platform and case view, strengthening and automating your KYB workflows.

Instead of stitching together state filings, federal sources, and internal systems, AiPrise coordinates multiple data sources into one continuous control layer. AI-prepared cases surface inconsistencies and hidden risk so analysts can focus on higher-impact decisions.

With AiPrise, you can:

- Reduce onboarding time by up to 80%.

- Prioritize higher-risk profiles and reduce unnecessary manual review.

- Detect shell entities and opaque ownership structures earlier.

- Keep risk assessments current through continuous monitoring.

In an environment defined by structural data gaps and rising enforcement expectations, KYB cannot be a one-time check. It has to be scalable and defensible. AiPrise helps you get there without multiplying vendors or operational complexity.

Ready to Future-Proof Your KYB Strategy?

US KYB requirements aren’t slowing down. As AML rules evolve, ownership transparency expands, and enforcement becomes more visible, you’re expected to maintain clear ownership visibility, consistent sanctions screening, and audit-ready documentation. Manual reviews and disconnected tools might get you by for now, but they become harder to manage as you scale.

KYB verification can’t just be an onboarding checklist. It needs to operate as an ongoing control that helps you validate business identities, detect risks early, and maintain defensible records as you scale.

When you build a scalable, continuously monitored KYB process, you don’t just reduce compliance risk. You create space to grow confidently. As expectations continue to shift, it’s worth asking whether your current workflow is truly built to keep up.

Ready to modernize and automate your KYB process? Book a demo and learn how AiPrise helps you centralize verification and monitor risk without adding complexity.

FAQs

How are AI and machine learning impacting Know Your Business (KYB)?

Artificial intelligence (AI) and Machine Learning (ML) are transforming the KYB landscape by enabling:

- Enhanced Risk Prediction: AI models analyze historical data to predict potential compliance issues.

- Fraud Detection: Machine learning algorithms identify unusual patterns or discrepancies in submitted business data.

- Improved Screening Accuracy: AI helps refine PEP and sanctions screening by reducing false positives.

With these technologies, businesses can overcome traditional KYB challenges such as slow processing times, incomplete records, and errors in verification.

What automation features should you look for in KYB software?

Automation plays a pivotal role in maintaining compliance with KYB regulations. When choosing technology to help you verify businesses at scale, look for these features:

- Automated Risk Scoring: Assigning risk levels to businesses based on their industry, geography, and ownership structure.

- Real-Time Alerts: Notifications for changes in business ownership, legal status, or appearances on sanctions lists.

- Integration with AML Systems: Automated KYB tools often connect seamlessly with Anti-Money Laundering (AML) systems for end-to-end compliance.

How can my company reduce false positives when screening business customers?

Automated screening tools can sometimes generate false positives, flagging legitimate businesses as high risk. This slows down the onboarding process and increases operational overhead. Employing AI-driven tools to refine and contextualize screening results can minimize such errors.

You might want to read these...

AiPrise

KYB Compliance: 2026 Regulations You Should Know About

As organizations expand globally and face tighter regulations, adherence to Know Your Business (KYB) standards has become one of the most critical compliance layers for fintech, online marketplaces, and other companies that need to verify business customers before letting them perform financial transactions.

.jpg)

%20Can%20Improve%20Your%20Compliance%20Strategy.png)

AiPrise

5 min read

How KYB Verification Works in the US: The Ultimate Guide for Navigating Know Your Business

You can approve a new business customer in minutes. Or you can lose them while your team searches through registries, ownership records, and sanctions lists, trying to piece everything together.

AiPrise’s data coverage and AI agents were the deciding factors for us. They’ve made our onboarding 80% faster. It is also a very intuitive platform.

Head of Operations

See your full compliance picture in one place

Use AI agents and global data to review businesses and users faster and more accurately